KOHO offers a reloadable Mastercard and account to make spending and savings easier than ever. But what makes it different from banks that provide the same service? Doesn’t the company just charge its customers hefty fees to inflate its own bottom line?

The answer might not be what you expect. KOHO makes the bulk of its money through premium paid subscriptions and interchange fees – not account or maintenance fees.

To find out more about KOHO and whether it’s right for you, read on for an overview of the company, along with the ins and outs of how does KOHO make money.

What Is KOHO?

KOHO provides a way to simplify your finances with a no-fee spending and savings account. You can add funds to your account, even a direct deposit of your paycheck, and then use your KOHO card to make purchases in person or online.

While it’s similar to using a credit card, a KOHO account is beneficial for these reasons:

- You use your own money. No need to extend credit limits and purchase items you can’t afford. Load the money you need onto your prepaid card, and use it without fear of accumulating bills you can’t pay.

- There’s no interest. Any credit card you apply for, even the most favourable one, will have some interest charge you’ll have to repay. Since KOHO uses your own money and not credit – no interest fees!

You can set up an account in minutes and have money sent to it via direct deposit, e-transfer, or through a linked bank account. Your KOHO Mastercard will arrive shortly after, and you’ll be ready to make purchases or pay bills, all while earning a high rate of interest on your balance and many cashback offers.

But KOHO Charges Fees, Right?

Let’s be honest, most financial institutions charge fees to make money. That is why it’s so hard to find a decent bank account. It takes forever to read through the fine print and make sure there aren’t exorbitant maintenance fees or hidden charges you aren’t expecting.

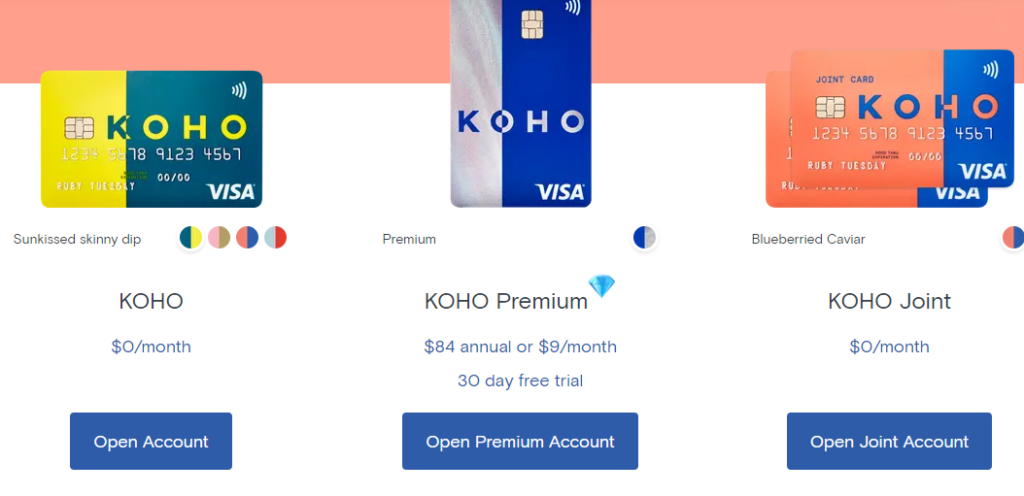

Banks make their money from interest on loans or account fees. Fortunately, KOHO isn’t a bank, so it’s a whole different operating system. Two of KOHO’s three account options (KOHO, KOHO Premium, KOHO Joint) are free to use, with no hidden fees.

This means no e-Transfer, account, NSF, or withdrawal fees. The only time a KOHO user is charged a fee on their free account is if they make an international purchase or use an ATM that charges its own fee.

What Is KOHO’s Premium Paid Subscription?

The only account out of KOHO’s three that charges a fee is its KOHO Premium. The charge is $9/month or $84 annually. With that fee comes added benefits, including 2% cashback on groceries, dining out, and transportation.

In addition, the upgraded account offers price matching and free financial coaching. However, one of the biggest benefits to this account is the waiver of foreign transaction fees. This could be huge if you make frequent purchases in other currencies.

Normally, credit card companies can charge users anywhere from 2%-3% on foreign transaction fees. It’s often overlooked but can quickly add up if you’re a repeat customer. Also, it’s probably not something you think about when you’re planning on opening a credit card.

The regular and joint KOHO accounts both charge a 1.5% foreign conversion fee, unlike KOHO Premium.

While KOHO does partially make its money from Premium subscribers, it is not necessarily the best bet for everyone. KOHO does its part to weigh the pros and cons of its free service versus the paid one. Like anything, the user needs to do their own research and come up with the best bet for their financial well-being.

What Is an Interchange Fee? How Do They Work?

Besides Premium subscription fees, the other way KOHO makes money is through interchange fees. But what is that? Well, it is a transaction fee that gets charged to merchants whenever a customer uses a credit or debit card, including a KOHO prepaid Mastercard.

After each credit or debit card transaction, the merchant must pay a fee to the payment processors or card-issuing financial institutions. These fees allow KOHO to garner a suitable amount of revenue without adding extra costs to their customers, as explained on their website.

KOHO CEO Daniel Eberhard explained how it works in an interview with The Georgia Straight. “Effectively, what Koho has done is we’ve removed enough costs so that we can be profitable off interchange alone.”

He went on to add that he expects to garner more users, especially Millenials. “I think we have a realistic chance to help people pay down debt sooner, get into homes sooner, and just be in a better financial position.”

Are There Other Ways KOHO Makes Money?

The two sources of revenue for KOHO are fees from its Premium subscription and interchange fees. While these bring sufficient cash flows, there is another way that KOHO saves money and passes those savings onto its customers.

KOHO’s entire setup is conducive to savings when compared to traditional banks. KOHO is a digital company, meaning there are no physical locations or branches typical of most banks or financial outlets. This means less overhead and costs. KOHO passes any savings down to the customer by keeping accounts fee-free.

Other KOHO Benefits

With two no fee and one low fee accounts, KOHO offers an affordable way for customers to budget, spend, and save their money. However, there are other benefits to consider.

- High-Interest Rate – KOHO is one of the only prepaid cards that lets you earn interest on your deposits. You can earn 1.20% if you set up a direct deposit.

- Savings Goals – Have a goal in mind? The KOHO app will help you achieve it. Looking for a new car you’d like to buy within a year? KOHO will show you how much you need to save on a daily or weekly basis to achieve your goal.

In addition, KOHO lets you round up your purchases for savings. With every item you purchase, you can elect to round it up to $1, $5, or $10. The added savings will go to a special “Round-Up” section of the app where you can either spend it, save it, or add it to a specific goal.

- Credit Builder – If you have had credit trouble in the past and need help building your score back up, KOHO can help. While other debit and prepaid cards can’t increase your credit score, KOHO does. For $10/month, you can subscribe to Credit Building. From there, KOHO will report your financial habits to one of the major credit bureaus, helping you increase your score in no time.

- Easy to Use App – The KOHO app streamlines all your “banking” needs at the click of a button. From the app, you can set up direct deposit, enroll in Credit Building, manage your bill payment, and transfer money.

- CDIC Insured – KOHO partnered with a federally regulated bank, Peoples Trust, to ensure its customers’ deposits, up to $100,000, are safe should KOHO cease to exist. In addition, the KOHO card is secured under Mastercard’s Zero Liability policy, meaning protection from fraudulent or unauthorized use of your card or account.

- Budgeting Tool – It might not seem like it since you use the KOHO card to make purchases, but it’s actually a great budgeting tool. Unlike credit cards, where you can easily spend more than you can afford, you need to preload money onto your KOHO card, keeping you well within your financial range. That means no more trouble paying your monthly bills or incurring outrageous interest costs.

In addition, you’ll receive balance updates after every purchase, keeping your financial picture and goals in sight. Still, need help? Check out KOHO’s blog for financial advice and money management tips.

Conclusion

With Canadians paying some of the highest banking fees, KOHO came on the scene to offer no-fee spending and savings accounts meant to break the brutal cycle of exorbitant account charges.

In the process, the company also changed the way they make money. Instead of gouging its customers with lofty fees, instead, they make do with subscription costs, interchange fees, and lowering overhead costs to maintain a strong bottom line.

If learning about KOHO piqued your interest, consider reviewing these top virtual credit cards in Canada.