When I was young and watched frightening loan sharks in movies, I always wondered why anyone would borrow from such people, instead of going to the bank. Then I grew up and found out about credit scores.

According to an estimate, about 25% of Canadians have a credit score below 600. Thankfully, loan sharks aren’t the only option for people with poor credit.

There are a lot of lenders that run a completely legitimate business, lending out to people with bad credit histories. LendingMate Canada is one such lender. The company offers small loans to people with bad credit, which makes them a real boon for many borrowers.

But there is a catch; in fact, there are two catches. One: To borrow from LendingMate, you have to have a guarantor backing up your request, willing to step in if you can’t pay back the loan. And two: There is an extremely high-interest rate, reaching 43% per annum in some cases.

If you are in the market for a small loan, I hope this LendingMate review will help you decide whether it’s for you or not.

LendingMate does what is advertised; it provides guarantor loans to people who have difficulty qualifying for a normal loan.

- Issues loans to borrowers with poor or no credit history.

- Unemployed people can also apply for a loan.

- If you have a valid guarantor, the process is simple and efficient.

- They perform a ‘soft credit check of the guarantor’s record.

- There are no hidden or extra processing fees.

- Better rates than a payday loan type of business

- Interest rates are higher than other lenders but within industry standards for subprime loans.

- The guarantor is on the hook for any payments you cannot make.

- The max loan amount is limited to $10,000.

- Only offer loans to borrowers in three provinces.

- The minimum loan duration is two years for loans of $3,000 and up, but you can pay off the loan early with no additional fees and save on interest costs.

What is LendingMate?

LendingMate is a lender that offers small loans to borrowers with bad credit, i.e., people who don’t qualify for loans from banks and other conventional institutions. Currently, it offers loans only to the residents of Ontario, British Colombia, and Quebec. The company markets itself as an “old-fashioned” lender.

Back in the good old days, when statistical analysis of one’s credit history (credit score) wasn’t the prerequisite to qualify for a loan, borrowers needed a guarantor.

These guarantors were people of good reputations and financial standing, and they vouched for the borrowers. And lenders used to issue loans because they knew even if the borrower defaulted, the guarantor would pay them back.

LendingMate uses this old guarantor-backed lending model, in place of the prevalent credit score-based model for issuing loans. It would have been a win-win for the borrower and the company if it wasn’t for the extremely high-interest rates.

But unfortunately, that has become a common practice. Many lenders ask for significantly higher interest rates from borrowers who have a poor credit history. Since such borrowers can’t get a loan at all from most other lenders, companies like LendingMate can capitalize on the need and ask for extravagant interest rates in return.

How does LendingMate work?

One of the things that they have going for them is the ease of loan processing. But that’s highly contingent on the financial standing of your guarantor. Since LendingMate offers guarantor loans, the legitimacy of your guarantor is a major requirement for the approval of your loan.

Ideally, the guarantor should have good credit and be a homeowner. Canadians who aren’t homeowners can also qualify as guarantors, but they have to have a very strong credit history. Homeownership augments a person’s financial position, as it’s a very valuable asset. It’s illiquid but an asset, nevertheless.

As for which currency does LendingMate use to make loans, it’s simple. It’s a local lender and makes all the loans in Canadian Dollars.

If we look at the step-by-step process of getting approved for the loan, it’s relatively very simple.

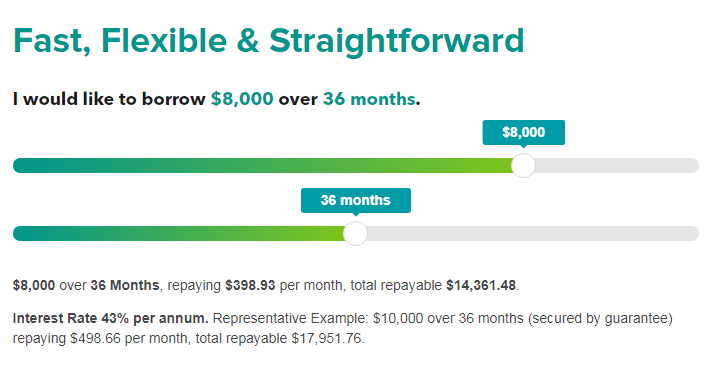

1. Use the loan calculator on the website to figure out how much your monthly repayment will cost you.

It’s relatively straightforward, and there are no hidden costs. Don’t take out a loan if you can’t pay it back.

2. Apply for a loan on the website. Put in the amount and the duration you will pay back the loan in. The longer the duration, the larger your total repayment sum will be. For example, for Ontario residents, a $10,000 loan will come out to about $17,952 in three years. The same loan will cost the borrower $24,458 if they pay it back in five years.

3. After your details, you will receive a link to forward to your guarantor, so they can provide their details for LendingMate to evaluate.

4. After filling in all the details, the guarantor will get a phone call. It will basically be an over-the-call interview. You (the borrower) may receive the call as well, but it doesn’t always happen.

5. Guarantor approval may take some time, but once it’s done, the loan is paid out within 24 hours (as the website claims). Some borrowers have found the time to get the loan issued a bit longer than that.

6. The loan is sent to the guarantor’s account and not the borrowers. It’s done this way to avoid fraud. The guarantor can then transfer the money or hand over the cash to the borrower.

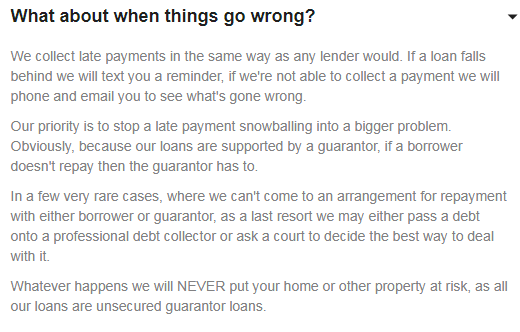

7. The loan repayment is monthly and has to be made by the borrower directly. The company makes a direct debit, and they also collect the debit card details as a backup if the direct debit fails. If the borrower misses paying a month’s installment, they are contacted.

8. If the contact fails, LendingMate contacts the guarantor and asks them to pay back instead. Legal action against the borrowers and guarantors is taken only when they both fail to comply with the repayment schedules. This usually reflects in the borrower and guarantor’s credit history.

LendingMate.ca comes under the parent company, LendingMate Finance Inc.

Is LendingMate Legit?

LendingMate Finance Inc, the parent company of LendingMate.ca, has only been in business for two years, and it’s not BBB accredited. But these two are the only red flags I have found so far, and no news or reviews about any LendingMate scam. LendingMate.ca has a good rating on Trustpilot (4/5).

And even the 1-star reviews were about the process and stringent guarantor requirements, and a few were about repayment mismanagement. But nothing seems off or gives the impression that the company is a scam.

Also, the business model itself is relatively safe. They issue loans based on the guarantee from a financially stable individual, who will have to pay back even if the primary borrower defaults. The amount of the loan itself is relatively safe.

LendingMate Phone Number and Contact

LendingMate primarily operates through its website. The address below isn’t provided on the website.

Address: 180 Dundas St West, Suite 1508

Toronto, Ontario

M5G 1Z8

Phone Number: (855) 360-5597 – Timings: 2pm-9pm, Mon-Fri

You can contact LendingMate using the following emails:

Inquiries: [email protected]

Send Docs: [email protected]

Complaints: [email protected]

Affiliates: [email protected]

Collections: [email protected]

You Should Use LendingMate If:

- Your credit score is too poor to apply for loans at good interest rates.

- A friend or family member can vouch for you and be willing to pay back the loan if you can’t.

- You only need a loan under $10,000.

- You are willing to pay an extravagant interest rate.

- Need a quick loan.

To be fair, if you have someone who is willing to become your co-borrower and share your financial liability for a small loan, it means they trust you and are financially stable. A much smarter choice would be to borrow directly from them.

Don’t Use LendingMate if:

- You can’t pay back the monthly installments promptly and on time.

- You can’t find a financially sound guarantor willing to become your co-borrower.

- Have literally any other option that will require a lower interest rate.

- You are near the good credit bottom line and can bring it up in a short time.

- Have long-term savings that you can borrow from (like an RRSP), with relatively lenient penalties compared to the 43% interest rate.

Conclusion

Entities and businesses like LendingMate are a boon for many people. Despite the stringent guarantor requirements and high interest rates, LendingMate has managed to furnish thousands of loans.

It shows that capitalizing on the financial needs of people with poor credit is a legitimate and highly profitable business. Even if the terms and business model seems evil, it’s a necessary evil of our current financial landscape.

LendingMate provides a last-resort option to many borrowers, and they do it on their own terms.

Lendingmate Review ([currentyear]): Last Resort Loans in Canada

Need a loan but have poor credit in Canada? Check out LendingMate, where you can get a guarantor loan, no matter how your credit is.

Product In-Stock: InStock

2