Have you ever returned a product that you bought from a business in Canada?

If so, you might have received something called a credit memo after completing the return.

If you’re a business owner, you might have seen a credit memo on your bank statements.

If you don’t know what a credit card memo is in Canada or why you got one, you’re not alone. A lot of readers have asked me what it is, and I felt that more people might be wondering about it as well.

In this post, I will give you an overview of what is a credit memo in Canada so that you can understand exactly why you might have received one.

What Exactly Is A Credit Memo?

A credit memo is something that both customers and business owners might find in their bank statements from time to time after a return, exchange, or refund.

Some merchants and financial institutions may also offer a physical copy of the credit memo for customers, similar to a receipt.

Essentially, a credit memo is a negative invoice. It indicates that the customer is owed a credit to their account.

Credit memos may be issued alongside a refund or may be sent before a refund is issued to indicate that an exchange or refund will take place in the future.

Credit memos are often issued when:

- Billing errors were made, resulting in a customer being overcharged

- To apply a promotional discount

- A product was returned

- A customer takes advantage of a money-back guarantee on a product or service

In some cases, the customer may choose to apply the refunded amount towards a new purchase, and the credit memo will indicate this.

When Is A Credit Memo Issued?

If you recently received a credit memo, it’s most likely because you have returned something to a business. Sellers and merchants often send credit memos to their customers after a product has been returned.

When a customer returns an item to a store, the merchant typically refunds the cost directly to the debit card or credit card that was used to purchase the item. Although this transaction typically appears on your statement, the added credit memo can provide added context to help you remember the transaction.

However, in some cases, the merchant may not issue a direct refund.

Instead, the merchant may offer store credit or may offer to exchange one item for another. This can happen if:

- The customer doesn’t have the receipt for the purchase

- The return was made after the end of the store’s return policy

- The customer requested store credit instead of a refund

In this case, the retailer may submit a credit memo to your credit card company to serve as proof of the transaction.

Even though it’s not required, it can make bookkeeping easier and can prevent future disputes with disgruntled customers. Essentially, it’s just an official record that

Is A Credit Memo A Refund?

Many people who have received a credit memo often wonder what the difference between a credit memo and a refund is.

At first glance, a credit memo and a refund might sound like they are the same thing. However, this isn’t always the case.

When you get a refund, the seller simply pays you back the money in cash or issues an electronic refund to your card or bank account.

While a credit memo may be issued alongside a refund, it can also be used to note that a customer has store credit that can be used for a future purchase.

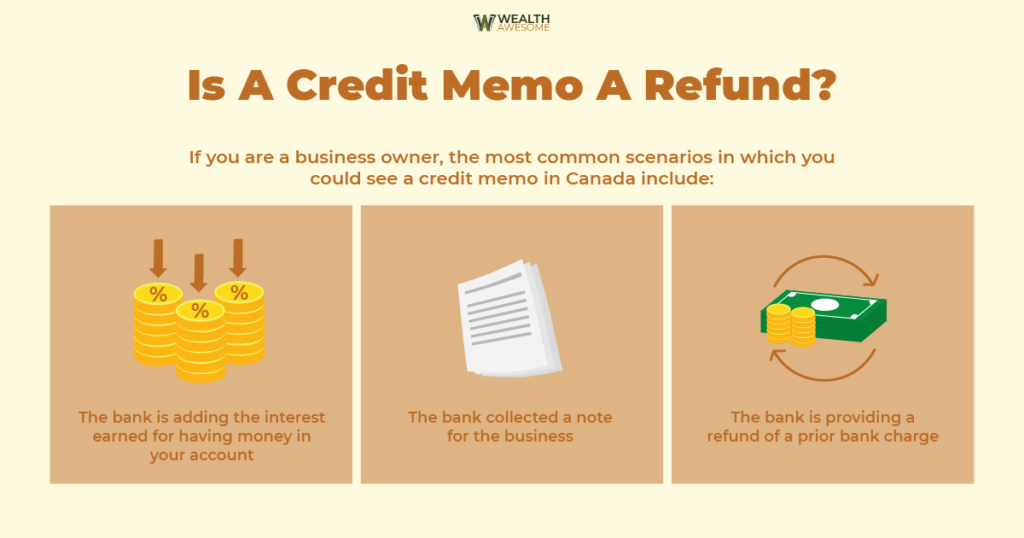

If you are a business owner, the most common scenarios in which you could see a credit memo in Canada include the following:

- The bank is adding the interest earned for having money in your account

- The bank collected a note for the business

- The bank is providing a refund of a prior bank charge

Business owners may also be issued a credit memo from one of their B2B partners.

For example, a convenience store owner may be issued a credit memo from a grocery wholesaler after a package was delivered with broken or spoiled goods. The store owner could then use this credit memo to ensure that a discount is applied to a future order from the grocery wholesaler.

What Is A Debit Memo Charge?

Credit memos are not the only thing you can expect to see.

You may also see a debit memo charge from your seller. Think of debit memos as the opposite of credit memos.

While a credit memo reduces the amount of money that a customer owes during their next purchase with the seller, a debit memo increases the amount that a customer owes the seller the next time they shop at the business.

This can often happen if a business undercharged a customer for a product or service (typically the result of human error or a glitch in the merchant system).

If a business makes the mistake of undercharging an account, the customer might owe extra money. Customers can pay off the amount directly or through a debit memo on their next purchase.

In either case, the debit memo serves as proof of the transaction and keeps both parties accountable.

If you are a business owner, you can expect to see a debit memo in your bank statement if:

- A bank service charge for maintaining your checking account,

- Subtracting the amount for a customer’s check that did not clear the customer’s bank account,

- A bank fee for handling a check that was returned for insufficient funds, or

- A monthly loan payment.

What Is A Bank Credit Memo?

Another type of memo that you may come across in the financial world is a bank credit memo.

Unlike credit memos and debit memos, which indicate that you owe (or are owed) a balance by another business, a bank credit memo is issued by a financial institution to a depositor notifying them that their account balance has increased.

For example, if a client pays an invoice or somebody wires money into your account, your bank or credit union may send you a bank credit memo to let you know that you’ve just received money and that your available balance has increased.

- Related Reading: Best Credit Unions In Canada

What Information Is Found On A Credit Memo?

Businesses often use credit and debit memos to keep track of their inventory and help with bookkeeping.

Most credit memos contain basic information, including:

- Date of the sale

- Items/services sold

- Shipping address

- Customer name

- Original purchase/sale price

- Amendment made to the transaction (debit or credit)

- Method of payment (cash, card, cheque, etc.)

Businesses often process hundreds (in some cases, thousands) of transactions per day. Keeping records of credit and debit memos ensures that they’re able to meet every customer’s needs and keep their business running smoothly.

Conclusion – What Is A Credit Memo In Canada?

Whether you’re a customer or a business, a credit memo is nothing to worry about. It simply serves as proof of a transaction and indicates that you’re owed a credit in the form of a refund, store credit, or an exchange.

Business owners who issue credit memos to customers who return products should take this into account while filing their taxes.

Learn more about the best banks in Canada here.

Thank you for the article!

How long is a small business required to keep a credit memo on file? What would be deemed reasonable?

I would say keep for 7 years, as that is how far back an audit can go.