Trying to find a bank or finance company just got harder. Years ago, choosing a bank came down to proximity and interest rates. But these days, with the advent of online banks and fintech companies, the rules have changed.

That’s where KOHO comes in – changing the game and offering its customers the same safety and convenience features of banks but at a lower cost.

I get asked this a lot: Which bank is Koho?

While KOHO isn’t a bank, the company partnered with the Peoples Trust Company, which is federally regulated, to ensure any funds you deposit are protected by Canada Deposit Insurance Corporation (CDIC).

KOHO is a no-fee alternative to the big banks of Canada. They offer spending and savings accounts, along with access to a prepaid reloadable Mastercard for purchases.

Are you wondering if which bank is KOHO and if it is right for you? Read on to learn more about its features and benefits.

When Was KOHO Formed?

Launched in 2017, Daniel Eberhard formed KOHO to help Canadians improve their finances and stop paying the exorbitant fees associated with banks.

They also partnered with Mastercard to offer a reloadable card. These cards are accepted anywhere Mastercard is, whether in-store or online.

How Does KOHO Work?

KOHO offers three different accounts, two of which are free. After signing up, you can transfer money onto your card either by payroll direct deposit or through an Interac e-Transfer.

Similar to a credit card, any purchases you make will earn you 0.5% cashback rewards. If you sign up to have money direct deposited into your account, you’ll earn additional interest on your entire balance.

KOHO also lets you add to your savings with their RoundUp program. Once enrolled, anytime you make a purchase, you can round it up to the nearest $1, $2, $5, or $10. The difference goes to your savings account.

What Makes KOHO Different?

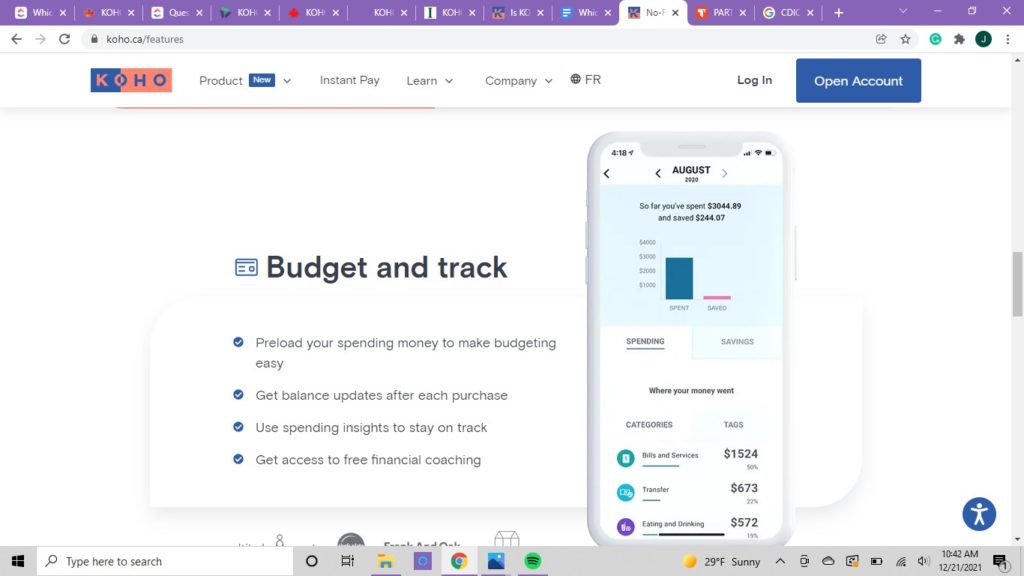

In addition to no monthly fees, one of the biggest benefits of a KOHO account is prioritizing your financial health with budgeting tools and real-time insights into your spending habits. Having this information right at your fingertips helps you consider the consequences of overspending.

In fact, right on their website, KOHO claims that its account holders spend 15% less than they used to and save $500. They attribute this to the company’s design – allowing users to be smarter with their money and taking away the steep fees paid at other big banks.

KOHO keeps users up to date by refreshing their balances after each purchase and comparing your spending habits to others.

KOHO does offer an upgraded Premium account for a fee ($9/month or $84 annually). This account includes 2% cashback on purchases, along with free financial coaching and no foreign transaction fees – a huge benefit if you’re a frequent traveler.

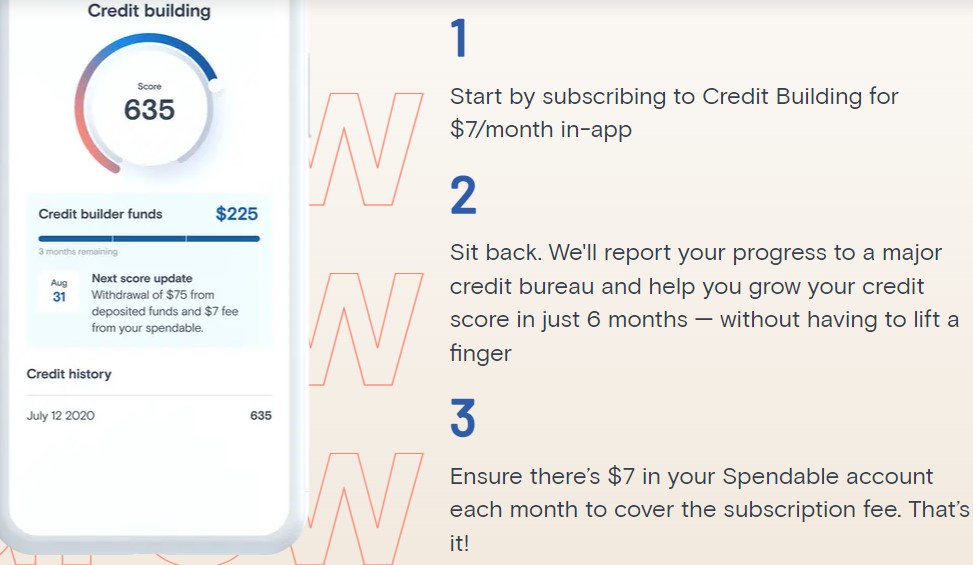

One major difference between KOHO and other debit cards offered by banks is that KOHO helps you build your credit. You can subscribe to KOHO’s credit building program for $7/month, and KOHO will send your financial progress to the major credit bureaus to help you improve your credit score.

Is KOHO Safe?

Canada is well known for the safety and security of its banks, which is why it might be hard to pry some people away from its confines. Just last year, Global Finance announced the safest banks in North America, and the top six are all from Canada.

While Canadian banks enjoy a certain level of security, so does KOHO. They have strong funding sources from multiple investors like Greyhound Capital and the National Bank of Canada.

However, even if KOHO were to go under, their partnership with Peoples Trust ensures the safety of your money.

In addition, the company has even more protocols in place to protect you. There’s its privacy and security policy that states KOHO won’t share your information with anyone other than to verify your identity.

KOHO has other security features like in-app card locking if you think your card is compromised.

The bottom line is that KOHO is as safe and effective as any of its banking counterparts.

Conclusion

While big banks offer Canadians plenty of security, they also charge some of the highest fees around. KOHO was formed to improve its customers’ financial health without charging them unsightly extras.

Today, KOHO rivals banks both with its safety features and its low cost. If you’re looking to find out more about the company, check out this KOHO card review.

My name is Joanne Boniface, i have a Koho visa preload card. i had a large amount put on my card on Feb 27th, and then my card got suspended because Koho is in the middle of changing from visa to master card, in the mean time i can not get acess to my funds, i have text over 50 different people, each saying they can help me, and i still haven got my fund , all them tell me a new card has being sent out, but i was reasonably told that the card that was shipped out on February 27th its now got lost in transit, so now i have to wait another 7 to 10 days, this is my disability cheque and i need my funds, can you help me. my cell number is 306-599-8009, i have ask to speak to someone at koho in person, and have being told the only way is through text, but still haven’t spoke to anyone that can helped me.

I’m sorry to hear about your situation, Joanne. I don’t have access to specific information about your Koho visa preload card or account. However, I suggest you keep following up with Koho’s customer support team and ask for updates on the status of your new card. You can also inquire about any alternative options they may have for accessing your funds, such as a bank transfer or check.

If you continue to experience difficulties in getting the assistance you need, you can try escalating your issue to a higher level of management within Koho or contacting your local consumer protection agency for further guidance.

You can try emailing, or my preferred method, which is through the chat function: https://help.koho.ca/en/articles/6401801-contact-support