CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

If you want to strengthen your portfolio, incorporating alternative investments could be a smart strategy. These assets can help reduce correlation to traditional markets and potentially improve risk-adjusted returns.

The Canada Pension Plan (CPP) invests heavily in alternatives, with over 50% of its asset mix allocated to private equity, real estate, infrastructure, and other alternative assets.

In this guide, we’ll break down the top alternative investments in Canada and help you understand whether they belong in your portfolio.

Advertisement

What is an Alternative Investment?

The easiest way to define an alternative investment is to explain what it isn’t – a traditional investment. Traditional investments include:

-

Publicly-traded stocks (as well as mutual funds and ETFs containing them)

-

Most bonds and fixed income that are available to trade

-

Cash, GICs, high-interest savings accounts

Investments or assets outside of this list fall into the alternative investment category.

We will go through a comprehensive list of alternative investments further below.

Pros and Cons of Alternative Investments

Alternative investments, like all other assets that you can invest in, come with their advantages and disadvantages. Several disadvantages can be avoided based on your characteristics as an investor.

Pros

- Returns are typically uncorrelated to traditional investments

- Ability to potentially access higher risk-adjusted returns than through traditional investments

- Lower volatility in cases where prices do not adjust on a daily basis

Cons

- Investments are much more complicated and less transparent

- Some alternative investments are only available to accredited investors

- Low liquidity

- Some strategies are dependent on a specific portfolio manager or team for results

- Alternative strategies (funds) can come with high fees

It is important to do a lot of careful research before investing in alternative assets or alternative funds.

Best Alternative Investments in Canada

1. Physical Real Estate

-

Professionally Managed: No

-

Liquidity: Low

-

Risk: Medium-to-High

-

Income Potential: Varies

-

Easy to Access: Yes

Physical real estate is one of the most common assets that people own. It refers to physically owning property, which can include:

-

Land

-

Single-Family Property (house)

-

Commercial Property (store, mall, plaza, etc.)

-

Multi-Family (Building with multiple units)

-

Hotels

As a buyer of physical real estate, you are responsible for managing it and renting it out for income. It is an illiquid alternative because buying and selling properties is a tedious process.

Physical real estate falls between stocks and bonds in terms of risks, especially because you can’t see daily fluctuations in the value of your properties. Income potential will depend on whether your properties are rented or not.

Lastly, physical real estate is accessible to almost all investors, assuming that they have the means to purchase it.

2. Listed Real Estate (REITs)

-

Professionally Managed: Yes

-

Liquidity: High

-

Risk: Medium-to-High

-

Income Potential: High

-

Easy to Access: Yes

Listed real estate (through REITS) is another way to access real estate and a different alternative to consider. A REIT pools together capital from investors. It then purchases properties, manages them, and passes rents back to investors.

REITs typically trade on exchanges, similar to stocks. They are considered to be riskier than physical real estate because investors will see daily price volatility. REITs behave more like stocks in the short term and more like physical real estate in the long term.

REITs are usually very liquid and are accessible to most investors. The rents passed on to investors usually result in a high-income stream.

Make sure to take a look at some of the best REITs in Canada.

3. Private Equity Funds

-

Professionally Managed: Yes

-

Liquidity: Very Low

-

Risk: High

-

Income Potential: Very Low

-

Easy to Access: No

Private equity funds invest in companies that are not publicly listed (don’t have a stock trading on an exchange). They usually buy a controlling share or a full company outright by pooling money from investors.

The private equity company then attempts to improve operations or profitability in order to sell it for a profit further down the road. Private equity funds either use leveraged buyouts (taking on debt to buy a company) or venture capital (investing in small, start-up companies.

Private equity funds usually come with long lock-up periods and with little or no income potential. They are usually considered high risk but can lead to exceptional returns.

Private equity funds typically come with high fees and performance fees above a specific level.

4. Hedge Funds (Offering Memorandum)

-

Professionally Managed: Yes

-

Liquidity: Depends on Strategy

-

Risk: Depends on Strategy

-

Income Potential: Depends on Strategy

-

Easy to Access: No

Hedge funds are almost always actively managed and are usually sold with an offering memorandum (OM). This greatly restricts your ability to invest in OM hedge funds unless you are an accredited investor.

Hedge funds can be extremely different in terms of strategy, risk, and return. They can invest in virtually anything. Some examples of hedge fund strategies include:

-

Global macro

-

Market-neutral

-

Long-short

-

Short-biased

Income, liquidity, and risk will vary substantially across different strategies (and within strategies as well).

Hedge funds typically come with high fees and the addition of performance fees, which reward portfolio managers for exceeding a pre-specified return or beating a benchmark.

5. Hedge Funds (Liquid Alternatives)

-

Professionally Managed: Yes

-

Liquidity: High

-

Risk: Depends on Strategy

-

Income Potential: Depends on Strategy

-

Easy to Access: Yes

Hedge funds can also be added to a portfolio as “liquid alternatives.” A liquid alternative is a hedge fund that is packaged in either a mutual fund or ETF wrapper and made available to most investors. In the case of a liquid alternative ETF, it trades on an exchange like any other stock.

Like OM hedge funds, liquid alternatives vary in terms of risk, return, and income. By being packaged in a mutual fund or ETF wrapper, liquidity and ease of access increase tremendously.

Liquid alternatives, like OM hedge funds, tend to come with high fees and are also usually offered with a performance fee.

Make sure to thoroughly assess a liquid alternative before investing in it, or take a look at our list of some of the best liquid alternatives in Canada.

6. Private Debt

-

Professionally Managed: If Investing through a Fund

-

Liquidity: Low

-

Risk: Medium-to-High

-

Income Potential: High

-

Easy to Access: No

Private debt can either be accessed through a fund (professionally managed) or done directly with the end borrower. In a lot of cases, private debt refers to relatively higher-risk loans to individuals that can’t access additional credit through traditional sources (such as a bank).

Private Debt funds pool capital from investors before loaning it out to borrowers. Debt can also be issued directly outside of a formal fund structure, where it becomes the investor’s responsibility to structure.

Lending money to high-risk borrowers can come with very high-interest rates (and, therefore, high-income streams). The main risk here becomes default risk, or the borrower’s ability to repay the principal at maturity.

Private debt is usually illiquid once issued.

7. Cryptocurrencies

-

Professionally Managed: If Investing through a Fund

-

Liquidity: High

-

Risk: Very High

-

Income Potential: None

-

Easy to Access: Yes

Cryptocurrencies continue to evolve as speculative digital assets. Canada now regulates crypto exchanges more closely, and platforms must register with Canadian securities regulators to operate legally.

Investors can access Bitcoin and Ether via ETFs like Purpose Bitcoin ETF (BTCC) or spot Bitcoin ETFs approved in 2024. Crypto remains highly volatile and non-income generating, but it’s liquid and accessible to most investors.

The main two cryptocurrencies globally are currently Bitcoin and Ether. A large number of smaller cryptocurrencies exist, but these come with an even higher risk. Cryptocurrencies are usually purchased through a crypto wallet.

Cryptocurrency ETFs allow investors to include the speculative investment within tax-preferred accounts.

Although cryptocurrencies are very liquid, they are usually considered very high-risk and have no income potential unless a crypto fund uses a covered call strategy.

8. Commodities

-

Professionally Managed: If Investing through a Fund

-

Liquidity: High

-

Risk: High

-

Income Potential: None

-

Easy to Access: Yes

Commodities refer to raw materials that are frequently traded through futures contracts on a futures exchange. Some examples include soybeans, oil, beef, gold, and coffee.

Trading commodities through futures can be very risky since futures are leveraged. Commodity contracts are either cash-settled or physically settled and require extensive research and trading knowledge.

Commodities are also usually available through ETFs or mutual funds. These funds are sometimes based on the price of the underlying futures for the commodity, or the funds invest in stocks that are involved in some way with the commodity (i.e. copper mining stocks).

Commodities can be a good way to diversify a portfolio and protect against inflation as they tend to increase in price during inflationary times.

Investing in commodities is usually fairly liquid but comes without any income potential. Commodities are easily accessible by the average investor.

9. Art and Other Collectibles

-

Professionally Managed: No

-

Liquidity: Low

-

Risk: High

-

Income Potential: None

-

Easy to Access: Yes

Art and other expensive collectibles (such as rare cars) are also considered an asset class and an alternative investment when it comes to building a portfolio.

Typically, these assets are acquired through auctions or private sales, making them fairly illiquid. They are also typically heterogeneous, meaning that very rarely are two pieces identical.

Art and collectibles vary in performance based on overall trends and preferences of collectors and wealthy individuals. Prices are mainly driven by supply and demand.

This alternative investment comes with a fairly high risk, low liquidity, and limited or no potential for generating income.

Average investors are typically able to invest in art and collectibles as long as they are able to afford them.

10. Foreign Currencies

-

Professionally Managed: If Investing through a Fund

-

Liquidity: High

Advertisement

-

Risk: High

-

Income Potential: None

-

Easy to Access: Yes

Foreign currencies can be invested in as an alternative asset. This can be done by directly buying and selling on the forex markets, by investing through an ETF or a mutual fund, or by simply purchasing the currency physically.

Currencies appreciate and depreciate between one another based on several factors. These include:

-

Differences in interest rates between the countries

-

Differences in inflation between countries

You may have exposure to different foreign currencies through your traditional investments if these are located outside of Canada. International or global funds are either currency hedged or currency unhedged.

Foreign currencies are typically very liquid, are considered high risk, have no potential for income, and are easily accessible to the average investor.

11. Financial Derivatives

-

Professionally Managed: If Investing through a Fund

-

Liquidity: Depends

-

Risk: High-to-Very High

-

Income Potential: Depends

-

Easy to Access: Yes

Financial derivatives are also sometimes encountered through more traditional investment funds. Common examples are covered call mutual funds or ETFs which are becoming increasingly popular in Canada.

Financial derivatives typically refer to:

-

Forwards

-

Futures

-

Options

-

Swaps

Financial derivatives are well-named because their price is usually derived from the price of a different underlying asset.

There are a lot of different investment approaches to take with financial derivatives, and they may even be the entire basis of a fund.

The liquidity of a derivative depends on what type of derivative you are investing in. Derivatives tend to be high or very high risk because they are often leveraged. They can be used to generate income and are easily accessible to the average investor.

12. Reinsurance

-

Professionally Managed: Yes

-

Liquidity: Average

-

Risk: High

-

Income Potential: Medium-High

-

Easy to Access: No

A growing area of interest in the hedge fund space is the concept of reinsurance. Insurance companies sometimes wish to offload certain insurance policies (or groups of policies) in order to have better control of risk. These policies are then structured into a product and sold.

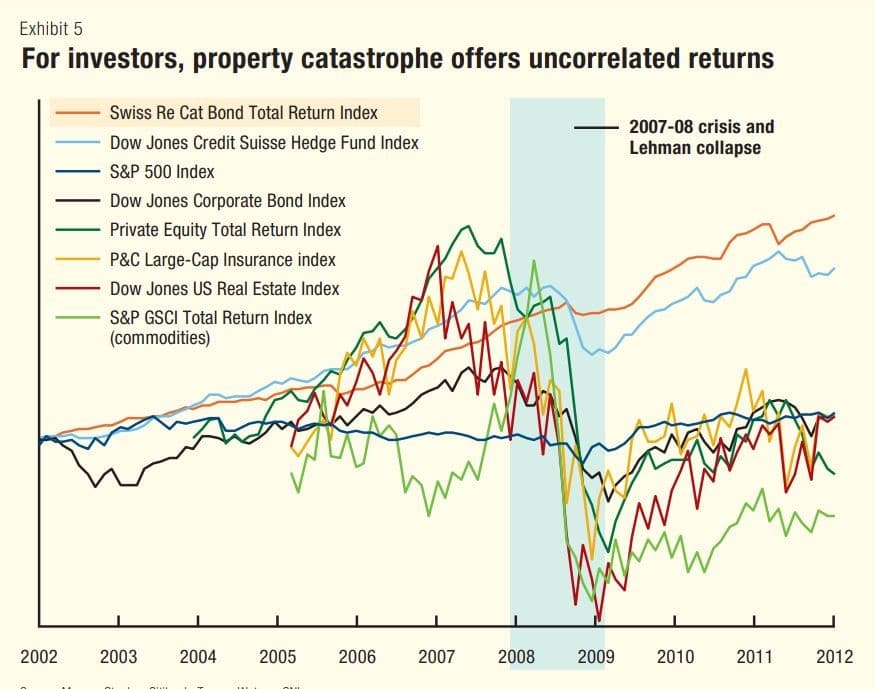

One of the key benefits of accessing these insurance-linked products is that they are highly uncorrelated from overall markets. The insurance products depend on underlying conditions (such as a natural catastrophe), which should be entirely independent of the performance of markets.

Reinsurance remains largely an institutional asset class, often structured via insurance-linked securities (ILS) and accessed through hedge funds or specialized funds.

While it offers attractive yield potential and low correlation to public markets, it is still out of reach for most retail investors in Canada.

13. Non-Fungible Tokens (NFTs)

-

Professionally Managed: If Investing through a Fund

-

Liquidity: Very Low

-

Risk: Very High

-

Income Potential: None

-

Easy to Access: Yes

An NFT is a new type of highly speculative investment that has become popular with the increased adoption of blockchain technology.

NFTs outline ownership in either a physical or digital asset within a blockchain. It’s important to understand that owning an NFT currently does not have any legal meaning around ownership or rights.

An example of an extremely popular NFT is that of the bored ape series.

Owning an NFT of a digital asset does not prevent you or others from sharing that asset.

With the increased popularity of investing in NFTs, professionally-managed NFT funds have begun to emerge for investors to easily access.

NFTs are currently highly illiquid and come with extremely high risks. They do not generate income and are typically easily accessible by average investors.

NFTs are blockchain-based digital assets that represent ownership of unique items like digital art, music, or collectibles. While once a red-hot trend, NFT markets have cooled significantly since 2022.

Liquidity remains very low, and value is highly speculative. They don’t generate income and are difficult to value. While still accessible to average investors, most financial advisors do not recommend NFTs as a core portfolio asset.

14. Structured Products

-

Professionally Managed: If Investing through a Fund

-

Liquidity: Medium

-

Risk: Depends on Strategy

-

Income Potential: Depends on Strategy

-

Easy to Access: Yes

Structured products are typically thought of as highly-customizable alternative fixed-income investments. Common examples that you may encounter include market-linked GICs, principal-protected notes, or principal-at-risk notes.

Structured products are usually created by an issuer and come with issuer risk (the terms of the offering are backed by whoever created the product). A market-linked GIC, for example, can provide investors with some of the return of an underlying index or basket of stocks over a fixed investment period.

These alternative investments can be extremely different and can be customized to be a higher or lower risk or to offer a high or no income stream.

Structured products are somewhat liquid since they can usually be sold back to the issuer before their term matures. Market-linked GICs and structured notes are common structured products that are available to most investors.

Investor Types when Considering Alternatives

Alternative investments, depending on their nature and complexity, may not be available for all investors to purchase. Alternatives do not always have to be purchased within an investment account.

Some examples of alternatives that can be purchased outside of an investment account include:

-

Real estate

-

Art

-

Commodities (physically)

-

Cryptocurrencies

-

Digital assets

-

Luxury cars

-

Collectibles

Managed alternatives such as private equity funds and hedge funds may only be available to specific investors. These are usually reserved for institutional investors or high-net-worth retail investors who meet specific criteria.

Accredited Investors

Accredited investors are able to access investment strategies not available to the general public. Although there are several ways to qualify as an accredited investor, the main ones are:

-

An individual who beneficially owns, or who together with a spouse beneficially own, financial assets having an aggregate realizable value that, before taxes but net of any related liabilities, exceeds $1,000,000;

-

An individual whose net income before taxes exceeded $200,000 in each of the two most recent years or whose net income before taxes combined with that of a spouse exceeded $300,000 in each of those years and who, in either case, has a reasonable expectation of exceeding the same net income level in the current year;

-

A company, limited liability company, limited partnership, limited liability partnership, trust or estate, other than a mutual fund or non-redeemable investment fund, that had net assets of at least $5,000,000 as reflected in its most recently prepared financial statements

Eligible Investors

Eligible investors have more of an ability to invest in alternatives than average investors or non-eligible investors.

An eligible investor is an individual who has:

-

Net assets, alone or with a spouse, in the case of an individual, exceed $400,000,

-

Net income before taxes exceeded $75,000 in each of the 2 most recent calendar years, and who reasonably expects to exceed that income level in the current calendar year, or

-

Net income before taxes, alone or with a spouse, in the case of an individual, exceeded $125,000 in each of the 2 most recent calendar years and who reasonably expects to exceed that income level in the current calendar year

Non-Eligible Investors

Non-eligible investors are extremely restricted in the types of managed alternative solutions they can purchase.

Are Managed Alternative Investments Worth the Fees?

Professionally managed alternative investment strategies, whether they are hedge funds or private equity funds, tend to come with higher fees (and additional performance fees on top).

Depending on the nature of the strategy, these funds can range from being conservative to being extremely high risk. More complex hedge funds may also be able to generate absolute returns, meaning positive returns through all market conditions.

There are several critical things to consider before deciding if an alternative fund is worth the fees:

-

Historical performance, especially relative to its benchmark

-

Length of track record

-

Stability of portfolio management team

-

How high the fund’s fees are relative to peers

Within the managed alternatives space, almost all funds are actively managed. Whether a fund is worth its fees should be determined on a fund-by-fund basis.

Which Investments Have the Best Returns in Canada?

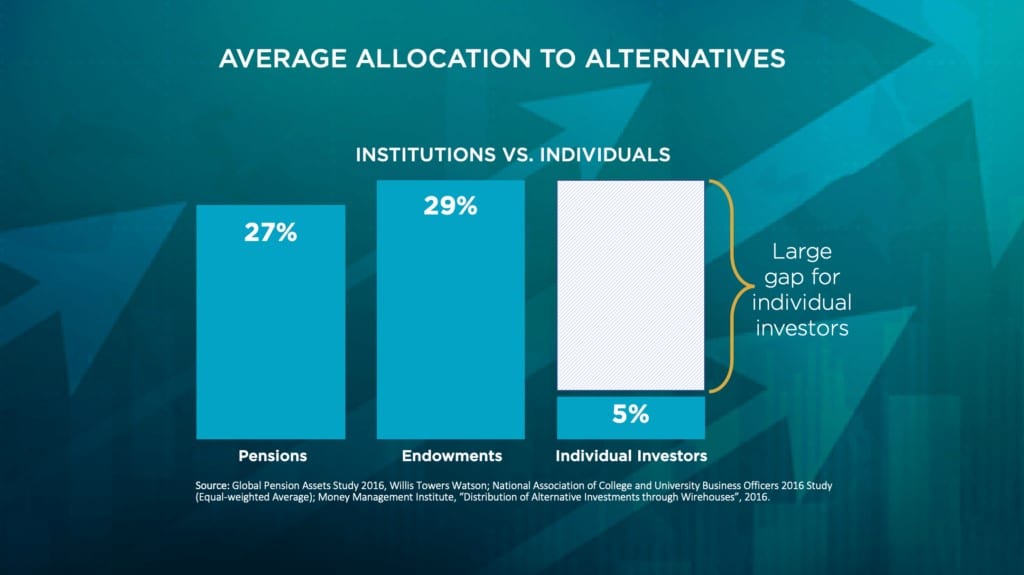

Some of the best-performing investments are likely to be found in the alternative space. Between 1990 and 2010, private equity firms outperformed the S&P 500 by 6.3%, net of fees.

Institutional portfolios (pension funds, endowments, etc.) are typically substantially more sophisticated and better diversified than the average retail investor’s portfolio. The key difference is the large allocation to alternatives, as seen in these charts here:

Are Alternative Investments Suitable for Everyone?

Not all alternative investments are appropriate for every investor. While some options like REITs, commodities, or structured products are available to the general public, others—like hedge funds and private equity—are limited to accredited or eligible investors.

Always consider your liquidity needs, time horizon, and risk tolerance. For average investors, liquid alternatives and real estate are typically more accessible and easier to manage than complex or illiquid private investments.

Is Bitcoin an Alternative Investment?

Bitcoin is considered an alternative investment. More specifically, Bitcoin is considered a digital asset.

Is an ETF an Alternative Investment?

Some ETFs may be considered alternative investments. Alternatives in ETF form are typically considered “liquid alternatives” and can generally be accessed by all types of investors.

Conclusion

The alternatives space is very broad and complicated to understand for the average investor.

Every single feature of an alternative investment can be different from one to another. Make sure that you understand key elements of an alternative before investing, including risk, return, liquidity, and fees.

Before investing in alternatives, make sure that you have properly assessed your current situation and future goals.

FAQs About Alternative Investments in Canada

What qualifies as an alternative investment in Canada?

Alternative investments include any assets outside of traditional stocks, bonds, and cash. Examples include real estate, private equity, hedge funds, commodities, cryptocurrencies, and collectibles.

Are alternative investments suitable for beginners?

Some alternatives like REITs or ETFs are accessible to beginners. However, others—like private equity or hedge funds—require more knowledge and are only available to accredited or eligible investors.

Are alternative investments safe?

Alternative investments often come with higher risks, lower liquidity, and less transparency. While they can offer diversification benefits, they should only form part of a well-diversified portfolio.

Do I need to be accredited to invest in alternatives?

For certain private investments like hedge funds, private debt, or private equity, yes. But liquid alternatives (ETFs or mutual funds) and public REITs are available to regular investors.

Which alternative investment is best for income?

REITs, private debt funds, and certain structured products are often used to generate income. Always assess yield stability and risk before investing.

Are crypto and NFTs good long-term investments?

These are highly speculative assets with high volatility and uncertain future value. While accessible, they should only represent a small portion of your portfolio if included at all.

How much should I allocate to alternative investments?

Most financial advisors recommend 5%–20% of your portfolio, depending on your risk tolerance, goals, and access to alternatives.

Best next step

Keep exploring this topic

If you want to go deeper, these are the most useful follow-up pages and tools for this topic.

Stocks tool

Check Canadian stock movers

See the latest TSX and TSXV winners and losers before digging deeper into a sector.

Research hub

Browse Canadian stock research

Use the stock section to jump from a theme article into individual company pages.

Diversification

Compare stocks with ETF options

If you want exposure to a theme without single-stock risk, screen matching ETFs instead.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.