You know about bank account numbers, and you’ve probably heard about routing numbers, but what is a Canadian bank financial institution number?

Each bank in Canada has a unique three-digit code that differentiates it from other financial institutions. The code remains the same for all the branches within the bank, regardless of their location.

But how do you find this number, and why is it so important? Read on to find out why it’s so critical to your everyday banking needs.

Why Is This Financial Institution Number Important?

In 2019, the top six largest banks saw 598 million online transactions and 784 million mobile banking transactions. With that volume, keeping account numbers straight is paramount to both the banks’ and individuals’ success.

Whether setting up a direct deposit with your employer or authorizing debit payments for a loan, both situations require you to hand over your banking information to complete the transaction.

The bottom line is that you need to know your institution number if you plan on making electronic transactions, including deposits, payments, and wire transfers.

Are There Other Significant Banking Numbers To Know?

Yes! In addition to your institute number, you should know your transit and bank account numbers.

The transit number is five digits and identifies which branch you used to open your account. The transit number, in addition to the institute number, forms the routing number commonly referenced on cheques.

As for your bank account number, that’s usually seven to twelve digits long and identifies your unique individual account.

Where Can I Find These Numbers?

You can find your bank’s institution number by contacting its customer service team, stopping by a local branch, or doing a quick internet search. To save you time, I’ve included a listing of some of the more popular Canadian financial institute numbers:

| Financial institution | Institution number |

|---|---|

| Bank of Montreal | 001 |

| Scotiabank (The Bank of Nova Scotia) | 002 |

| Royal Bank of Canada | 003 |

| The Toronto-Dominion Bank | 004 |

| National Bank of Canada | 006 |

| Canadian Imperial Bank of Commerce | 010 |

| HSBC Bank Canada | 016 |

| Canadian Western Bank | 030 |

| Laurentian Bank of Canada | 039 |

| Bank of Canada | 177 |

Account and Routing Numbers

As for the account and routing numbers, they were most likely provided to you when you opened your account. However, if you have access to cheques, you can find all the above numbers located on them. Here’s how:

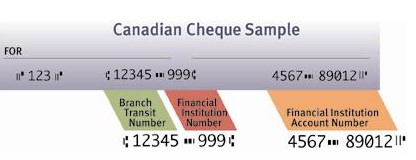

You might not even realize that the numbers on the bottom of your cheques have meaning. In this example, the first set of numbers, “123,” represents your cheque number.

The next set, “12345,” is the transit number identifying the branch where you opened the account. “999” serves as the financial institution number and together with the transit number, makes up the routing number. Your personal account number follows.

What Other Questions To Ask and Things To Consider When Opening a Bank Account?

Finding out your financial institution’s number probably isn’t high up on your priority list when you open a bank account, but as you can see, it’s an important figure to have.

That got me thinking that maybe there are other questions potential customers should ask when opening an account. Here’s what I came up with.

Fees

Without a doubt, this one jumps to the forefront. There are so many different accounts to choose from – how do you know which one gives you the best deal? The only way to find your perfect fit is to do your research.

That includes diving into the details and learning about each account’s charges and fee structure.

Promotional Periods

Many banks extend deals to new customers. Whether it’s a free chequing or a higher interest rate over a certain period, these perks often don’t last past a few months.

That’s not to say a bank that offers a promotion isn’t the one for you. It just means you need to be aware it’s a marketing scheme to pull you in, but does the financial institution hold up and meet your needs once it’s over?

Accessibility

Consider what you want from your bank. Do you need in-person service? Are there local branches near you? What about ATMs? Does the bank you’re considering have ones nearby?

Maybe you don’t care about brick-and-mortar branches and are more concerned with online services.

What if something goes wrong? What does the customer service situation look like with your online bank?

Considering these questions before you sign up for an account can save you a lot of headaches in the future.

Additional Products

Maybe you’re looking to open a chequing account, but does your financial institution offer other products and services?

You might not be interested in mortgage or investment services currently, but that doesn’t mean you won’t need them in the future.

Often, keeping all your financial endeavours in one place makes it easier on you and can get you better deals and interest rates. Even if you aren’t considering additional services now, it’s a good idea to at least glance over the banks’ other options before making your final decision.

Final Thoughts

Now that you know an institute number is a unique three-digit code assigned to each Canadian financial institution, do you know what yours is?

If not, check out the list above so you won’t be left in a lurch when you’re looking to set up a direct deposit, send a wire transfer, or make a loan payment.

In the meantime, if you’re looking for a new bank to grow your money, check out these top 5 picks for 2022.