CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

Capital Gains Tax in Canada ([currentyear]): The New 66.67% Rule

Capital gains tax is one of the most significant taxes for Canadian investors to understand—especially after a recent legislative update.

If you buy and sell investments like stocks, ETFs, real estate, or other capital assets, the profit you make (called a capital gain) is taxed. However, only a portion of the gain is included in your taxable income.

As of June 25, 2024, the capital gains inclusion rate has changed from 50% to 66.67% (two-thirds) for certain gains.

Capital Gains Tax in Canada Explained

Capital gains tax applies to the profit you make from selling capital assets such as stocks, mutual funds, real estate, or other investments.

Here’s how it works in 2024:

-

For individuals:

-

The inclusion rate is still 50% on annual gains up to $250,000.

-

Gains above $250,000 are taxed at a new, higher 66.67% inclusion rate.

-

-

For corporations and trusts:

- The new 66.67% inclusion rate applies to all capital gains, regardless of amount.

So, if an individual earns $300,000 in capital gains during the year:

-

The first $250,000 is subject to the old 50% inclusion rate (i.e. $125,000 is taxable).

-

The remaining $50,000 is taxed at 66.67% (i.e. $33,335 is taxable).

-

The total taxable capital gain becomes $158,335.

This taxable amount is then added to your income and taxed at your marginal rate.

How to Calculate Capital Gains:

-

Determine the Adjusted Cost Base (ACB):

This is what you originally paid for the asset, plus related acquisition costs (like legal fees or capital improvements for real estate). -

Calculate the Capital Gain:

Capital Gain = Proceeds of Disposition − Adjusted Cost Base -

Apply the Relevant Inclusion Rate (50% or 66.67%)

Depending on your income level and type of entity (individual or corporation), apply the correct inclusion rate to your capital gain.

Common Examples of Capital Gains

Below are updated examples to reflect the new capital gains tax rules effective June 25, 2024, which apply a 66.67% inclusion rate on capital gains exceeding $250,000 for individuals, and on all gains for corporations and trusts.

Stocks (Under $250,000 total gains – Individual)

You buy 100 shares of Company A at $10 per share (total cost: $1,000).

Later, you sell all these shares for $20 each (total sale: $2,000).

Your capital gain: $2,000 − $1,000 = $1,000

Taxable amount (50% inclusion rate): $500 (still under $250,000 threshold)

Real Estate (Over $250,000 total gains – Individual)

You buy a vacation property for $200,000.

You invest $50,000 in improvements → ACB = $250,000

You later sell the property for $650,000 → Capital gain = $400,000

Taxable capital gain:

-

First $250,000 × 50% = $125,000

-

Remaining $150,000 × 66.67% = $100,005

Total taxable gain = $225,005

Collectibles (Corporation or Trust)

A corporation buys a rare sculpture for $5,000 and sells it for $15,000.

Capital gain = $10,000

Inclusion rate = 66.67% (for all corporate capital gains)

Taxable capital gain = $6,667

It's important to keep records of the purchase and sale of assets, as well as any costs associated with improvements, to accurately determine the capital gains.

There are certain exemptions and special considerations, such as the principal residence exemption in Canada, which may allow homeowners to avoid paying capital gains tax on the sale of their primary residence under specific conditions.

Tax Treatment of Capital Loss

Capital losses continue to play a vital role in offsetting capital gains. However, due to the updated inclusion rates introduced in June 2024, capital losses must now be applied at the same inclusion rate that the original capital gain was taxed at.

Key Rules:

-

Capital losses must match the inclusion rate of the gains they offset:

-

50% inclusion rate: for the first $250,000 of gains for individuals

-

66.67% inclusion rate: for amounts exceeding $250,000 (and all corporate/trust gains)

-

-

Carryforward and carryback rules remain the same:

-

Carry capital losses back up to 3 years

-

Carry forward indefinitely

-

-

The superficial loss rule remains unchanged.

Example 1: Offsetting a 66.67% Inclusion Rate Gain

You have a $100,000 capital loss in 2024. You also had a $300,000 capital gain in 2024.

-

First $250,000 taxed at 50% inclusion = $125,000

-

Next $50,000 taxed at 66.67% = $33,335

To offset this, you must apply:

-

$250,000 capital loss to offset the 50% gain

-

$50,000 × 1.33 = $66,665 capital loss needed to offset the higher inclusion gain

Your $100,000 loss will not fully cover both, since 66.67% losses require more loss value to offset.

Superficial Loss (Unchanged):

You sell a stock at a $2,000 loss and repurchase it within 30 days.

This is deemed a superficial loss and cannot be claimed for tax purposes.

Instead, the $2,000 is added to the ACB of your repurchased shares.

Examples:

-

Real Estate:

-

You buy a plot of land for investment at $150,000.

-

Later, you sell the property for $100,000.

-

Your capital loss is: $100,000 (sale) - $150,000 (purchase) = -$50,000.

-

If you don't have capital gains in the current year, you can carry this loss backward to the previous three years or forward indefinitely until you can offset it against capital gains.

-

-

Superficial Loss:

-

You sell a stock at a loss of $2,000.

-

Within 30 days, you buy back the same stock.

-

This $2,000 loss is considered a superficial loss, and you can't claim it. Instead, the loss amount gets added to the ACB of the newly purchased stock.

-

Carry Capital Loss Forward

Capital losses can still be carried forward indefinitely, but as of June 25, 2024, they must be applied based on matching inclusion rates.

Here’s what that means:

-

If the original capital gain being offset was subject to a 50% inclusion rate, then a 50% inclusion loss must be applied.

-

If the capital gain was taxed at the new 66.67% rate (e.g. on the portion over $250,000 for individuals), then the capital loss must also be from a year with a matching 66.67% inclusion rate, or it must be grossed up.

Updated Inclusion Rate Table:

| Period Capital Loss Incurred | Inclusion Rate |

|---|---|

| Before May 23, 1985 | 1/2 (50%) |

| May 23, 1985 – 1987 | 1/2 (50%) |

| 1988 – 1989 | 2/3 (66.6667%) |

| 1990 – 1999 | 3/4 (75%) |

| 2000 | IR |

| 2001 – June 24, 2024 | 1/2 (50%) |

| June 25, 2024 onward | 1/2 (up to $250K), 2/3 (above $250K or corporate/trust gains) |

Key Notes:

-

When applying older losses to new gains, CRA will provide a gross-up calculation to ensure the matching rate.

-

This means you can still use older losses, but their value may be reduced or adjusted when applied to higher-inclusion-rate gains.

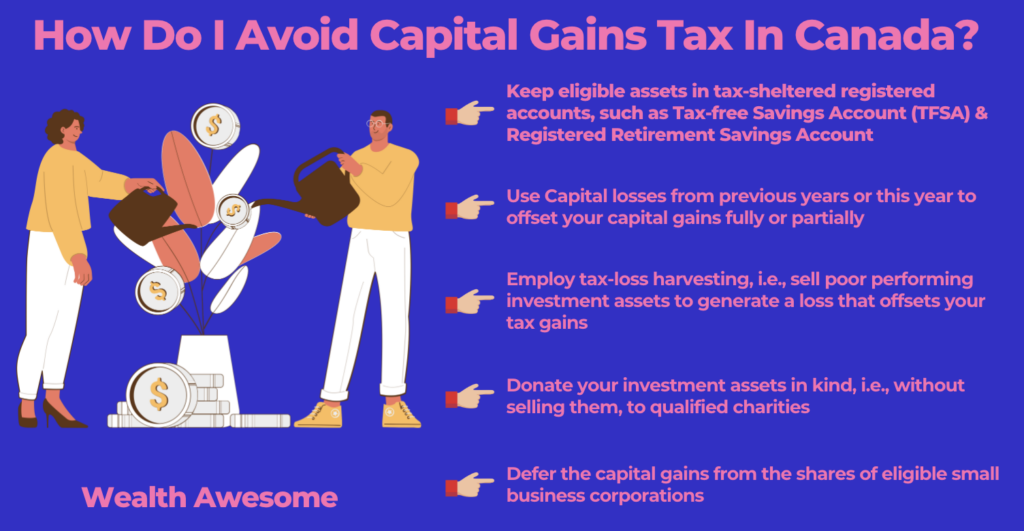

How Do I Avoid Capital Gains Tax in Canada?

While avoiding capital gains tax entirely isn’t always possible, there are several legal strategies to reduce what you owe:

-

Use Registered Accounts: Hold investments inside a TFSA (tax-free) or RRSP/RRIF (tax-deferred). Gains inside a TFSA are never taxed, and RRSP withdrawals are taxed as income (not capital gains).

-

Tax-Loss Harvesting: Sell underperforming investments at a loss to offset realized capital gains in the same year. This can lower your taxable gain. Just watch out for the superficial loss rule.

-

Offset with Carryforward Losses: Apply capital losses from previous years to current gains. If the gain is now taxed at the new 66.67% inclusion rate (post-June 25, 2024), ensure losses are matched or grossed-up accordingly.

-

Split Gains Over Two Years: If you’re close to the $250,000 individual threshold (after which the higher 66.67% rate applies), consider realizing gains over multiple calendar years to stay in the lower tax band.

-

Donate Appreciated Securities: You can donate public securities “in kind” to a registered charity and avoid capital gains tax on the appreciation, while still getting a full tax receipt.

-

Use the Lifetime Capital Gains Exemption (LCGE): If you own qualified small business shares or farm/fishing property, you may be eligible to claim the LCGE, shielding up to $1,016,836 (2024) in capital gains from tax.

-

Principal Residence Exemption: If you're selling your primary residence, you may be fully exempt from capital gains tax, as long as it was designated your principal residence during the time it was owned.

Capital Gains vs. Business Income

Understanding the difference between capital gains and business income is vital because each is taxed differently. The Canada Revenue Agency (CRA) looks at intent, frequency, and nature of activity to decide how your profits are classified.

Here’s a breakdown of the key differences:

| Feature | Capital Gains | Business Income |

|---|---|---|

| Definition | Profit from the sale of an investment held for growth (stocks, real estate, collectibles, etc.). | Profit earned from active, frequent, or business-like trading or flipping. |

| Taxable Amount | 50% taxable (increasing to 66.67% for gains over $250,000 starting June 25, 2024). | 100% taxable at your marginal tax rate. |

| Frequency | Infrequent or long-term holding. | Frequent or systematic trading. |

| Deductible Expenses | Only direct acquisition/sale costs. | Broad range of business-related expenses. |

| Loss Treatment | Losses can only offset capital gains. | Business losses can offset all forms of income. |

CRA Assessment Example (Updated Scenarios):

-

Capital Gains: You hold Apple stock for 3 years and sell it at a profit → capital gain.

-

Business Income: You day-trade stocks 4–5 times per week, generating short-term profits → business income.

-

Capital Gains: You sell your personal vacation home after 10 years.

-

Business Income: You flip 3 homes per year with renovations → likely business income.

⚠️ Important: CRA may reclassify capital gains as business income if it believes you’re acting like a business (e.g., flipping properties or active trading). This could double your tax bill. Keep good records and consult a tax professional if you're unsure.

Unique Situations and Exemptions of Capital Gains Tax

The CRA offers specific exemptions and reliefs for unique asset classes and situations. These can reduce or eliminate capital gains tax altogether:

-

Principal Residence Exemption

If the property you’re selling qualifies as your principal residence for every year you owned it, the entire capital gain is exempt from tax. You must report the sale to claim the exemption. -

Lifetime Capital Gains Exemption (LCGE)

For qualified small business corporation (QSBC) shares, qualified farm property, or qualified fishing property, you may be eligible to claim the LCGE, which allows you to shelter up to $1,016,836 (2024 indexed amount) in lifetime capital gains from tax. This can be a powerful planning tool for business owners and farmers. -

Farm and Fishing Property Rollover

Transfers of qualified farm or fishing property between generations (e.g., from parent to child) can be done on a tax-deferred basis. The gain is not immediately taxable and can be rolled over to the next generation. -

Donation of Publicly Traded Securities

Donating publicly traded securities (stocks, mutual funds, ETFs) directly to a registered charity allows you to avoid paying capital gains tax on the appreciated value — while still receiving a full donation tax credit.

How Long Do You Have to Live in a House to Avoid Capital Gains Tax in Canada?

The CRA doesn’t explicitly specify a timeline about how long you have to live in a house before it’s considered your primary residence and exempted from capital gains tax.

However, if you or your family members have inhabited a property for some time of the year, and it’s not your business to buy properties, live there for a time, and sell them for a profit, you might be able to avoid capital gains tax.

Conclusion

Capital gains tax is a key part of Canada’s tax system and affects most investors at some point. Whether you're selling stocks, real estate, or other assets, knowing how the 50% inclusion rule works — along with exemptions like the principal residence or Lifetime Capital Gains Exemption — can help you plan more tax-efficiently.

Use registered accounts like TFSAs and RRSPs to avoid or defer tax when possible, and consider tax-loss harvesting or strategic timing of asset sales to minimize liability.

When in doubt, consult with a qualified tax advisor to make sure you're making the most of available deductions and exemptions.

FAQs About Capital Gains Tax in Canada

1. How much is capital gains tax in Canada?

Only 50% of your capital gain is taxable. This amount is added to your income and taxed at your marginal tax rate, which varies based on your income level and province.

2. When do I have to pay capital gains tax?

Capital gains tax is due when you sell a capital asset (e.g., stocks, real estate, collectibles) for more than your adjusted cost base. You report this on your income tax return for the year the sale occurred.

3. What is the principal residence exemption?

If the property sold was your principal residence for every year you owned it, you may not have to pay any capital gains tax on the sale.

4. Can I avoid capital gains tax with a TFSA or RRSP?

Yes. Assets held inside a TFSA are not subject to capital gains tax at all. RRSPs defer tax until withdrawal, at which point withdrawals are taxed as regular income.

5. What is a capital loss, and how can it help?

A capital loss occurs when you sell an asset for less than you paid. You can use capital losses to offset capital gains in the current year, or carry them back 3 years or forward indefinitely.

6. What is a superficial loss?

A superficial loss occurs if you sell a security at a loss and repurchase it (or a similar one) within 30 days. This loss can’t be claimed for tax purposes.

7. Is there a lifetime capital gains exemption in Canada?

Yes. If you sell qualifying small business shares or certain farming/fishing property, you may be able to claim the Lifetime Capital Gains Exemption (LCGE), which allows you to exclude a large portion of the gain from tax.

Best next step

Keep exploring this topic

If you want to go deeper, these are the most useful follow-up pages and tools for this topic.

Tax tool

Run the income tax calculator

Estimate take-home pay and tax impact before choosing software or planning contributions.

Registered account

Check your TFSA contribution room

Use excess cash more efficiently after filing by checking your tax-free savings capacity.

Cash management

Compare today’s savings rates

Find a better home for refunds, emergency savings, or short-term cash after tax season.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.