CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

Your credit score and financial history are essential for a variety of reasons. Whether you are looking to buy a home, a new car or even get health insurance for yourself, your credit history is taken into consideration by lenders to assess your creditworthiness.

You have probably heard the saying that money attracts more money. A fair credit score makes you an attractive borrower, and lenders are more willing to offer you credit.

The more credit you get and repay on time, the better your credit score becomes.

Advertisement

A good credit score will help you get better deals and more opportunities. When your credit score is high enough, you are considered a low-risk prospect. Lenders will offer you loans at a lower interest rate, reducing your cost of credit.

What is a Fair Credit Score Exactly?

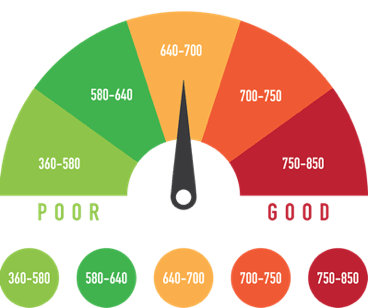

Before we talk about fair credit scores, let's understand how the credit rating scales work. There is one main ways that credit rating agencies rank credit score, which is the FICO score. Both scales run from a range of 300 to 850. Lower scores are considered poorer, while higher scores are considered excellent.

Fair credit is a slightly subjective term here. Every lender and financial institute may have its definition of what is considered a fair or good credit score. For most credit advancing firms, fair credit starts at somewhere around 630, but you may find lenders that consider a score of 600 a fair score.

While the word fair may give you an indication that the score is adequate, the truth is that a fair score is often considered below average.

Lenders will generally require you to have at least a fair credit score before they consider your loan applications. Some lenders ask for a good score to approve loans. A score of 680 or above is considered good enough to get you approved for most types of credit.

How Can A Better Credit Score Improve Your Life?

People use credit for a variety of purposes. Some use it for shopping and buy everyday goods on credit from groceries to clothes and accessories. Others use credit to buy a better car, a mobile phone or a new home. Still, others use credit to finance their business that earns them an income or pay their medical expenses through credit.

No matter what you use your credit card for it helps you fill gaps in what you can afford and what you need at the moment.

When you use credit responsibly it can improve your life in the following five ways:.

-

A fair credit score may allow you to get better rates on mortgages

-

You could get better rates on insurance with a high credit score.

-

Car insurance companies usually charge a lower premium rate for a client with a high credit score.

-

If you are looking to buy a new mobile device, a better credit score could mean that you don’t have to pay any security deposit upfront.

-

Lastly, a fair credit score can also influence your social interactions. Employers are more receptive to hire employees who have at least a fair score. Financial and legal professions, in particular, try to avoid hiring people with bad credit history. A good score can also affect your prospects for dating. Surveys show that people try to avoid potential romantic partners with a bad credit because they fear these partners could become a financial burden on them.

Having Fair Credit Opens Doors

Advertisement

The business world is built on credit. Whether you are looking to get a new mortgage, insurance or business loan with another company, they will ask to see your credit report to get an idea of how you have managed your finances so far [1].

The credit report shows them two things. First, it tells them your credit history and whether you have missed any payments. Second, it shows your credit score, which is based on various factors such as your outstanding debt, past delinquencies, and length of credit history, etc.

A fair credit score opens up new opportunities to raise finances and do business. A large number of businesses are built on long-term and short-term debt. If you can get credit easily, you can invest it into profitable opportunities that come your way.

If you don’t have good credit, you won’t be able to raise finances quickly when you need them. This can hinder your potential to build positive cash flows and keep you from gaining useful employment.

Fair vs. Poor Credit

A credit score below 580 is generally considered poor. Mortgage lenders expect a score of at least 620. Most lenders would be reluctant to offer you credit when your score is poor unless you can offer collateral to cover the chance of default. Those who do offer loans would charge you a higher interest rate or ask you to take out expensive loan insurance.

A poor score can cost you hundreds of dollars in interest and insurance payments every year. Lower scores indicate that you have missed payments before or that you have a high debt to income ratio.

As investors expect a higher return for higher risk propositions, a low score means you will often end up paying more for a loan than someone with a fair or good rating pays for that same loan.

Fair vs. Good Credit

It is easier to get your credit into the fair range, which runs from around 580 to 680 on the scale. To get into the good credit range of 700 – 780, you will need to monitor and plan your outstanding credit lines actively.

This could mean you have to apply for multiple credit lines and make payments on time consistently. Many people actively build up their credit before applying for a new mortgage or insurance because they understand that a good score can reduce their interest rate.

Ask any financial advisor, and they will tell you that it is always worth the effort (and money) to move from fair credit rating to good, especially before you apply for a new loan. It gives you three significant advantages.

-

A good score allows you to qualify for better credit cards, home loans, and business finance.

-

Your interest rates and insurance premiums will be lower when your credit score is good or higher.

-

With a good score, you will find it easier to rent a place, get new deals without paying a deposit, and get utilities connected.

Your credit score is like your financial reputation. A good reputation is better than fair. Businesses and individuals will be more open to trusting you when your score is good.

Why Is Knowing Your Credit Score Important?

It is essential to be aware of your credit score so you can take actions to improve your credit decisions. When you monitor your credit score regularly, you will be able to determine what is causing the score to drop and get errors corrected that may be hurting your credit score.

Conclusion

Credit scores are measured in a range of 300 – 850 by credit rating agencies. A fair credit score is around 580 to 680 on this range. It is easy to attain and necessary for getting loan approvals as most lenders would ask you to have at least a fair credit score before they consider your application.

Generally, lenders can set their own criteria for approving credit applications. However, if you know where you stand on the credit score range, you can make informed guesses about your loan eligibility and financial situation. This can save you both disappointment and headache from loan rejection.

A good credit score, coupled with knowledge about your score will allow you to better predict whether your application will be approved or denied. You will also be able to tell whether you qualify for lower interest rates or other favorable terms like 0% deposit.

Best next step

Keep exploring this topic

If you want to go deeper, these are the most useful follow-up pages and tools for this topic.

Mortgage rates

Compare today’s mortgage rates

Move from mortgage education into current fixed and variable rate comparisons.

Mortgage tool

Run the mortgage calculator

Estimate payments and affordability before contacting a lender or broker.

Special case

Use the self-employed mortgage calculator

If your income is variable, use the calculator built for self-employed borrowers.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.