CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

Refinancing can help you save money by securing a lower mortgage rate or accessing extra funds. With rising mortgage costs in Canada - like a $300,000 mortgage jumping by $509/month from 2021 to 2024 - homeowners are exploring refinancing options. Here's what you need to know:

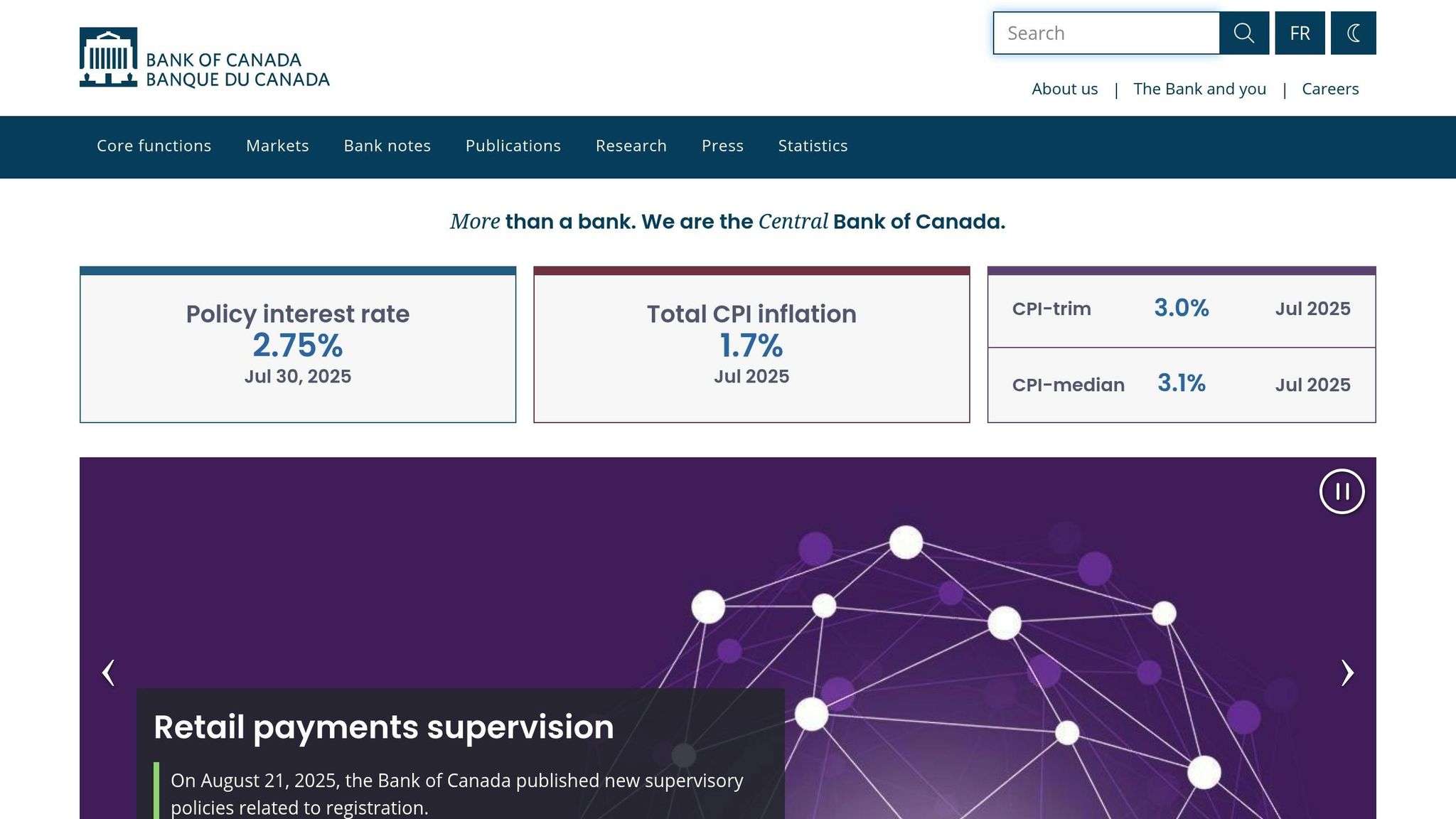

- Rates are improving: The Bank of Canada lowered its benchmark rate to 2.75% in early 2025, creating opportunities for better deals.

- Fixed vs. Variable: Fixed rates offer stability but can be costly if broken early. Variable rates fluctuate with market trends but often have lower penalties.

- Credit matters: A score of 740+ gets the best rates, while scores below 600 face challenges.

- LTV ratio: Your home equity impacts your refinancing options - more equity often means better terms.

- Timing is key: Watch Bank of Canada rate announcements and bond yields for the best opportunities.

To secure the best rate:

Advertisement

- Check and improve your credit score.

- Compare lenders using tools like RateHub.ca.

- Negotiate terms, including fees and perks.

- Time your application strategically.

Even small rate improvements can save you thousands over time.

What is Mortgage Refinancing – Access Cash and Maximize Savings!

Basic Refinancing Terms Every Canadian Should Know

Understanding the basics of refinancing can help you negotiate better rates and save money on borrowing costs.

Fixed vs. Variable Interest Rates Explained

When choosing between fixed and variable interest rates, it’s essential to weigh the pros and cons of each.

- Fixed rates lock in your interest rate for the entire term of your mortgage, which can range from one to several years in Canada. This stability ensures consistent monthly payments, making it easier to budget. However, you might miss out on savings if rates drop during your term.

- Variable rates, on the other hand, are tied to the Bank of Canada's policy rate and your lender's prime rate. These rates fluctuate with market conditions, meaning you could benefit from lower payments or faster principal repayment when rates decrease. However, they come with the risk of higher payments if rates increase.

It’s worth noting that fixed-term agreements often come with higher penalties for breaking the mortgage early, calculated using either additional months' interest or an Interest Rate Differential (IRD) formula. Meanwhile, variable rate mortgages typically have lower penalties, offering more flexibility if you decide to refinance.

Finally, understanding how your home's equity - measured by the loan-to-value (LTV) ratio - impacts refinancing options is key to making informed decisions.

Loan-to-Value Ratios and Mortgage Types

Your Loan-to-Value (LTV) ratio measures the percentage of your home's value that is financed. This ratio plays a significant role in determining your interest rate and whether you qualify for certain mortgage types.

- Conventional mortgages are available to homeowners with a lower LTV, meaning they have more equity in their home. These mortgages typically come with better rates, as they pose less risk to lenders.

- High-ratio mortgages apply to borrowers with a higher LTV. These mortgages require mortgage loan insurance, provided by organizations such as the Canada Mortgage and Housing Corporation (CMHC), Genworth Canada, or Canada Guaranty. While this insurance adds an extra cost, it helps secure competitive borrowing rates by reducing the lender’s risk.

- Home Equity Lines of Credit (HELOCs) allow homeowners to borrow against their available equity. Many Canadians use HELOCs as part of their refinancing strategy, combining them with a traditional mortgage for added flexibility.

As you pay down your mortgage, your LTV ratio improves, potentially unlocking better refinancing opportunities. However, regional differences in home prices across Canada can influence your equity and, in turn, your refinancing options.

How Bank of Canada Rates Affect Your Borrowing Costs

The Bank of Canada's policy rate is the cornerstone of lending rates across the country, directly influencing borrowing costs.

Canadian banks typically set their prime rates slightly above the Bank of Canada's policy rate. When applying for refinancing, lenders conduct a stress test by adding a fixed margin to the benchmark rate. This ensures borrowers can handle potential payment increases if rates rise in the future.

The Bank of Canada announces its policy rate on a set schedule throughout the year, providing insights into possible changes. Some borrowers align their refinancing applications with these announcements, although lenders may adjust their rates based on market conditions even before official updates.

Additionally, mortgage bond yields, such as those on Government of Canada bonds, affect fixed mortgage rates. When bond yields rise due to economic or inflationary pressures, fixed rates may increase - even if the Bank of Canada's policy rate remains steady.

How to Improve Your Credit Score for Better Rates

Your credit score plays a major role in determining your refinancing rate. In Canada, lenders generally reserve their best rates for borrowers with strong credit scores. If your score is lower, you might face rates that are 1-2 percentage points higher, which could add up to thousands of dollars in extra interest over the life of your mortgage. The first step? Make sure your credit report is accurate.

Checking and Fixing Your Credit Report in Canada

Before refinancing, get your credit reports from both Equifax and TransUnion. These reports are available for free and can be requested online, by phone, or by mail. Since the two credit bureaus may have slightly different information, reviewing both gives you a fuller picture of your credit health.

Go through your reports carefully to spot any errors that might be dragging down your score. Common mistakes include incorrect payment records, accounts that don’t belong to you, or paid-off debts still showing as unpaid.

If you catch an error, act quickly and file a dispute. For Equifax Canada, disputes can be submitted online or by calling 1-800-465-7166. TransUnion Canada also allows you to dispute errors through their online portal or by phone at 1-877-713-3393. Be sure to include any supporting documents, such as payment receipts or bank statements, to back up your claim.

The credit bureaus are required to investigate disputes within 30 days. During this time, they’ll contact the creditor to verify the information. If the creditor can’t confirm the disputed item, it will be removed from your report. Once your reports are accurate, focus on improving your daily financial habits to boost your credit score.

Practical Tips to Improve Your Credit Score

Your payment history has the biggest impact on your credit score. Setting up automatic payments can help you avoid missed payments, which can lower your score by 50-100 points and stay on your report for up to six years.

Another important factor is your credit utilisation ratio - the percentage of your available credit that you’re using. Aim to keep this ratio under 30%, though staying below 10% is even better. Paying down existing balances can improve your score within 30-60 days, which is especially helpful before refinancing.

Avoid applying for new credit in the months leading up to your refinancing application. Each hard inquiry - when a lender checks your credit - can temporarily lower your score by 5-10 points. Multiple inquiries in a short period may also signal financial trouble to lenders.

If possible, request a credit limit increase on your existing cards without using the additional credit. This lowers your utilisation ratio and can give your score a boost. Many Canadian banks make it easy to request increases online or through their apps.

Finally, keep old credit accounts open, even if you don’t use them often. The length of your credit history contributes to your score, and closing older accounts can hurt you by reducing your available credit and shortening your average account age.

Credit Score Benchmarks for Refinancing Rates

Having a higher credit score doesn’t just lower your rates - it also gives you access to more lenders. In Canada, the best refinancing rates are typically offered to borrowers with scores of 740 or higher. Scores between 680-739 can still get competitive rates, though they may be slightly higher.

If your score is in the 600-679 range, you’ll likely face higher interest rates and may need to work with alternative lenders. Some lenders specialize in helping borrowers in this range, but you should expect to pay a premium.

Scores below 600 make refinancing through traditional lenders difficult. In this case, you might need to consider private lenders or focus on improving your credit score before applying. The difference in rates between excellent and poor credit can be dramatic - sometimes as much as 3-4 percentage points or more.

Keep in mind that most Canadian lenders will also evaluate your debt-to-income ratio alongside your credit score. Even if you have excellent credit, carrying too much debt relative to your income can limit your refinancing options or result in higher rates.

Where to Find the Best Rates: Banks, Credit Unions, and Online Lenders

Once you've got a strong credit score and a good understanding of refinancing terms, the next step is finding the right lender. This decision can have a big impact on your finances, potentially saving you thousands over the life of your mortgage. In Canada, lenders generally fall into three categories: traditional banks, credit unions, and online lenders. Each option offers unique benefits depending on your needs and financial situation. Let’s break down what each has to offer.

Banks vs. Credit Unions vs. Online Lenders: What to Expect

Traditional banks dominate the Canadian mortgage market, handling about 72% of outstanding mortgages. They offer competitive rates and excellent digital tools that make managing your mortgage easier. However, banks are bound by federal stress test rules, which means their eligibility requirements are often stricter. If your financial situation is complex, you might find it harder to qualify.

Advertisement

Banks also tend to sell their mortgages to outside investors. While this standardised practice ensures consistency, it can reduce their flexibility in tailoring loan terms or supporting you through financial difficulties. The service, while efficient, might feel less personal compared to other lenders.

Credit unions, on the other hand, take a different approach. With nearly 700 credit unions across Canada, these member-owned institutions focus on providing more personalised service. They often offer lower rates and fees than banks and have more flexible lending criteria. For example, credit unions frequently waive the federal mortgage stress test, making them a great choice for self-employed borrowers or those with unique financial circumstances. Many credit unions also keep mortgages in-house, which allows them to offer customised solutions throughout the term of your loan.

The downside? Credit unions usually have a more limited reach, serving specific local communities. That said, many are improving their online and mobile banking services to compete with larger institutions.

Online lenders and non-bank lenders have become increasingly popular in recent years. These lenders cater to borrowers who might not fit the traditional mould. While they’re a lifeline for people with non-standard financial profiles, they often charge higher rates, especially for higher-risk borrowers.

Here’s a quick comparison of the three:

| Lender Type | Best For | Typical Rates | Key Advantages | Main Drawbacks |

|---|---|---|---|---|

| Big Banks | Standard financial profiles | Competitive | Nationwide access, advanced technology | Strict criteria, less flexibility |

| Credit Unions | Unique situations, local borrowers | Often lower than banks | Flexible criteria, personalised service | Limited geographical reach |

| Online Lenders | Non-traditional borrowers | Higher than banks/credit unions | Serves borrowers with non-traditional profiles | Higher rates and fees |

Rate Comparison Tools for Canadian Borrowers

Once you’ve explored your lender options, the next step is comparing their rates. Instead of contacting each lender individually, you can use online tools to quickly compare rates from multiple institutions. Websites like Ratehub.ca provide real-time mortgage rates from banks, credit unions, and alternative lenders, helping you identify the best deals.

Another great resource is Wealth Awesome, which focuses on providing mortgage comparisons tailored specifically for Canadians. Their data-driven approach not only highlights rates but also explains the features and potential restrictions of various mortgage products.

When using these tools, don’t just focus on the advertised rate. Take a closer look at the annual percentage rate (APR), which includes fees and other costs. Sometimes, a lender offering a slightly higher rate might actually save you money if their fees are lower or their terms are more favourable.

It’s also worth noting that the rates listed online are usually for borrowers with excellent credit and straightforward financial situations. If your credit history is less than perfect or your financial profile is more complex, the rate you qualify for may differ from what’s advertised.

sbb-itb-24a3f88

When to Refinance and How to Negotiate Better Terms

Once you've built a solid credit profile and compared lenders, the next step is to focus on timing your refinance and negotiating effectively. In Canada’s cyclical mortgage market, timing can make a big difference in securing favourable rates. Let’s explore when to refinance and how to approach negotiations to get better terms.

Best Times to Refinance Based on Market Conditions

Keeping an eye on market trends is crucial for refinancing at the right time. Here are some key moments to consider:

- Bank of Canada Rate Announcements: Pay attention to policy updates from the Bank of Canada. If they signal a shift toward lower interest rates or a more accommodative stance, it might be a good time to refinance.

- Bond Yields: Fixed-rate mortgages in Canada often follow the movement of Government of Canada bond yields, particularly the 5‑year bond. A steady drop in bond yields can indicate that lower mortgage rates are on the horizon.

- Seasonal Trends: Winter tends to be a quieter time for the mortgage market, which can prompt lenders to offer more competitive rates and flexible terms to attract borrowers.

- Economic Uncertainty: During periods of economic instability, lenders may offer better rates to stimulate borrowing. Keep an eye on indicators like employment statistics and inflation rates.

- Before Mortgage Term Expiry: Start tracking rates several months before your current mortgage term ends. This allows you to act quickly if market conditions become favourable.

How to Negotiate with Canadian Lenders

Once you've identified the right time to refinance, negotiating effectively is the next step. Here’s how to strengthen your position and secure better terms:

- Rate Matching: Bring a written offer from a competing lender to your preferred lender. This can often encourage them to match or even beat the rate.

- Leverage Relationships: If you already have a relationship with your lender, use it to your advantage. Long-standing clients may be offered better terms.

- Reduce Fees: Negotiate appraisal, legal, and processing fees to lower your overall refinancing costs.

- Ask for Cash-Back Offers: Some lenders provide cash-back incentives that can help offset closing costs - don’t hesitate to inquire.

- Timing Your Negotiation: Lenders may be more flexible near the end of their fiscal periods when they’re aiming to meet targets.

- Be Prepared: Gather all necessary documents, such as pay stubs, tax returns, bank statements, and your credit report. Having pre-approvals from multiple lenders can also give you more leverage.

- Consider Additional Features: Discuss options like prepayment privileges or other flexible features that could benefit you in the long run.

Your Action Plan for Getting the Best Refinancing Rate

To lock in the best refinancing rate, it’s all about preparation, research, and timing. Here’s a step-by-step guide to help you navigate the process and save money in the long run.

Check your credit report first. Start by obtaining your free credit reports and reviewing them thoroughly. Correct any errors, pay down high balances, and steer clear of taking on new credit for at least six months. Aim for a credit score of 680 or higher to qualify for more competitive rates.

Do your homework on lenders. Use tools like RateHub.ca to get a snapshot of the current market. Then, reach out to a mix of lenders - major banks, credit unions, and online platforms - to compare their rates, terms, and any special offers. Each lender brings something different to the table, so don’t settle without exploring your options.

Time your application wisely. Keep an eye on Bank of Canada updates, bond market trends, and seasonal patterns that could influence rates. If your mortgage renewal date is approaching, act quickly to take advantage of favourable conditions.

Negotiate like a pro. Gather written offers from competing lenders and use them as leverage. Remember, you can negotiate more than just the interest rate - ask about fees, cash-back deals, and other perks. If you’ve been a reliable customer, mention your payment history to strengthen your position.

Get your paperwork in order. Speed up the process by having everything ready in advance. This includes your most recent pay stubs, two years of tax returns, bank statements, and detailed information about your current mortgage.

A little effort can go a long way. Even a small difference in your refinancing rate can mean saving thousands over the life of your mortgage. By following these steps, you’ll be well-positioned to secure a rate that works in your favour.

FAQs

Should I choose a fixed or variable rate mortgage when refinancing in Canada?

Deciding between a fixed or variable rate mortgage comes down to your financial situation, comfort with risk, and expectations about interest rate trends. Fixed-rate mortgages, currently hovering between 4.1% and 4.3%, offer consistent payments, making them a solid choice if you value predictability or are worried about rates going up.

On the flip side, variable-rate mortgages, which might dip to around 4%, can offer savings if interest rates drop or stay steady. However, they carry the risk of higher payments if rates rise.

Think about how well you could manage fluctuating payments, your long-term financial plans, and where you think rates are headed before making a decision. If you prefer stability, a fixed rate may be the way to go. If you're open to some risk in exchange for potential savings, a variable rate might suit you better.

How can I boost my credit score in Canada before refinancing?

Improving your credit score before refinancing can make a big difference in the interest rates you’re offered. Start by ensuring you pay all your bills on time - late payments can have a serious negative impact on your score. Another key step is keeping your credit utilization low; aim to use no more than 30% of your available credit limit. Also, think twice before closing old credit accounts, as having a longer credit history works in your favour.

Take the time to review your credit report for any errors. Mistakes can happen, and correcting them ensures your report accurately reflects your financial situation. Finally, steer clear of unnecessary credit applications - too many inquiries can drag your score down. These practical steps can help boost your credit profile and increase your chances of securing the best refinancing terms available in Canada.

How can I negotiate better refinancing terms with lenders in Canada?

How to Negotiate Better Refinancing Terms in Canada

If you're looking to refinance in Canada, the first step is to do your homework. Check out the current interest rates and take a close look at your credit score. A solid credit profile can give you an edge when it comes to negotiating with lenders.

When you're ready to approach lenders, do so with confidence. Ask them for their best rates and let them know you're shopping around with other banks, credit unions, or brokers. If you have quotes from competitors, use them as leverage to push for a better deal. And don’t feel pressured to accept the first offer - lenders often have some flexibility in their rates, so it's worth pushing for better terms.

Timing is another key factor. Locking in a rate when market conditions are in your favour can lead to significant savings over time. Keep an eye on the market and be ready to act when the timing feels right.

Related Blog Posts

Best next step

Keep exploring this topic

If you want to go deeper, these are the most useful follow-up pages and tools for this topic.

Mortgage rates

Compare today’s mortgage rates

Move from mortgage education into current fixed and variable rate comparisons.

Mortgage tool

Run the mortgage calculator

Estimate payments and affordability before contacting a lender or broker.

Special case

Use the self-employed mortgage calculator

If your income is variable, use the calculator built for self-employed borrowers.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Qayyum Rajan, CFA

Qayyum is the CEO of Wealth Awesome, a leading Canadian personal finance publication. As a CFA charterholder with extensive experience in fintech, data science, and quantitative finance, he brings a unique analytical perspective to investing and wealth management.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.