CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

What is a Mortgage Investment Corporation?

A Mortgage Investment Corporation (MIC) is an investment entity in Canada that gathers capital from various investors to issue mortgages primarily across residential sectors. These corporations focus predominantly on Canadian properties and must distribute the mortgage interest income they receive to investors as dividends. The structure of MICs offers a tax advantage—they do not pay corporate tax, thereby preventing double taxation and potentially increasing investor returns. MICs operate under strict regulations, including a minimum investment in residential properties and a cap on shareholder ownership to ensure diversified control.

How MICs Operate

Advertisement

MICs function as flow-through entities, meaning they pass all income directly to shareholders without corporate taxation, similar to mutual fund trusts. Investors buy shares in MICs and earn dividends proportional to their investment. These corporations often serve as private lenders, providing loans even to subprime borrowers, which carries higher risks but also the potential for higher returns. MICs manage risk by maintaining conservative loan-to-value ratios, limiting mortgage terms, and focusing their lending in major urban areas in Canada.

Key Insights into Mortgage Investment Corporations (MICs)

As of recent data, Mortgage Investment Corporations (MICs) represent a modest but growing segment of the Canadian mortgage market. Historically, by 2018, about 200 MICs managed $12.5 billion in mortgages, constituting less than 1% of the market. This niche market has seen expansion, with MICs increasing their market share to 1.7% by September 2022. Notably, a significant proportion of MIC loans are secured by first mortgages, with the larger funds primarily investing in Ontario and British Columbia.

Best Mortgage Investment Corporations in Canada

| MIC | Lending Focus | Property Type Focus | Average Interest Rate/Dividend Yield | Average Loan-to-Value (LTV) |

|---|---|---|---|---|

| Alta West Capital | Alberta, British Columbia, and Ontario | Residential Lending | 8.50% - 9.00% | 69% |

| MCAN Financial Group | Urban (Ontario, Alberta, and British Columbia) | Single-family homes, Construction, Commercial | 9.3% | 67% |

| Atrium Mortgage Investment Corporation | Urban (GTA, Vancouver) | Residential, Commercial | 8.5% | 59% |

| Cannect | Ontario | Residential, Construction, Commercial | 9.1% | 44% |

| Canguard | British Columbia | Residential, Construction, Commercial, Agricultural | 9.5% | 54% |

| Firm Capital | Ontario | Residential, Commercial | 9.5% | N/A |

| RiverRock | Ontario | Residential | 8% | 68% |

| CMI | Ontario | Urban | 6% - 11% | 68% |

| AP Capital | Western Canada (British Columbia and Alberta) | Residential | 8% | 58% |

| Timbercreek Financial | Across Canada | Multi-residential, Commercial | 10.7% | 67% |

Alta West Capital Investment Summary

| Metric | Value |

|---|---|

| Annual Dividend Yield | 9.3% |

| 1-Year Stock Return | 20% |

| Average LTV | 67% |

Company Profile Alta West Mortgage Capital Corporation, a stalwart in the residential mortgage lending sector, requires a minimum investment of $10,000. With a focus on providing stable returns, the portfolio predominantly consists of single-family residential properties, deliberately excluding large-scale developments such as condos with more than six units, significant commercial properties, and land development projects.

Investment Dynamics

-

Dividends: Payments are made monthly, with a flawless record of no missed payments since the company's inception.

-

Redemption Policy: Monthly redemptions are allowed without early redemption fees or lock-up periods, contingent upon fund availability.

-

Purchasing Policy: Implemented weekly to minimize cash drag, reflecting strategic fund management.

-

Mortgage Diversity: Features smaller average loan sizes across a considerable number of mortgages.

Strategic Focus Established in 1991, Alta West Capital has demonstrated robust leadership in managing residential portfolios, adapting through various economic conditions to safeguard and grow investor capital consistently. As one of the select alternative lenders, it specializes in short-term residential mortgages throughout Canada, aiming to protect investor capital while ensuring regular income.

Targeted Clientele Alta West primarily caters to self-employed individuals, entrepreneurs, and newcomers to Canada, offering them primary and supplementary mortgage financing through two managed MIC funds: AWM Diversified MIC and First Place MIC. These products are designed for those who may find it challenging to secure traditional bank financing.

MCAN Investment Summary

| Metric | Value |

|---|---|

| Loan-to-Value | 78% |

| Max Loan Term | 12% |

| Max LTV | 85% |

MCAN Financial Group Investment Overview

Essential Details

-

Minimum Investment: Purchase as little as one share.

-

Stock Symbol: MKP

-

Lending Focus: Urban areas including Ontario, Alberta, and Vancouver.

Property Type Focus

-

Single-family homes

-

Construction projects

-

Commercial properties

Corporate Overview Originally known as MCAN Mortgage Corporation, MCAN Financial Group is now a publicly-traded Mortgage Investment Corporation (MIC) listed on the Toronto Stock Exchange (TSX) under the ticker symbol MKP. The group primarily lends for single-family residential properties, but its portfolio also extends to construction and commercial real estate loans through its subsidiary, MCAN Home Mortgage Corporation.

Financial Mechanics MCAN strategically utilizes deposits received into its CDIC-eligible term deposits at MCAN Wealth to fund its mortgage operations. These term deposits, protected under CDIC, demand a minimum deposit of $10,000 for terms shorter than a year and $5,000 for longer durations. The financial structure is designed to capitalize on the spread between the interest paid on deposits and the income generated from mortgage lending. In 2023, this spread amounted to 3.5%, illustrating MCAN’s effective use of capital to enhance shareholder returns.

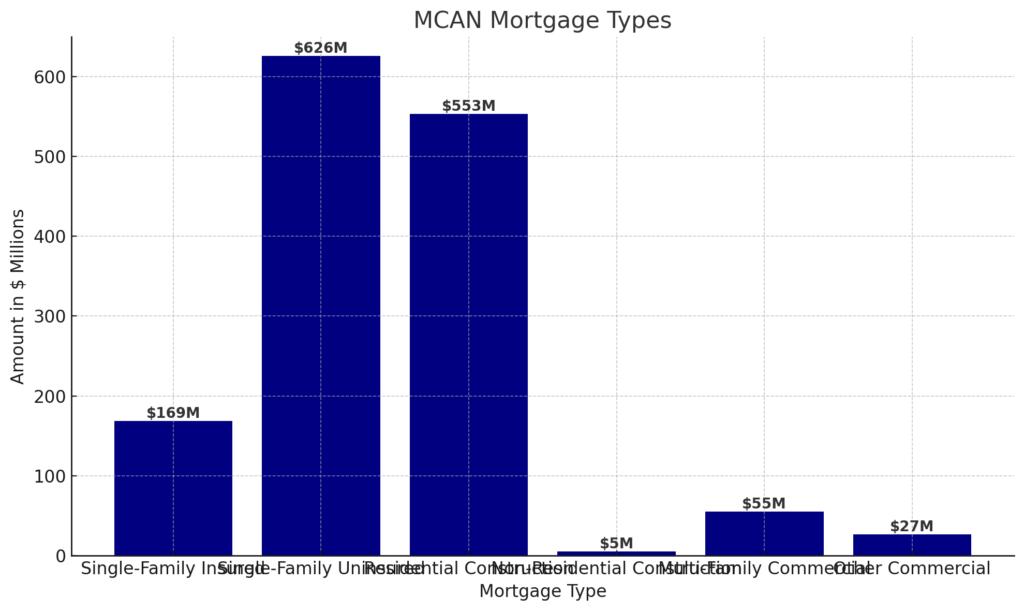

MCAN Mortgage Types

| Mortgage Type | Portfolio |

|---|---|

| Single-Family Insured | $169 Million |

| Single-Family Uninsured | $626 Million |

| Residential Construction | $553 Million |

| Non-Residential Construction | $5 Million |

| Multi-Family Commercial | $55 Million |

| Other Commercial | $27 Million |

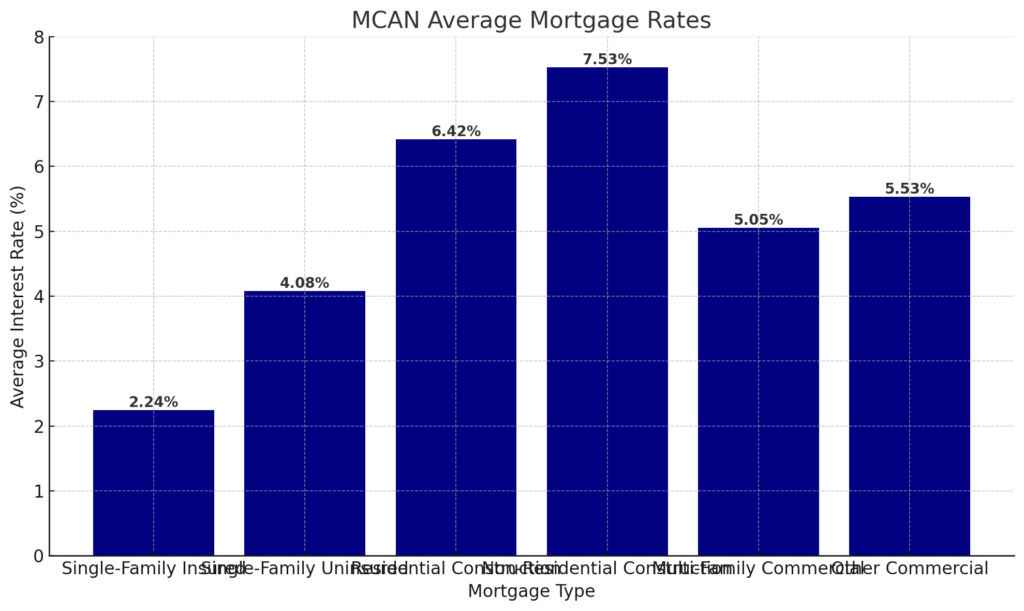

MCAN Average Mortgage Rates

| Mortgage Type | Average Interest Rate |

|---|---|

| Single-Family Insured | 2.24% |

| Single-Family Uninsured | 4.08% |

| Residential Construction | 6.42% |

| Non-Residential Construction | 7.53% |

| Multi-Family Commercial | 5.05% |

| Other Commercial | 5.53% |

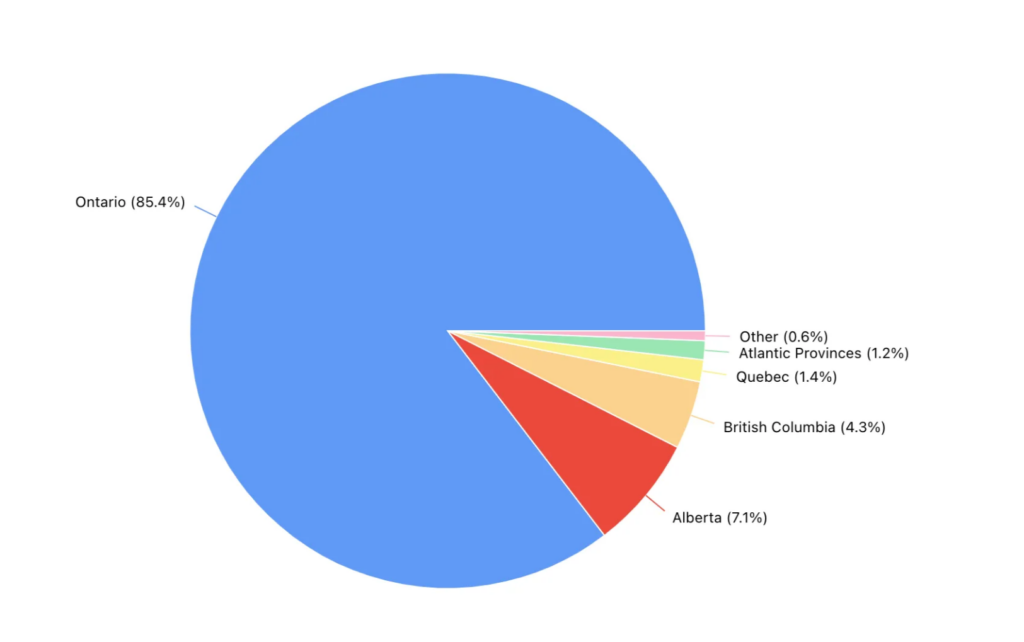

MCAN Mortgages by Province

| Province | Single-Family Mortgages | Share (%) |

|---|---|---|

| Ontario | $2.23 billion | 85.4% |

| Alberta | $186 million | 7.1% |

| British Columbia | $112 million | 4.3% |

| Quebec | $36 million | 1.4% |

| Atlantic Provinces | $31 million | 1.2% |

| Other | $16 million | 0.6% |

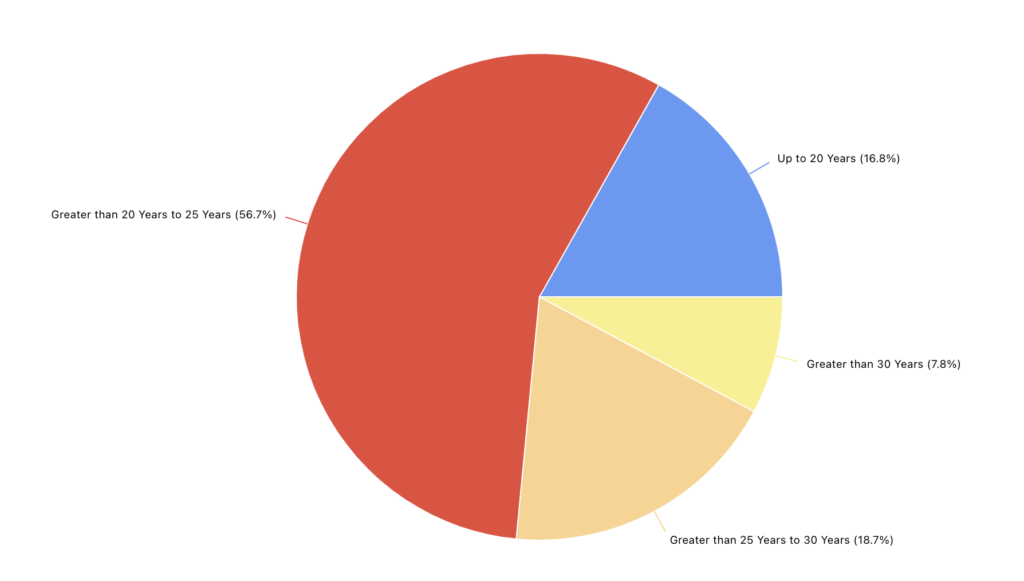

MCAN Mortgage Amortization Periods

| Amortization Period | Single-Family Mortgages | Share (%) |

|---|---|---|

| Up to 20 Years | $440 million | 16.8% |

| Greater than 20 Years to 25 Years | $1.48 billion | 56.7% |

| Greater than 25 Years to 30 Years | $489 million | 18.7% |

| Greater than 30 Years | $204 million | 7.8% |

Atrium MIC Investment Summary

| Metric | Value |

|---|---|

| Annual Dividend Yield | 8.5% |

| 1-Year Stock Return | 11.8% |

| Average LTV | 59% |

Atrium Mortgage Investment Corporation Overview

Key Investment Details

-

Minimum Investment: 1 share

-

Stock Symbol: AI

-

Lending Focus: Urban areas including Ontario, British Columbia

-

Property Type Focus:

-

Residential

-

Commercial

-

Corporate Profile Atrium Mortgage Investment Corporation is strategically positioned within major Canadian urban centers, particularly focusing on the Greater Toronto Area (GTA) and Vancouver, while also extending operations throughout Ontario and parts of British Columbia and Alberta. The corporation predominantly invests in first mortgages but also maintains a diverse portfolio that includes second and third mortgages as well as commercial loans.

Financial and Operational Highlights Since 2001, Atrium has consistently distributed monthly dividends without interruption and dispenses a special dividend every February. This practice ensures that all of Atrium's net earnings are returned to shareholders, effectively exempting the corporation from paying income taxes.

Portfolio Composition A significant portion of Atrium’s portfolio, 88.5%, is comprised of residential mortgages, predominantly targeting mid-rise and high-rise developments. The remaining 11.5% of the portfolio is dedicated to commercial properties. Despite an average mortgage size of $3.6 million, the majority of mortgages within Atrium's portfolio are valued below $2.5 million, underscoring their focused market segment.

This summary encapsulates Atrium's commitment to providing stable and consistent returns through meticulously managed mortgage investments in high-demand urban areas.

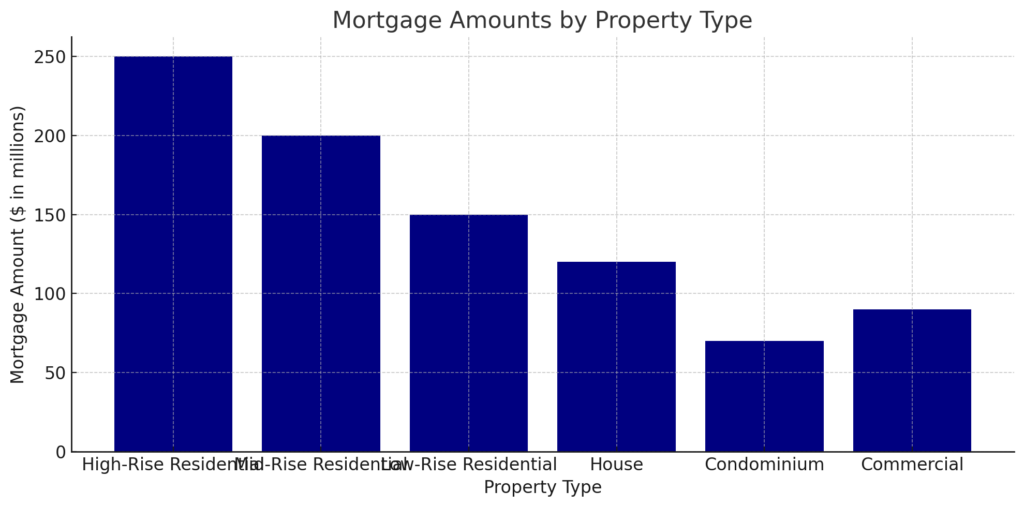

Atrium Mortgage Types

| Mortgage Type | Number | Amount | Share (%) |

|---|---|---|---|

| High-Rise Residential | 17 | $257 million | 31.4% |

| Mid-Rise Residential | 32 | $245 million | 30.0% |

| Low-Rise Residential | 13 | $120 million | 14.7% |

| House | 145 | $105 million | 12.8% |

| Condominium | 12 | $1.5 million | 0.2% |

| Commercial | 24 | $89 million | 10.9% |

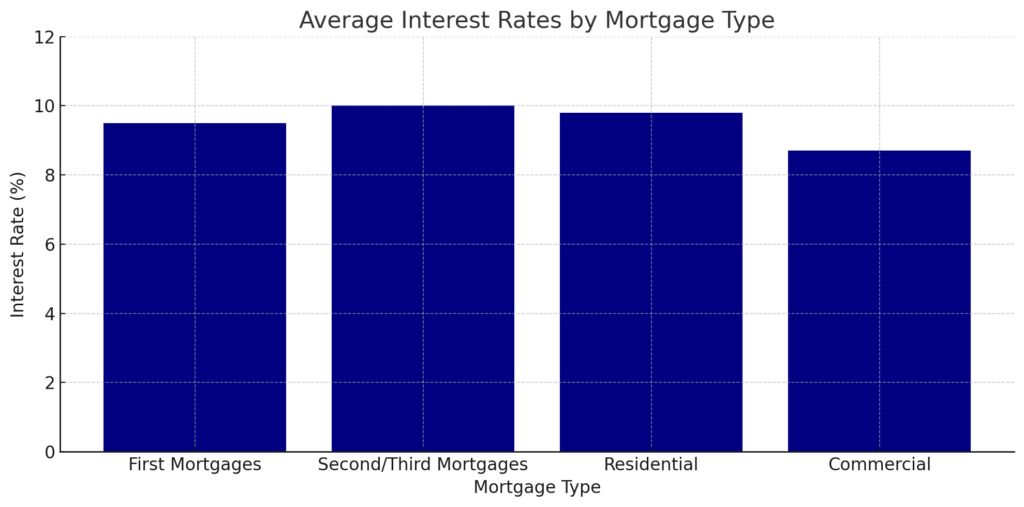

Atrium Average Mortgage Rates

| Mortgage Type | Average Interest Rate |

|---|---|

| First Mortgages | 8.81% |

| Second/Third Mortgages | 9.99% |

| Residential | 9.44% |

| Commercial | 8.84% |

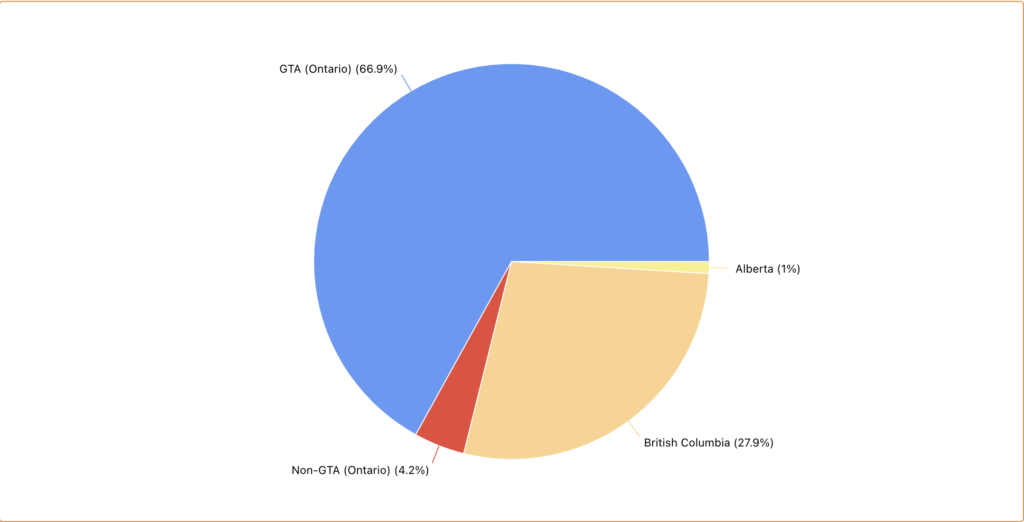

Atrium Mortgages by Province

| Province | Mortgages | Share (%) |

|---|---|---|

| GTA (Ontario) | $547 million | 66.9% |

| Non-GTA (Ontario) | $34 million | 4.2% |

| British Columbia | $228 million | 27.9% |

| Alberta | $8 million | 1% |

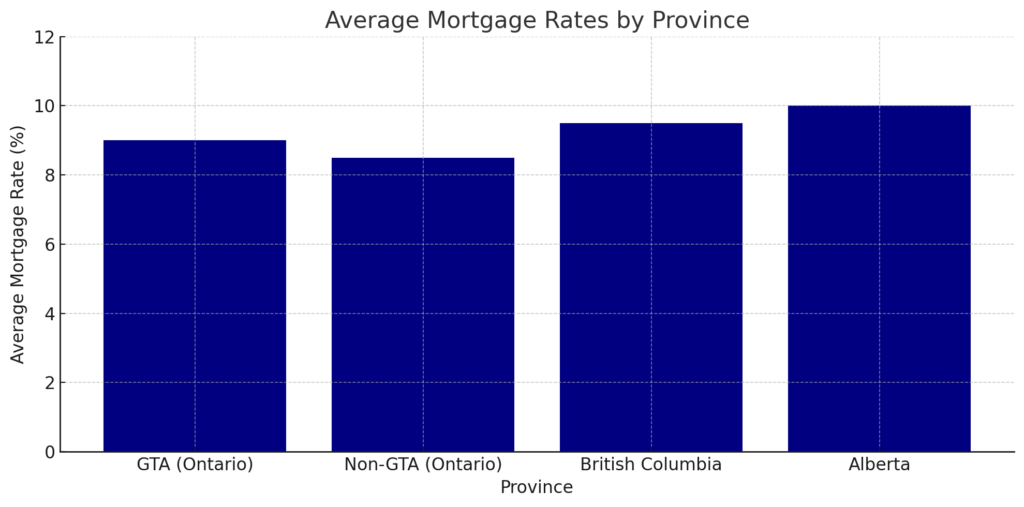

Atrium Average Mortgage Rates by Province

| Province | Average Mortgage Rate |

|---|---|

| GTA (Ontario) | 9.06% |

| Non-GTA (Ontario) | 7.44% |

| British Columbia | 8.7% |

| Alberta | 10.15% |

Cannect MIC Investment Summary

| Metric | Value |

|---|---|

| Historical Rate of Return | 8.6% |

| Annual Fee | 2% |

| Average LTV | 50% |

Cannect Mortgage Investment Corporation Overview

Key Investment Details

-

Minimum Investment: $10,000

-

Annual Management Fee: 2%

-

Exempt Market Dealer: Meadowbank Asset Management

-

Lending Focus: Ontario

-

Property Type Focus:

-

Residential

-

Commercial

-

Construction

-

Corporate Profile Cannect Mortgage Investment Corporation, established a decade ago, primarily serves the Toronto and Greater Toronto Area (GTA). As a private MIC, Cannect does not offer publicly traded shares; instead, investments are made through a Cannect Invest account, which accommodates a range of account types including non-registered accounts, TFSAs, RRSPs, RRIFs, RESPs, joint, and business accounts. Central 1 Trust Company acts as the trustee for registered accounts.

Investment Limits and Conditions Investment limits vary based on investor status:

-

Accredited Investors: No investment limit.

-

Eligible Investors: Can invest up to $30,000.

-

Non-Eligible Investors: Limited to $10,000.

-

Investors advised by portfolio managers, investment dealers, or exempt market dealers may invest up to $100,000.

Strategic Approach Cannect employs a direct approach to both raising capital and lending, ensuring a close connection with investors and consumers. The corporation is notable for its significant holdings in second mortgages, making up 40% of its portfolio, and maintains a lower-than-average loan-to-value (LTV) ratio to mitigate risk.

Fees and Liquidity Cannect charges a 2% annual management fee and imposes additional fees for early withdrawals:

-

Withdrawals within the first 12 months incur a 5% fee.

-

Withdrawals typically take up to 30 days to process, reflecting the less liquid nature of investments in a private MIC.

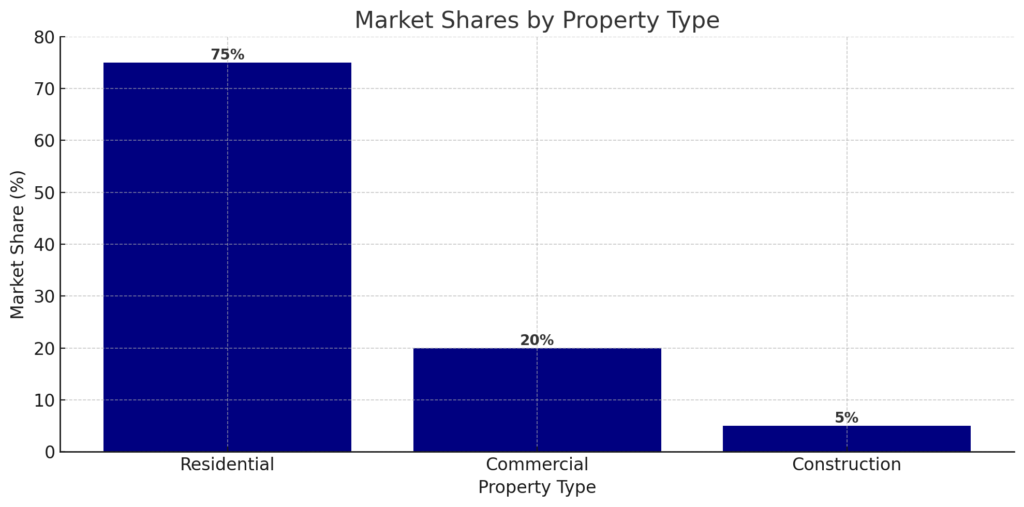

Cannect Mortgage Types

| Mortgage Type | Share (%) |

|---|---|

| Residential | 68.6% |

| Commercial | 19.2% |

| Construction | 12.2% |

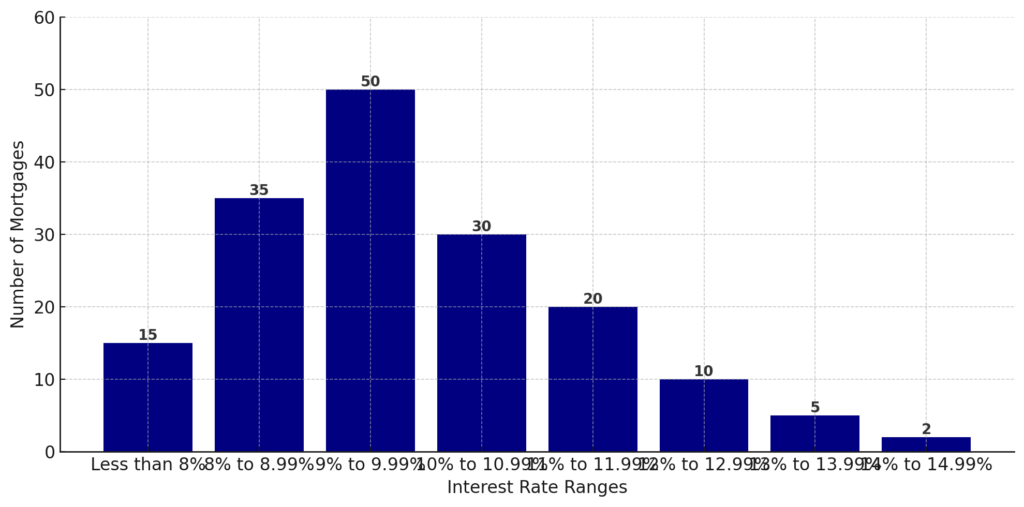

Cannect Mortgage Rates

| Interest Rate | Number of Mortgages | Average LTV |

|---|---|---|

| Less than 8% | 17 | 36.4% |

| 8% to 8.99% | 44 | 55.7% |

| 9% to 9.99% | 31 | 55.5% |

| 10% to 10.99% | 18 | 62.1% |

| 11% to 11.99% | 10 | 63.7% |

| 12% to 12.99% | 5 | 63.2% |

| 13% to 13.99% | 1 | 61.9% |

| 14% to 14.99% | 2 | 66.7% |

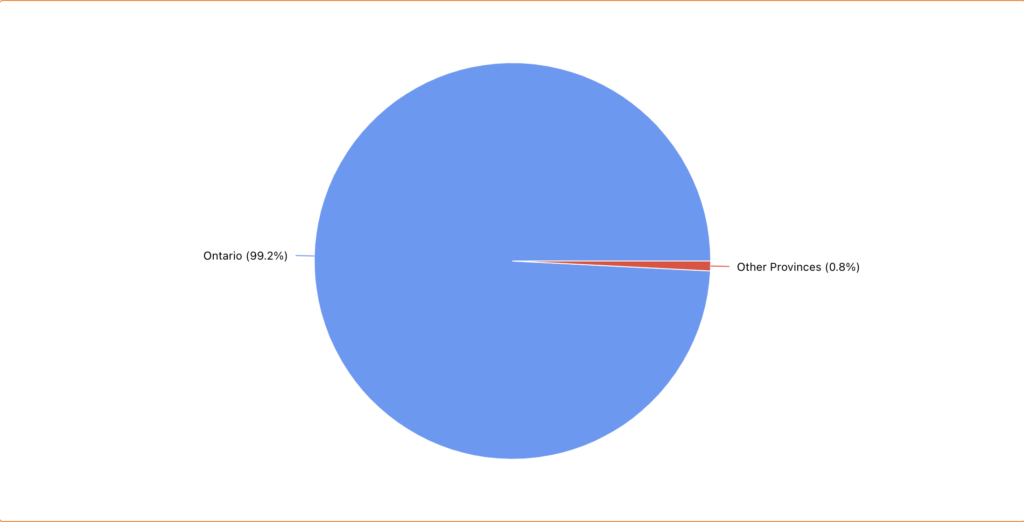

Cannect Mortgages by Province

| Province | Share (%) |

|---|---|

| Ontario | 99.2% |

| Other Provinces | 0.8% |

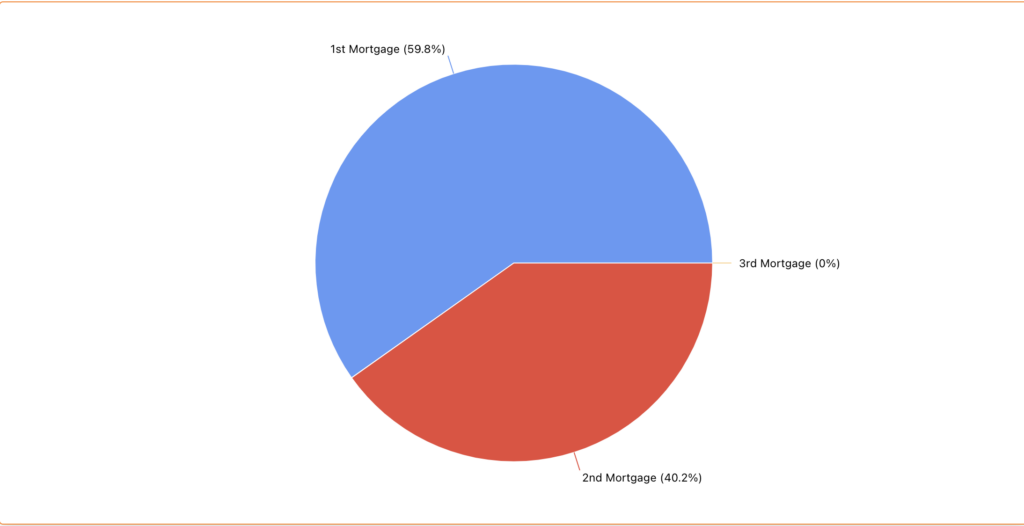

Cannect Mortgage Position

| Mortgage Position | Share (%) |

|---|---|

| 1st Mortgage | 59.8% |

| 2nd Mortgage | 40.2% |

| 3rd Mortgage | 0% |

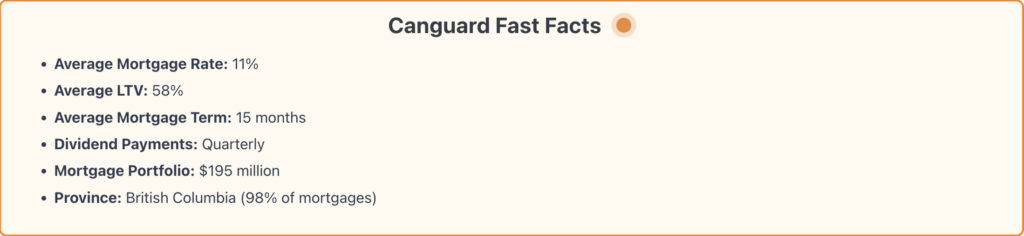

Canguard MIC Investment Summary

| Metric | Value |

|---|---|

| Annual Dividend Yield | 9.5% |

| Administration Fee | 1.5% |

| Average LTV | 54% |

Canguard Mortgage Investment Corporation Overview

Investment Essentials

-

Minimum Investment: $10,000

-

Annual Administration Fee: 1.5%

-

Exempt Market Dealer: Kite Financial Solutions Ltd.

-

Lending Focus: British Columbia

-

Property Type Focus:

-

Residential

-

Commercial

-

Construction

-

Agricultural

-

Operational Focus Canguard operates exclusively within British Columbia, concentrating its efforts in areas like Surrey/White Rock and Vancouver. This private, open-fund MIC primarily issues secured mortgages, with residential properties making up just over 50% of its portfolio, adhering to the stipulations of the Income Tax Act. Additionally, it manages a substantial number of residential land development, construction, and commercial agricultural loans, diversifying its investments throughout the province.

Financial Practices and Policies Canguard's investment strategy is to secure mortgages with a maximum Loan-to-Value (LTV) ratio of 75%, maintaining an average mortgage term of 15 months, predominantly in first mortgages. In 2022, a small portion of its portfolio, 3.82%, faced foreclosure.

Canguard is unique in its lending criteria, as it does not require a minimum credit score or impose debt service ratio limits, and it permits interest-only payments. It supports borrowers who may not have conventional proof of income, such as self-employed individuals, by allowing stated income. Additionally, it levies a lending fee ranging from 1% to 2% for terms ranging from one to two years.

Investment Conditions for Clients The corporation assesses a monthly-paid annualized administration fee of 1.5% to its investors, who do not receive any of the typical loan fees, generally about 1% to 2% of the mortgage principal. Canguard offers investment opportunities in registered accounts like RRSPs or TFSAs through Olympia Trust Company, exclusively available to British Columbia residents.

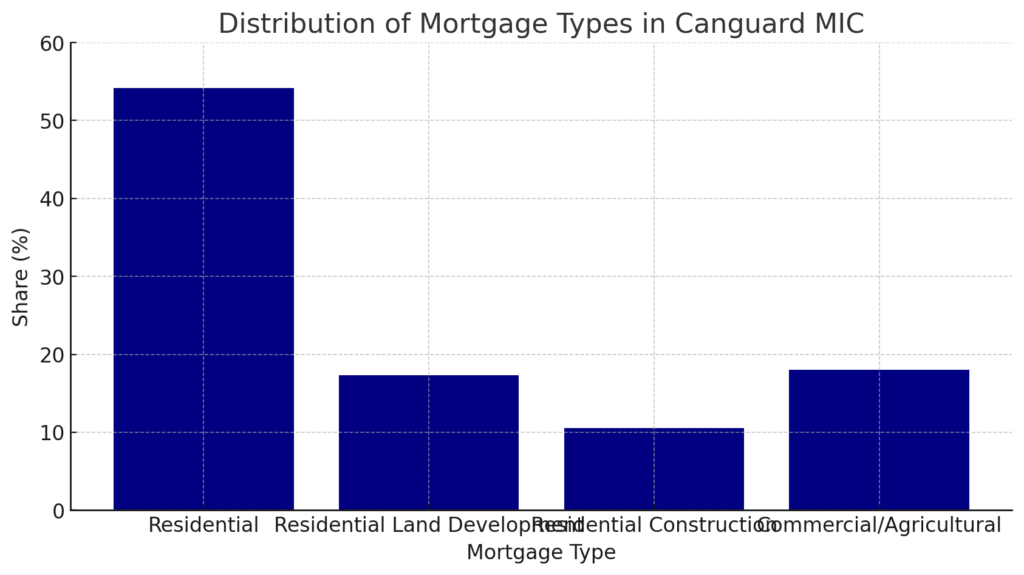

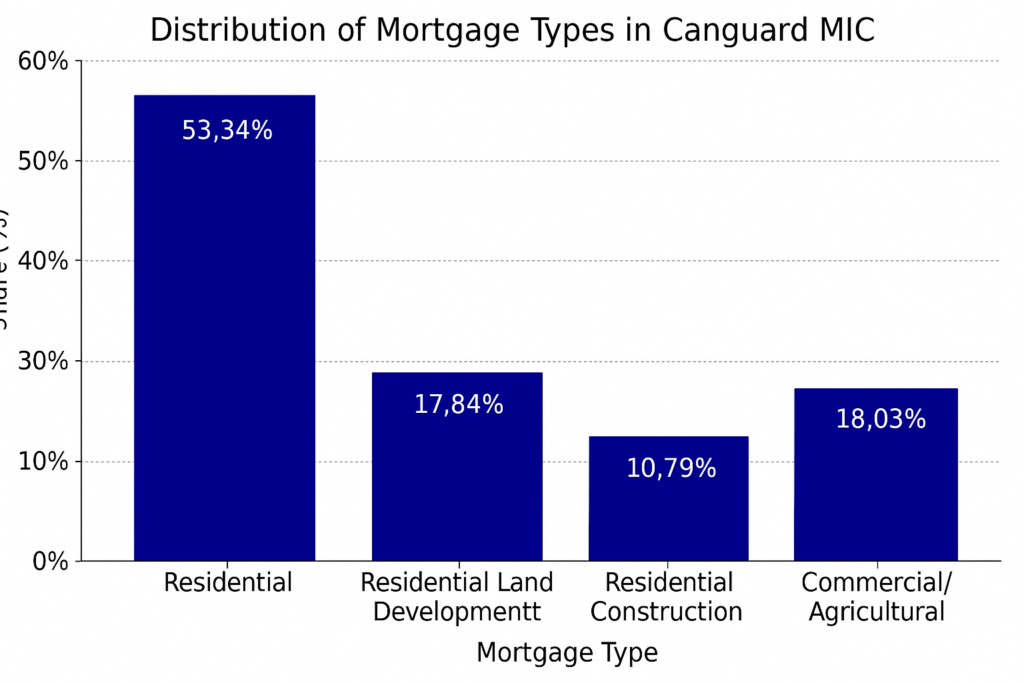

Canguard Mortgage Types

Advertisement

| Mortgage Type | Share (%) |

|---|---|

| Residential | 53.34% |

| Residential Land Development | 17.84% |

| Residential Construction | 10.79% |

| Commercial/Agricultural | 18.03% |

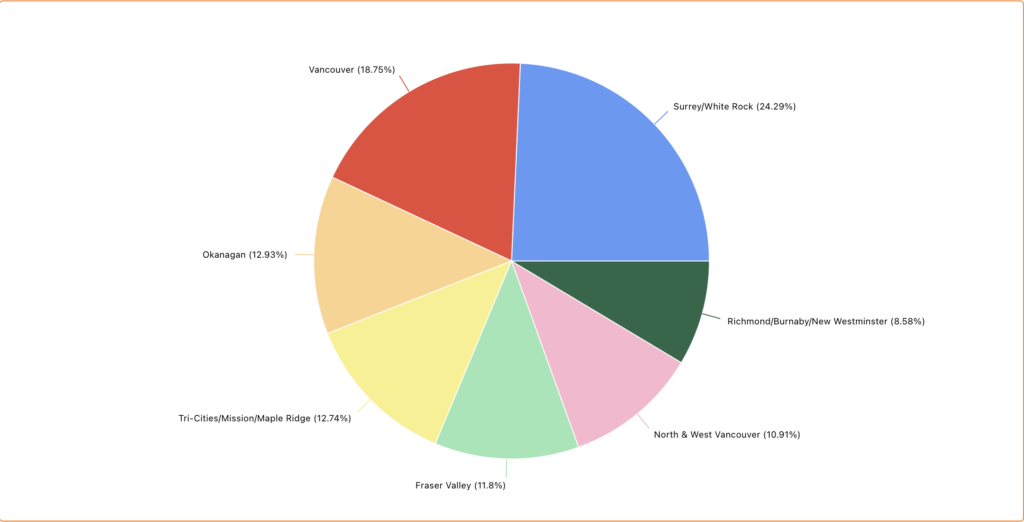

Canguard Mortgages by Area

| Area | Share (%) |

|---|---|

| Surrey/White Rock | 24.29% |

| Vancouver | 18.75% |

| Okanagan | 12.93% |

| Tri-Cities/Mission/Maple Ridge | 12.74% |

| Fraser Valley | 11.8% |

| North & West Vancouver | 10.91% |

| Richmond/Burnaby/New Westminster | 8.58% |

Canguard Mortgages by Province

| Province | # of Mortgages |

|---|---|

| British Columbia | 121 |

| Alberta | 1 |

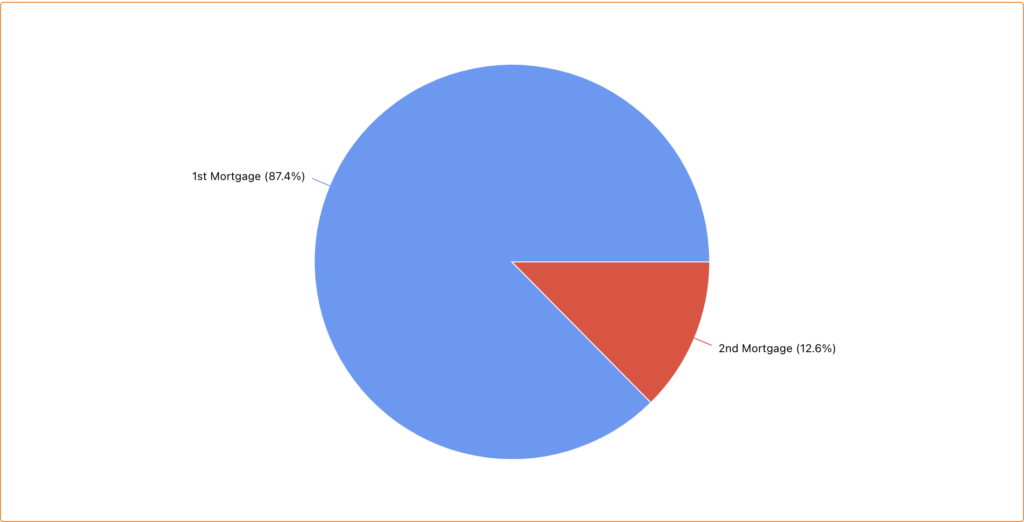

Canguard Mortgage Position

| Mortgage Position | Share (%) |

|---|---|

| 1st Mortgage | 87.4% |

| 2nd Mortgage | 12.6% |

Firm Capital MIC Investment Summary

| Metric | Value |

|---|---|

| Annual Dividend Yield | 9.5% |

| 1-Year Stock Return | -9.5% |

| 10-Year Stock Return | 5.2% |

| Average Mortgage Rate | 11.1% |

Firm Capital Mortgage Investment Corporation Overview

Investment Details

-

Minimum Investment: Purchase as little as one share.

-

Stock Symbol: FC

-

Lending Focus: Ontario

-

Property Type Focus:

-

Residential

-

Commercial

-

Company Profile Firm Capital Mortgage Investment Corporation (FCMIC) is a publicly listed Mortgage Investment Corporation (MIC) on the Toronto Stock Exchange under the ticker symbol FC. Firm Capital is dedicated to achieving returns that exceed the 1-year Government of Canada treasury bill yields by 400 basis points. As of September 2023, the investment portfolio boasts an average rate of 11.1%, yielding a return of over 9%.

Operational Focus Predominantly operating in Southern Ontario, Firm Capital manages a portfolio where 95% of the mortgages are variable, and 76% are set to mature within 12 months, all maintaining a Loan-to-Value (LTV) ratio below 75%. The corporation has been actively managing its mortgage investment portfolio since its inception in October 1999.

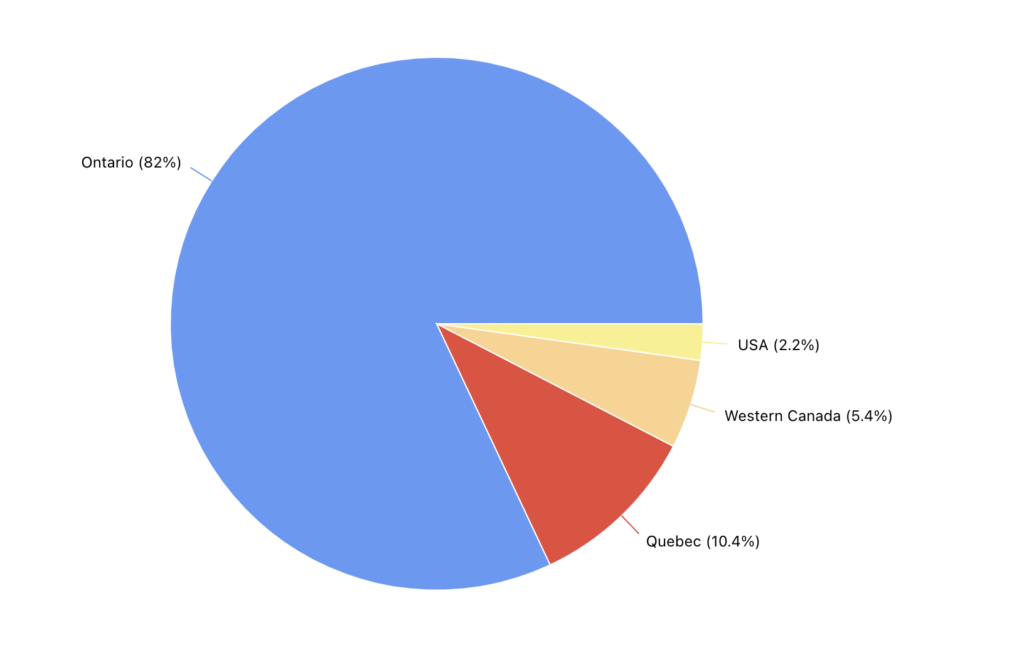

Geographical Distribution A significant 54% of Firm Capital’s portfolio is concentrated in the Greater Toronto Area (GTA), with 33.5% located in other parts of Ontario. The company also holds a smaller portfolio in Quebec, Western Canada, and the United States, diversifying its investment reach beyond its primary market.

This overview encapsulates Firm Capital’s strategic approach to mortgage lending, focusing on generating robust returns and maintaining a diverse and secure portfolio.

Firm Capital Mortgages by Province

| Province | Share (%) |

|---|---|

| Ontario | 82% |

| Quebec | 10.4% |

| Western Canada | 5.4% |

| USA | 2.2% |

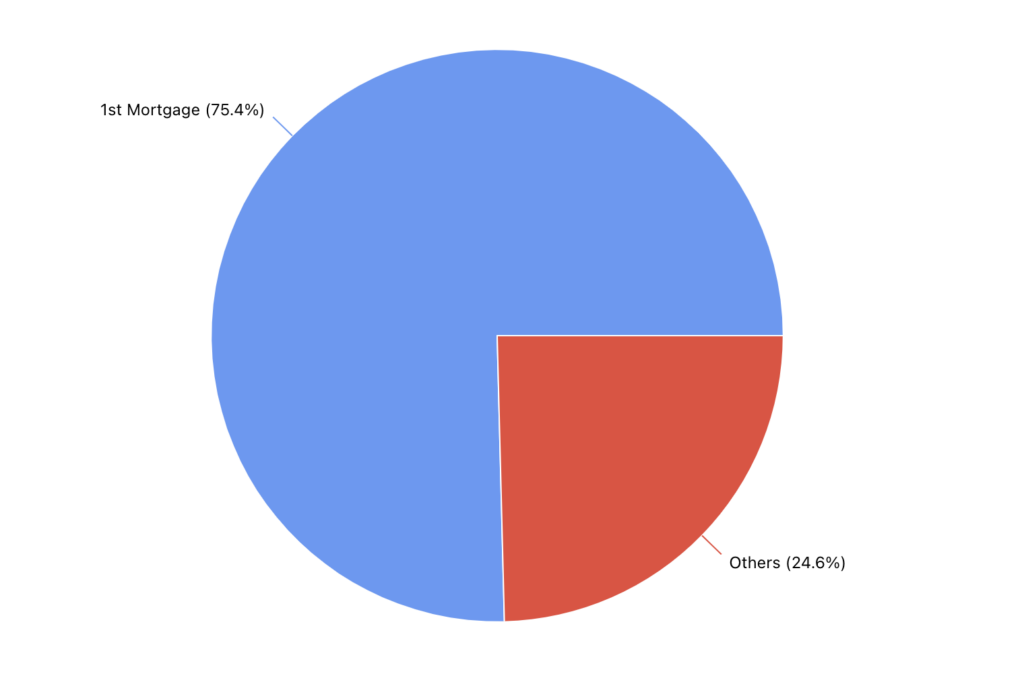

Firm Capital Mortgage Position

| Mortgage Position | Share (%) |

|---|---|

| 1st Mortgage | 75.4% |

| Others | 24.6% |

RiverRock MIC Investment Summary

| Metric | Value |

|---|---|

| Annual Dividend Yield | 8% |

| Mortgage Terms | 1 Year |

| Average LTV | 68% |

RiverRock Mortgage Investment Corporation Overview

Investment Details

-

Minimum Investment: $150,000 for non-accredited investors; $25,000 for accredited investors.

-

Annual Administration Fee: 1.25% for Series F; 2.25% for Series N.

-

Exempt Market Dealer: Donville Kent Asset Management Inc.

-

Lending Focus: Ontario

-

Property Type Focus: Residential

Company Profile RiverRock Mortgage Investment Corporation specializes in providing residential mortgages in Ontario. It targets a specific market segment including newcomers to Canada, individuals with poor credit scores, and self-employed borrowers. RiverRock's mortgage offerings are characterized by a one-year term and a maximum Loan-to-Value (LTV) ratio of 80%, with an average LTV of 68% across its portfolio, indicating a higher risk profile compared to other MICs.

Investor Terms and Liquidity RiverRock positions itself as a less liquid investment option, requiring investors to hold their shares for at least one year before eligibility for redemption. Following this period, Class A shares can be redeemed quarterly, while Class A1, F, and N shares require six months' notice prior to redemption. This structure is designed to stabilize the fund's capital base, providing a more secure foundation for mortgage lending despite its less flexible redemption terms compared to other open-end MICs.

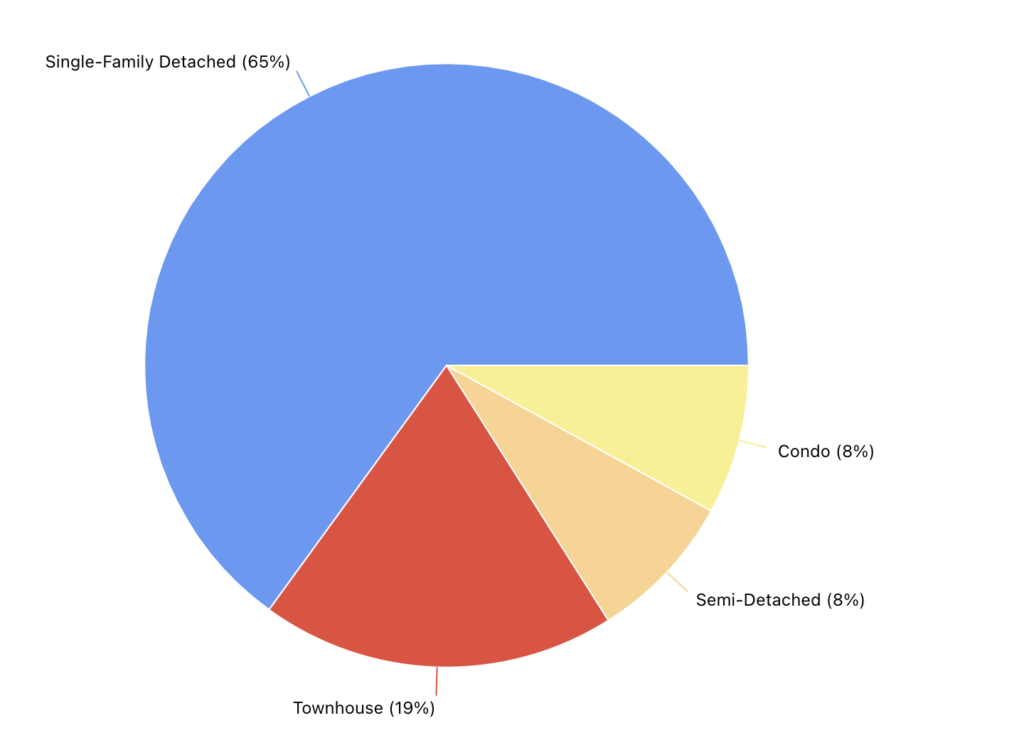

RiverRock Mortgage Types

| Mortgage Type | Share (%) |

|---|---|

| Single-Family Detached | 65% |

| Townhouse | 19% |

| Semi-Detached | 8% |

| Condo | 8% |

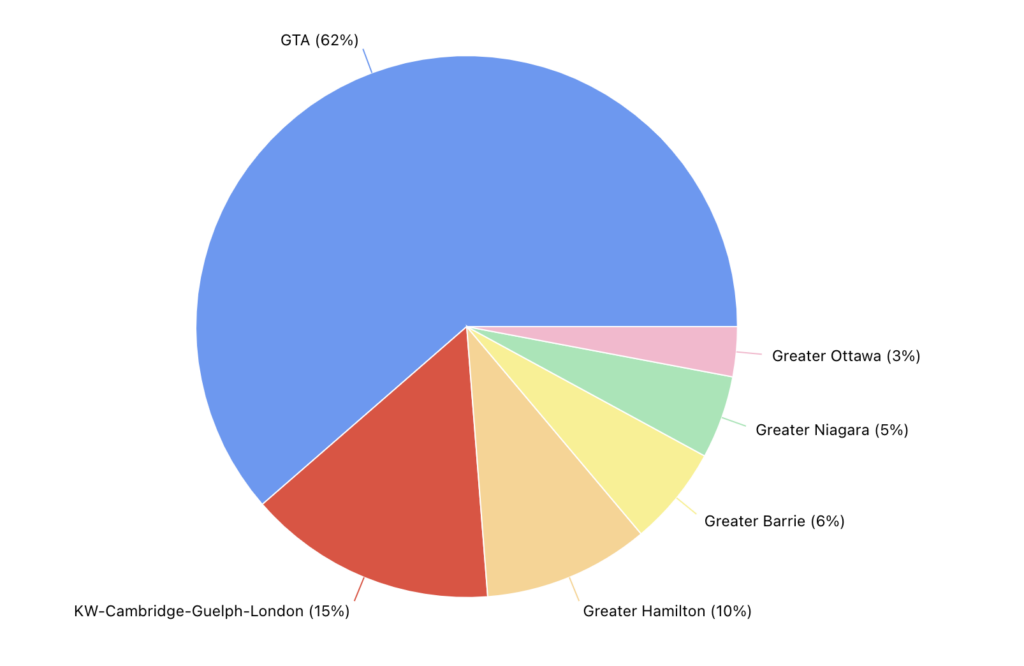

RiverRock Mortgages by Area

| Area | Share (%) |

|---|---|

| GTA | 62% |

| KW-Cambridge-Guelph-London | 15% |

| Greater Hamilton | 10% |

| Greater Barrie | 6% |

| Greater Niagara | 5% |

| Greater Ottawa | 3% |

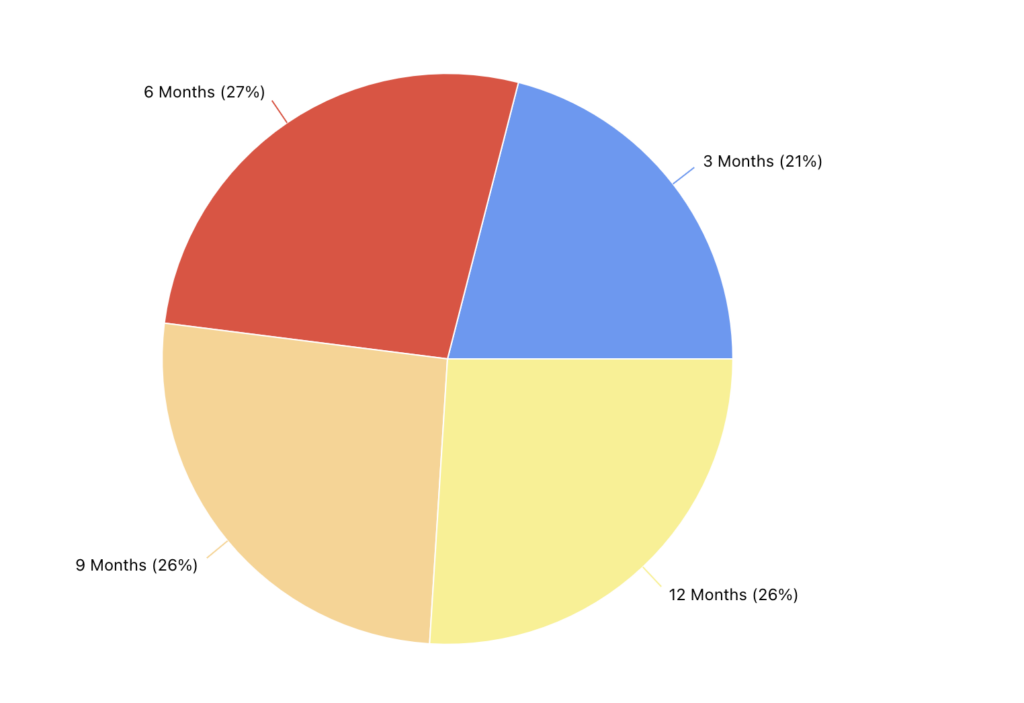

RiverRock Mortgage Maturities (Remaining)

| Area | Share (%) |

|---|---|

| 3 Months | 21% |

| 6 Months | 27% |

| 9 Months | 26% |

| 12 Months | 26% |

CMI MIC Investment Summary

| Metric | Value |

|---|---|

| Annual Dividend Yield | 6% - 11% |

| Annual Fee | 1% |

| Average LTV | 68% |

CMI MIC Overview

Investment Essentials

-

Minimum Investment: $5,000

-

Annual Management Fee: 1%

-

Exempt Market Dealer: Corton Capital

-

Lending Focus: Urban

-

Property Type Focus: Residential

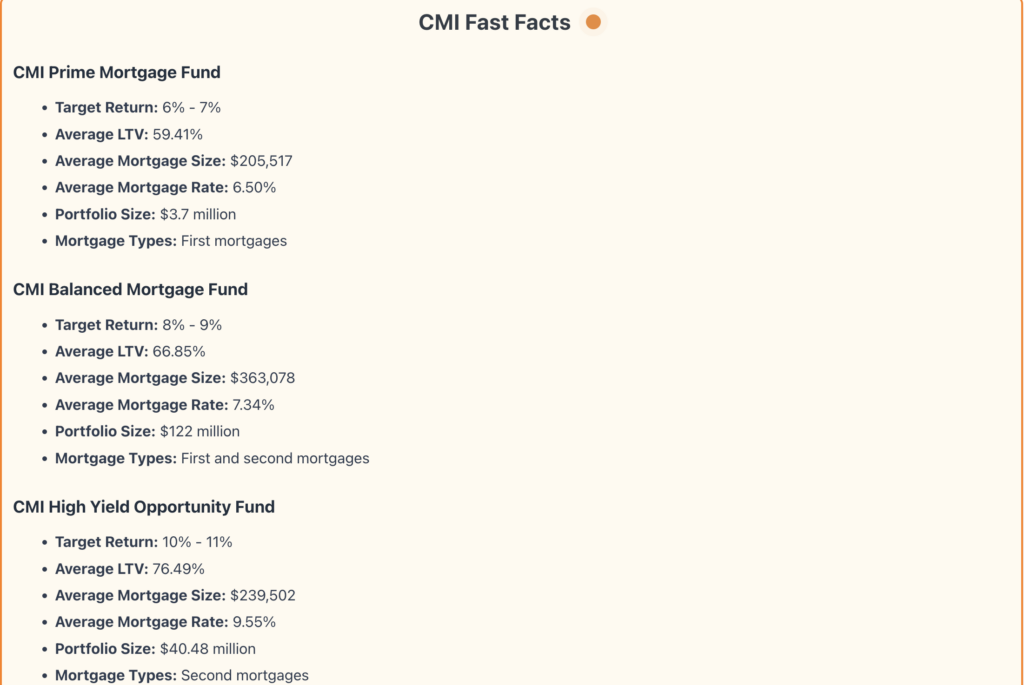

Company Profile Canadian Mortgages Inc. (CMI) operates as a private Mortgage Investment Corporation (MIC) specializing in urban residential properties across Ontario, British Columbia, Alberta, Nova Scotia, and Newfoundland & Labrador. CMI offers a structured investment approach with a $5,000 minimum investment threshold and a standard 1% management fee across all portfolios. Additionally, a performance fee of 20% is levied on returns that exceed predetermined targets annually.

Investment Portfolios

-

Prime Mortgage Fund: Targeted at conservative investors seeking to reduce volatility, this fund maintains mortgage Loan-to-Value (LTV) ratios at a maximum of 65% and primarily invests in first mortgages. It typically delivers annual returns between 6% and 7%.

-

Balanced Mortgage Fund: Designed for those seeking moderately higher returns, this fund mixes first and second mortgages with an LTV cap of 75%, aiming for returns between 8% and 9%.

-

High Yield Opportunity Fund: Geared towards aggressive investors comfortable with higher risk levels, this fund focuses on second mortgages with an LTV limit of 85% and targets annual returns of 10% to 11%.

Operational Highlights CMI's newest fund, the Prime Mortgage Fund, launched in July 2020, extends the option for quarterly redemptions, providing investors with relatively frequent liquidity opportunities within the constraints of a private MIC framework.

This summary outlines CMI’s commitment to offering diversified mortgage investment opportunities tailored to varying investor risk tolerances, facilitated through structured portfolio strategies.

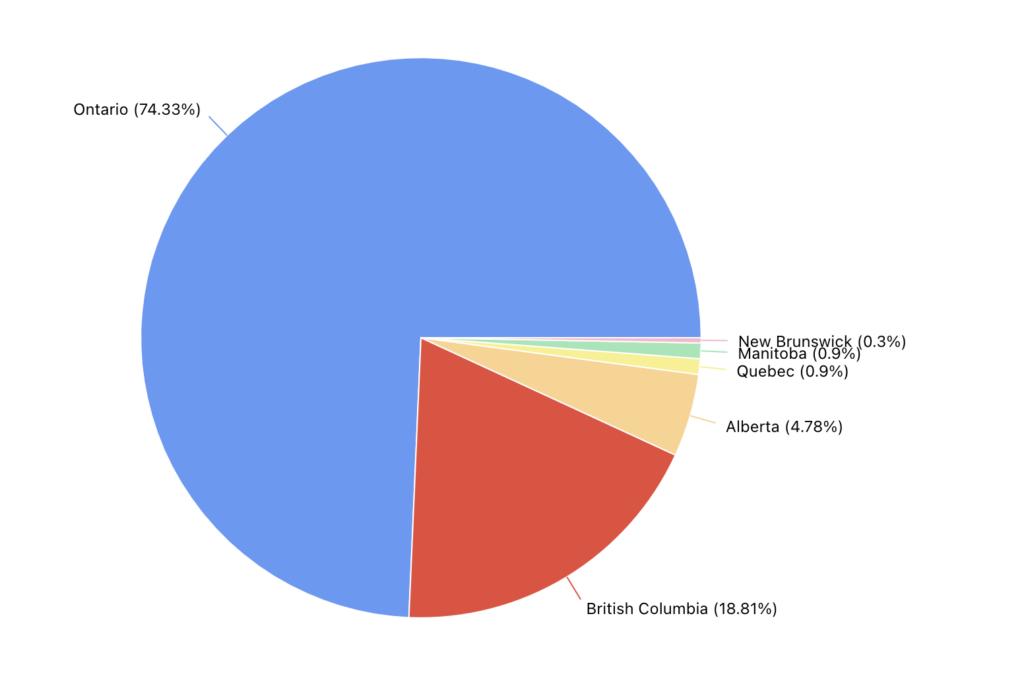

CMI Mortgages by Province

| Province | Share (%) |

|---|---|

| Ontario | 74.33% |

| British Columbia | 18.81% |

| Alberta | 4.78% |

| Quebec | 0.9% |

| Manitoba | 0.9% |

| New Brunswick | 0.3% |

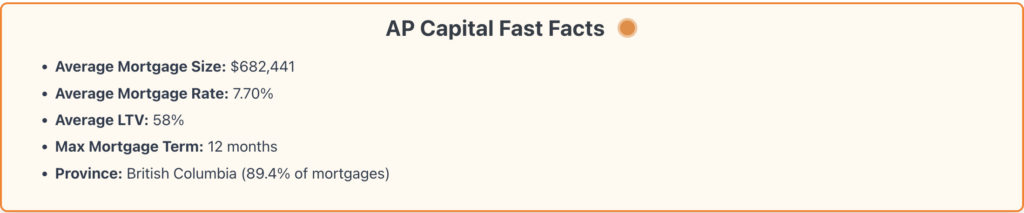

AP Capital Investment Summary

| Metric | Value |

|---|---|

| Annual Dividend Yield | 8% |

| Annual Fee | 1.5% |

| Average LTV | 58% |

AP Capital MIC Overview

Investment Essentials

-

Minimum Investment: $10,000

-

Annual Management Fee: 1.5%

-

Exempt Market Dealer: Diversifi Alternative Investments Ltd

-

Lending Focus: Western Canada

-

Property Type Focus: Residential

Company Profile AP Capital MIC primarily operates within the urban markets of Western Canada, focusing on British Columbia and Alberta. The investment corporation specializes in residential first mortgages, particularly targeting single-family detached homes in Vancouver and the Fraser Valley. A significant portion of the portfolio comprises non-owner occupied homes, such as second homes and investment properties.

Investment Terms and Conditions As a private Mortgage Investment Corporation, AP Capital mandates a minimum investment of $10,000 and imposes a 60-day notice period for redemptions. It levies a 1.5% annual management fee. The MIC's mortgage sizes are generally larger than average due to the dynamic housing market in British Columbia.

Investor Composition and Options The majority of AP Capital's investors, approximately 70%, hold non-registered (cash) accounts, while 30% maintain registered accounts. The corporation offers a Dividend Reinvestment Plan (DRIP), utilized by 44% of its investors. Conversely, 56% of the investors prefer receiving monthly cash distributions. As of September 2023, AP Capital experienced a foreclosure rate of 5% on its mortgages.

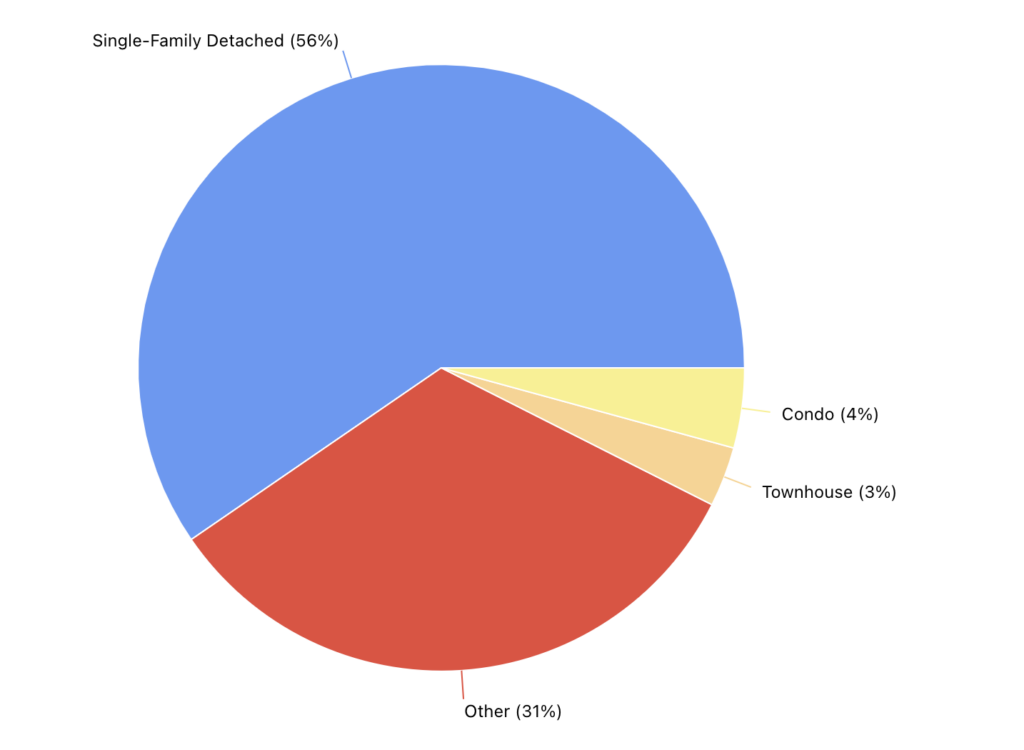

AP Capital Mortgage Types

| Mortgage Type | Share (%) |

|---|---|

| Single-Family Detached | 56% |

| Other | 31% |

| Townhouse | 3% |

| Condo | 4% |

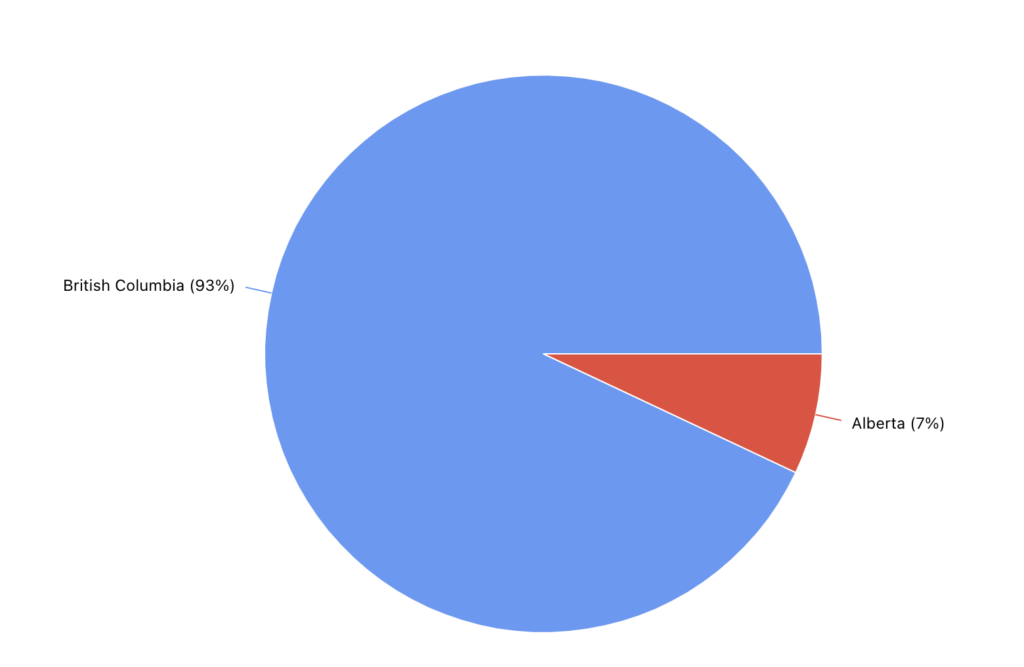

AP Capital Mortgages by Province

| Province | Share (%) |

|---|---|

| British Columbia | 93% |

| Alberta | 7% |

Timbercreek Financial Investment Summary

| Metric | Value |

|---|---|

| Annual Dividend Yield | 10.7% |

| 1-Year Stock Return | -8.9% |

| Average LTV | 67% |

Timbercreek Financial Overview

Investment Details

-

Minimum Investment: Purchase as little as one share.

-

Stock Symbol: TF

-

Annual Management Fee: 0.85%

-

Lending Focus: Across Canada

-

Property Type Focus:

-

Multi-Residential

-

Commercial

-

Company Profile Timbercreek Financial is a publicly traded Mortgage Investment Corporation (MIC) specializing in lending for income-producing, multi-residential, and commercial properties across Canada. With an average mortgage size of $10.5 million, Timbercreek manages a substantial portfolio, boasting $3 billion in assets. Beyond Canada, Timbercreek extends its financial services internationally, originating mortgages in the United States, Ireland, and the United Kingdom.

Investment Strategy and Portfolio Composition Timbercreek's investment strategy emphasizes commercial and multi-residential properties that generate regular income, which is crucial for enhancing overall portfolio yield. The portfolio predominantly consists of properties with variable interest rates, with 87% of the mortgages set to floating rates. Notably, 89.3% of the mortgages are directed towards income-producing properties, of which 64.9% are multi-residential, underlining Timbercreek's focus on stable and high-yield investment opportunities.

About MICs in Canada

Understanding Mortgage Investment Corporations (MICs) in Canada

Regulatory Framework for MICs

MICs are regulated under section 130.1 of the Income Tax Act, with specific guidelines ensuring operational integrity:

-

Must be a registered Canadian corporation.

-

Solely focused on lending funds, not permitted to manage or develop real estate directly.

-

Investments are restricted within Canada and cannot be extended to foreign properties or non-Canadian corporate shares.

-

A minimum of 20 shareholders is required, with no single shareholder owning more than 25% of total shares.

-

At least half of the MIC's assets must be in debts secured by residential properties as defined in the National Housing Act or related housing projects.

-

No more than 25% of the assets can be invested in properties not acquired through foreclosure or default.

Investing in MICs

MICs can be either public or private entities:

-

Public MICs: These are listed on stock exchanges and shares can be bought and sold freely through brokers, offering lower entry barriers.

-

Private MICs: More restrictive, these MICs require dealings through financial advisors and often cater to specific investor categories. Investments here are less liquid, with entrance thresholds and investment limits set based on an investor's accreditation status.

Tax Implications and Benefits

MICs operate as flow-through entities, meaning the corporation itself doesn't pay taxes on the income it generates. Instead, the tax obligation transfers directly to the shareholders who treat the income as personal income, thus avoiding double taxation—a benefit not available in typical corporate investments. This setup effectively lowers the tax burden compared to other investment vehicles.

Investment Conditions for Different Investor Types

-

Accredited Investors: Typically face no investment cap.

-

Eligible Investors: May have investment limits, e.g., $30,000.

-

Non-Eligible Investors: Often restricted to lower investment thresholds.

Exempt Market Dealers (EMDs) For private MICs, investments are facilitated through EMDs who assess and validate investor eligibility, ensuring compliance with financial regulations and suitability standards.

Potential for Enhanced Returns in Registered Accounts MICs are permissible in registered accounts like RRSPs, TFSAs, and RESPs, which can shield investment returns from taxes, potentially enhancing net gains.

Engagement and Qualification Criteria Engaging with a MIC through an EMD involves an assessment process where investor qualifications are verified, determining investment capabilities and limitations based on financial status.

This overview encapsulates how MICs function within Canada's financial landscape, offering insights into their structure, regulatory compliance, and the nuanced investment opportunities they present across different investor profiles.

Best next step

Keep exploring this topic

If you want to go deeper, these are the most useful follow-up pages and tools for this topic.

Stocks tool

Check Canadian stock movers

See the latest TSX and TSXV winners and losers before digging deeper into a sector.

Research hub

Browse Canadian stock research

Use the stock section to jump from a theme article into individual company pages.

Diversification

Compare stocks with ETF options

If you want exposure to a theme without single-stock risk, screen matching ETFs instead.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Qayyum Rajan, CFA

Qayyum is the CEO of Wealth Awesome, a leading Canadian personal finance publication. As a CFA charterholder with extensive experience in fintech, data science, and quantitative finance, he brings a unique analytical perspective to investing and wealth management.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.