CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

Aren’t we always on the verge of SOME kind of crash??

Canada's housing market has been a topic of intense debate and concern for years. Recent data suggests that the Canadian housing bubble has reached unprecedented levels, even compared to other G7 nations, raising alarms about its sustainability.

Advertisement

The Extent of Canada's Housing Bubble

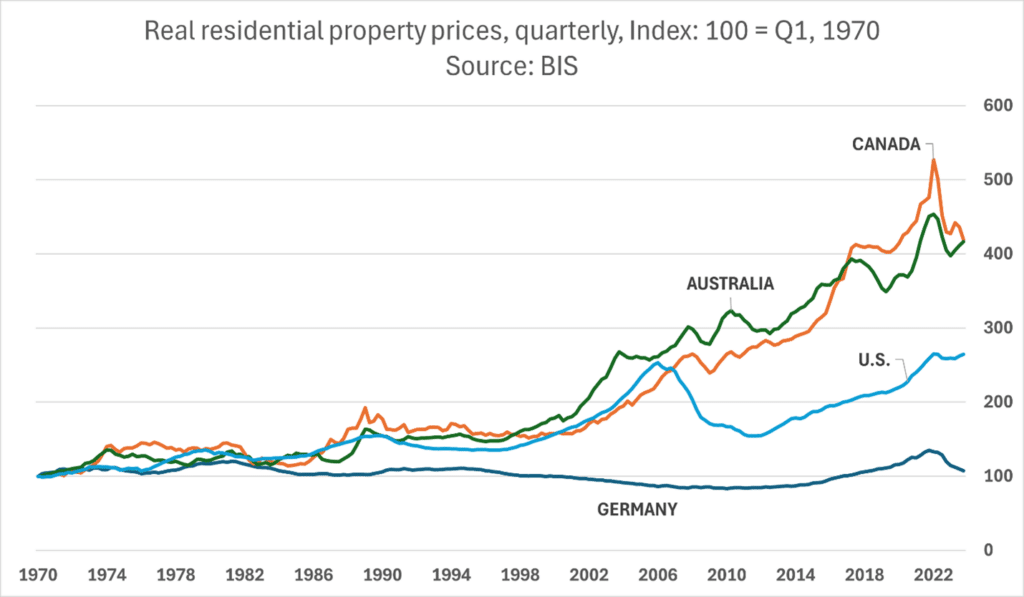

According to the Bank for International Settlements (BIS), real residential house prices in Canada have grown by more than four-fold since 1970. This staggering increase means that house prices have far outpaced inflation, making housing in Canada extremely unaffordable compared to historical norms and other countries.

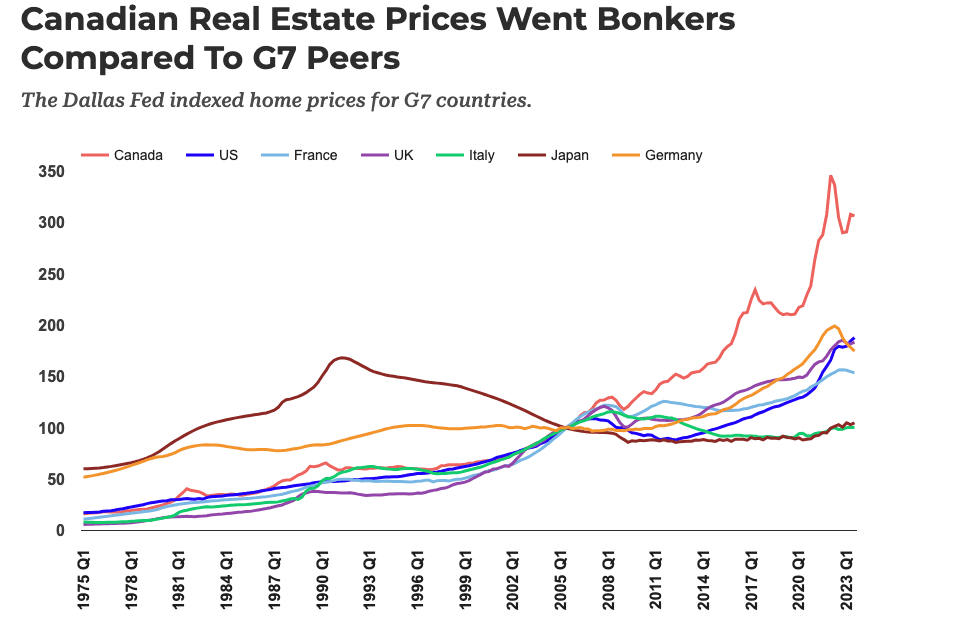

A recent report from the US Federal Reserve Bank of Dallas provides further evidence of Canada's exceptional housing market. In the first quarter of 2022, Canada's Housing Price Index (HPI) saw an increase of 59% compared to the same period in 2020, reaching a peak of 346.15. While prices have since dipped, with Q3 2023 showing an HPI of 306.76, this still represents a significant bubble compared to other G7 nations.

Comparing Canada to Other G7 Countries

When looking at the housing markets of other G7 countries, Canada's situation stands out:

-

United States: The US housing market tracked Canada's bubble until 2006 when the subprime mortgage crisis caused a 38% price drop. Since then, US prices have rebounded but not to the extent seen in Canada.

-

Germany: Unlike Canada, Germany has never experienced a significant housing bubble, largely due to stricter mortgage lending rules. As a result, only about 40-50% of Germans are homeowners, with the remainder living as long-term renters.

-

Australia: The Australian housing market shows similarities to Canada's, with both countries experiencing significant price growth over the past decades.

-

Other G7 nations: Countries like France, the UK, Italy, and Japan have seen housing price increases, but none have reached the levels observed in Canada.

Factors Fuelling the Bubble

Several key factors have contributed to Canada's housing bubble:

-

Low interest rates: From 2010 to 2020, interest rates were kept close to zero, making borrowing cheap and fueling housing demand.

-

Generous mortgage terms: Lenders provided large amounts of credit on favorable terms to many borrowers, often with the assumption that rising house prices would sustain these loans.

-

Population growth: Canada's booming population has outpaced housing supply, putting upward pressure on prices.

-

High household debt: According to the Canada Mortgage and Housing Corporation (CMHC), Canada has the highest household debt levels in the G7, with mortgages accounting for about three-quarters of this debt.

Signs of a Potential Crash

While the housing market has shown resilience, there are increasing signs of stress:

-

Rising interest rates: Rates have increased from below 1% on variable mortgages to more than 5%, making it difficult for many households to meet their financial obligations.

-

Increasing delinquencies: Equifax reported that for the first time since 2020, Canadian households are starting to miss mortgage payments. In Ontario, total mortgage balances reaching "severe delinquency" exceeded $1 billion for the first time.

-

Growing unemployment: The unemployment rate in Ontario has reached 6.7%, which could further pressure the housing market.

-

Price corrections: While modest so far, some areas are seeing price declines as the market adjusts to new economic realities.

The Potential Impact of a Crash

If the Canadian housing bubble bursts, the consequences could be severe:

-

Widespread foreclosures: As more homeowners struggle with payments, foreclosure actions could push prices significantly lower.

-

Economic ripple effects: A housing crash could have far-reaching impacts on Canada's overall economy, affecting everything from consumer spending to construction employment.

-

Financial system stress: With high household debt levels, a crash could put significant strain on Canada's banking and financial systems.

Can the Canadian Housing Market Be Fixed?

Addressing Canada's housing bubble will require a multi-faceted approach:

-

Stricter lending rules: Following Germany's example of more conservative mortgage lending practices could help stabilize the market.

-

Increased housing supply: Efforts to boost housing construction to meet population growth could help alleviate price pressures. The Canada's National Housing Strategy aims to address this issue.

-

Gradual market correction: Allowing for a controlled decline in prices over time might help avoid a sudden, devastating crash.

-

Policy interventions: The Bank of Canada's monetary policy and government housing policies will play crucial roles in shaping the market's future.

As Canada grapples with its housing bubble, policymakers, lenders, and homeowners will need to work together to navigate the challenges ahead. The coming months and years will be crucial in determining whether Canada can achieve a soft landing or if it will face the harsh reality of a housing market crash.

For those concerned about the housing market, staying informed through resources like the Canadian Real Estate Association (CREA) and Statistics Canada can help in making informed decisions in these uncertain times.

Frequently Asked Questions about Canada's Housing Bubble

Advertisement

Q1: What is a housing bubble?

A: A housing bubble occurs when house prices rise to levels significantly above their real value. In Canada's case, real residential house prices have grown more than four-fold since 1970, far outpacing inflation and income growth.

Q2: How does Canada's housing market compare to other G7 countries?

A: Canada's housing market has experienced more significant growth compared to most G7 countries. While countries like the US experienced a major correction in 2008, and Germany has maintained stable prices due to stricter lending rules, Canada's market has continued to grow almost uninterrupted until recently.

Q3: What factors have contributed to Canada's housing bubble?

A: Several factors have fueled Canada's housing bubble:

-

Low interest rates from 2010 to 2020

-

Generous mortgage terms

-

Population growth outpacing housing supply

-

High levels of household debt

Q4: Are there signs that Canada's housing bubble might burst?

A: Yes, there are several warning signs:

-

Rising interest rates making mortgages less affordable

-

Increasing mortgage delinquencies

-

Growing unemployment rates

-

Early signs of price corrections in some areas

Q5: What could be the consequences of a housing market crash in Canada?

A: A housing market crash could lead to:

-

Widespread foreclosures

-

Significant economic ripple effects, impacting consumer spending and employment

-

Stress on Canada's banking and financial systems

Q6: How does Canada's household debt compare to other countries?

A: According to the Canada Mortgage and Housing Corporation (CMHC), Canada has the highest household debt levels among G7 countries, with mortgages accounting for about three-quarters of this debt.

Q7: What measures could be taken to address Canada's housing bubble?

A: Potential solutions include:

-

Implementing stricter lending rules

-

Increasing housing supply to meet population growth

-

Allowing for a gradual market correction

-

Government policy interventions, such as the National Housing Strategy

Q8: How high have interest rates risen in Canada recently?

A: Interest rates on variable mortgages have increased from below 1% to over 5% in recent years, significantly impacting affordability for many homeowners.

Q9: Are some regions in Canada more affected by the housing bubble than others?

A: While the article doesn't specify regional differences, it's worth noting that housing markets can vary significantly across different provinces and cities in Canada. Urban centers like Toronto and Vancouver have traditionally seen higher prices and more significant growth.

Q10: Where can I find reliable information about Canada's housing market?

A: Reliable sources for information on Canada's housing market include:

-

The Canadian Real Estate Association (CREA)

-

Statistics Canada

-

The Bank of Canada

-

Canada Mortgage and Housing Corporation (CMHC)

Best next step

Keep exploring this topic

If you want to go deeper, these are the most useful follow-up pages and tools for this topic.

Stocks tool

Check Canadian stock movers

See the latest TSX and TSXV winners and losers before digging deeper into a sector.

Research hub

Browse Canadian stock research

Use the stock section to jump from a theme article into individual company pages.

Diversification

Compare stocks with ETF options

If you want exposure to a theme without single-stock risk, screen matching ETFs instead.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.