CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

If you’re shopping around for a robo-advisor in Canada, you must take a close look at Wealthsimple Invest.

Wealthsimple Invest is the leading robo-advisor in Canada, with over 1.5 million customers and $15 billion in assets under management (AUM).

Robo-advisors have soared in popularity in Canada and the U.S. recently due to their effective system of investing in exchange-traded funds (ETFs) with low fees.

Advertisement

Do Wealthsimple’s products and features justify its massive asset under management (AUM)? Or is the company all hype and no substance?

Let’s take a peek into all the details with this Wealthsimple Canada review.

During the March 2020 market crash, Canadian ETFs still saw an inflow of $2.9 billion.

Pros

Cons

What is Wealthsimple?

Although Wealthsimple has launched a wide variety of products, at its core, Wealthsimple is an online investment management company. The company tries to live up to its namesake of keeping investing simple, which should be the overall goal of all robo-advisors.

Wealthsimple was launched in 2014 and has since grown rapidly. By 2021, they received $750 million dollars in funding at a $5 billion valuation.

Who owns Wealthsimple: Power Corporation of Canada owns the majority of Wealthsimple. Power Corp is a massive company, with a market cap of over $12 billion and owns numerous financial assets in Canada.

Wealthsimple Invest - Main Product

If you’re wondering how Wealthsimple works, you’re probably thinking about Wealthsimple Invest. Wealthsimple Invest is the core product of the company.

Wealthsimple follows the strategy of passive investing, where you buy and hold ETFs that invest in its benchmark index. Your portfolio returns should track that market very closely.

With a robo-advisor like Wealthsimple, they'll handle all of the rebalancing and ETF selection, so you don't have to lift a finger.

Passive investing could potentially outperform active investing due to a few key reasons:

-

Lower fees: Canadian mutual funds are notorious for having very high fees

-

Lower transaction costs: Because you’re only buying and holding, you won’t be hit with many trading or transaction costs.

-

Modern portfolio theory: By investing in the entire market across different countries and sectors, you will be well diversified. Diversification is key in this proven theory to minimize risk and maximize return.

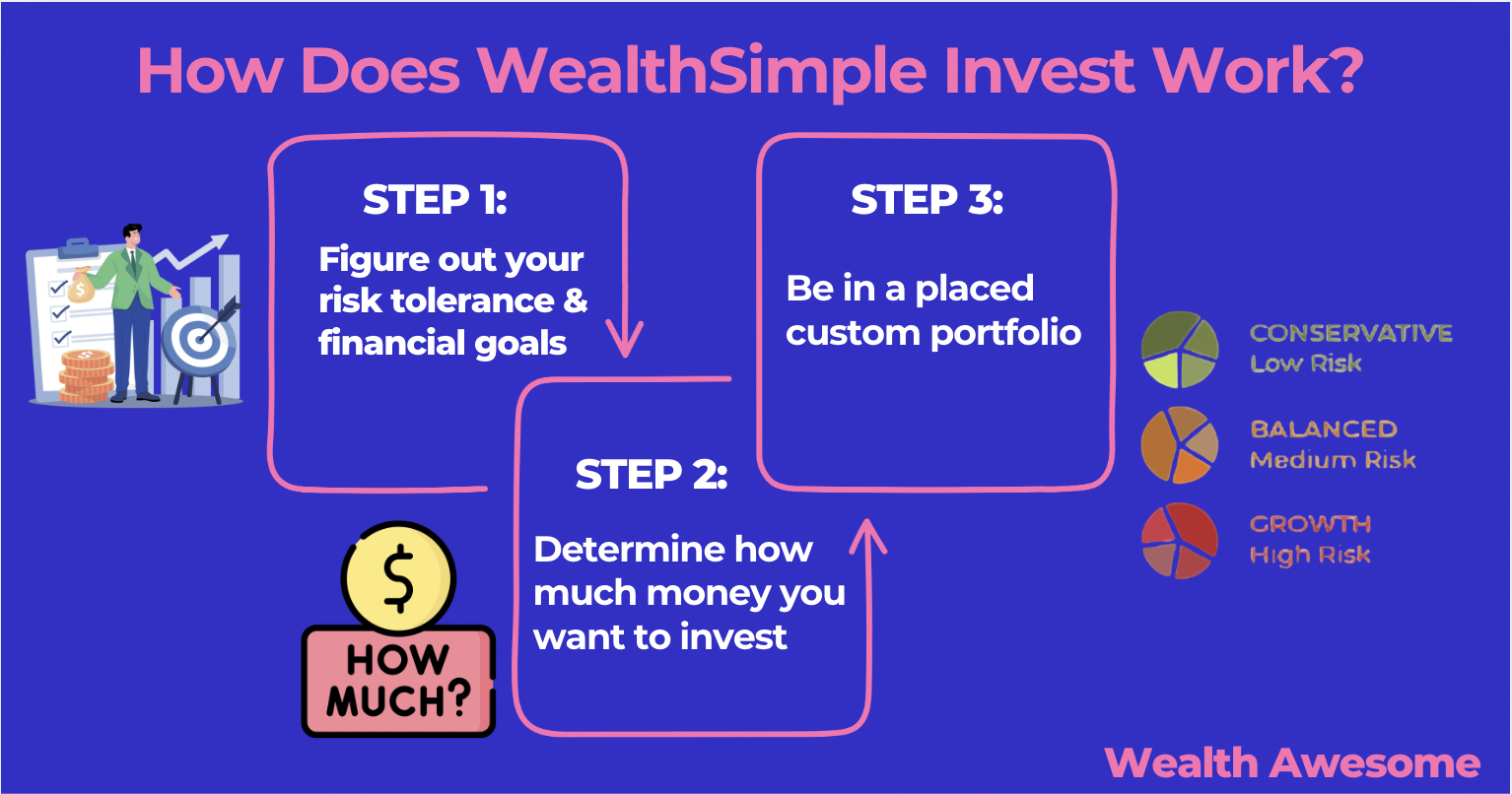

How Does Wealthsimple Invest Work

Wealthsimple Invest is essentially a low-fee portfolio of ETFs that’s structured to meet your financial goals and risk tolerance.

It’s an easy three-step process:

Step 1. Figure out your risk tolerance and financial goals

When you sign up for Wealthsimple, you’ll complete an online questionnaire that will determine your risk tolerance and financial goals. If you have any questions, an actual human advisor can help you over the phone, email, or live chat.

You can even get a full portfolio review completed by a Wealthsimple advisor, which I recommend you go through. This first step of figuring out your goals and risk tolerance is crucial, and I recommend you spend enough time going through this.

Step 2. Determine how much money you want to invest

Wealthsimple has no minimums, so you can invest any amount you’d like.

Step 3. Be placed in a custom portfolio

You’ll be placed in a portfolio of ETFs that suit your financial goals, risk tolerance, and time horizon.

What Wealthsimple Invests In

Wealthsimple keeps it straightforward by having only three main portfolios, with a different mix of stocks and fixed income. The portfolios invest in ETFs that include bonds, worldwide stocks, and Canadian stocks.

Here are the asset allocations for the conservative, balanced, and growth portfolios:

1. Wealthsimple Conservative Portfolio Asset Allocation

Asset allocation: ~35% Equity, 65% Fixed Income

2. Wealthsimple Balanced Portfolio Asset Allocation

Asset allocation: ~50% Equity, 50% Fixed Income

3. Wealthsimple Growth Portfolio Asset Allocation

Asset allocation: ~75-90% Equity, 10-25% Fixed Income

➡️ Wealthsimple Signup - $50 Cash Bonus

Legal Disclaimer for Wealthsimple

Wealthsimple Portfolios Holdings (Canada)

Wealtsimple invests in a combination of eight different exchange-traded funds (ETFs), all of which are publicly traded.

The portfolios give you access to global exposure to bonds and stocks:

Wealthsimple Performance

As you move from the Wealthsimple Conservative to Growth Portfolio, you should expect larger variations in your Wealthsimple returns in the short term because of the higher investments in stocks.

Stocks are more volatile than bonds, so the potential for larger short-term losses or gains is higher with the growth portfolio than with the conservative one.

This also means that the growth portfolio has a higher long-term return potential than the conservative portfolio.

The illustration below is a useful visual that shows how in the short-term 1-year returns, the growth portfolio can vary greatly, but this volatility will narrow over a longer time frame.

Illustrative purposes only

Wealthsimple Conservative Portfolio Performance

Risk tolerance: Low

Time horizon: Short

With the conservative portfolio, you should expect the least amount of variation for returns but a lower portfolio performance in the long term.

Wealthsimple Balanced Portfolio Performance

Risk tolerance: Medium

Time horizon: Medium

With a balanced portfolio, you should expect a medium amount of variation for returns and medium portfolio performance in the long term.

Wealthsimple Growth Portfolio Performance

Risk tolerance: High

Time horizon: Long

With the growth portfolio, you should expect the highest amount of variation for returns and the highest portfolio performance in the long term.

Wealthsimple Fees

How does Wealthsimple make money: Mainly by collecting fees from investors in its portfolios.

Wealthsimple Management Fees

Core: Under $100,000 – 0.5%

Premium: $100,000–$500,000 – 0.4%

Generation: $500,000+ – 0.2%–0.4%

Wealthsimple MER

On top of the fees that Wealthsimple charges, there are also fees charged by the investment fund managers of the portfolio. These fees are called the management expense ratio (MER).

-

Classic Portfolios: 0.12%–0.15%

-

SRI Portfolios: 0.21%–0.23%

-

Halal Portfolios: 0.25%–0.50%

| Wealthsimple Save | Fee |

|---|---|

| Above $1 | None |

Wealthsimple Other Products

Wealthsimple has an impressive and wide range of products. The company seems to be in tune with what Canadian investors are looking for, and has launched a series of products that are aimed to suit those needs:

1. Wealthsimple Trade

Summary: Commission-free stock and ETF trades

Wealthsimple trade is the most impressive new product that Wealthsimple has come out with. It is a platform that allows you to make commission-free stock and ETF trades, similar to Robinhood in the U.S.

The zero commissions are a fantastic offering and could cut down on your trading costs significantly if you transact frequently.

Be aware that if you’re trading international or U.S. stocks that aren’t traded on Canadian stock exchanges, a foreign exchange fee will be added to the trade unless you purchase a Plus subscription.

Read my full Wealthsimple Trade Review here.

2. Wealthsimple Cash

Features:

-

No-fee everyday spending account

-

Earn competitive interest on your balance

-

Free Visa debit card (tungsten design)

-

Free e-transfers and bill payments

-

ATM access across Canada

-

No foreign transaction fees

Wealthsimple Cash is also a fantastic new offering by Wealthsimple. The Wealthsimple savings account provides a higher savings interest rate than the big banks in Canada.

Wealthsimple Cash is now a full everyday spending and savings account with a Visa debit card, ATM access, free e-transfers and bill payments, competitive interest, and no foreign transaction fees.

3. Wealthsimple SimpleTax

Features:

-

Tax-filing software: Easy to use and file taxes

-

Free to use: The software is free to use, but you can choose to donate whatever amount you’d like.

In 2019, Wealthsimple purchased the Vancouver fintech company SimpleTax. SimpleTax is a free tax filing software for Canadians. It’s free to use and accepts donations only.

The software is easy and intuitive, with a sleek-looking design.

I think it’s a great acquisition by Wealthsimple, and it will only help to grow trust in its brand by providing these outstanding free services for Canadian customers.

You can use Simpletax to file this year’s taxes at simpletax.ca.

Wealthsimple Unique Investment Options

1. Wealthsimple Socially Responsible Investing (SRI)

Summary:

-

Ethical investing: Environment, social, and governance threshold

-

Fast-growing sector: 30% of assets in Canada are SRI

-

Three portfolios are available: Conservative, balanced, and growth option.

-

Higher fees: Higher MER than normal portfolios

Socially responsible investing (SRI) has seen considerable growth, with more than $22 trillion invested worldwide in SRI funds. It seems more people are more conscience about choosing ethical ways to invest.

The fees for managing a Wealthsimple SRI portfolio will be significantly higher. For example, for the SRI growth portfolio, the MER is 0.43%.

This is almost triple the normal Wealthsimple Growth portfolio MER of 0.16%. Combined with Wealtsimple’s fee of 0.5%, you will be paying 0.93% total for the growth SRI portfolio, which is getting quite pricey.

The higher costs go towards making sure that the companies invested in meet the SRI thresholds. Over one year, this doesn’t make much of a difference in returns, but compounded over the long term can be a significant difference.

Because of the higher fees, the SRI portfolios will likely underperform the normal portfolios over the long term.

Advertisement

2. Wealthsimple Halal

Summary:

-

Build a Halal portfolio: Your investments will comply with Halal law

-

Investment screening: By third-party Shariah scholars

-

Uses individual stocks: Instead of ETFs, uses stocks

-

Three portfolios are available: Conservative, Balanced, and Growth

-

No fixed income: Instead of fixed income, the portfolios use cash.

If you follow the Islamic principles of investing, there are several rules you must follow. You can’t take on or profit from debt, so bonds and other fixed-income are not available.

You also can’t invest in companies that profit off things such as gambling, alcohol, tobacco, pork, and weapons, among other things.

Wealthsimple Halal abides by these rules and is a good option for those who also follow these principles.

The portfolio is available for anyone to invest in, but be aware that it is an all-equity portfolio.

Wealthsimple Accounts

You can open almost any type of investment account in Canada with Wealthsimple Invest:

-

TFSA

-

RRSP

-

Spousal RRSP

-

Non-registered Account

-

Wealthsimple Cash

-

RESP

-

RRIF

-

LIRA

-

LIF

-

Corporate

Wealthsimple Account Tiers

Wealthsimple offers three main tiers depending on how much you invest across your accounts:

Core

**Summary:

**Assets under $100,000

Management fee: 0.5% per year

Features:

-

Automated ETF portfolios

-

Access to Wealthsimple Invest and Trade

-

Basic financial tools and support

Premium

**Summary:

**$100,000–$500,000 invested

Management fee: 0.4% per year

Features:

-

All Core features

-

Enhanced financial planning support

-

Priority customer service

Generation

**Summary:

**$500,000+ invested

Management fee: 0.2%–0.4% per year

Features:

-

All Premium features

-

Dedicated team of advisors

-

Advanced, holistic financial planning

How to Open a Wealthsimple Account

It’s easy to open a new account with Wealthsimple, and is only a few simple steps. You will be ready to go in minutes:

-

Visit the Wealthsimple website ($10,000 is managed for free)

-

Enter your information

-

Answer the investment questionnaire. With this questionnaire, you’ll receive a customized plan with your recommended portfolio. The plan is customized to your risk tolerance, time horizons, and investment goals.

-

Choose an account to open, such as a TFSA, RRSP, LIRA, etc, or you can transfer one from another provider.

-

Transfer in your money. And that’s it! You’re ready to invest.

Wealthsimple App

The platforms available are:

-

Both iOS and Android and desktop also

-

Wealthsimple now supports iOS, Android, and full desktop access for both Invest and Trade. This makes it easier to manage your portfolio from any device.

Is Wealthsimple safe and legit?

-

256-bit encryption: Uses the same encryption as all the major banks for digital protection.

-

2-factor authentication: Added security feature that you can enable

-

$1,000,000 Insurance: CIPF coverage

Wealthsimple is regulated by the same organizations as your regular banks, so they are just as safe and legit as a traditional bank. If they weren’t as safe, they wouldn’t have passed regulations.

The funds you invest are held with Wealthsimple’s custodial broker, ShareOwner Investment Inc, which is a member of the Canadian Investor Protection Fund (CIPF). Your assets are protected up to $1,000,000 if Wealthsimple were to go bankrupt or insolvent.

Wealthsimple is also owned by Power Financial Corporation, which is one of the world’s largest financial companies.

Wealthsimple vs Competitors

1. Questrade vs Wealthsimple Trade

Questrade is a discount brokerage popular among do-it-yourself (DIY) investors in Canada.

Wealthsimple Trade is aimed directly at enticing customers from Questrade, and it has a very strong case with its lower fees.

Comparison:

-

Wealthsimple Trade offers $0 commission trading for both ETFs and stocks (buy and sell). Questrade offers free ETF purchases only, and you must pay for ETF sales and stock buys and sells.

-

Questrade supports more accounts such as RESPs, LIRA, Margin, and Corporate.

-

Questrade has a $1,000 minimum for opening an account, and Wealthsimple Trade has no minimum.

-

Wealthsimple now offers both mobile and desktop platforms, while Questrade also offers full desktop and mobile trading.

It depends on your needs, but either of these brokerages is a solid choice for your trading needs. If you’re a frequent trader who is comfortable with trading on your mobile device, Wealthsimple is the better choice. But if you need access to accounts such as RESPs, Questrade will be the better choice.

Go here for a full comparison of Questrade vs Wealthsimple.

2. CI Direct Investing (Formerly Wealthbar) vs Wealthsimple

CI Direct Investing is another Canadian company that is similar to Wealthsimple. Because they are both robo-advisors who follow passive ETF investing for its investors, let’s focus on how they differ. I see two main ways in which the two companies are different:

Fees

-

Wealthsimple: 0.5% on assets under $100,000 (Core), 0.4% on $100,000–$500,000 (Premium), and 0.2%–0.4% on $500,000+ (Generation)

-

CI Direct Investing: 0.6% on the first $150,000, 0.4% on the next $350,000 and 0.35% above $500,000

Wealthsimple Trade

Wealthsimple offers zero-trade commission on trades, and CI Direct Investing does not, which I think is its killer feature. With both accounts offering savings accounts, zero commissions are a big bonus.

Wealthsimple also has lower fees or equal for accounts under $350,000, so that’s another plus.

3. Tangerine vs Wealthsimple

Tangerine is owned by Scotiabank and is better known as an online bank. The company also provides investment funds, which is what I will compare here:

Fees

-

Wealthsimple: 0.5% on assets under $100,000 (Core), 0.4% on $100,000–$500,000 (Premium), and 0.2%–0.4% on $500,000+ (Generation)

-

Tangerine: 1.07% on its investment funds

Savings Rates: Wealthsimple offers a higher interest rate on your savings deposits than Tangerine.

Trading: Wealthsimple allows you to trade your own ETFs and stocks with no commissions. Tangerine does not even offer trading.

My opinion: Wealthsimple is a better investing platform with commission-free trading, lower fees and a higher interest savings rate, but Tangerine has more banking features. Once Wealthsimple adds more banking features, I can’t think of any reason why you’d choose Tangerine over Wealthsimple.

4. Moka (Formerly Mylo) vs Wealthsimple

Moka is another Canadian fintech company that touts passive ETF investing. Where the companies differ is that Moka is mostly focused on investing your spare change, and they have additional features surrounding that, such as a multiplier for your round-ups.

Moka doesn’t offer nearly as many products or features as Wealthsimple. If you’re interested mainly in investing your spare change, consider Moka.

If you’re looking for more products and features, such as a savings account, a trading account, and actual robo-advising with human advisors you can talk to, I think you’re better off with Wealthsimple.

Read my full Moka Review here.

Other Options as a Canadian Investor

Let’s take a look at a few of your options for how you can start investing in Canada. A robo- advisor isn’t your only option, and you should consider all your options beforehand:

1. Do-it-yourself (DIY) investor:

Difficulty and time spent: High

Fees: Very low

Platform examples: Questrade, Qtrade

2. Robo-advisor (Like Wealthsimple)

Difficulty and time spent: Low

Fees: Low

Platform examples: Wealthsimple, Nest Wealth

3. Financial Advisor

Difficulty and time spent: Low

Fees: Generally high

Platform examples: RBC, TD, Assante

Read my full breakdown of seven other great investment options in Canada here.

Wealthsimple Withdrawal

-

Log in to your Wealthsimple account through your computer (not your mobile app!).

-

Click on your name on the top right of the screen

-

Go to the Withdrawals tab

-

Select the account and amount you want to withdraw, and click “Set withdrawal.”

You Should Use Wealthsimple If:

-

You want a low-fee robo advisor in Canada

-

You want access to savings accounts

-

You want access to a zero-commission trading account

-

You want access to a human advisor for advice

Don’t Use Wealthsimple if:

-

You are knowledgeable enough to be a do-it-yourself (DIY) investor

-

You need to see someone face-to-face for advice

Conclusion

Is Wealthsimple worth it? To me, it absolutely is. Wealthsimple has the most robust product line of any robo-advisor in Canada.

The company seems well in tune with its customers, and its product and features have proven so.

I’m excited to see what they will come out with in the future. Try out Wealthsimple Invest here.

Best next step

Keep exploring this topic

If you want to go deeper, these are the most useful follow-up pages and tools for this topic.

Stocks tool

Check Canadian stock movers

See the latest TSX and TSXV winners and losers before digging deeper into a sector.

Research hub

Browse Canadian stock research

Use the stock section to jump from a theme article into individual company pages.

Diversification

Compare stocks with ETF options

If you want exposure to a theme without single-stock risk, screen matching ETFs instead.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.