CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

13 Smart Ways to Avoid the OAS Clawback

With the cost of living on the rise in Canada, retirees need to maximize their financial resources. If you're approaching retirement, the Old Age Security (OAS) recovery tax, also known as the OAS clawback, might be a concern. Here are some updated and effective strategies to minimize or completely avoid the OAS clawback, keeping more income for your golden years in 2025.

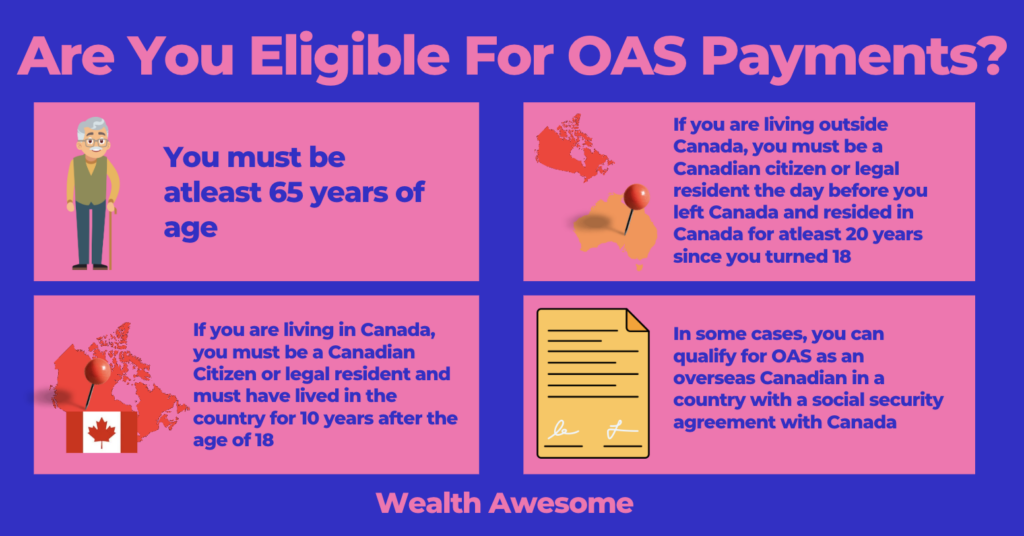

How Does the Old Age Security (OAS) Clawback Work?

Advertisement

The OAS clawback starts to kick in if your net income exceeds a certain threshold, which is set at $93,000 for 2025. If your income surpasses this limit, you will need to repay 15% of the excess income up to the maximum cap.

Deduction Timeframe and Income Reference for 2025:

| Timeframe | Income Reference Year | Minimum Deduction Income Level | Maximum Deduction Income for Ages 65-74 | Maximum Deduction Income for Age 75 and Above |

|---|---|---|---|---|

| July 2025 - June 2026 | 2025 | $93,000 | $153,000 | $158,000 |

Calculating the amount of OAS clawback involves finding the difference between your income and the threshold for that year, with 15% of this excess amount due as repayment.

Example: In 2025, the set limit is $93,000.

Suppose your 2025 income totaled $115,000. The amount to be repaid would be 15% of the difference between $115,000 and $93,000:

$115,000 - $93,000 = $22,000

$22,000 x 0.15 = $3,300

So for the period from July 2025 to June 2026, you'd be responsible for returning $3,300 as an OAS clawback.

Strategies to Minimize or Reduce Old Age Security (OAS) Clawback

-

Maximize Your TFSA: Contributions to your Tax-Free Savings Account (TFSA) are not counted as taxable income. Maximize your TFSA to shield more of your income from taxes and clawbacks.

-

Defer Your OAS: You can defer your OAS pension for up to five years starting at age 65. Each month of deferral increases your future OAS pension by 0.6%, which accumulates to a 36% increase if deferred until age 70. This also raises the income threshold at which the clawback kicks in.

-

Split Pension Income: If your spouse earns significantly less, consider splitting up to 50% of your pension income to lower your taxable income and reduce the risk of hitting the clawback threshold.

-

Defer Your CPP: Similar to OAS, you can defer your Canada Pension Plan (CPP) payments up to age 70, increasing the payment amount by 42% compared to starting at age 65, and potentially keeping your earlier retirement income below the clawback threshold. Learn more about when to take your CPP.

-

Withdraw RRSP Early: If you anticipate being in a higher tax bracket later, consider withdrawing from your RRSPs before age 65. This strategic withdrawal could reduce your total taxable income during the years you receive OAS.

Advertisement

-

Trigger Capital Gains Early: If you own assets that have appreciated in value, consider selling them before you turn 65 to avoid increasing your taxable income during the clawback period.

-

Optimize Deductions: Ensure you're claiming all possible deductions, including business expenses and investment-related expenses, to lower your taxable income.

-

Use Loan Interest Deductions: If you've borrowed money for investing, the interest you pay can be deducted from your income, potentially keeping you below the clawback threshold.

-

Careful with Dividend Income: Dividends are grossed up for tax purposes, which can inflate your reported income. Consider holding investments that do not distribute dividends directly in non-registered accounts.

-

Watch Interest Income: Interest income is fully taxable. Be cautious with how much interest you're accruing in non-registered accounts if you're close to the clawback threshold.

-

Understand Capital Gains Impacts: Only 50% of capital gains are included in your taxable income, making them more favorable than other income types for staying under the clawback limit.

-

Contribute to RRSP Post-Retirement: Continue contributing to your RRSP until age 71 if you have contribution room, to lower your taxable income during the clawback period.

-

Adjust RRIF Withdrawals: If your spouse is younger, you can base your Required Minimum Distributions (RMDs) from a Registered Retirement Income Fund (RRIF) on their age, potentially lowering the amount you must withdraw and declare as income.

Conclusion

By adopting these strategies, you can effectively manage your income and reduce or avoid the OAS clawback. Planning your finances well can help you maximize your income during retirement.

Frequently Asked Questions (FAQ)

1. What is the OAS clawback threshold for 2025? The OAS clawback threshold for 2025 is set at $93,000. Income above this level will be subject to a 15% clawback.

2. How can I calculate the OAS clawback? To calculate the OAS clawback, subtract the clawback threshold from your total income to find the excess amount. Multiply this excess by 15% to find the amount of OAS that will be clawed back.

3. Can deferring OAS and CPP benefits reduce my taxable income? Yes, deferring OAS and CPP can significantly reduce your taxable income because you delay receiving these incomes, potentially lowering your overall taxable income during the clawback period.

4. What are the best strategies to avoid the OAS clawback? The best strategies include maximizing your TFSA, deferring OAS and CPP, splitting pension income, and strategically managing RRSP withdrawals and capital gains.

5. Are there other considerations for managing OAS clawbacks? Yes, it's important to consider all income sources, including RRIF withdrawals, investment income, and any capital gains, as these can all contribute to increasing your total income and affecting your OAS benefits.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.