CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

As you approach retirement, deciding when to start receiving your Canada Pension Plan (CPP) payments is crucial. The choice to begin CPP between ages 60 and 70 offers flexibility but also requires strategic planning based on your financial situation and retirement goals.

Comparison of CPP Payouts at Ages 60, 65, and 70

Understanding the financial implications of starting CPP at different ages can help you make a more informed decision. Here’s what you might expect if you choose to begin payments at 60, 65, or 70, based on a hypothetical initial monthly payout of $1,000 at age 65:

-

Age 60: Starting CPP at 60 will reduce your monthly payments by 36% compared to starting at 65, due to early penalty reductions of 0.6% per month.

-

Age 70: Delaying your CPP until age 70 increases your payments by 42%, with an increase of 0.7% for each month you delay past 65.

Here’s how the numbers could add up over the years, assuming you live beyond ages 74 and 81, which are common benchmarks for financial planning:

When Should You Start Your CPP?

Deciding when to start your CPP involves several considerations:

-

Immediate Financial Needs: If you need income immediately at retirement, starting CPP at 60 may be beneficial despite the reduction in monthly payments.

-

Health and Life Expectancy: If you are in good health and have a family history of longevity, delaying CPP to maximize your lifetime benefits might make sense.

-

Tax Implications and OAS: Consider how your income level might impact the Old Age Security (OAS) clawback. Starting CPP later could mitigate the risk of hitting the clawback threshold.

-

Investment Opportunities: Money received earlier from CPP could potentially be invested, possibly offsetting the reduced payout from taking CPP early.

For detailed strategies and considerations, check out our guide on how to maximize your retirement income.

1. Comparison of CPP payout money you receive at 60, 65, and 70

Below is a year-by-year comparison of how much CPP you will receive at 60, 65, and 70. For simplicity's sake, I assumed a $1,000/month CPP payout at age 65.

The amount you receive could be more, but more likely will be less. The average CPP payout is around $717.15/month, but the CPP max amount for 2023 is $1,306.57/month.

Highlights of the results:

-

If you live past age 74: You will earn more money if you start the CPP payout at age 65 than at age 60.

-

If you live past age 81: You will earn more money if you start the CPP payout at age 70 than at age 65.

-

If you start taking CPP at age 60: You will receive 0.6% less per month or 36% less if you start taking your CPP at age 60 vs. age 65.

-

If you start taking CPP at age 70: You will receive 0.7% more per month or 42% more than if you start taking your CPP at age 70 vs. age 65.

Assuming a $1,000 CPP payout at age 60:

| Start CPP Age 60 | Start CPP Age 65 | Start CPP Age 70 | |

|---|---|---|---|

| CPP Received/month | $ 640 | $ 1,000 | $ 1,420 |

| CPP Received/Year | $ 7,680 | $ 12,000 | $ 17,040 |

Total cumulative CPP you will receive by each age, depending on when you start payments:

| Total CPP Received | Start CPP Age 60 | Start CPP Age 65 | Start CPP Age 70 |

|---|---|---|---|

| Age 60 | $ 7,680 | $ - | $ - |

| Age 61 | $ 15,360 | $ - | $ - |

| Age 62 | $ 23,040 | $ - | $ - |

| Age 63 | $ 30,720 | $ - | $ - |

| Age 64 | $ 38,400 | $ - | $ - |

| Age 65 | $ 46,080 | $ 12,000 | $ - |

| Age 66 | $ 53,760 | $ 24,000 | $ - |

| Age 67 | $ 61,440 | $ 36,000 | $ - |

| Age 68 | $ 69,120 | $ 48,000 | $ - |

| Age 69 | $ 76,800 | $ 60,000 | $ - |

| Age 70 | $ 84,480 | $ 72,000 | $ 17,040 |

| Age 71 | $ 92,160 | $ 84,000 | $ 34,080 |

| Age 72 | $ 99,840 | $ 96,000 | $ 51,120 |

| Age 73 | $ 107,520 | $ 108,000 | $ 68,160 |

| Age 74 | $ 115,200 | $ 120,000 | $ 85,200 |

| Age 75 | $ 122,880 | $ 132,000 | $ 102,240 |

| Age 76 | $ 130,560 | $ 144,000 | $ 119,280 |

| Age 77 | $ 138,240 | $ 156,000 | $ 136,320 |

| Age 78 | $ 145,920 | $ 168,000 | $ 153,360 |

| Age 79 | $ 153,600 | $ 180,000 | $ 170,400 |

| Age 80 | $ 161,280 | $ 192,000 | $ 187,440 |

| Age 81 | $ 168,960 | $ 204,000 | $ 204,480 |

| Age 82 | $ 176,640 | $ 216,000 | $ 221,520 |

| Age 83 | $ 184,320 | $ 228,000 | $ 238,560 |

| Age 84 | $ 192,000 | $ 240,000 | $ 255,600 |

Deeper analysis:

-

Immediate Benefit: Starting the CPP at age 60 gives an immediate inflow of cash, totalling $38,400 by age 64, even before one starts receiving CPP at age 65.

-

Break-Even Analysis:

-

For someone starting at age 60 compared to age 65: By age 70, the person who started at age 60 has received $84,480, while the person starting at age 65 has received $72,000. It means that for almost 10 years (from age 60 to age 69), the earlier start date has a monetary advantage.

-

For someone starting at age 65 compared to age 70: The break-even point comes around age 81. By age 81, both have received approximately $204,000. So, the advantage of starting at age 65 lasts for about 16 years.

-

-

Long-Term Perspective: However, after age 81, starting at age 70 becomes more lucrative. By age 84, if you started at age 70, you'd have received $255,600, whereas starting at age 65 would yield $240,000 and at age 60 would yield $192,000.

-

Age Consideration: One's life expectancy and health conditions play a crucial role in this decision. If someone has a family history or personal health considerations that indicate a shorter life expectancy, starting earlier could be more beneficial. On the other hand, if longevity runs in the family and the person is in good health, waiting till age 70 might yield the maximum benefit. Keep in mind that the average life expectancy of Canadians is around 80-82

-

Financial Needs & Retirement Goals: A person’s immediate financial needs can dictate the choice. Some may need the money at 60 due to personal commitments or to enjoy their early retirement years, while others might be in a position to delay it for a greater payout later on.

-

Opportunity Cost: The money received earlier could potentially be invested, which is not directly evident from the table. For example, the $38,400 received from age 60-64 could be invested and may provide returns that aren't reflected in the simple cumulative values provided.

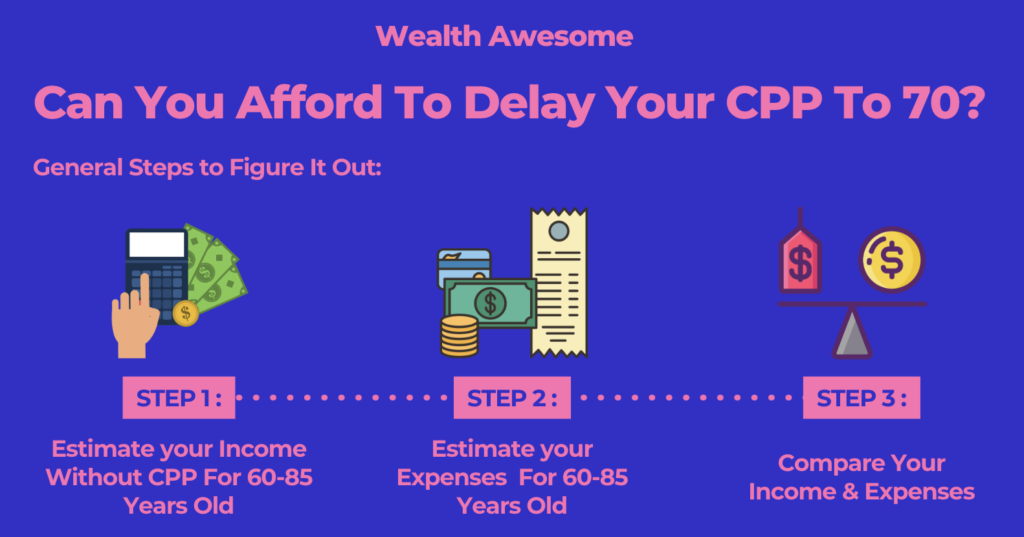

2. Can you afford to delay your CPP to 70?

This will take a little bit of work to figure out, but here are the general steps to take:

Step 1: Estimate your income without CPP for 60-85 years old

You will need to estimate your retirement income from all sources, except your CPP, for the ages of when you are 60-85. You will need to determine how much your total investments and savings will be from all sources and how much you will draw from them each year.

Step 2: Estimate your expenses for 60-85 years old

You will need to estimate what your expenses will be for every year, between 60-80. You can use the rule of thumb of 70%-100% of your last year’s income, which will differ depending on your situation.

Step 3: Compare your income and expenses

If you retire and your income is less than your expenses or close to it without any CPP payments, you might need to start taking CPP early.

If you have lots of cushion between your income and expenses though, you have more flexibility to delay your payments.

Related Reading: How much do you need to retire in Canada?

3. Forecast your life expectancy

Guessing how long you will live is not a pleasant task, but it’s necessary to figure out when is a good time to start your CPP.

The best way is to look at your family history and examine your current health. Go for a medical checkup and consult your doctor, who can give you a full breakdown of how good your health is right now.

If you want to go by statistics, depending on when you were born, the average Canadian is expected to live to around 80-82.

If you're in good health and think you will live well into your 80s and 90s, then delaying your CPP could be the right decision. However, if you're in poor health, taking your CPP earlier might be the wiser choice.

4. OAS clawback

If you are close to the OAS clawback amount at age 65, consider delaying your CPP payments to a later age. Currently, the OAS clawback threshold for 2023 is $86,912, so if you're close to this income consider this carefully when deciding when to start your CPP.

You could start getting clawed back on your OAS, which works out to a 15% tax if your income is too high. Delaying your CPP could help to reduce this OAS tax.

Read about strategies on how to reduce your OAS clawback here.

5. If you stopped working by age 60

If you are retired by the time you are 60, consider taking your CPP earlier. The years you aren’t working from 60-65 could decrease your retirement pension.

Each year of having zero contributions to your CPP might decrease your CPP payout. This is a tricky calculation that you will have to work out as you approach 60 to see what is more beneficial.

One advantage of taking your CPP at 60 is you can save or invest it to earn a return, which could work out to be a better option than receiving it at age 65 or 70. It depends on how your investment performs, though, so it does come down to a bit of luck.

Related Reading: CPP Payment Dates for [currentyear]

Post-Retirement Benefit

For individuals who continue to work and make CPP contributions after starting to receive their pension, the Post-Retirement Benefit (PRB) comes into play. The PRB allows you to contribute to the CPP and, in turn, receive an increased CPP retirement pension. This provision encourages continued participation in the workforce while rewarding individuals who contribute beyond their eligibility for a regular CPP pension.

Child-Rearing Provision

The Child-Rearing Provision recognizes the financial challenges faced by parents who took time away from the workforce to raise children. It allows for the exclusion of some years of low or zero earnings from the CPP pension calculation. This provision can lead to a higher CPP pension for individuals who took time off from work to care for their children.

FAQ Section

-

What are the benefits of taking CPP at age 60?

- Taking CPP at 60 provides early access to funds, which can be beneficial if you retire early or need immediate income. However, monthly payments are reduced.

-

How much more do I get if I delay CPP until age 70?

- Delaying CPP until age 70 increases your monthly payments by 42% compared to starting at age 65. This can significantly boost your lifetime pension if you live well into old age.

-

Is there a break-even point for taking CPP early versus late?

- The break-even point varies based on the age you start receiving CPP payments. Generally, if you live beyond age 81, starting CPP at 70 becomes more advantageous financially than starting at 65 or 60.

-

How does continuing to work affect my CPP?

- Continuing to work while receiving CPP can increase your benefits through post-retirement contributions, enhancing your pension amount regardless of when you start taking it.

-

Can I change my mind after starting CPP early?

- Once you begin receiving CPP, the decision is irreversible. Thus, it's important to make a well-informed choice based on your financial health and retirement goals.

Final Thoughts

Choosing when to start your CPP payments involves careful consideration of your financial needs, health status, and long-term financial planning. Whether you start at 60, 65, or 70, understanding the implications of your choice will help ensure that you maximize your benefits throughout retirement.

For more insights and to keep updated on CPP payment dates for 2025, visit our comprehensive section on CPP payment schedules.

Lots of people choose to start CPP payments at age 60 because nobody knows precisely when they will die.

However, if you’re an average Canadian in good health and don’t need the money immediately, taking your CPP at age 65 is a good compromise and a sweet spot for many. If you live past 74, you will earn more money in the long run.

It will take you until age 81 to earn more if you delay the CPP until age 70, which could be too long for most people. And maybe it's better to have more money earlier in your retirement to spoil your grandchildren!

Still not sure how CPP works? Check out my YouTube explainer video here:

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.