CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

Are you thinking of investing in the most robust stock market in the world, the U.S.?

If you don't want the hassle of picking your own stocks, then a common way to invest in America is to buy an S&P 500 ETF.

The famed investor Warren Buffett has stated that after his death, he has instructed his estate to invest 90% of his vast fortune into a simple S&P 500 index.

We will cover the best S&P 500 ETFs in Canada below to help you make your buying decision.

Just have a few minutes ? Here's the quick summary

| ETF Name | Symbol | MER | Description | Profile |

|---|---|---|---|---|

| Vanguard S&P 500 Index ETF (CAD-hedged) | VSP.TO | 0.09% | Vanguard S&P 500 Index ETF (CAD-hedged) offers protection against currency fluctuations with a low MER, tracking the S&P 500 closely. It's a long-term growth option with quarterly distributions, growing $1,000 to over $3,500 since Dec 2012. | |

| Evolve S&P 500 Enhanced Yield Fund | ESPX.TO | 0.45% | A covered-call ETF focusing on distributions with a monthly frequency. With a 33% covered call strategy, it aims for capital preservation and healthy income, offering an 8.42% annualized distribution yield. | |

| Invesco S&P 500 ESG Tilt Index ETF | ISTE.TO | 0.17% | Tracks S&P 500 companies meeting ESG criteria, covering about 449 companies. Despite underperforming compared to direct S&P 500 funds, it's a solid choice for ESG-focused investing. |

What is a Canadian S&P 500 ETF?

A Canadian S&P 500 ETF is an ETF that aims to track the performance of the S&P 500 index and is available for purchase on the Canadian stock exchanges. It's often considered a benchmark for the overall U.S. stock market and an indicator of the health of the U.S. economy. The Canada specific S&P500 ETFs sometimes include a few extra features such as hedging Canadian vs US currency.

Instead of picking individual stocks, when you buy shares of an S&P 500 ETF, you're basically buying a small piece of all 500 companies in the index.

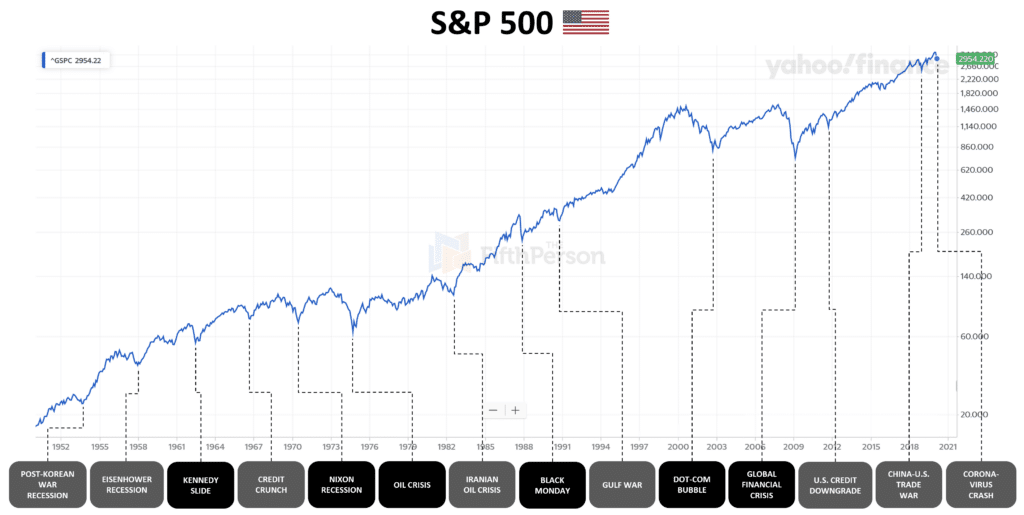

Here is the performance of the S&P 500, broken down by major market events. Between 1957 and 2021, this index earned investors an excellent average annualized return of 11.88%.

Pros and Cons of Investing in S&P 500 ETFs

Investing in S&P 500 ETFs is a popular choice among investors due to several advantages. However, like any investment, there are both pros and cons to consider. Let's take a look at them:

Pros

-

Very inexpensive MERs when compared to other funds and ETFs

-

Diversification through exposure to 500 companies

-

Excellent long-term index historical performance

-

Indirect international exposure, as many U.S. corporations have global businesses.

-

High liquidity for easy buying and selling

-

Potential dividend income.

-

Tax-efficient structure

-

Historically, many active funds underperform the S&P 500.

Cons

-

Only covers large-cap U.S. stocks.

-

No protection during market downturns.

-

Possible sector overconcentration risks (like tech)

-

Weighted by market cap, so larger firms dominate the performance

The Best S&P 500 ETFs in Canada

-

Vanguard S&P 500 Index ETF(CAD-hedged) (VSP.TO)

-

Evolve S&P 500 Enhanced Yield Fund (ESPX.TO)

-

Invesco S&P 500 ESG Tilt Index ETF (ISTE.TO)

1. Vanguard S&P 500 Index ETF(CAD-hedged)

![]()

-

Ticker: VSP.TO

-

Distribution Yield: 1.30%

-

Assets Under Management: 2.45B

-

Management Expense Ratio: 0.09%

-

Stock Price: $116.20

-

YTD Return: +6.66%

Vanguard S&P 500 Index ETF(CAD-hedged) is a pure-play S&P 500 fund similar to VFV, with just two differences. The first and most significant difference is that it's CAD-hedged. So, it shields you from price fluctuations and prevents you from getting a cherry on top of the usual returns when USD is strong against CAD.

The other difference has minimal impact on your returns. One is Assets Under Management (AUM) of $2.6 billion, which is low compared to VFV but still significantly higher than most other ETFs in Canada.

This fund carries a minimal MER of 0.09%. The fund tracks the performance of the underlying benchmark quite faithfully, with limited variation (under 1%). It also offers quarterly distributions, though the yield is quite low at 1.2% when writing this.

You may consider this ETF for its faithful tracking of the S&P 500, safety against currency fluctuations, and incredibly low investment cost. It's a healthy long-term growth instrument and a perfect buy-and-forget investment.

The fund has grown $1,000 of its investor's capital to over $3,500 since Dec 2012, and with a pace like this, you can build a sizable nest egg with a reasonable amount of capital.

2. Evolve S&P 500 Enhanced Yield Fund

-

Ticker: ESPX.TO

-

Distribution Yield: N/A

-

Assets Under Management: 69.31M

-

Management Expense Ratio: 0.45%

-

Stock Price: $25.49

-

YTD Return: -0.16%

Evolve S&P 500 Enhanced Yield Fund is quite young (started out in Jan 2023). It's a covered-call ETF with quite a reasonable fee of 0.45%. This particular S&P 500 ETF focuses on distributions.

It has a monthly distribution frequency, and at the time of writing this, the fund is offering an annualized distribution yield of about 8.42%.

But it’s different from a typical covered call ETF. The fund managers only write covered call options for about a third (33%) of the portfolio, which reduces the overall risk associated with the covered-call ETFs. However, its impact on the performance of the fund (compared to the underlying index) is quite significant.

In the last 12 months, when the S&P 500 grew over 24%, the fund only grew by about 8%. That's a reasonable trade-off, considering the sizable monthly distributions the fund offers.

If you are looking for an income-oriented S&P 500 fund with relatively limited risk, this new fund is worth looking into.

The total assets under management are just $76 million at the time of writing this, and the relatively small amount of time the fund has spent on the market means we don't have enough data to gauge its long-term prospects accurately.

But even with the limited information on hand, this appears to be a great pick for capital preservation and healthy income.

3. Invesco S&P 500 ESG Tilt Index ETF

-

Ticker: ISTE.TO

-

Distribution Yield: 1.15%

-

Assets Under Management: 0.17%

-

Management Expense Ratio: 2.04M

-

Stock Price: $27.60

Invesco S&P 500 ESG Tilt Index ETF is tiny, easily the smallest fund on this list in terms of the assets under management. It's relatively young, too. It started out in January 2022 and hasn't gotten the traction that it should have, considering its low MER of 0.17% and almost direct exposure to the S&P 500 companies.

The key here is “almost.” The fund tracks the performance of the S&P 500 companies that meet certain ESG criteria. Currently, the fund is tracking the performance of about 449 companies.

The weight of the stocks is determined by the combination of their actual weight in the S&P 500 group and their S&P DJI ESG Scores.

If we compare it directly with another S&P 500 fund like VFV, the performance between Nov 2022 and Nov 2023 fell short by a sizable margin.

However, if more big money and retail investors start leaning towards ESG investment and S&P 500 companies with a high ESG score start outperforming the rest of the sector and offer outsized returns, the pattern may tilt in this ETF's favour.

It’s a good pick, especially if you are focused on ESG investing. It undercuts the performance of the underlying index but at the cost of responsible investment.

Historical Performance of the S&P 500

The S&P 500 has undergone significant changes and seen a variety of market conditions from the 1980's to 2021. Here is a summarized overview divided into decades, highlighting major events and trends.

1980s - Tech Boom Begins:

-

Performance: The S&P 500 saw a surge, especially in the latter half, with an average annual return of about 17.5%.

-

Key Events: Reaganomics, Black Monday of 1987 (largest single-day market crash), and the rise of technology companies.

1990s - Continued Tech Surge:

-

Performance: The rise of the internet and tech companies fueled the market, seeing average annual returns of approximately 18.2%.

-

Key Events: Dot-com bubble towards the end of the decade, dissolution of the Soviet Union, and the launch of the euro.

2000s - Dot-Com Bust and Financial Crisis:

-

Performance: The early 2000s experienced a market downturn due to the dot-com bubble burst. The 2008 financial crisis further strained the markets. The S&P 500 had an average annual return of just 0.6% for the decade.

-

Key Events: 9/11 attacks, Iraq War, and the housing bubble burst leading to the global financial crisis.

2010s - Bull Market Resurgence:

-

Performance: One of the longest bull markets in history. Despite some volatility, the S&P 500 had an average annual return of about 13.6% for the decade.

-

Key Events: Recovery from the financial crisis, tech giants' dominance, U.S.-China trade wars, and the beginnings of Brexit.

Notable Years:

-

1987: Black Monday saw the S&P 500 drop by over 20% in a single day.

-

2008: The S&P 500 fell 37% over the year, one of its worst annual performances due to the financial crisis.

-

2013: The market soared, with the S&P 500 returning over 32% due to economic recovery and growth.

-

2020: A year of extremes; the S&P 500 dropped around 34% from February to March but ended the year up by over 16%.

Should you Invest in an S&P 500 ETF?

Whether or not you should invest in an S&P 500 ETF depends on several factors related to your individual circumstances. Let's discuss the considerations you should keep in mind:

Factors to Consider Before Investing:

-

Risk Tolerance: While the S&P 500 ETF provides diversification, it is still subject to market risk. If the overall market declines, the ETF will likely decline as well.

-

Investment Horizon: Historically, the stock market has been a good place for long-term investments. If you have a short-term horizon, you might want to consider your investment choices carefully due to the potential for volatility.

-

Financial Goals: Ensure that investing in an S&P 500 ETF aligns with your financial goals, whether they be for retirement, buying a home, or other objectives.

-

Other Investments: Review your existing investment portfolio. If you're already heavily invested in U.S. large-cap stocks, adding an S&P 500 ETF might not provide as much diversification.

-

Market Conditions: While it's challenging to time the market, and it's often not recommended, be aware of current market valuations and economic conditions when making investment decisions.

-

Tax Implications: Understand the tax implications of ETFs in Canada, including taxation of dividends and capital gains.

If you're unsure about things like your risk tolerance, investment horizon, and financial goals, a great place to start is by doing this free investor questionnaire from Vanguard.

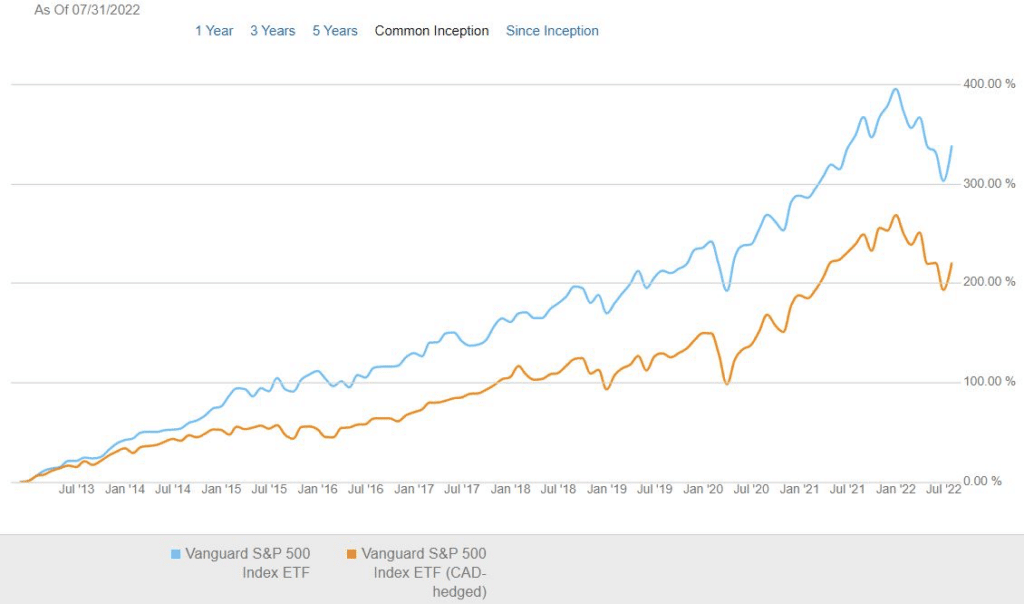

Should you Currency Hedge your S&P 500 Investment?

Investing in the S&P 500 index stocks through an ETF invests you in US companies. These companies have to be purchased in US dollars, exposing Canadian investors to an additional risk: currency fluctuations between the Canadian dollar and the US dollar.

Once you are invested in a US company, any appreciation in the US dollar against the Canadian dollar helps your investment returns down the road. This is because you are able to buy back more Canadian dollars once you sell your USD investment.

An unhedged investment means that currency fluctuations will impact your total return, while a hedged investment removes currencies from the equation. Hedging typically comes with additional costs but can reduce volatility.

The VSP and VFV ETFs offered by Vanguard both track the S&P 500 ETF, with the VSP being hedged to the Canadian dollar. The difference in performance between the two is due to currency fluctuations.

The currency unhedged version (VFV) has currently outperformed the VSP significantly since inception.

Using the S&P 500 as an Investment Benchmark

Investors today are frequently quoting the performance of the S&P 500 index as a proxy for excellent investment returns.

Comparing the performance of a fund or portfolio to that of the S&P 500 index is often not an apples-to-apples comparison. Remember that the S&P 500 index invests only in the largest US stocks, while a robust portfolio typically includes global stocks as well as other asset classes such as bonds.

The S&P 500 is a good benchmark to use if you are looking to assess the performance of an active portfolio manager versus the broad US market (for US active strategies).

For a lot of investor portfolios, investing only in an S&P 500 Index fund or ETF will not provide an appropriate level of diversification or risk management.

Impact of Foreign Withholding Tax

One factor often overlooked when investing in foreign stock ETFs is the impact of foreign withholding tax. This tax is levied on international investments and is particularly relevant for Canadian investors eyeing the S&P 500 index ETFs.

What is Foreign Withholding Tax?

Foreign withholding tax is a fee imposed by a foreign government on the income earned within its borders by foreign investors. In the context of S&P 500 ETFs, dividends generated by the underlying U.S. stocks can be subject to this tax before they reach Canadian investors.

The drag caused by the foreign withholding tax can reduce the after-tax return for Canadian investors.

How do S&P 500 ETFs Handle this Tax?

Different ETFs handle this tax in varied ways. Some ETFs, especially those domiciled in Canada that hold a U.S.-based ETF as their primary asset, might be subjected to this tax twice – once at the U.S. ETF level and again when distributions are made to Canadian unit holders.

However, ETFs that directly own the underlying stocks (rather than holding another ETF) can bypass double taxation.

Which S&P 500 ETFs are Most Affected?

While the impact of foreign withholding tax is a reality for almost all international investments, Canadian-domiciled ETFs that directly hold the underlying stocks, such as the Vanguard VFV S&P 500 ETF, can offer a more tax-efficient structure for investors in registered accounts. On the other hand, wrap or fund-of-fund structures can result in higher tax drags.

FAQs:

Are there any Canadian unhedged S&P 500 ETFs available?

Yes, there are Canadian unhedged S&P 500 ETFs available. An unhedged ETF allows Canadian investors to benefit not only from any potential growth in the S&P 500 but also from potential gains in the U.S. dollar against the Canadian dollar.

Examples include the iShares Core S&P 500 Index ETF (CAD-Hedged) (XSP) and the Vanguard S&P 500 Index ETF (VFV).

Can S&P 500 ETFs be purchased on the TSX?

Yes, S&P 500 ETFs can be purchased on the TSX (Toronto Stock Exchange). Many Canadian ETF providers offer versions of the S&P 500 ETF listed on the TSX, which makes it convenient for Canadian investors to gain exposure to the U.S. market without the need to open a U.S.-based brokerage account. All the ETFs mentioned above can be purchased on the TSX.

How do I buy an S&P 500 Index Fund in Canada?

An S&P 500 Index fund or ETF can be purchased in three main ways. These include:

-

In a self-directed, discount brokerage account, such as Wealthsimple or Questrade.

-

Through a robo-advisor such as Questwealth.

-

With the help of an investment or financial advisor.

Conclusion

If you are looking to add US stocks to your portfolio, purchasing an S&P 500 ETF is one of the easiest and most robust ways to go about it.

While most of the S&P 500 ETFs available to Canadian investors are virtually identical, small differences remain between them.

If you are looking to invest outside of just large US stocks, make sure to consider other fantastic ETF options available to Canadians.

Best next step

Keep exploring this topic

If you want to go deeper, these are the most useful follow-up pages and tools for this topic.

ETF hub

Browse ETF categories by goal

Jump into core, dividend, fixed-income, and sector ETF clusters from one place.

ETF tool

Use the Canadian ETF screener

Filter ETFs by yield, AUM, and performance when you are narrowing a shortlist.

Popular guide

Start with our top ETF roundup

Start with a broad ETF guide if you want a quick shortlist across the main fund categories.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.