CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

Worried about not having enough money to retire in Canada? You’re not alone.

Over half (54%) of older Canadians have decided to delay retirement, mainly due to grim inflation numbers, according to this Global News survey.

My parents have both recently retired, and I used my past experience as an advisor to help them plan their retirement and investments.

Advertisement

Canadians now believe they need a whopping $1.7 million to retire, according to BMO's annual retirement survey. But is this really a reality? The number seems a bit high.

Let's dive deep into this to finally answer the question of "how much do I need to retire in Canada?"

Average Spending of Canadian Retirees

According to the 2021 Survey of Household Spending, the average annual consumption for Canadian senior households (age 65+) was $61,855 (excluding taxes, insurance, pension payments, and gifts).

If you assume that you and your partner will retire at age 65 and live until age 82, this will work out to be $48,453 * 17 = $823,701 total spent during retirement per household.

Remember that these are average numbers and don't account for inflation, and yours could be much higher or lower depending on your circumstances. If you’re looking at that number and thinking that it’s way too high, continue reading to see how you can save and invest to reach your goal.

Simple Retirement Saving Rules

Rules are a way to simplify a complex concept and might not suit your exact situation. But they are a good place to start if you’re unsure how much to save.

1. 50/30/20 Rule

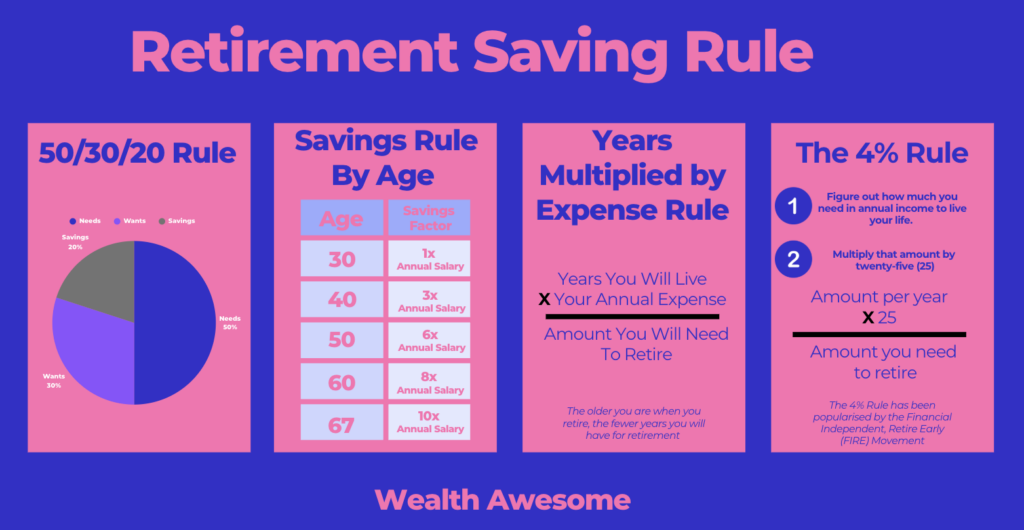

A popular rule of thumb is to use 50% of your money on needs like housing and food, 30% on wants such as travel or entertainment, and 20% on savings.

Is 20% for personal savings a reasonable amount? I wasn’t exactly sure, so I did some calculations. I assumed that you would invest all your money at a 4% investment rate of return, a savings period of 40 years (age 25 - 65), and zero taxes to keep things simple, and also to assume that people would take advantage of their TFSA and RRSP accounts. Here are the results:

50/30/20 rule:

| Average Salary (after-tax) | $ 50,000 | $ 75,000 | $ 100,000 |

|---|---|---|---|

| Savings/Year (20%) | $ 10,000 | $ 15,000 | $ 20,000 |

| Length (years) | 40 | 40 | 40 |

| Rate of Return (%) | 4% | 4% | 4% |

| Amount Saved | $950,255 | $1,425,383 | $1,900,510 |

As you can see, even with only a $50,000 average salary throughout your whole career, if you save 20% and invest all your money, you’ll almost have a million dollars by the time you retire.

Main takeaway: The 20% saving rule seems like it would be good enough for most people to save money for retirement.

2. Savings By Age Rules

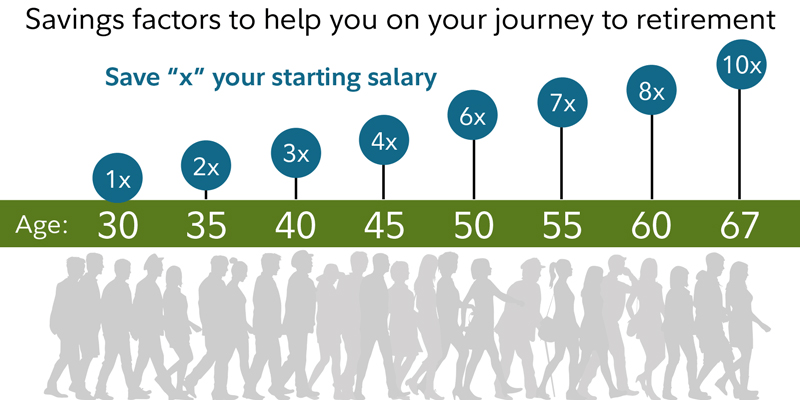

Fidelity came out with an interesting rule of thumb, which states that you should have a multiple of your salary saved by the time you hit a certain age:

-

Age 30: one time your annual salary

-

Age 40: three times your annual salary

-

Age 50: six times your annual salary

-

Age 60: eight times your annual salary

-

Age 67: ten times your annual salary

You can likely achieve this goal if you start saving around 15% of your income at age 25 and investing at least half of your money into stocks over your lifetime.

3. Years Multiplied by Expenses Rule

Determine how many years you will live and multiply it by your annual expenses to get the amount you need to retire. The older you are when you retire, the fewer years you will have for retirement:

Example: Jeff will retire late, at age 70. He calculates he will need $80,000 a year when he retires and wants to have enough money to last him until age 85, or 15 years. 15 years multiplied by $80,000 is $1.2 million, which is what he wants to have when he’s retired.

4. The 4% Rule

The 4% Rule is a widely used guideline in the financial independence and early retirement (FIRE) community. It helps individuals estimate how much money they need to save and how much they can safely withdraw from their investment portfolio during retirement without depleting their savings too quickly.

The rule is based on the Trinity Study, a research project that analyzed historical investment returns and withdrawal rates over different time periods.

Here's a detailed example of how the 4% Rule works:

-

Estimate your annual expenses during retirement: Suppose you want to retire and have determined that your annual expenses in retirement will be $40,000.

-

Determine the total amount needed for retirement: Using the 4% Rule, you would need to save 25 times your annual expenses to have a high probability of your money lasting for at least 30 years in retirement. In this case, 25 x $40,000 = $1,000,000.

-

Invest in a diversified portfolio: To follow the 4% Rule, you would typically invest in a diversified portfolio consisting of stocks and bonds, aiming for a mix that balances risk and potential returns. A common allocation is 60% stocks and 40% bonds, but the exact allocation will depend on your risk tolerance and investment horizon. It is popular to use ETFs to achieve this investment mix.

-

Begin withdrawals during retirement: Once you have reached your $1,000,000 savings goal and retire, you can start withdrawing 4% of your portfolio's value each year. In this example, you would withdraw $40,000 (4% of $1,000,000) in the first year of retirement.

-

Adjust withdrawals for inflation: To maintain your purchasing power throughout retirement, you would increase your annual withdrawals to account for inflation. For example, if inflation is 2% in the first year, you would withdraw $40,800 (1.02 x $40,000) in the second year.

It's important to note that the 4% Rule is a general guideline and may not be suitable for everyone. The rule assumes a 30-year retirement period, so if you plan to retire early and expect a longer retirement, you may need to adjust your withdrawal rate or savings goal accordingly.

Also, the rule does not account for changes in market conditions, so it's essential to remain flexible and adjust your withdrawal rate or investment strategy if necessary.

5 Steps to Figure Out How Much Money to Retire in Canada

For those who want to dive deeper into how much to save for retirement and don’t just want to rely on a simple retirement savings rule, follow these steps:

Step 1: How Much Money Will You Spend Per Year in Retirement?

Here are a few ways you can estimate how much money you’ll spend when you retire. If you are far away from retirement, I suggest using use methods 1 and 2 below. If you are close to retirement, I recommend using method 3.

1. 70% Pre-Retirement Income Rule

A rule of thumb is you’ll need about 70% of your pre-retirement income to spend every year in retirement. The rule states that if you made $100,000 before you retired, you would need about $70,000 annually after retirement.

2. Variable % Pre-Retirement Income Rule

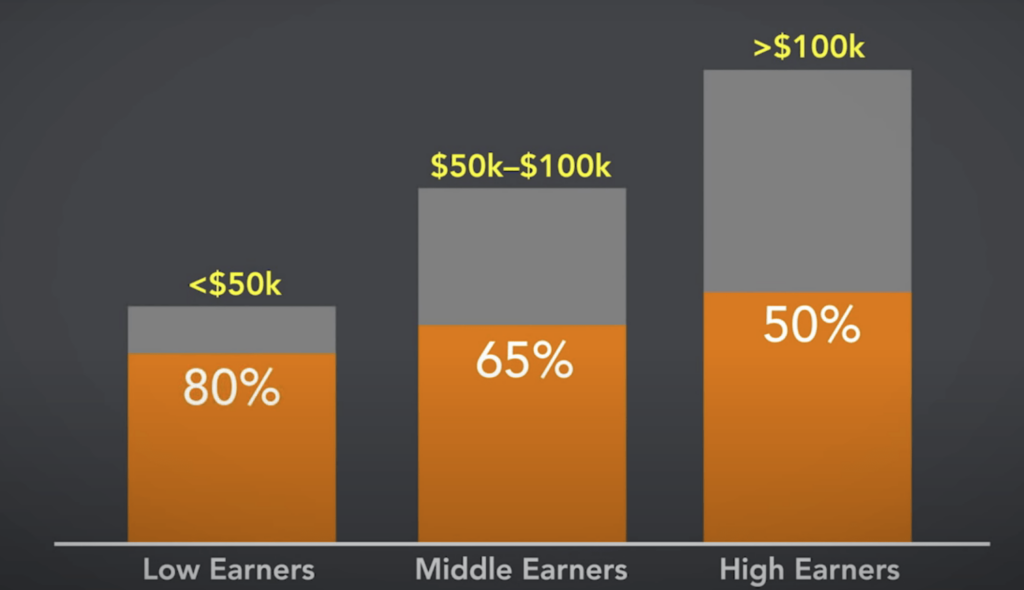

Some find the previous 70% rule too rigid and does not apply well to all income levels. This variable rule states that the more pre-retirement income you make, the less percentage you’ll likely need when you retire:

-

Lower-income earner (Less than $50K per year): Will spend 80% of pre-retirement income per year.

-

Middle-income earner ($50 - $100K per year): Will spend 65% of pre-retirement income per year.

-

Higher-income earner (Over $100K per year): Will spend 50% of pre-retirement income per year.

3. Detailed Budgeting

The closer you are to retirement, the more detailed you can get with your budget. By this time, you’ll have a clearer picture of your life after retirement. Some things to consider are:

-

What type of property do you want to live in

-

What kind of travelling do you want to do

-

Will there be high healthcare expenses

-

Is your mortgage paid off

-

Do you have grandchildren or children to care for

-

Will you live a significant portion of the year out of Canada

Step 2: Estimate How Many Years Will You Live

A tough part about figuring out how much money you need when you retire is that you’ll have to think about how long you’ll live. It’s not pleasant to think about death, but with retirement planning, it is unfortunately necessary.

The average life expectancy is around 82 years in Canada, so unless you have some major health complications, you should plan to have your money last until at least 85 to be safe. I recommend planning for 90, which gives you a lot of buffer room.

The older you are, the less money you’ll need to retire, as you’ll have fewer years to live. A person retiring at age 60 should plan to have 30 years of retirement income, versus a person retiring at age 70 who only needs to plan for 20.

Step 3: Estimate Much Government Income Will You Receive

In addition to your retirement nest egg in your Registered Retirement Savings Plan (RRSP), business income, and other sources, you may also be able to rely on government benefits to help fund your retirement lifestyle.

The two primary sources of government retirement income are the Canada Pension Plan (CPP) and Old Age Security (OAS).

The Canada Pension Plan

The Canada Pension Plan is the most common retirement benefit that Canadians can expect. Unlike OAS, it's not an income-tested benefit, which means that most Canadians are eligible to receive it, provided they contributed to CPP throughout their working years.

Almost all Canadians are required to contribute to the CPP, and contributions are usually automatically deducted from most workers' paycheques. Those who are self-employed will usually pay into the program when they file their annual income tax returns.

Although the maximum monthly payment is $1,306, the average new CPP retirement pension taken at age 65 was $723.89 per month as of 2023

In addition to the base CPP amount, disabled retirees may also qualify for the CPP disability supplement, which has an average monthly payout of $1,133.

While these are the most common CPP payments, some recipients may receive additional supplements and one-time payments, including:

-

Survivor's Pension

-

Death Benefit

CPP payment amounts are frequently updated to account for inflation and the ever-changing economic landscape. Calculating your CPP benefits can be tricky, as it depends on a number of different factors, including the age you retire.

To see how much you may be eligible for, try using the CRAs Retirement Income Calculator.

Old Age Security

Advertisement

Old Age Security (OAS) is another government retirement benefit that offers a modest monthly payment to eligible retirees.

Unlike the Canada Pension Plan (CPP), OAS is an income-tested program. This means that your benefit amount may be reduced or "clawed back" entirely based on your annual income.

- Read More: How To Avoid OAS Clawback

Generally, OAS is available to Canadians who are 65 years of age or older, though some residency conditions must be met.

To be eligible, you typically need to have lived in Canada for at least 10 years since the age of 18. If you've lived or worked abroad, certain international agreements could help you meet the eligibility criteria. Payments are usually issued automatically, without requiring a separate contribution like CPP.

Assuming you're eligible to receive a full OAS pension, here's what to expect in monthly benefit payments, depending on your age, as of July 2023:

-

65-74: $698.60 per month

-

75 or older: $768.46

Remember, the amount you receive can vary depending on your income and living situation.

If your income exceeds a certain threshold, the OAS clawback kicks in, and you may receive reduced benefits or none at all.

Guaranteed Income Supplement

In addition to OAS payments, low-income seniors may qualify for the Guaranteed Income Supplement (GIS), which offers extra financial support on top of OAS. The GIS amount is also income-tested and can vary depending on your individual situation.

Like CPP, OAS benefits are periodically adjusted to keep pace with inflation.

Step 4: Take Stock of Your Current Assets

To know the path to your goal, you must know how close to it you currently are.

While this will vary significantly by individual, some of the major assets to consider are:

-

Any equity in real estate investments

-

Your TFSA and RRSP account amounts

-

Workplace pensions that you might have

-

Investment accounts

-

Assets such as jewelry, precious metals, or art.

Step 5: Calculate How Much You Will Need to Retire

By this step, you should have figured out a few key numbers. You should know what age you want to retire, how many years you will be retired, how much you’ll spend in retirement, and how much money you currently have.

Method 1: Ballpark Estimation

Here’s a very simplified example, which doesn’t take into account any investment losses or gains, plus assumes a 0% rate of return in retirement so it’s likely an overestimation, but this will help give you an idea of how to estimate your retirement number:

Example: Greg is 40 years old. He wants to retire when he’s 60 and estimates that he lives until 90, so he will need 30 years of income. He has calculated he will spend about $50,000/year in retirement. With CPP and OAS payments and his pension from work, he estimates he’ll actually need only about $40,000/year, or roughly $1.2 million throughout the 30 years.

His current assets are worth $500,000, mainly in his primary residence, TFSA, RRSP, and workplace pension. He’ll need to increase his assets by $700,000 to reach his goal by age 60, and he has set up a retirement savings and investment plan that will help him reach that goal.

Method 2: Use a Retirement Income Calculator

After you have your ballpark estimate, compare it to what a retirement income calculator will give you. A retirement income calculator will likely show a more promising plan, as you'll assume a non-zero rate of return on your assets. My two favourite ones to use in Canada are:

-

Wealthsimple Retirement Income Calculator: Extremely easy to use and understand, plus I love how you can adjust the assumptions easily.

-

Sun Life Retirement Income Calculator: Similar to the first calculator, but with a different design that some people might find more appealing.

Saving vs Investing for Retirement

If you are only saving your money in a bank account, it’s going to be very difficult for you to hit your retirement goals. Most of the major banks in Canada have extremely low savings rates.

With online high-interest savings accounts (HISA) like EQ Bank, you can get a better interest rate of [sc name="eqbanksavingsrate"][/sc].

Compare this to if you are investing in the stock market. The U.S. S&P 500 index returned 12.1% on average for the 40 years that ended on December 31, 2019 (in CAD), and the TSX index returned 8.8% on average for the same period.

For a long-term estimate of the TSX and S&P 500 going forward, I would conservatively forecast a 5-7% return, which should still be well above a simple savings account.

What Is The Average Canadian Retirement Income?

According to the 2024 Canadian Income Survey, the average after-tax retirement income for senior families in 2022 was $74,200 annually, while individual seniors had an average of $33,600 per year.

However, it's been a few years since that report, so the number has likely increased due to inflation and other economic factors.

Averages can often be misleading, though.

A 2023 report by the Healthcare of Ontario Pension Plan (HOPP) revealed some disturbing statistics about participants' retirement and savings patterns:

-

44% of participants between 55 and 64 have less than $5,000 in total savings

-

44% of working participants were unable to set aside money for retirement in 2022

-

86% claimed they were concerned about their ability to save for retirement due to inflation and rising living costs

In troubling economic times, it's even more important to stay on top of your finances and create a budget plan that allows you to set aside money for retirement.

For more budget tips, be sure to read my tips for saving money on a tight budget.

When Does The Average Canadian Retire?

As of 2023, the average retirement age in Canada is 63.5 years. That being said, some Canadians may choose to retire earlier or later based on their savings, monthly income, and how much they enjoy their careers.

Life Changes That Can Affect Your Retirement Income

Retirement planning is all about making adjustments. Life is unpredictable, and chances are the retirement plan you make at age 30 will look nothing like your reality at age 60. Here are some factors that will make you need to revisit your retirement calculations

-

Significant changes in your income, such as landing (or losing!) a high-paying job or launching a successful business.

-

Large changes in your asset value. Real estate is a good example of this; anyone who owned a property in Toronto or Vancouver in the last decade has seen enormous gains in their assets. Albertans have not been as fortunate.

-

Investment gains and losses.

-

Health issues can cause a change in your life expectancy.

-

Changes in family life, such as getting married, having children, or getting divorced.

Mental Tricks to Help You Save More

If you’re struggling to save enough money for retirement, try these mindset tips to help you save more:

-

Track your spending: It’s undeniable that if you track your spending, you will become a better saver. I like to use an Excel spreadsheet at Squawkfox, or you can also use a mobile app like Mint. I review my spending every day and calculate my net worth every month to see if I’m on track to my financial goals.

-

Ask yourself this before buying - Will this purchase improve my life in the long term? This tip has helped me save a lot of money on impulse buys and shifted my spending towards things that actually matter to my happiness.

-

$100 rule: If I spend more than $100 on something, I’ll do a lot of research first.

-

Money saved today will multiply with time: A dollar saved today will be worth multiple times that amount if invested and held onto longer, which can give you freedom in the future.

Conclusion - How Much Do I Need To Retire Comfortably?

Retirement planning is tough. You’re trying to forecast something that will happen far into the future. There will be adjustments and mistakes made along the way.

$1.7 million is more than necessary for most Canadians to retire, so if you're looking at that number and getting anxious, don't worry. You likely won't need that much.

There are many Canadians who retire with no money at all, and they do alright because of Canada's excellent social support system.

Planning out how much you need to retire will increase your chances of hitting that goal. It’s also a relief to have a retirement plan, and it will eliminate some uncertainty in your mind.

Worried you don't have enough saved for retirement? Check out some of the common retirement income sources in Canada.

🧠 Frequently Asked Questions About Retiring in Canada

1. How much money do you need to retire in Canada?

It depends on your lifestyle and expected expenses, but a common benchmark is between $750,000 and $1.2 million. Some Canadians aim for $1.7 million as per BMO’s survey, while others retire comfortably with less by supplementing their income with CPP, OAS, and personal savings.

2. Is $500,000 enough to retire on in Canada?

It can be — especially if you’re receiving full CPP and OAS payments, have minimal expenses, and live in a lower-cost area. However, it may not be sufficient for those who plan to retire early or have high living costs.

3. What is the retirement age in Canada?

The average retirement age in Canada is currently 63.5. You can start receiving CPP at age 60 (with a reduced amount) and OAS at 65, with bonuses for deferring payments.

4. How long will $700,000 last in retirement in Canada?

That depends on your annual spending, investment returns, and inflation. With modest spending of around $40,000 per year and some government benefits, $700,000 could last 25+ years.

5. What are the main sources of retirement income in Canada?

The key retirement income sources in Canada are:

-

Canada Pension Plan (CPP)

-

Old Age Security (OAS)

-

Guaranteed Income Supplement (GIS) for low-income seniors

-

RRSPs and TFSAs

-

Workplace pensions

-

Investment income

6. Can I retire to Canada from the US?

While you can retire in Canada as a U.S. citizen, it requires proper immigration status. Most retirees apply for residency through family sponsorship or investment-based immigration. Canada does not offer a specific retirement visa.

7. When is the best month to retire in Canada?

Many choose to retire in December to maximize annual income and benefits. However, the best month to retire depends on factors like your pension start date, CPP/OAS eligibility, and employer policies.

8. How can I increase my retirement income in Canada?

-

Delay CPP and OAS to increase monthly payments

-

Invest in TFSAs or RRSPs

-

Downsize your home or use reverse mortgages

-

Start a side hustle or part-time work during early retirement

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.