CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

Are you a Canadian that’s looking to buy stocks but doesn’t know where or how to get started?

Only 41% of Canadians don’t invest in the stock market, while three out of four Canadians were confident in the stock market in 2022.

The three main ways to buy stocks in Canada are:

-

Buying stocks yourself through a self-directed (or discount) brokerage

-

Having stocks purchased through a robo-advisor

-

Working with an advisor who can purchase stocks for you

We’ll cover how to buy stocks in Canada below and discuss the three approaches in more depth.

How to Invest in Stocks in Canada

Approach 1: Buying Stocks through a Self-Directed Brokerage

Deciding to purchase stocks through a self-directed account puts you in charge of your investments. A self-directed brokerage does not provide you with investment advice – it simply allows you to trade within your accounts.

There are five steps to buying stocks through a self-directed brokerage. These are:

-

Deciding which stocks to invest in

-

Finding the best type of account to open

-

Open an account with a Canadian self-directed brokerage

-

Buy your stocks

-

Monitor your investments over time

Step 1 – Deciding Which Stocks to Invest in

Before you even begin researching which stocks to buy, you must make sure that stocks are an appropriate investment for you.

Stocks are considered medium-risk investments by most brokerages in Canada. Since they are riskier than bonds, they can drop significantly during periods of market volatility.

Within the stock universe, riskiness can vary. The stock of a new start-up company is likely to be much riskier than the stock of a well-established, blue-chip company.

Stocks to consider should be aligned with your personal goals and be good long-term investments. If you are looking for income, consider a stock with a high dividend yield. If you are looking for stability, consider a blue-chip value stock like a bank.

Make sure to avoid making emotional purchases when it comes to stock. Do a lot of research and always consider market trends and what industry experts are saying.

Step 2 – Finding the Best Type of Account to Open

The type of account that you will be buying stocks in is extremely important, especially for tax purposes.

Tax-preferred accounts such as a Tax-Free Savings Account (TFSA) and Registered Retirement Savings Plan (RRSP) can you from potentially paying a ton of money in taxes over time.

If you do not have any tax-preferred accounts open, or have some open but still have contribution room, consider investing through these accounts before investing through a non-registered account.

Examples of tax-preferred accounts include:

-

RRSP

-

TFSA

-

LIRA

-

RDSP

-

RESP

You may not be able to open or access all of the above tax-preferred accounts. Once all of your other options are exhausted, the default type of account is a non-registered account.

Step 3 – Open an Account with a Canadian Self-Directed Brokerage

Once you have decided on the type of account you will be opening, it’s time to consider which self-directed brokerage you would like to use.

If you are looking for inexpensive options, we recommend checking out Questrade or Wealthsimple.

Experienced investors may also want to consider Qtrade or Interactive Brokers.

Major financial institutions, like the big banks, offer their versions of self-directed brokerages.

If you are looking to purchase US stocks, you will need to make sure that the brokerage supports US dollar accounts. US stock purchases have to be made on the US side of your accounts.

Most discount brokerage accounts can be opened by going online or calling support and starting the process over the phone.

The opening of an account typically requires a lot of forms to be completed. Make sure to have a government-issued ID handy. The opening of your account will sometimes require a minimum level of funding.

Once your account is opened, it is time to finally buy your stocks.

Step 4 – Buy Your Stocks

Once your account is ready and funded, the next step is to purchase the stocks that you have researched. The most important type of orders to understand are market orders and limit orders when it comes to buying and selling stocks

Market Orders

The most well-known type of order for most people is the market order. This type of order immediately trades for you once you have inputted your information.

The main drawback of market orders is a stock’s bid-ask spread and uncertainty around what price you will actually buy your stock at.

The bid-ask spread is the difference in price between current sellers and buyers. Smaller and more illiquid stocks tend to have a large bid-ask spread – a big difference between the price at which a stock is being bought and sold.

Other than the difference in price, there is also a specific quantity that is available to be bought or sold.

When a market order is submitted, you trade immediately but don’t have control over the final price.

Limit Orders

Limit orders are quite a bit different from market orders. When a limit order is placed, you have control over what price to buy a stock at, but not over when the stock will actually be purchased.

Limit orders are usually placed and stay open until your shares are purchased or a specific period of time lapses.

You have the flexibility to place a limit order at any price. If a limit order is placed to buy a stock at a price that is above the current market price, you will be filled at the lowest possible price (the market price).

On the other hand, if a limit order is placed to buy at a price below the current market price, you will have to wait until the stock price reaches or drops below your inputted price.

Limit orders are strongly recommended when you are at the start of your investing journey. A limit order placed around the current market price will let you know exactly how much money you will be investing in each stock (once the order fills).

Limit orders can be partially filled, meaning that only a part of the order is successfully traded. If your order is not fully filled, only part of your money will be invested in the stock. This is the main drawback of limit orders.

Most discount brokerages have made the process of trading stocks fairly simple to understand on their online platforms. You can also buy and sell stocks by calling in to place an order, although there may be additional fees involved with this.

Step 5 – Monitor your Investments Over Time

The last step of the process is to watch over your stocks over time and determine whether they continue to be appropriate investments for you.

A major problem with most investors is that they check their investments too often, sometimes even on a daily basis. This can lead to a lot of stress if markets are volatile.

Portfolios can be reviewed at different intervals. The most common ones are:

-

Quarterly

-

Semi-Annually

-

Annually

Stocks can undergo quite a few different events that can have a big impact on their price. These include

-

Unexpected changes to a stock’s dividend

-

Changes to a share repurchase program

-

Stock splits or reverse stock splits

-

Bankruptcy

As a person ages, their risk tolerance tends to go down. This is because long-term goals draw closer and there is less time that money can stay invested before it has to be withdrawn.

Your goals and objectives can change throughout life as well. Take into consideration any changes to your lifestyle and make sure to adjust your portfolio accordingly.

Make sure to take a look at our full guide to buying stocks in Canada without a broker.

Approach 2: Buying Stocks through a Robo-advisor

A good alternative to buying and taking care of your own stocks is to use a Robo-advisor.

What is a Robo-Advisor?

A Robo-advisor is a platform designed to replace a human investment or financial advisor. This advisory service uses little or no human input and is based on mathematical formulas and algorithms.

The video below does an excellent job outlining the specifics of Robo-advising.

https://www.youtube.com/watch?v=q3j70Nq\_5LI

Robo-advisors typically begin with a few questionnaires and construct a portfolio for you. Robo-advisors at different companies may offer different services and options.

Robo-advisors have become more popular as investors look to reduce fees and technology continues to advance. The service is a low-cost alternative to using an investment advisor or portfolio manager.

In terms of quality Robo-advising platforms in Canada, we recommend those from Questrade and Wealthsimple.

Questrade offers Questwealth while Wealthsimple offers Wealthsimple Invest.

Buying stocks through a Robo-advisor is usually done indirectly through the purchase of low-cost ETFs or mutual funds. The amount of stock or equity exposure that your portfolio will have depends on the risk tolerance determined by your answers to the program’s questionnaires.

Pros and Cons of Robo-Advisors

Robo-advisors have their advantages and disadvantages when compared to working with an actual advisor or taking a self-directed approach.

Make sure to take a look at a full list of the best Robo-advisors in Canada.

Pros

- Lower fees relative to working with an investment or financial advisor

- Excellent guidance around building a well-diversified portfolio

- Potential access to financial planning

Cons

- Fees being charged (unlike the self-directed approach)

- Less control over your investment portfolio

- Lack of personalization to specific circumstances

Approach 3: Buying Stocks through an Investment Advisor

Working closely with an investment advisor to manage your accounts can also be an approach to buying stocks.

There are three main types of advisors in Canada: MGA, MFDA, and IIROC advisors. There are major differences between the three types – make sure to understand the differences.

Not all advisors invest in stocks for their clients. A large portion of advisors in Canada use funds, either mutual funds or ETFs, instead of directly purchasing stocks.

Discretionary vs Non-Discretionary Advisors

Advisors that invest in stocks can do so in two ways for clients.

Non-discretionary advisors must obtain verbal confirmation, typically over the phone, before buying or selling any stock or investment for their clients.

Discretionary advisors are able to manage their clients’ accounts freely. In most cases, they do not have to inform a client when a stock is being bought or sold.

Advisors typically charge significant fees for managing your money. These fees can seriously impact your returns over a long period of time.

Given how available information is, there are hardly any reasons to justify paying 1% or more in fees for an investment advisor.

How to Buy Stocks in Canada Online (With Trading Platforms)

If you have decided on the discount brokerage approach to buying stocks, you will have to choose from several brokerage options. We will outline some options to consider below.

Our top three choices when picking a discount brokerage are:

| Questrade | Wealthsimple | Qtrade | |

|---|---|---|---|

| ETF Trading Fees | Free to buy, $4.95 - $9.95 to sell | Free to buy and sell | Free to buy if on select ETF list, $8.75 for Investor, $6.95 for Investor Plus |

| Annual Fees | $0 | $0 | US registered accounts are charged a $15 fee quarterly |

| Stock Trading Fees | Minimum $4.95 – Maximum $9.95 to buy or sell ($0.01 per share traded) | Free to buy and sell | $8.75 for Investor, $6.95 for Investor Plus |

| USD Account | Free | $10/month | Free |

Questrade – Best for Flexibility

![]()

Questrade offers a very robust trading platform that can suit the needs of most Canadians when it comes to trading and investing.

Questrade has a platform for self-directed investing as well as a Robo-advisory service, Questwealth.

The self-directed platform comes with its advantages and disadvantages.

Pros

- Free ETF Purchases (only when you buy)

- $1,000 minimum needed to start investing

- USD accounts are available for purchasing US stocks and funds

- Low-cost trading for stocks, funds, and options

- The ability to start a dividend reinvestment plan (DRIP)

Cons

- ECN and foreign exchange fees on some trades

- Low mobile app ratings

- Periods of downtime have happened in the past during high investor volume

Discount brokerages charge investors two main types of fees – account fees and trading fees.

Questrade’s Account Fees

The platform’s account fees include:

-

Annual Fees: $0

-

Transfer Fees: $0, with a potential $150 reimbursement for transfer fees

-

Withdrawal Fees: $0

-

Foreign Exchange Fee: 1.75%

With small minimum requirements for accounts and zero annual fees, Questrade is an excellent choice for fee-sensitive investors.

Since Questrade offers US dollar accounts, you can buy and sell US stocks and funds. Be mindful that conversions between the US dollar and Canadian dollar (or other foreign currencies) can be costly in terms of exchange fees.

The foreign exchange fee can be reduced significantly in some cases by using Norbert’s gambit. Make sure to take a look at our guide explaining how to use Norbert’s gambit with Questrade.

Questrade’s Trading Fees

The platform’s trading fees include:

-

ETFs – Free to buy, $4.95 - $9.95 to sell

-

Stocks – Minimum $4.95 – Maximum $9.95 to buy or sell ($0.01 per share traded)

-

Options - $9.95 to buy or sell plus $1 per options contract

-

GICs and Bonds – No fee if at least $5,000 is purchased

-

International Equities – 1% of the value when buying or selling, with a minimum fee of $195 plus additional stamp or exchange fees

-

Initial Public Offering (IPO) – No fee if at least $5,000 is purchased

-

Precious Metals – US $19.95 per buy or sell

Take a look at our full review of Questrade as a platform to consider.

Wealthsimple – Lowest Fee Option

![]()

Wealthsimple is a brokerage that can save you a considerable amount of money in fees. It allows you to buy and sell stocks and ETFs without paying a commission for trading (no-fee trading).

Wealthsimple has a platform for self-directed investing as well as a Robo-advisory service, Wealthsimple Invest.

Wealthsimple Trade comes with its advantages and disadvantages.

Pros

- Free trades when selling or buying stocks and ETFs

- Fractional share purchases for some stocks

- USD accounts are available with a Plus subscription

- Ability to purchase cryptocurrencies

Cons

- Inability to trade bonds, international equities, mutual funds, or GICs

- High foreign exchange fees if trading US ETFs or stocks without a Plus subscription

- Lack of key registered accounts such as RESP, RRIF, and LIRA

Below is a breakdown of the fees charged by Wealthsimple Trade.

Wealthsimple Trade’s Account Fees

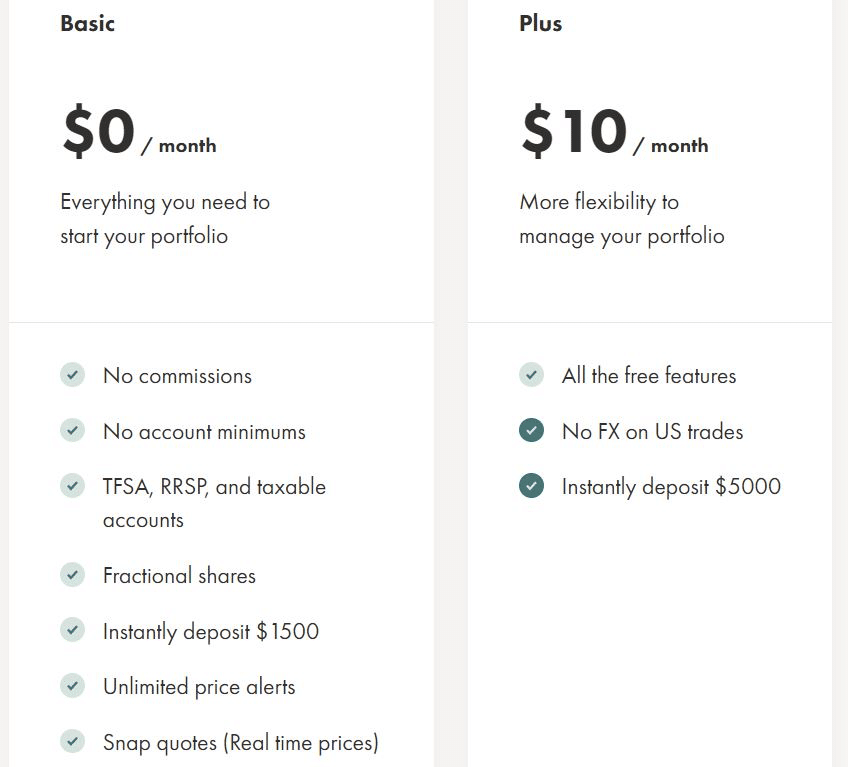

The basic version of Wealthsimple Trade comes with no account fees, while Wealthsimple Trade Plus comes with a fee of $10 per month.

Wealthsimple Trade does not require an account minimum for either its Basic or Pro offering (unlike Questrade).

If you are thinking of trading either US stocks or US ETFs, especially in large volumes, Wealthsimple Trade Plus is highly recommended. The subscription allows you to trade US instruments without paying a foreign exchange fee.

Currently, Wealthsimple Trade will not allow you to use Norbert’s gambit to avoid paying hefty exchange fees within a Basic account.

When opening a basic account, deposits of up to $1,500 will be added to your account instantly. When opening a Plus account, this amount increases to up to $5,000.

Fractional Shares with Wealthsimple Trade

The ability to purchase fractional shares is a huge advantage for investors with small portfolios. Some stocks, especially in the US, can rise to trade at very high prices per share.

Generally speaking, if you wouldn’t have enough money to purchase at least one share of a company’s stock, you wouldn’t be able to invest directly in it. Fractional shares allow you to bypass this problem.

Wealthsimple currently offers over 500 ETFs and stocks for fractional trading, including:

-

Shopify

-

Royal Bank of Canada

-

Toronto Dominion Bank

-

Canadian National Railway Co.

-

Amazon

-

Google

-

Apple

-

Microsoft

-

Facebook

-

Netflix

-

Tesla

-

AirBnB

-

Coinbase

-

Nvidia

Make sure to check out our full review of Wealthsimple Trade, which covers all of the platform’s aspects in even more detail.

Qtrade – Top User Experience and Customer Service

![]()

Qtrade’s mission is to deliver Canada’s best online brokerage experience. It places a high emphasis on great customer support and having an intuitive platform for investors to use.

Questrade offers an excellent platform for self-directed investing.

Like its peers, Qtrade comes with its advantages and disadvantages.

Pros

- Over 100 ETFs are available to buy and sell without commissions (no-fee trading)

- Excellent customer service

- Diverse account types available for clients

- Useful analytical and educational tools

Cons

- Only offers the US and Canada as markets

- Quarterly fees of $15 for U.S registered accounts

Qtrade’s Fees

Qtrade has two different client categories – Investor and Investor Plus.

A client who has more than $500,000 in assets with Qtrade or that makes over 150 trades per quarter automatically belongs to the Investor Plus tier. Investor Plus clients get substantial discounts in several areas.

Qtrade’s trading fees include:

-

ETFs – Free to buy if on select ETF list, $8.75 for Investor, $6.95 for Investor Plus

-

Stocks – $8.75 for Investor, $6.95 for Investor Plus

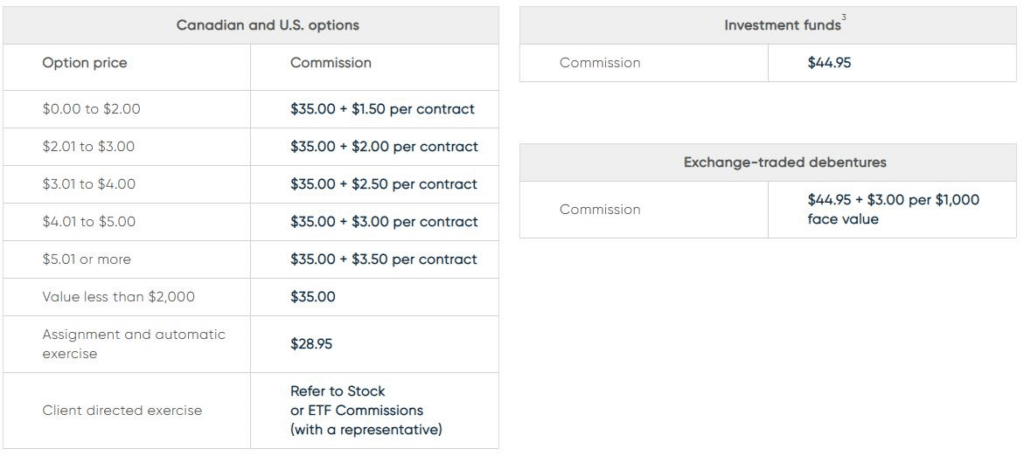

-

Options - $8.75 to buy or sell plus $1.25 per contract for Investor, $6.95 to buy or sell plus $1.25 per contract for Investor Plus

-

Mutual Funds– $8.75 for Investor, $6.95 for Investor Plus

-

Fixed-Income - $1 fee per $1,000 face value for Investor and Investor Plus

Qtrade also comes with several non-trade-related fees.

-

US registered accounts are charged a $15 fee quarterly (except for Investor Plus)

-

Transfer fees of $150 (when transferring out)

-

$100 fee for closing your account within the first 12 months

-

$25 quarterly fee unless one of the following conditions are met:

-

Having a balance greater than $25,000 in your account

-

Trading at least twice in the past quarter

-

Trading at least eight times in the last 12 months

-

M_onthly automatic deposits of at least $100_

-

The client is between the age of 18 and 30 years old with a monthly automatic deposit of at least $50

Norbert’s gambit can be done on the Qtrade platform to switch between currencies.

Qtrade Portfolio Tools

Qtrade offers clients a few tools to help with their self-directed investing. These include:

Portfolio Score: your portfolio is scored and compared to benchmarks

Investment Planning: you are able to project your net worth and create a plan for future goals

Portfolio review: you can see insights and portfolio statistics

Qtrade is a platform focused more on the client experience and functionality as opposed to being a cost leader like Wealthsimple Trade.

Make sure to read our full review of Qtrade before deciding if it is an appropriate platform for you.

Self-Directed Brokerages at the Big Canadian Banks

All of the major banks in Canada offer clients the choice of working with various advisors or using their self-directed brokerages.

Below is an overview of the self-directed brokerages at each of the major Canadian banks:

-

RBC – RBC Direct Investing

-

TD – TD Direct Investing

-

Scotia – Scotia iTrade

-

BMO – BMO InvestorLine

-

CIBC – CIBC Investor’s Edge

-

National Bank – National Bank Direct Brokerage

The self-directed brokerages at major banks are not forced to be as competitive when it comes to pricing. This is because of the well-established network that the banks already have with Canadians.

Clients that are unsuitable for working with an advisor are frequently referred to the bank’s discount brokerage. Given the constant influx of clients, most big bank discount brokerages charge high fees relative to Questrade, Wealthsimple Trade, and Qtrade.

One major exception is National Bank’s platform.

National Bank Direct Brokerage – An Option to Consider

National Bank was actually the first institution in Canada to offer commission-free trading for clients.

National Bank Direct Brokerage, while lagging behind in quite a few features when compared to our top three choices, is a good option to consider relative to the big banks.

National Bank’s platform comes with its advantages and disadvantages.

Pros

- Free trades when selling or buying stocks and ETFs

- A large variety of investments to choose from

- Supports a wide range of investment accounts

- Operated and owned by a major Canadian bank

- Strong physical presence in Quebec

Cons

- Annual inactivity fee

- Poor customer support

- High foreign exchange costs

- Lack of mobile application

As a bank-owned brokerage, National Bank Direct Brokerage supports a very wide range of account types. This level of account inclusion is typically only found with major bank brokerages.

Examples include:

-

Tax-Free Savings Account (TFSA)

-

Registered Retirement Savings Plan (RRSP)

-

Registered Retirement Income Fund (RRIF)

-

Registered Education Savings Plan (RESP)

-

Spousal RRSP

-

Spousal RRIF

-

Individual Pension Plan

-

Locked-In Retirement Account (LIRA)

-

Locked-In Retirement Savings Plan (LRSP)

-

Life Income Fund (LIF)

-

Non-registered accounts (cash, margin, and short selling)

-

Investment club accounts

-

Corporate investment accounts

Account Fees for National Bank Direct Brokerage

National Bank’s platform charges investors a handful of situational fees, which can quickly add up:

-

RRSP/RRIF/LIF Withdrawal Fee: $50

-

Excess Contribution Reimbursement Fee: $100

-

Yearly Account Administration Fees: $100 (if your account balance is under $20,000 or you don’t meet other criteria)

-

Transfer Out Fee: $150

-

Duplicate Statement or Confirmations: $10

Trading Fees for National Bank Direct Brokerage

The platform’s trading fees include:

-

ETFs (Canadian and US-Listed) – No fees when trading

-

Stocks (Canadian and US-Listed) – No fees when trading

-

Options - $0 to buy or sell plus $1.25 per options contract (minimum fee of $6.25) or maximum fee of $19.95 if the total trade value is less than $2,000

You can also place trades over the phone, but the fees for doing so are significantly higher:

National Bank Direct Brokerage supports US dollar accounts, meaning that you are free to trade US dollar-denominated investments.

You do not need to be a banking client with National Bank in order to open a National Bank Direct Brokerage account.

Make sure to read our full review of National Bank’s self-directed brokerage.

How to Classify a Stock

Stock is typically classified in several ways, which can help to evaluate how well-diversified your portfolio is and what overall attributes it has

Market Capitalization

Market capitalization is one of the ways that investors can categorize stocks. It refers to the current market value of a company’s total outstanding stock. Companies can be considered small, medium-sized, or large. In investment terms, these are:

-

Small-cap

-

Mid-cap

-

Large-cap

Value vs Growth

Stocks also typically fall on a value or growth spectrum based on how investors value company shares.

A value stock typically has fewer future growth prospects and may be operating in a mature industry. These stocks are considered relatively inexpensive, and investors commonly pay less for earnings relative to growth stocks.

Growth stocks tend to come with a higher price tag for their earnings relative to value stocks. Growth stocks usually have large future growth prospects, and company earnings are expected to grow constantly at high rates.

Sectors

Stocks can also be differentiated by the various sectors that businesses can operate in. Common examples of sectors include:

-

Materials

-

Consumer Staples

-

Consumer Discretionary

-

Technology

-

Healthcare

-

Financials

-

Utilities

There are many more ways to differentiate between stocks – these are commonly thought of when using a stock screener.

Frequently Asked Questions

Can I Buy Stocks Online for Free in Canada?

Currently, Wealthsimple Trade is the platform of choice for the commission-free trading of most stocks and ETFs. National Bank Direct Brokerage is also an alternative to consider if you would like to buy stocks for free.

What Kind of Stocks Should I Buy?

The type of stocks to purchase depends on your characteristics as an investor.

More risk-averse investors should consider less volatile stocks, such as blue-chip value stocks, which tend to fluctuate less during bumpy markets.

Growth-oriented investors will want to look at stocks with more explosive growth potential, such as tech stocks.

How Much Money do I need to buy Stocks?

When you are buying stocks, the minimum amount needed to invest is usually enough to be able to purchase one share of a company. In some cases, some brokerages offer the option to purchase fractional shares – less than one share.

How do Beginners Buy Stocks?

Beginners should follow our guide above when purchasing stocks. If you a new investor, getting stock exposure through a low-cost ETF is likely a better idea. An ETF can make sure that you are properly diversified.

How Can I Buy US Stocks in Canada?

Buying US stocks in Canada is fairly straightforward. Make sure to follow our in-depth guide.

How Do Stocks Work in Canada?

A stock represents ownership in a publicly-traded company. Large corporations can be worth hundreds of millions, if not billions of dollars – buying stock in the company means that you own an extremely tiny portion of the business.

As you buy more shares of a company, your ownership stake increases. In some cases, you can theoretically buy an entire publicly-traded company if you can afford to buy all of its shares.

Conclusion

If you’ve decided against using a broker and want to manage your own investments, there are two main ways to buy stocks in Canada.

Purchasing stocks through a discount brokerage will give you full control over your portfolio and trading.

Using a Robo-advisor will allow you to get stock exposure, typically at a fraction of a full-service broker’s advisory fee.

It’s critical that you perform great due diligence on any stocks before purchasing them in your accounts. If you have decided to select and manage your own investments, using a stock screener can help immensely with stock research.

Best next step

Keep exploring this topic

If you want to go deeper, these are the most useful follow-up pages and tools for this topic.

Stocks tool

Check Canadian stock movers

See the latest TSX and TSXV winners and losers before digging deeper into a sector.

Research hub

Browse Canadian stock research

Use the stock section to jump from a theme article into individual company pages.

Diversification

Compare stocks with ETF options

If you want exposure to a theme without single-stock risk, screen matching ETFs instead.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.