CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

Retirement planning is one of the most important parts of personal finance but also one of the most intimidating.

There are so many retirement factors to consider, and everyone has different goals.

As a former financial advisor, and also from having run this blog and getting feedback from thousands of Canadians over the past few years, I know that retirement planning is a big struggle for many people.

That’s why I’ve put together this ultimate guide on retirement planning in Canada, which pulls together my best content on retirement into one comprehensive article.

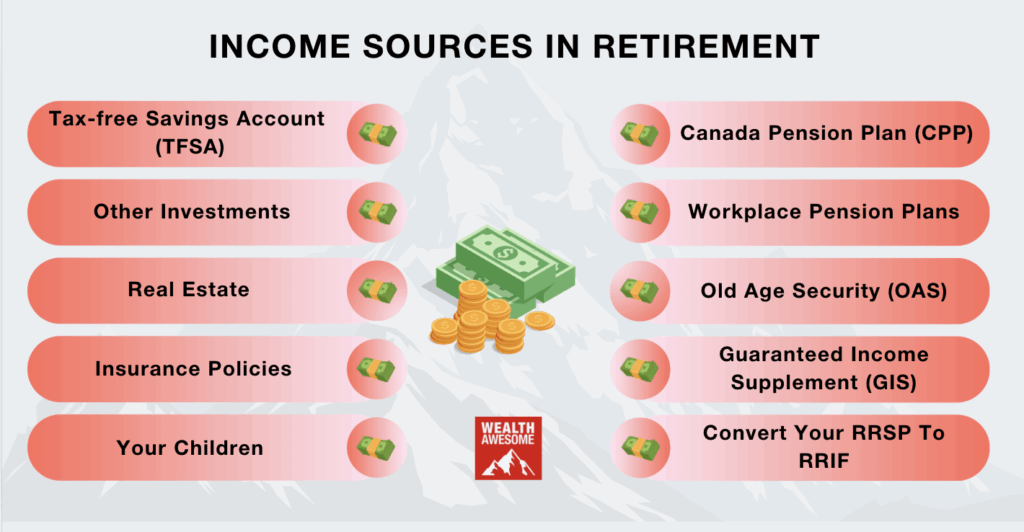

Income Sources in Retirement

Wondering exactly what type of income you'll have in retirement? Here are some of the fundamental income sources that many Canadians can rely on after they retire.

1. Canada Pension Plan (CPP)

The CPP tops this list because it’s the most common source of retirement income for all Canadians. Most working Canadians should qualify for this payment, regardless of income level.

How Much CPP Can You Get?

The average CPP payout for 2023 was around $717.15/month, but the CPP max amount was $1,306.57/month if started at age 65.

It’s a bit of a complicated calculation to figure out your exact payments, and it’s only an estimation until you actually retire.

Related Reading: Learn more about how much CPP you can get.

What Age Should You Start Your CPP?

Deciding what age to start your CPP is crucial. You’ll be able to start it at any year between the ages of 60 to 70.

-

If you start taking CPP at age 60: You will receive 0.6% less per month or 36% less if you start taking your CPP at age 60 vs. age 65.

-

If you start taking CPP at age 70: You will receive 0.7% more per month or 42% more than if you start taking your CPP at age 70 vs. age 65.

Related Reading: In-depth breakdown of what age to start your CPP.

2. Workplace Pension Plans

There are two main types of workplace pension plans you can receive:

Type 1: Defined Contribution Pension Plan (DCPP – More Common Today)

The way this plan in Canada works is that you make contributions to the DCPP while you work for your company.

If you are a part of this plan, you can allocate a portion of your salary (before taxes!) to the plan.

Your company does not manage the amount in your DCPP. As an employee, you have the power to choose where the contributions are invested, but you’re usually limited by the partners and investment options provided by your company.

With a DCPP, there is no guarantee of a fixed amount that you can receive when you retire. It all depends on how well your investments perform.

Related Reading: Learn more about defined contribution pension plans.

Type 2: Defined Benefit Pension Plan (DBPP – Less Common Today)

According to this plan, the company you work for will pay you a predefined monthly income for life after you retire as an employee of the company.

The DBPP amount you receive after you retire can be calculated in various ways. Typically, the formula used to calculate the payments you receive is based on the average highest salary you made while you were at the company and the number of years of service you provided the company.

Most companies today only issue the defined contribution type of pension plan. Companies don’t want the risk of having to pay a specific amount of employees anymore, so you’re seeing almost no new issuances of DBPPs in recent years in Canada.

Related Reading: Learn more about the defined benefit pension plan.

3. Old Age Security (OAS)

Your OAS payment can be different depending on how long you have lived in Canada. You must have lived in the country for at least 40 years after turning 18 to receive the full OAS pension payment.

If you have not resided in Canada for 40 years after turning 18, you can receive partial pension benefits.

OAS Example: John arrived in Canada at the age of 45. He has been living in the country for 20 years. It means John has spent 20 years as an adult living in Canada. According to the requirements, John is eligible to receive 20/40th of the full benefit – half of what he would receive if he had been living in Canada for 40 years.

The payment cycles for OAS start in July of each year. For Oct to Dec 2022, you can receive a maximum of $685.50 per month in your OAS pension.

Related Reading: Learn more about how much and when you can receive OAS here.

OAS Clawback

Be aware that the CRA will not give you your full amount of OAS even if you do qualify for it. You could be subject to an OAS clawback if you made over $79,845 as a retiree in 2021.

Related Reading: Learn more in this ultimate guide on the OAS clawback.

4. Guaranteed Income Supplement (GIS)

The GIS is an additional benefit available to seniors with a low retirement income in Canada who either already receive or qualify for an OAS Canada pension. To qualify for GIS, you must:

-

Have an annual income lower than the maximum annual threshold, and

-

Currently receive an OAS pension.

Check out if you qualify for the GIS here.

5. Convert Your RRSP to an RRIF

To get the most out of your registered retirement savings plan (RRSP) and maximize the tax benefits, you’ll need to convert it to an RRIF.

There are four main steps to converting your RRSP to an RRIF:

-

Choosing the investment institution: This is simply figuring out where you will hold your money.

-

Complete the RRIF application.

-

Choosing an RRIF beneficiary: Most commonly chosen are your spouse or children

-

Figure out withdrawal schedule: This is by far the hardest step, and it can get quite complicated in the calculations. You have to start withdrawing by age 71, but you can start before that also.

Refer to this RRIF rules article to learn more.

6. Tax-Free Savings Account (TFSA)

The TFSA is Canada's most popular investment and savings account. It edges out the RRSP, with over 57% of Canadians owning a TFSA.

The max limit as of 2023 is $88,000, and more Canadians are choosing the TFSA as their main retirement account instead of the RRSP.

It’s also the most versatile and flexible investment account. It has such a simple concept that it’s extremely easy to understand: (almost) everything that you invest inside this account will not be taxed on any of the income it earns.

You can plan to take out the TFSA in whatever way you choose as you retire, and there are no withdrawal limitations.

Read more with this TFSA Ultimate Guide.

7. Other Investments (Non-registered and More)

All the previous sources of retirement income on this list have either been government payouts, pensions, or registered accounts.

Here are some other common retirement income sources that don’t fall into these categories:

-

ETFs and Mutual Funds

-

Stocks

-

Bonds

-

Cash Equivalents: GIC, High-Interest-Savings-Account (HISA)

-

Robo-Advisors

-

Alternative Investments

Read more about the best investment options in Canada here.

8. Real Estate

Canadians love investing in real estate. There are several ways that you can get retirement income from real estate:

-

Primary Residence – Can take out a Home Equity Line of Credit (HELOC). You can also sell your home, and live in a smaller one when you retire. With the primary residence tax-free allowance, you get all the capital gains for free.

-

Rental Income – If you have a residential or commercial property, you can rent it out for extra income

-

Airbnb – You can rent out a room or two in your existing property.

To learn more, here are some of the best real estate investment options in Canada.

9. Insurance Policies

Here are some ways you can receive retirement income from insurance policies:

-

Term life insurance – if someone you know who has passed away has named you as a beneficiary.

-

Whole life or Universal Life Insurance – There is an investment component to these policies, and you can draw out an income as you get older. It’s also good for bypassing probate laws and setting up inheritances.

-

Critical Illness Insurance – You can get income from a policy such as this if you suffer from something like a stroke or heart attack. It’s usually given as a lump sum payment.

-

Disability Insurance – If you aren’t able to work due to a disability, you can qualify for these monthly payments if you have the proper insurance in place.

If you're looking for insurance, learn about the best life insurance companies in Canada here.

10. Your Children

If you’re fortunate enough to have raised successful and kind children, they can help provide income and care for you in your golden retirement years if you’re in need.

Your parents can also provide for you. Sometimes it’s through an allowance, but unfortunately, it is usually through an inheritance when they pass away.

How Much Money Do You Need to Retire?

This is perhaps the most important step of retirement planning, which is estimating how much you’ll need to retire.

A CIBC survey shows that 79% of Canadians aged 35 – 54 are worried about not having enough money to retire.

The older you are, the easier it gets to forecast this amount. I’ve included tactics here for both young and old Canadians to try and estimate their expenses in retirement.

Average Canadian Retirement Expenses

The 2019 Household Spending Survey by Statistics Canada revealed that the average annual expenditure for Canadian households with members aged 65 and above was $48,453 (excluding taxes, insurance, pension payments, and gifts).

Assuming you and your partner retire at 65 and live until 82, the total expenses during retirement for your household would be $48,453 multiplied by 17 years, which equals $823,701.

Keep in mind that these figures are only averages and do not factor in inflation. Your actual expenses could be significantly higher or lower based on your specific situation. If the estimated amount seems too high, continue reading to learn how to save and invest toward achieving your financial goals.

Retirement Saving Rules of Thumb

Rules are a way to simplify a complex concept and might not suit your exact situation. But they are a good place to start if you’re not sure how much to save.

Take a look at these rules, and try to follow one that suits your situation.

1. 50/30/20 Rule

A popular rule of thumb is to use 50% of your money on needs like housing and food, 30% on wants such as travel or entertainment, and 20% on savings.

Even with an average salary of only $50,000 throughout your lifetime, assuming that you saved 20% for 40 years at a rate of return of 4% and zero taxes, you’ll have $950,255 saved, so this rule seems legit. Read more about how I calculated this retirement savings amount.

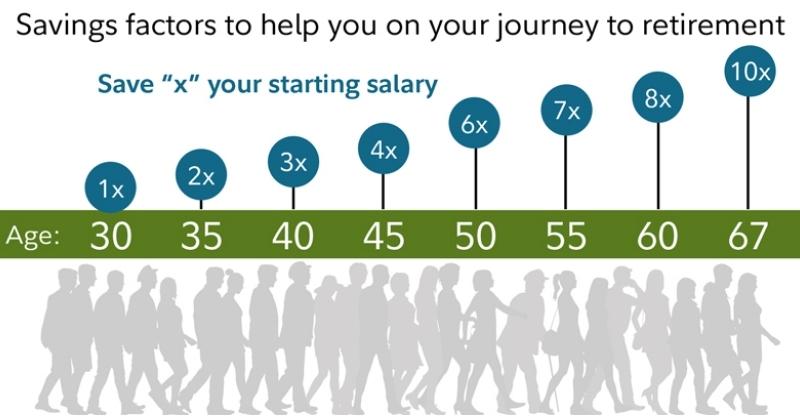

2.Savings By Age Rules

There’s an interesting rule of thumb, which states that you should have a multiple of your salary saved by the time you hit a certain age, which should provide you with a good retirement amount.

-

Age 30: one times your annual salary

-

Age 40: three times your annual salary

-

Age 50: six times your annual salary

-

Age 60: eight times your annual salary

-

Age 67: ten times your annual salary

You can likely achieve this goal if you start saving 15% of your income at age 25, and investing at least half of your money into stocks over your lifetime.

3. The 4% Rule

The 4% rule has been popularized by the Financial Independent, Retire Early (FIRE) movement, but it can be used by people at any age, not just young retirees.

First, figure out how much you need in annual income to live your life. Then, multiply that amount by 25, and that will be how much you need to retire, no matter how old you are. In theory, even if you’re only 30 years old, you can retire and have enough money to last you for the rest of your life.

Example: Jessie wants to retire at age 40. She needs $40,000 per year when she retires. Multiply that by 25, and you’ll get $1 million. $40,000 is 4% of $1 million. She can withdraw $40,000 every year without having to worry about having enough money.

4. 70% Pre-Retirement Income Rule

A rule of thumb is you’ll need about 70% of your pre-retirement income to spend every year in retirement. The rule states that if you made $100,000 before you retired, you would need about $70,000 per year after retirement.

5. Variable % Pre-Retirement Income Rule

Some find the previous 70% rule too rigid and does not apply well to all income levels. This variable rule states that the more pre-retirement income you make, the less percentage you’ll likely need when you retire:

-

Lower-income earner (Less than $50K per year): Will spend 80% of pre-retirement income per year.

-

Middle-income earner ($50 – $100K per year): Will spend 65% of pre-retirement income per year.

-

Higher-income earner (Over $100K per year): Will spend 50% of pre-retirement income per year.

You can read my full breakdown here on how much you need to retire in Canada.

How Many Years Will You Be Retired?

A tough part about figuring out how much money you need when you retire is that you’ll have to think about how long you’ll live. It’s not pleasant to think about death, but with retirement planning, it is necessary.

The average life expectancy is around 82 years in Canada, so unless you have some major health complications, you should plan to have your money last until at least 85 to be safe.

Two out of five Canadians who are 65 currently will live past the age of 90, which is a very long time to retire. I recommend planning for 95, which gives you a lot of buffer room.

The older you are, the less money you’ll need to retire, as you’ll have fewer years to live. A person retiring at age 65 should plan to have 30 years of retirement income for example to be safe.

Other Important Retirement Considerations

Life Changes That Can Affect Your Retirement Income

Retirement planning is all about making adjustments. Life is unpredictable, and chances are the retirement plan you make at age 30 will look nothing like your reality at age 60. Here are some factors that will make you need to revisit your retirement calculations:

-

Significant changes in your income, such as landing a higher-paying job or launching a new business.

-

Large changes in your asset value. Real estate is a good example of this; anyone who owned a property in Toronto or Vancouver in the last decade has seen enormous gains in their assets. Albertans have not been as fortunate.

-

Investment gains and losses.

-

Health issues can cause a change in your life expectancy.

-

Changes in family life, such as getting married, having children, or getting divorced.

Choosing a City to Retire

One choice that will have a huge impact on how much money you’ll need is choosing the city you’ll retire in. For many people, it will be where their grandchildren are. But if you have a choice, here are some things to consider:

-

Cost of living

-

Weather

-

Lifestyle

-

Population

-

Property Tax Rates

-

Housing Prices

-

Doctor per 100,000 Population

-

Crime Rate

Using these criteria, here’s a list of the best places to retire in Canada.

Moving Abroad to Retire

More Canadians are choosing to retire abroad either full-time or for part of the year. The benefits are obvious, such as much better weather and a much cheaper cost of living.

One big factor to consider is access to quick and good health care if you choose this route.

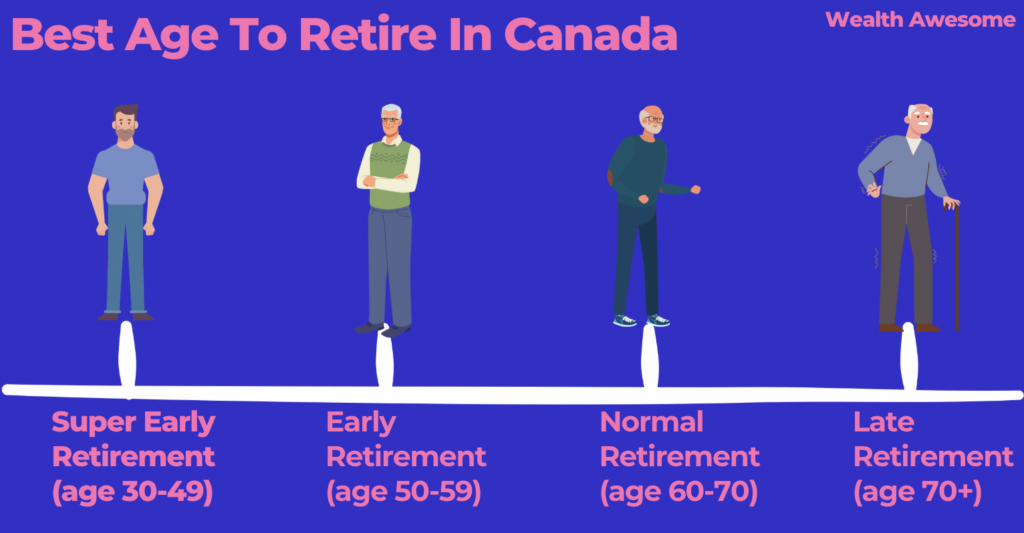

What Age Should You Retire?

According to this survey, 46% of Canadians expect to retire between 60 and 70.6% of Canadians expect that they will never retire. Here are some retirement options for you to consider:

1. Normal Retirement: Age 60 – 70

Most Canadians choose to retire in this age range, and it’s easy to see why. Government pensions will kick in during this time, such as your Canada Pension Plan (CPP) and Old Age Security (OAS) payments. This can be a significant income source for many Canadians, so many have no choice but to wait until this age.

There’s also societal pressure to retire at this age. If most of your friends and colleagues are retiring in this age range, you might get lonely or bored if you decide to retire earlier or later.

2. Late Retirement – Age 70 and Older

According to Stats Canada, the number of Canadians retiring 70 and older has more than doubled in the last ten years.

Here are some of the reasons more Canadians are choosing to retire later in life:

-

No more mandatory retirement age of 65: In 2009, the government decided to get rid of this restriction, giving Canadians a choice to continue to work longer.

-

People are living longer: With advancements in health care and the overall well-being of Canadians, we are living longer than ever. That means that more money will be needed in retirement, so more people choose to work longer.

-

Some people enjoy their work: Some people are passionate about their job, so decide to continue to work.

-

Money: Probably the most obvious one is that you will earn more money when you work more. You’ll also maximize your retirement income payouts such as your Canada Pension Plan (CPP) and OAS.

3. Early Retirement – Between Ages 50 – 64

Many Canadians dream about retiring early, as they start to get burned out from their work in their 40s and 50s. I’m sure that most people would choose to retire early if they had the means.

Having a good chance at early retirement requires a lot of discipline and investing wisely.

While it’s easy to see the benefits of early retirement, such as more free time, less stress, and the ability to travel, there are also downsides to early retirement.

If early retirement is your goal, think it through carefully, and make sure you have planned your finances out perfectly!

4. Super Early Retirement: Between Ages 30 – 49

There’s a new movement called financial independence, retire early (FIRE), where many people are choosing to adopt a very focused and ambitious goal of retiring very early in their life, usually by saving a lot of money and investing in the stock market or exchange-traded funds (ETFs).

It requires a lot of discipline in your early years of life, with many starting to save in their 20s or even as teens aggressively.

While there are many benefits of retiring early, there can be a lot of risks in planning for extremely early retirement. You’ll have to consider the huge sacrifices that will need to be made and the unpredictability of life.

A lot can happen in life that would throw your calculations off, and you may need to either start working again or abandon it altogether. You’ll also need to find other projects or things to find meaning and satisfaction from living.

Putting it All Together (Calculate How Much You Will Need to Retire)

How to put it all together now that you have this information

Step 1: Gather all Your Data from the Previous Sections

Now that you’ve gone through this article, you should have a pretty good idea of things like your sources of income in retirement and your approximate annual spending amount. Record all this information, I recommend using something like Google Sheets or Google Docs, as they are both free and convenient.

Step 2: Use a Retirement Calculator

Plug all these numbers into a retirement income calculator. My two favourite ones to use in Canada are:

-

Wealthsimple Retirement Income Calculator: Extremely easy to use and understand, plus I love how you can adjust the assumptions easily.

-

Sun Life Retirement Income Calculator: Similar to the first calculator, but with a different design that some people might find more appealing.

Note that these are estimates only, and they rely on assumptions that are almost impossible to forecast correctly, such as your expected rate of return.

But that’s what retirement planning is, your best-estimated guess, so you might as well use the best tools available to simplify the process!

Step 3: Consult a Retirement Professional When Needed

If you think your retirement circumstances might need some professional consultation, don’t hesitate to get some advice. For instance, you might need to talk to an accountant about your business retirement planning or a lawyer for your estate plan and make a will.

Also, consider a fee-only financial advisor that could help you put together a more in-depth plan without taking a hefty annual management fee. Try to find one with a Certified Financial Planning (CFP) designation, as this is the gold standard for financial planners.

Planning Your Retirement Lifestyle

Retirement is not just about financial planning; it's also about envisioning the lifestyle you want to lead during your golden years. Here are some key points to consider as you plan your retirement lifestyle:

-

Location: Determine whether you want to stay in your current residence, downsize to a smaller home, or even relocate to a different city or country. Your chosen location can greatly impact your cost of living, access to amenities, and overall quality of life.

-

Activities: Think about the activities you enjoy and how you want to spend your time. Whether it's travelling, pursuing hobbies, volunteering, or learning new skills, retirement offers the freedom to explore your passions.

-

Social Connections: Consider your social network and how you plan to maintain and expand it during retirement. Building and nurturing relationships can contribute significantly to your happiness and well-being.

-

Healthcare: Factor in healthcare facilities and services available in your chosen location. Access to quality healthcare becomes increasingly important as you age.

-

Financial Security: Align your retirement lifestyle with your financial resources. Ensure that your chosen activities and living arrangements are sustainable within your budget.

Saving vs. Investing for Retirement

If you are only saving your money in a bank account, it’s going to be very difficult for you to hit your retirement goals. Most of the major banks have very low interest rates, well below 0.2% per year, which won’t even keep pace with inflation.

With online high-interest savings accounts (HISA) like EQ Bank, you can get a better interest rate of [sc name="eqbanksavingsrate"][/sc] per year.

Compare this to if you are investing in the stock market. The U.S. S&P 500 index returned 12.1% on average for the 40 years that ended on December 31, 2019 (in CAD), and the TSX index returned 8.8% on average for the same period.

For a long-term estimate of the TSX and S&P 500 going forward, I would conservatively forecast a 5-7% return, which should still be well above a simple savings account.

Best Ways to Invest for Retirement

Investing in my opinion is a must if you are doing proper retirement planning in Canada. There are many ways you can start investing, but my two favourite ways are:

1. Discount Brokers

Investment Knowledge Needed: Medium to High

Time commitment: Low to High (depends on your investment)

Fees: Low to None

Also known as a trading platform, discount brokers are the cheapest way to invest in stocks and ETFs in Canada. Trading fees are minimal or even zero, depending on the broker you choose.

Discount brokers allow you to trade bonds, stocks, ETFs, and a few other types of investments online. They lower the barrier to entry into the world of stock market investing for the average Canadian investor.

Discount brokers facilitate stock market trading, but they do not offer direct investment advice. Discount brokerage accounts are usually available as online platforms that essentially provide investors with a self-service option.

Typically, investors who develop more of an understanding of the markets and do not need investment advice should choose discount brokers.

2. Robo-Advisors

Investment Knowledge Needed: Just a little

Time commitment: Very low

Fees: Low

Robo-advisors can often be the best option for first-time investors as they are building an understanding of investing and constructing portfolios based on financial goals. Robo-advisors provide you with financial advice and hands-off portfolio management based on your preferences.

Robo-advisors are investing platforms that design and manage your investment portfolio for you, usually automatically. It is a hands-off approach to investing in Canada.

Robo-advisors buy and balance a basket of ETFs for you based on your investment goals and risk tolerance. They determine everything by having you fill out an investment questionnaire.

Since robo-advisors operate solely online and trade low-cost ETFs, you can expect lower fees for their services than a traditional brick-and-mortar bank. If you need some basic advice, you can usually contact them via email, chat, or phone.

I consider Wealthsimple the best overall robo-advisor platform in Canada for its wide product selection and customer service, and Questwealth for its low fees and if you want an active management approach.

Early Retirement and Living Abroad

For some, retirement might come earlier than anticipated, opening up unique opportunities, such as living abroad. Early retirement offers a chance to experience different cultures, explore new environments, and create a fulfilling lifestyle beyond traditional borders.

I've been living abroad for the last few years and love the lifestyle. Here are some points to consider if you're contemplating early retirement abroad:

-

Cost of Living: Research and compare the cost of living in different countries to identify affordable yet desirable options. Some countries offer a lower cost of living without compromising on quality.

-

Healthcare Considerations: Evaluate the healthcare systems of potential retirement destinations. Access to quality medical care is essential, especially as you grow older.

-

Legal and Financial Aspects: Understand the legal requirements and financial implications of retiring abroad. This may include visas, residency permits, taxation, and managing international accounts.

-

Cultural Adaptation: Prepare for cultural differences and the process of adapting to a new way of life. Embrace the opportunity to learn and immerse yourself in a different culture.

-

Language: Consider the language spoken in your chosen country. Learning the local language can enhance your experience and ease day-to-day interactions.

-

Social Network: Plan how you'll establish a social network in your new location. Engaging with local communities and expatriate groups can help you connect and make friends.

Retirement plan seminars in Canada

Canada hosts numerous retirement planning seminars and workshops. Financial institutions, advisory firms, and community organizations offer sessions on retirement strategies, investment planning, taxes, and estate planning.

These seminars allow attendees to learn from experts and address their specific concerns. To find seminars, search online, check local institutions, or consult financial advisors.

Conclusion

Retirement planning in Canada is a huge task, but one that you can break down into a series of simple steps. I hope this article has helped you plan out your dream retirement.

If you need more help, look at the how much do you need to retire article or learn more about the retirement income sources in Canada.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.