CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

Knowing when to expect OAS payments can be crucial in your financial planning during retirement.

Available for Canadians 65 years old or older, you can receive the benefit if you meet certain qualifications.

Let's go over the OAS payment dates so you know when you'll receive your money in [currentyear].

OAS Payment Dates For [currentyear]

The upcoming [currentyear] OAS payment dates are as follows:

-

January 29, 2025

-

February 26, 2025

-

March 26, 2025

-

April 28, 2025

-

May 28, 2025

-

June 25, 2025

-

July 29, 2025

-

August 27, 2025

-

September 24, 2025

-

October 29, 2025

-

November 26, 2025

-

December 19, 2025

The OAS pension payments are issued on the same as the CPP payment dates, and should be issued via direct deposit. Service Canada distributes the payments for both OAS and CPP on the same dates, and you can view your upcoming and previous payments through your Service Canada Account.

You can also check out my article on CPP Payment Dates.

What Is OAS?

The Old Age Security pension is one of Canada’s retirement income sources for its aging citizens.

The OAS is among the three main retirement income plans in Canada.

The other two are the Canada Pension Plan (CPP) and the Employment Pensions Plan or Individual Retirement Savings. Unlike the CPP and Employment Pensions Plan, your OAS does not depend on your employment history in any way.

You need to be a resident of Canada or a Canadian citizen aged above 65 to receive the monthly taxable income.

For the CPP, you must retire to begin receiving your pension. You can receive OAS pensions if you are still working or have not worked a day in your life.

If you earn too much income, you can get some or all of your OAS clawed back. Learn how to avoid the OAS clawback here.

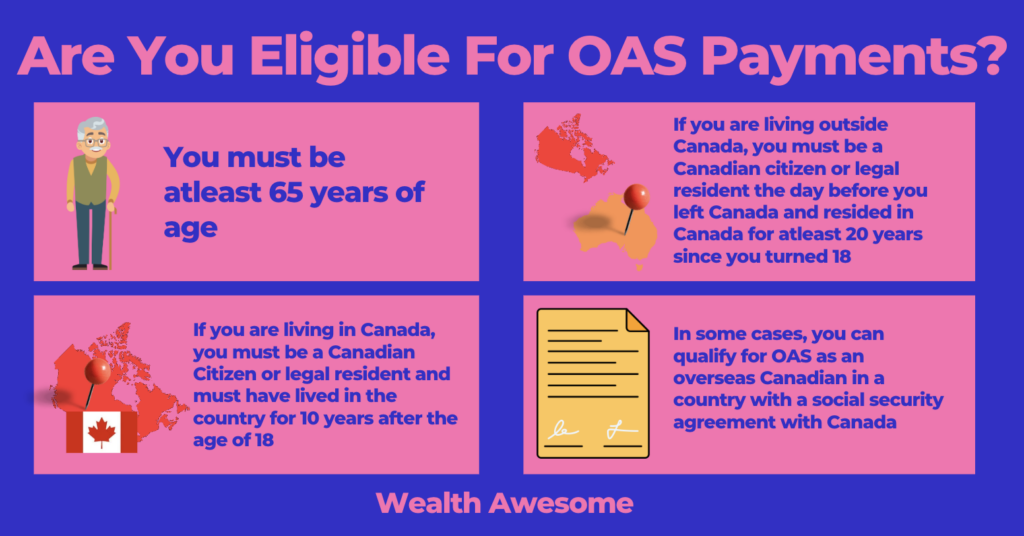

Are You Eligible For OAS Payments?

You need to qualify for the OAS pension benefits before you can begin collecting a monthly pension payment. Here are some of the eligibility requirements for OAS:

-

You must be at least 65 years of age.

-

If you’re living in Canada, you must be a Canadian citizen or legal resident and have lived in the country for at least ten years since turning 18.

-

If you’re living outside Canada, you must have been a Canadian citizen or legal resident the day before you left Canada and resided in Canada for at least 20 years since you turned 18.

-

In some cases, you can qualify for OAS as an overseas Canadian in a country with a social security agreement with Canada.

This is just a basic overview of the requirements to begin receiving pension payments. You can view the more comprehensive details about eligibility for OAS here.

How Much OAS Can You Receive In [currentyear]?

The monthly OAS pension payment cycles start in July of each year.

Maximum Monthly OAS Payments (April–June 2025):

-

Ages 65–74: $727.67 (if 2023 net world income is below $142,609)

-

Ages 75+: $800.44 (if 2023 net world income is below $148,179)

However, you must have lived at least 40 years in Canada as an adult to qualify for the full amount.

To help you understand how OAS works, here’s an example:

Jonathan moved from the US to Canada at 35. He has been living in the country for 30 years by the time he reaches 65. It means he has lived 30 years as an adult in Canada.

According to the requirements, Jonathan is eligible to receive 30/40th of the full benefit through the OAS. That is 3/4th of what he would receive if he had been living in Canada for 40 years.

For the quarter of Jul-Sept 2022, Jonathan can receive 3/4th of $666.83 per month (This was the max for that period).

Before you know about the Old Age Security payment dates, you should know how much you stand to make monthly. The OAS can vary from person to person, depending on how long you have lived in Canada as an adult.

Service Canada updates the maximum monthly amount you can receive based on the Consumer Price Index every quarter in January, April, July, and October.

If you have not lived in Canada for 40 years after turning 18, you can still receive partial pension benefits through OAS Canada. Service Canada determines partial pension benefits through 1/40th of the full pension amount for every full year you have lived in Canada since you turned 18.

Are OAS Benefits Taxable?

With the exception of periodic one-time payments, all monthly OAS benefits that you receive during the year count towards your annual income.

This means that they will be added to your existing income (if you have any), and you will be taxed on the full amount you earn during the year.

For example, if you earn $45,000 per year and receive $7,200 in annual OAS payments, you’ll pay taxes on $52,200 worth of income.

History of OAS Increases

OAS benefits increase periodically to adjust for inflation. This ensures that the payments are fair and helps offset financial difficulties caused by inflation.

Here’s a list of the most recent OAS increases in 2022:

-

Starting in January 2022, OAS payments increased by 1.1%.

-

Starting April 1st 2022, for the second quarter of the year, payments increased another 1%.

-

Most recently, beginning July 1st 2022, monthly payments increased by another 1.2%.

So far, OAS benefits have increased by a total of 3.3% in 2022. They are expected to increase incrementally during the final quarter of 2022 (October - December) as well.

Here’s another bit of welcome news for OAS recipients over the age of 75:

Starting July 2022, OAS payments to seniors over 75 will be permanently increased by an additional 10%. This increase will be automatically applied to your existing pension plan, so you don’t have to worry about making any phone calls or filling out additional paperwork.

OAS Benefits vs. CPP: What’s The Difference?

OAS Benefits are sometimes confused with CPP payments, as both programs provide scheduled monthly payments to seniors. Other than this one similarity, the two programs are completely different, though.

Here’s a quick table outlining the difference between OAS benefits and CPP payments:

| OAS Benefits | CPP Payments |

|---|---|

| Old Age Security | Canada Pension Plan |

| Available to seniors over the age of 65 | Available to seniors over the age of 60 |

| Supplemental retirement pension for eligible Canadians | Contributory retirement plan |

| Not dependent upon work history | Based on the amount contributed to CPP during your work history |

| Impacted by your current income | Negligibly impacted by your current income |

While both OAS and CPP are pension plans, they each have a different purpose. The goal of OAS is to ensure that aging Canadians don’t have to live below the poverty line or wonder how they’re going to pay their bills.

OAS is designed to provide financial security to long-term Canadian residents, regardless of how low their income is. It’s not dependent upon your work history and isn't something that you contribute to during your working years.

Canadians with no employment history can receive OAS, while CPP is almost entirely dependent upon your work history.

CPP, on the other hand, is a pension plan that you pay into with every employment cheque you receive. The amount you pay into CPP depends on the amount of the cheque. Once you retire, you’ll start receiving this money back as a form of supplemental income to help you live comfortably through retirement.

Eligible Canadians may be able to receive both OAS and CPP payments.

If you plan on retiring soon, be sure to read my guide to retirement income sources for Canadians.

One-Time OAS Payments For Seniors In 2022

In addition to their regular scheduled OAS benefits, eligible seniors may have received a one-time supplemental payment of $300 by the end of April 2022 to help offset the costs of the COVID-19 pandemic.

Those who are receiving GIS (Guaranteed Income Supplement) in addition to their regular OAS benefits should have received an extra $200, for a total of $500.

This one-time payment is tax-free and does not count toward your 2022 income. As such, you don’t need to worry about reporting it on your tax returns.

How Are OAS Benefits Calculated?

OAS benefits are primarily intended for long-term Canadian residents who’ve lived in-country for 40 years after their 18th birthday. However, those who’ve lived in the country for a shorter amount of time can still receive a fractional amount of OAS benefits proportional to their time spent in the country.

The main stipulation to receive OAS benefits is that you must have lived in Canada for at least 10 years after turning 18.

Here’s a quick look at how this could affect your OAS benefits:

-

Lived in the country for 40 years = 100% of eligible OAS benefits

-

Lived in the country for 30 years = 75% of eligible OAS benefits

-

Lived in the country for 20 years = 50% of eligible OAS benefits

-

Lived in the country for 10 years = 25% of eligible OAS benefits

In addition to the amount of time you’ve lived in Canada, your OAS payments are also determined by your current income. If your income surpasses the clawback threshold, then your OAS benefits will be adjusted accordingly.

How OAS Clawback Affects Your Benefits

OAS is primarily designed to help lower-income earners live comfortably through their retirement. If you’re over 65 and still earning good money, then the government will reduce your OAS benefits accordingly.

This is known as the OAS pension recovery tax and is commonly referred to as OAS clawback since the government is taking back money that it deems you aren’t in immediate need of.

If you earn more than the minimum threshold, you’ll be required to pay a 15% recovery tax on the amount over the threshold that you make.

For 2025, the OAS clawback threshold has increased to $93,454, up from $90,997 in 2024. If your net world income exceeds this amount, your OAS benefits will be reduced at a rate of 15 cents for every dollar above the threshold.

Example:

Let’s just say that you earn $85,000 per year, which is $3,239 over the threshold. This extra amount would be taxed by 15%, and the resulting amount would be deducted from your total eligible OAS benefits.

This means that $485.85 (0.15 x 3,239) would be taken out from your annual OAS benefits. When divided across twelve monthly payments, your monthly OAS payments would be reduced by $40.49.

Use the following equation to figure out the amount that will be deducted from your monthly OAS payments:

(Annual income over threshold x 0.15) / 12 = OAS Clawback

When Will OAS Clawbacks Stop?

Once your annual income falls below the minimum recovery threshold, you will no longer have to pay the 15% recovery tax and are eligible to receive the full amount of your OAS benefits (accounting for time spent in the country, of course).

You don’t have to wait till the next year to request a stop to your recovery tax either. If, at any point in the year, you believe that your annual income will amount to less than the recovery threshold, you can fill out CRA form T1213OAS.

Simply submit this form to your closest CRA office, and your case will be reviewed.

Avoid Or Reduce OAS Clawback With A TFSA

If you're looking for a "hack" that could reduce or eliminate OAS clawback and allow you to take full advantage of the OAS pension plan, this section is for you.

Currently, only 57% of Canadians have TFSAs and 90% aren't maximizing their available contribution room. If you're contributing more to your RRSP than you are to your TFSA, then this could cost you in the form of future OAS clawbacks.

Here's why.

TFSAs are a powerful investment vehicle, as investment profits realized within a TFSA aren't subject to capital gains tax and won't affect your personal income taxes.

However, TFSAs have specific advantages when it comes to retirement planning, particularly in avoiding the Old Age Security (OAS) clawback.

Unlike contributions to Registered Retirement Savings Plans (RRSPs), money put into a TFSA has already been taxed. This means that any future withdrawals from a TFSA are not considered taxable income. You can also withdraw money from your TFSA at any time without penalty.

The OAS clawback is triggered when a retiree's taxable income surpasses a certain threshold. Since RRSP withdrawals count as taxable income, pulling large sums from an RRSP during retirement could push your income over the limit and result in a reduction of your OAS benefits.

Since TFSA withdrawals do not affect your taxable income, they won't directly result in OAS clawback.

For example, with the current OAS clawback threshold of $81,761, you would be allowed to withdraw up to $6,813 per month from an RRSP before having to worry about OAS clawback.

What if you need more to cover your living expenses, though?

Instead of withdrawing more from your RRSP to cover living expenses, you could withdraw the additional amount from your TFSA with no OAS clawback penalties.

For those already on the verge of retirement, this may not be as viable of an option. However, for the younger readers out there who are just starting to save for retirement, this trick could really help you maximize your future retirement benefits.

Are OAS Payments Affected By The Province I Live In?

No. Since the OAS pension plan is a federal program, the amount you are eligible for will not be affected by the province you live in. OAS payments are only determined by the number of years you’ve lived in Canada past age 18 and your current annual income.

OAS Supplemental Benefits You Can Apply For

If you’re over the age of 65 and you’re already receiving OAS benefits, you may also be eligible for the GIS supplement. These benefits are designed to offset potential causes of financial hardship and can put some extra money in your pocket.

Guaranteed Income Supplement (GIS)

The Guaranteed Income Supplement, which is commonly referred to as the GIS is designed to help lower-income Canadians.

The GIS amount you’re eligible for depends on several factors, including your annual income and whether or not you have a spouse or common-law partner.

Here are the current thresholds and GIS payments offered by the government:

| Living Situation | Maximum GIS Supplement | Income Threshold |

|---|---|---|

| Single and living alone | $995.99 | $20,208 |

| Your partner receives full OAS compensation | $599.53 | $26,688 |

| Your partner receives the Allowance payment | $599.53 | $37,392 |

| Your partner does NOT receive OAS compensation | $995.99 | $48,432 |

If you’re eligible, the amount of your GIS supplement will be added to your existing OAS benefits and should be deposited at the same time as your monthly OAS payment.

How Do I Apply For OAS In Canada?

If you are nearing age 65, then your OAS benefits may be immediately applied. The CRA may begin issuing monthly OAS benefits to eligible seniors based on their income from the previous tax year.

If your OAS benefits are to be automatically applied, the CRA will issue you a letter a month after your 64th birthday explaining that you’ve been enrolled in the program.

Alternatively, if the CRA needs more information to complete your enrollment, they’ll send a similar letter explaining what they need from you and inviting you to apply.

You can apply with a traditional paper form or apply through your My Service Canada Account. I suggest applying online, as your application will be processed quicker and you don’t have to worry about anything getting lost in the mail.

During your application process, you’ll enter your personal banking information, which is where your OAS payments will be deposited every month.

When Can I Apply For OAS?

You don’t have to wait until you're 65 to apply for OAS. You can begin the application process a month after you turn 64. This gives you time to make sure that everything is set up and ready to go so that you can start receiving your benefits as soon as you turn 65.

How Long Does It Take To Receive My OAS Payments After I Apply?

As long as all of your paperwork is in order and your OAS application has been processed by the CRA, then you can expect to receive OAS payments starting the month after you turn 65.

OAS payments are issued every month on specific dates. Refer to the list of payment dates above to see the closest payment date after your birthday.

Applying For OAS Retroactively (After Age 65)

If you apply for your OAS benefits after you turn 65, you can be compensated for up to twelve months of payments that you would have received if you had applied on time.

For example, if you wait until age 68 to apply for OAS, then you’d only be eligible to receive back payments for the previous year, starting after you turn age 67.

This is why it’s very important to make sure that you apply for and are approved for your benefits by age 66 at the latest. Otherwise, you’ll be missing out on money that you would have otherwise been eligible for.

Should I Defer My OAS Benefits?

If you’re approaching your 65th birthday and still earning a decent income, you may want to consider deferring your OAS benefits for a year or so. This can help you avoid the OAS clawback and increase the number of OAS benefits you’re eligible for.

Every month after age 65 that you defer OAS benefits, you’ll be awarded 0.6% extra when you do start accepting your benefits. This totals out to an extra 7.2% for every year that you defer payments.

You can only defer your payments for up to five years, though, for a total of 36% additional OAS benefits. After this point, there’s no further benefit to deferring your payment. Here’s a quick visual breakdown:

| OAS Benefit Starting Age | Months Past Age 65 | OAS Benefit Increase |

|---|---|---|

| 66 | 12 | 7.2% |

| 67 | 24 | 14.4% |

| 68 | 36 | 21.6% |

| 69 | 48 | 28.8% |

| 70 | 60 | 36% |

Can You Receive OAS If You Live Outside Of Canada?

Canadian citizens who live outside of the country can receive eligible OAS benefits if they meet one of the following criteria:

-

You spent at least 20 years in Canada after your 18th birthday.

-

You’ve lived and worked in a country that shares Canada’s social security agreement. You must have spent a collective 20 years between Canada and that country.

As an out-of-country resident, the 10-year minimum residency required for standard OAS payments in Canada is increased to a 20-year minimum. As you approach retirement, keep this in mind and plan your living situation accordingly to ensure that you receive full benefits.

Are OAS Benefits Changing In 2023?

As of 2025, the eligibility age to receive OAS benefits remains at 65 years.

While there have been discussions about increasing this age, no changes have been implemented. Research suggests that Canadians are living longer and healthier, so this change reflects that.

Aside from this major change, you can also expect incremental quarterly increases in OAS benefit payments to account for the ever-changing inflation rates.

Why The OAS Age Increase Is So Controversial

This policy shift was originally proposed as a measure to address the long-term sustainability of the OAS program amid changing demographics (specifically the aging population and increased life expectancy).

The plan to increase the retirement age from 65 to 67 was first proposed in the 2012 federal budget and has been a topic of hot debate since.

Proponents argue that:

-

People are living longer today than they were in previous generations

-

Increasing the age is necessary to ensure the program remains for future generations

-

A default retirement age of 65 can put social pressure on those are able and who want to work later in life

Critics argue that:

-

It disproportionately affects vulnerable populations, such as lower-income individuals

-

Those with physically demanding jobs could be forced to work later despite declining health and energy levels

This demographic often relies heavily on OAS benefits, and delaying access could put them at financial risk or force them to work despite declining health conditions.

There is also the issue of generational equity.

According to a recent survey by the Healthcare of Ontario Pension Plan (HOPP), 86% of Canadians under 35 are already concerned about their ability to save for retirement with the rising cost of living.

Now, they're being asked to work even longer.

Shifting the age requirement puts an unfair burden on younger generations, who must now work longer to receive the same benefits that older generations received at age 65.

At its core, this changes the social contract and the expectations that people have been planning around for their retirement.

What are your opinions on the recent change from 65 to 67? Let me know in the comments below!

Conclusion

The OAS pension plan is available to all eligible Canadians over age 67 and provides more financial security during your retirement.

If you want to maximize your OAS benefits, it’s important to start planning ahead, though.

Are you prepared for your retirement?

The more prepared you are, the more comfortable you’ll be able to live and the less stress you’ll have to deal with.

If you’re ready to start preparing and planning for your retirement, be sure to check out my ultimate guide to retirement planning in Canada next!

Not sure how much you need to retire? Check out a Youtube video I made about it here:

Frequently Asked Questions (FAQs) About OAS Payments in Canada

1. What is the OAS payment amount for 2025?

As of April–June 2025, the maximum monthly OAS benefit is:

-

$727.67 for ages 65–74

-

$800.44 for ages 75 and older

These amounts are reviewed quarterly based on changes to the Consumer Price Index (CPI).

2. When will I receive my next OAS payment?

OAS payments are issued monthly. You can check the full OAS payment schedule here to see the exact dates for 2025.

3. How is my OAS payment calculated?

Your payment is based on:

-

How many years you've lived in Canada after age 18 (full benefits require 40 years)

-

Your net world income

If you’ve lived in Canada less than 40 years, you’ll receive a prorated amount.

4. Is OAS income taxable?

Yes, your monthly OAS payments are considered taxable income and must be reported on your tax return.

5. What is the OAS clawback threshold for 2025?

If your net world income exceeds $93,454, your OAS benefits may be reduced at a rate of 15% for every dollar above that threshold.

6. Can I defer my OAS payments?

Yes, you can defer receiving OAS for up to 5 years (until age 70). You’ll earn 0.6% more per month deferred, up to a maximum increase of 36%.

7. Can I receive OAS while living outside Canada?

Yes, if you’ve lived in Canada for at least 20 years after age 18, or if you qualify under a social security agreement, you may receive OAS abroad.

8. How do I apply for OAS?

You can apply online through your My Service Canada Account or by submitting a paper application. You may also receive an automatic enrollment letter around your 64th birthday.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.