What’s the best age to retire in Canada? Let’s first take a look at when Canadians are choosing to retire.

46% of Canadians expect to retire between 60 and 70, according to this Scotiabank survey.

This is quite accurate, as Stats Canada shows that the average retirement age of Canadians in 2021 was 64.4 years old.

My parents have both retired within this age range, and it seems that our society is set up for people to retire around this time.

But more people than ever are choosing to buck the trend and retire either earlier or later in life.

You must determine what is the best age to retire given your unique situation. I’ll review several options that you can choose from, but first, let’s begin with the most common age range.

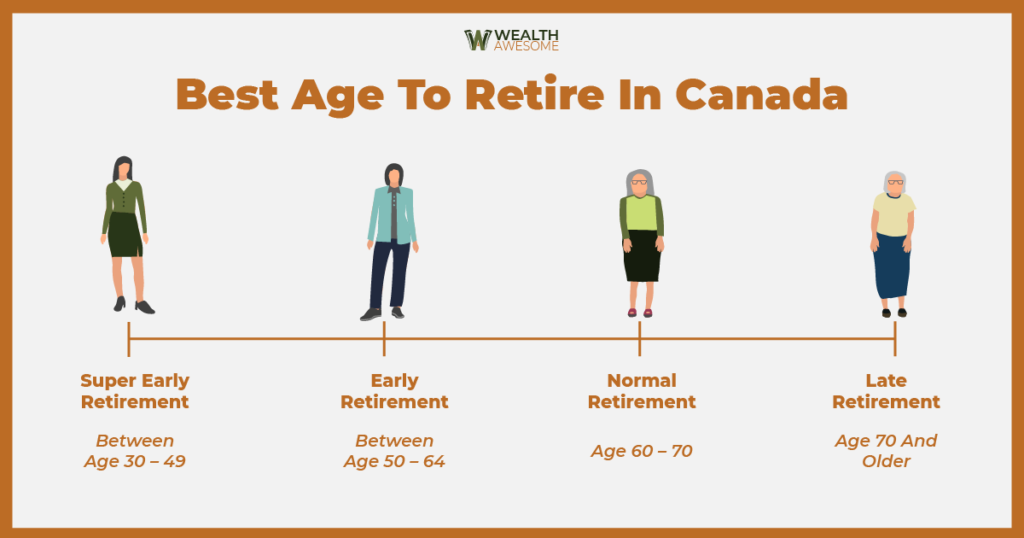

Retirement Age In Canada: What’s Normal?

Some begin planning their retirement as soon as they enter the professional workforce, while others are halfway through their careers and just starting to contribute to a retirement savings account.

Although the average age most Canadians retire at is between 64 and 65, there’s really no “right” age to retire at, as this is largely dependent on individual wants and needs.

If you truly love and enjoy the work you do, then you shouldn’t feel pressure to retire. On the other hand, if you’re willing to work hard and budget wisely, you could stand to retire at a far earlier age and begin pursuing your true hobbies.

Normal Retirement Range: Age 60 – 70

Most Canadians choose to retire in this age range, and it’s easy to see why. Government pensions will kick in during this time, such as your Canada Pension Plan (CPP) and Old Age Security (OAS) payments.

You can start taking your CPP Pension the earliest at age 60, but the longer you delay, the higher the payments you will receive.

- If you start your CPP at age 60, you’ll receive 36% less than if you start it at age 65.

- If you start your CPP payments at age 70, you’ll receive 42% more than if you start it at age 65.

This can be a significant retirement income source for many Canadians, so many have no choice but to wait until this age.

There’s also societal pressure to retire at this age. If most of your friends and colleagues are retiring in this age range, you might get lonely or bored if you decide to retire earlier or later.

Late Retirement – Age 70 and Older

The number of Canadians retiring 70 and older has more than doubled in the last ten years, which is a staggering increase.

Here are some of the reasons more Canadians are choosing to retire later in life:

- No more mandatory retirement age of 65: In 2009, the government decided to get rid of this restriction, giving Canadians a choice to continue to work as long as they wanted to.

- People are living longer: With advancements in health care and the overall well-being of Canadians, we are living longer than ever. That means that more money will be needed in retirement, so more people choose to work longer. Two out of five Canadians who are 65 currently will live past the age of 90, which is a very long time to retire.

- Some people enjoy their work: I know it sounds crazy, right? But it’s actually quite common for many people to get bored during retirement. Or they are passionate about their job, so they decide to continue to work.

- Money: Probably the most obvious one is that you will earn more money when you work more. You’ll also maximize your retirement income payouts, such as your Canada Pension Plan (CPP) and OAS. The fear of running out of money keeps many people working past the age of 70.

Early Retirement – Between Age 50 – 64

Many Canadians dream about retiring early, as they start to get burned out from their work in their 40s and 50s. I’m sure most people would retire early if they had the means.

It requires a lot of discipline, and you must be either able to save a high percentage of your income each year and invest it wisely or make a lot of money.

While it’s easy to see the benefits of early retirement, such as more free time, less stress, and the ability to travel, there are also downsides to early retirement.

Stress can be added if you didn’t save enough money, with a constant worry about not having enough to last. You could also get bored or lonely if nobody else you know is retired, which can harm your health.

If early retirement is your goal, think it through carefully, and ensure you have planned your finances perfectly!

Super Early Retirement: Between Age 30 – 49

There’s a new movement called financial independence, retire early (FIRE), where many people are choosing to adopt a very focused and ambitious goal of retiring very early in their life, usually by saving a lot of money and investing in the stock market or Exchange-Traded Funds (ETFs).

It requires a lot of discipline in your early years of life, with many starting to save in their 20s or even as teens aggressively.

While there are many benefits of retiring early, there can be a lot of risks in retirement planning for extremely early retirement. You’ll have to consider the huge sacrifices that will need to be made and the unpredictability of life.

There’s a lot that can happen in life that would throw your calculations off, and you may need to either start working again or abandon it altogether.

You’ll also need to find other projects or things to find meaning and satisfaction from doing. I’ve had some personal experience with the FIRE movement, and you can learn about it here.

Retirement Income Sources

No matter what age you plan on retiring at, you’ll need to have a reliable source of income to sustain you from the day you retire through the end of your life.

Most Canadians are entitled to some government retirement benefits, including:

However, these government benefits alone aren’t enough to keep up with most retirees’ cost of living.

This is why it’s important to start investing in your retirement as young as you can. The more you’re able to save while you’re young, the more financial security you’ll have when you decide to retire.

With that in mind, here’s a breakdown of the top retirement income sources you can tap into.

Registered Retirement Income Fund (RRIF)

Any Canadian over 18 can open and contribute to a registered retirement savings plan (RRSP). These registered retirement accounts can hold cash savings but are more often used as investment vehicles to hold:

- Stocks

- Bonds

- ETFs

- GICs

Over the course of your career, these investments should steadily grow, compounding tax-free over time.

To ensure fairness, RRSPs are federally regulated, and account holders must stay within their annual contribution limits, as defined by the CRA each tax year. The good news is that RRSP contributions are income-tax deductible, which can help you save on taxes each year.

Once you officially retire, your RRSP will be transferred into a registered retirement income fund (RRIF), and you’ll be able to schedule regular withdrawals to fund your retirement. These withdrawals will be subject to standard income tax, similar to if you were receiving a regular paycheque.

Tax-Free Savings Account (TFSA)

TFSAs are another type of registered account available to all Canadians. While they’re not specifically meant for retirement, they can be used as tax-advantaged investment vehicles, allowing you to invest in stocks, bonds, and other investments.

Any profits realized within these accounts can be withdrawn tax-free, meaning you don’t have to worry about capital gains tax.

- Related Reading: TFSA vs RRSP: Which Is Better?

Business Income

If you are retiring from managing a business that you own (whether fully or in part), you could earn a steady income as the business continues to profit.

Alternatively, many retirees start a business after retiring and leaving their careers behind. While starting a business can be risky, it can provide you with a fulfilling project to work on and may become a significant income source.

Life Income Fund (LIF)

LIF retirement accounts are similar to RRIFs and are retirement income accounts typically associated with employer-sponsored LIRAs and RRSPs.

These aren’t as common as RRIFs, due to the fact that they’re harder to transfer in the event of a career change. You can read more about them here.

Part-Time Retirement Income

An increasing number of Canadian retirees are working part-time jobs even after retirement.

Some simply get bored of the stagnant retiree lifestyle and want to get out and about, meet new people, and stay active. Others do so because their other sources of retirement income aren’t enough to keep up with the inflated costs of living in the country.

Entering the gig economy by driving for rideshare companies like Uber or Lyft is a great way to earn some side income while retaining a flexible schedule that fits your lifestyle.

There are also lots of opportunities to earn part-time retirement income online by tutoring, writing, and even creating art.

- Related Reading: Best Retirement Jobs From Home

Finding the Balance

There’s no right answer as to what is the best age to retire in Canada. It’s such a personal decision, and sometimes, it’s not a choice of when you retire. You can get forced out by your company, or you might need the money, so you can’t retire until later.

The most important thing is finding a balance and making the decision that will ultimately make you the happiest. Maybe you enjoy your work and colleagues and want to continue past your 60s.

Or maybe you want to retire early because you value your time with your grandchildren or spouse or quit the rat race to travel in an RV across the continent.

Whatever age you plan on retiring, try to time it the best that you can! Learn more about the best pension plans In Canada here.

Still unsure of when to retire? Check out my Youtube video on this topic here:

Great article. I would be interested to see what the long term trend is for people who choose the “FIRE” option. Do they end up going back to work? Full-time? Part-time? Perhaps this movement hasn’t been around long enough to see the trends?

A lot of people don’t truly “retire”, but they are always working on projects, only now they have the freedom to really choose whatever they want to do.

Informative concise article! I think there is a typo in this statement “If you start your CPP payments at age 70, you’ll receive 42% more than if you start it at age 70. ” I think you meant “start it at age 70” to be “start it at age 60.” right?

Thanks Tony, I changed it to start it age 70 vs age 65

nope 65-70