Do you have trouble meeting your expenses? Don’t worry; you’re not alone. Millions of Canadians find it hard to survive in today’s expensive world.

About 48% of Canadians are left with only about $200 at the end of the month after paying off debts and covering primary living expenses.

What if there was a better alternative? Before quitting my job to pursue my dream of working online and travelling the world, I had to save heavily to start my own business. I cut out unnecessary expenses and adopted a frugal lifestyle.

It was a hard switch at first, but many of the habits I picked up during that time stayed with me.

If you are looking to make some lifestyle changes and tame your ever-growing expenses, this article may help you. Adopting at least some of these tips can allow you to start your own frugal living in Canada journey.

What Does Frugal Living in Canada Mean to You?

Frugal living in Canada is quite similar to living frugally anywhere else. Basically, it requires you to live below your means. The key is to do it without sacrificing any of your happiness or freedom.

Many people turn their noses up to the notion of frugal living because they don’t have clarity regarding frugal vs. cheap. They think it’s all about pinching pennies, saving money whenever and wherever you can, and only spending money on necessities.

To me, that’s a completely wrong take on the word. It leans more towards being financially disciplined and careful.

Financial frugality is freeing, not limiting. By saving a lot of money, it gives you options in life. The option to quit your job to pursue a business. The option to retire early to spend more time with your children. The freedom to never have to rely on anyone else for financial support.

Another confusion that many people have regarding frugal living is about class. They believe you must spend a certain amount on certain things to fit into a social class. The truth is that frugality can be one of the defining characteristics of wealth, as shown by billionaires such as Warren Buffett, who lives well below his means.

Creating a Budget

Before you try any of the tips below, create a budget! This is one of the most important steps in frugal living. A budget helps you keep track of your income and expenses and can help you make informed decisions about your spending.

Tracking Expenses

The first step in creating a budget is to track your expenses. This means keeping track of every dollar you spend, from rent and groceries to entertainment and clothing. There are many ways to track your expenses, including using a spreadsheet, a budgeting app, or simply writing everything down in a notebook.

Once you have a good idea of where your money is going, you can start to look for areas where you can cut back. For example, you might find that you’re spending too much on eating out or buying unnecessary items online.

Related Reading: 25 Best Budget Apps in Canada

Reducing Debt

If you have debt, it’s important to make a plan to pay it off. This might mean making extra payments on your credit cards or loans or consolidating your debt into a single payment with a lower interest rate.

Reducing your debt can help you free up more money for savings and other important expenses. It can also improve your credit score and help you achieve your long-term financial goals.

Establishing an Emergency Fund

This is a savings account that you can use to cover unexpected expenses, such as car repairs or medical bills.

Ideally, your emergency fund should have enough money to cover at least three to six months’ worth of expenses. This can help you avoid going into debt or relying on credit cards when unexpected expenses arise.

Frugal Living Canada Tips

Though frugal living practices might differ significantly from individual to individual, the tips we share can be used by everyone. Also, the amount you can save through the tips below is based on what part of your income you usually spend on it.

LifeStyle

Lifestyle expenses should be the first ones you trim down when you are adopting a frugal lifestyle.

1. Clothing

Potential Monthly Saving: $50-$100

Canadians are not as fashion-crazed as some other nations, but you might still spend between 2.5% and 4% of your income on clothing.

You can cut that down by learning to mend and sew so that your old clothes will serve you longer. Buy rugged clothing items that last longer.

Follow wash-dry instructions not to wear out the fabric before its time. Better yet, buy second-hand, and hit garage sales and thrift stores. Trade your expensive clothes at consignment stores. Buy when clothes (especially out-of-season ones) are on sale.

2. Fitness

Potential Monthly Saving: $40-$200 (Depends if you attend a high-end gym or a basic one)

The most “frugal” of gyms can cost you about $10 a month and about $40-$50 at the time of initiation. Instead of going to a mid-to-high-end gym, you can choose one of these basic gyms to get healthy or beef up. Better yet, don’t choose a gym in the first place. Set up a home gym, walk, jog or run for cardio, and do push-ups, squats, and crunches to get fit.

I’ve switched from weight lifting to calisthenic body-weight training, and not only has it saved me a lot of money because I don’t need a gym membership, but I’m in the best shape of my life, and my joints don’t hurt anymore.

You can also get social and try low-cost sports like basketball or soccer or join a running club.

3. Accessories

Potential Monthly Saving: $30-$55 (You can save even more by sticking with a few basic accessories)

Minimizing your selection, buying a few good-quality accessories that last longer, and taking care of your stuff can help it last longer.

Buy simple jewelry items and sturdy handbags that can go with most of your outfits. If you always wear a watch, invest in a rugged watch that can weather the times with you.

4. Switch to a High-Interest Savings Account (HISA)

Potential Monthly Savings: $10 – $100+

If you’re currently earning a very low-interest rate on your savings, consider switching to an online bank with a high-interest savings account.

Instead of earning less than 0.1% interest on your savings, you can currently earn 2.50% per year at an online bank like EQ Bank here.

Read my full guide on the best high-interest savings accounts in Canada here.

Related Reading: Best GIC Rates in Canada

5. Use Cloth Diapers

Potential Monthly Saving: $80-$160

It’s truly a lifestyle choice if you decide to wash soiled diapers yourself. Of course, there is the “grossness” factor, and this method of saving might be a bit too extreme for most people.

Cloth diapers would initially cost more than a pack of disposable diapers, and this is one thing I would definitely recommend buying new! But over time, you should save significantly on your diaper cost. If you don’t wash them yourself, don’t bother with buying cloth diapers. If you get them professionally laundered, the cloth diapers will likely cost you the same or even more than disposable ones.

Transportation

There are so many ways to save on transportation and here are some of my top choices:

6. Save on Gasoline

Potential monthly savings: $100 – $300

Gasoline prices are unpredictable, and when it is high, it can really hurt your wallet. Some great ways to save on gasoline are:

- Use an app like Gasbuddy or CAA to track prices

- Go to Costco for cheaper prices

- Change your driving habits to make your fuel use more efficient

- Keep your car well-maintained

Check out this list of the top ways to save money on gasoline in Canada.

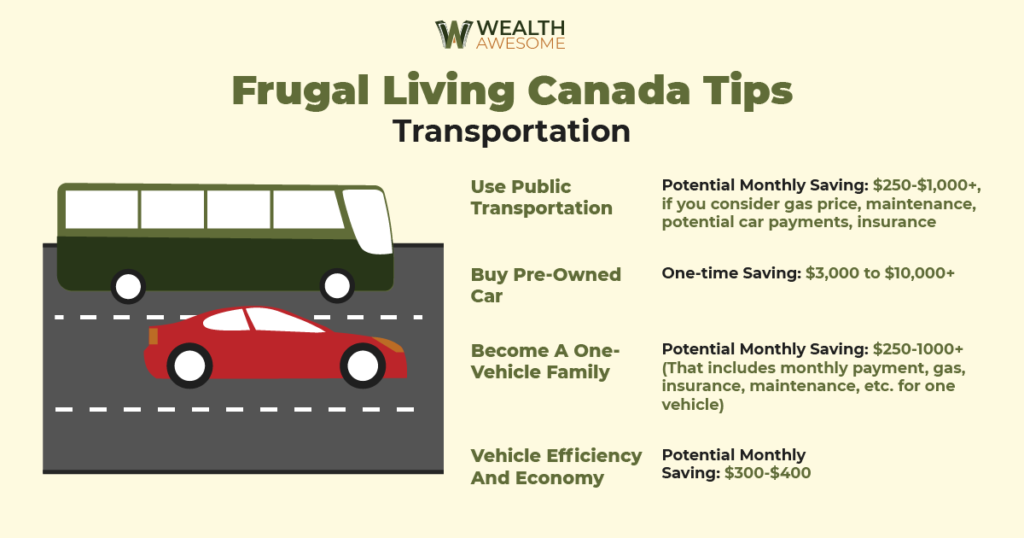

7. Use Public Transportation

Potential Monthly Saving: $250-$1,000+, if you consider gas price, maintenance, potential car payments, insurance

Even if you own your car, you can save a lot of money by using public transport for the bulk of your commute (travelling to and from work). If you don’t own a car and plan on buying one in installments, public transportation will be a significantly cheaper and frugal option.

8. Buy Pre-owned

One-time Saving: $3,000 to $10,000+

If you are planning to buy a car, why not choose a pre-owned vehicle that’s in decent shape instead of shopping around for a brand-new one? You can get three, to four-year-old models that are just driven 50,000 kilometres in total. If it’s in good shape, you don’t have to worry about fuel economy.

Ideally, you should buy it outright, saving you money on interest on monthly payments. Even if you can’t, monthly payments and insurance for pre-owned cars can be cheaper than new vehicles.

9. Become a One-Vehicle Family

Potential Monthly Saving: $250-1000+ (That includes monthly payment, gas, insurance, maintenance, etc., for one vehicle)

If you have two vehicles in your household, switching to one can be an amazing way to save money. It might be a bit inconvenient, especially if two working spouses have to go to the opposite side of the city to work. You can alternate daily or weekly on who takes the car to work. The other person can use public transport. It will free up a lot of your monthly income.

10. Vehicle Efficiency and Economy

Potential Monthly Saving: $300-$400

Even with just one car, you can save on many costs. Although I never recommend getting a car loan, if you have to, by choosing a five-year loan term instead of two or three, you can lower your monthly payments considerably though it would cost a lot more in the long run.

If you bundle your vehicle insurance with home insurance, you can cut the cost between 10% and 15%. You can contact a car insurance broker to find a better deal if you’re in a privatized insurance province.

I cut my monthly car insurance from $150 to about $80 with a quick phone call (I lived in Alberta at the time)

Learn to maintain your car yourself, and only consult a mechanic when necessary. Park your car where you don’t need to pay a fee and walk from there. Gas credit cards (if used wisely) can earn you a decent amount of cashback.

Related Reading: Is buying a hybrid car in Canada worth it?

Utilities and Entertainment

Cutting some home and utility expenses can help you “live within your means.”

11. Save on Electricity

Potential Monthly Saving: $30-50 per month (Ontario rates, if electricity consumption drops from 1,000 kWh to 750 kWh)

Use a programmable thermostat and program it to the most cost-friendly setting. If it seems chilly, you can wear a sweater and socks. Use a slow cooker and benefit from natural light as much as possible. Buy energy-efficient appliances and don’t keep them on standby.

12. Save on Heating

Potential Monthly Saving: $30-$45 (If you can bring down your heating costs by about 30%)

Lower your thermostat settings at night, and warm only the room you are sleeping in. Turn the heat down on your water heater by about ten degrees. You will get used to it, and it will save a lot of fuel.

Rework your insulation, clean your filters, and re-caulk if you feel a draft coming in. Insulation around the windows and keeping doors and windows closed can also prevent heat from escaping.

13. Cut the Cable Cord

Potential Monthly Saving: $25-$40 (If you opt for Netflix and other Online providers instead of Cable)

How much time do you really spend watching TV nowadays? The chances are that you spend more time on the internet or streaming movies. If you cut the cord, you can easily save about $25 to $40 a month. You can also hunt for free or cheaper services to increase your options while keeping the cost lower than cable.

14. Eating Out

Potential Monthly Saving: $100 – $300+ (for each meal)

If you eat only twice a month, you can save a lot of money by only going out once. Most families eat out way more than this, though.

Choosing to go out for lunch over dinner can also reduce the cost. If your pride can handle it, you can look at deals on websites like Groupon to see if there are any good restaurant discounts in your area. For example, a quick search on Groupon in Vancouver shows a lot of 30% or more discounted restaurants.

Grocery Expenses

Grocery costs are getting sky-high in Canada. Here are some ways to save.

15. Cook from Scratch

Potential Monthly Saving: Three to five times less if you cook rather than order in or go out for lunch/dinner.

If you can learn to cook from scratch and buy your ingredients in bulk (not the fresh items), you can cut your food budget down to a fraction. That’s especially true for working individuals who prefer to eat lunch at a restaurant. If they switch to home-cooked meals for work, a one-time $15 meal will only cost about $2 – $4.

16. Buy Generic Brands

Potential Monthly Saving: $75 – $100 (about 25%-50% if you typically only buy name brands)

Generic and local brands are usually much cheaper, and if you can find the right one, they are even better than the name brands. For most basic ingredients, there isn’t much difference in taste and quality at all.

It might take some getting used to (and a significant bit of hunting to find the right replacement), but it can save you a lot of money in the long run.

The best example I can find with this is the Kirkland brand in Costco, which I find to be better than most big-name brands for many of their products.

Related Reading: Is a Costco Membership Worth It?

17. Buy and Cook in Bulk

Potential Monthly Saving: About 25% on your grocery bill

If you buy non-perishables, seasonal fruits and vegetables, cheese, nuts, canned goods, flour, meat, and other items in bulk, especially when they are on sale, you can reduce your grocery bill by at least 25%.

Similarly, cooking in bulk and freezing it for later use not only saves you time but it’s also better for your electricity consumption and ingredient usage.

18. Coupons, Sales, and Price Match

Potential Monthly Saving: $80 to $100

Make use of coupons whenever you can. Whether you are shopping online or cutting coupons out from flyers, there are various ways to get a little discount when you are grocery shopping. Similarly, try visiting your regular store whenever they are having a sale.

But to stay within your means, make sure you write a grocery list and follow it instead of buying wastefully simply because it’s cheap. If your store offers price matching, a little research can easily save you some bucks.

For a complete list, check out this full guide on how to save money on groceries in Canada.

Housing

Housing is the core expense for most Canadians. If you can find some easy ways to save even a fraction of the cost, that can go a long way.

19. Search for Lower Rent

Potential Monthly Saving: $300 to $1,000 (Varies significantly from city to city, province to province)

Ideally, you shouldn’t spend more than 30% of your pre-tax income on rent. But the lower, the better. You can pay less in rent by widening your search radius and shopping away from downtown.

Don’t rent a bigger place if you don’t need it. If you can live in a studio apartment, don’t shop around for a two-bedroom. Ask about the utility cost and parking situation. You may be able to negotiate the landlord to a lesser price if the apartment/home has been sitting on the market for a long time.

20. Shop for the Best Mortgage Rates

Potential Monthly Saving: A wide range, but you can reduce your monthly payment by about $800 simply by opting for a longer amortization period

You can only get eligible for the best mortgage rates if you have an excellent credit score. By saving up for a 20% down payment, you can save money on CMHC insurance. Shop around for the best rates and terms possible, and calculate whether a fixed or variable mortgage suits you.

21. Downgrade To a Smaller/Cheaper Home

Potential Monthly Saving: About 25% to 50% on monthly mortgage payments

You can save a lot of money if you choose a smaller home that’s a bit far away from the suburbs instead of choosing the best house you can afford.

Your home is an asset; the sooner you can pay it off, the better it will be for your housing expense. A cheaper home would be significantly easier to pay off, and your monthly payments will be lower.

22. Put Your Home To Work

Potential Monthly Saving: $325 to $1,100 (median and average Airbnb earnings)

If you have enough space and you don’t want to downgrade, put your home to work. Short-term rentals (Airbnb) can easily earn you about $300 or more a month (don’t forget about the taxes), while more successful hosts earn significantly more than that. If you are open to long-term rentals, that might be even better. You will have a steady income stream, which can go towards your housing.

23. DIY Projects

Taking on some DIY projects around the house can save you money and give you a sense of accomplishment. Here are some ideas for DIY projects:

- Make your own cleaning products: You can save money and reduce your exposure to harmful chemicals by making your own cleaning products using simple ingredients like vinegar and baking soda.

- Start a vegetable garden: Growing your own vegetables can save you money on groceries and provide you with fresh, healthy produce.

- Repair instead of replace: Before you throw out a broken appliance or piece of furniture, consider if it can be repaired instead. You can save money and reduce waste by fixing things instead of buying new ones.

- Seasonal shopping: Shopping for seasonal items like gardening supplies and holiday decorations at the end of the season can save you money. Look for clearance sales and discounts on items that will be in season next year.

24. Leave Canada

I had to sneak this one in here because it is near and dear to my heart. If you can work online from anywhere, consider leaving Canada to live in another much cheaper country.

You won’t have to sacrifice much in terms of luxury if you do it right, and you can enrich your life in so many other aspects. Here’s an example of what a $ 400-a-month apartment looks like in Vietnam (see the video above), which is steps away from a beautiful beach.

I’ve travelled to places in Mexico, throughout Asia, and Europe, which had much cheaper rents than Canada. For the rent price of a 1-bedroom condo in a place like Vancouver or Toronto, you can cover nearly all your living expenses in a cheaper country like Thailand, Mexico, or Columbia.

I know this isn’t the most feasible option for many Canadians, but if you can take steps to build this type of lifestyle, it can be very rewarding!

Smart Banking and Credit Use

When it comes to frugal living, smart banking and credit use can help you save money and avoid unnecessary fees. Here are some tips to help you make the most of your banking and credit options.

25. Choosing the Right Bank

Choosing the right bank can make a big difference in how much you pay in fees and how much interest you earn on your savings. Look for a bank that offers low or no-fee accounts, competitive interest rates on savings accounts, and convenient online banking options.

Consider credit unions as an alternative to traditional banks. Credit unions are not-for-profit organizations that often offer lower fees and better interest rates than banks.

26. Understanding Credit Cards

Credit cards can be a useful tool for building credit and earning rewards, but they can also be a source of debt and fees if not used wisely. Here are some tips for using credit cards wisely:

- Pay your balance in full each month to avoid interest charges.

- Choose a card with no annual fee and a low-interest rate.

- Use your card responsibly to build your credit score.

- Avoid using your credit card for cash advances or balance transfers, which often come with high fees.

27. Avoiding Late Fees

Late fees can add up quickly and eat into your savings. Here are some tips for avoiding late fees:

- Set up automatic payments for your bills to ensure they are paid on time.

- Keep track of your due dates and set reminders to avoid missing payments.

- Contact your creditors if you are having trouble making payments to discuss your options and avoid late fees.

Conclusion

Frugal living in Canada can help you live within your means. Even if you earn a decent amount of money, some of these tips can help you save more, which will help you achieve your other financial goals faster.

You may pay off your home and your car sooner, choose early retirement or take more vacations. By maximizing your income, careful financial planning, and adopting some frugal habits, you can easily achieve financial independence in Canada.

Check out this master list of ways to save money in Canada.

I feel like I am a frugal person but there is always room for improvement! My husband and I are also trying to buy a house in the DC area and it is proving almost impossible to do so without spending more than you want. We will keep looking though!

Great tips! The one thing I would add to the transportation category are scooters, as in those cute things people associate with countries like Italy. I’m assuming that the rest of Canada is like BC (if not, my apologies), where your car license is all you need to ride a 49 cc or smaller. Unfortunately, for anything above that a minimum modified motorcycle license is required. My husband and I live in Metro Vancouver, and have commuted to work for years on our scooters. At one point we lived across the street from a Skytrain station in Burnaby. I worked downtown Vancouver, and it was significantly cheaper to commute by scooter than it was by public transit. And I got there in the same amount of time as it would have taken by Skytrain. I was fortunate that I was allowed to park by the bike racks my employer had set up for cyclists, so no downtown parking fees. As for speed, it kept up easily with traffic, and I often passed cars, who for some reason never thought to use the non-HOV curb lane.

Great tip Jennifer! I love scooters. In Southeast Asia most people travel with scooters, and it’s amazing how cheap they are to buy and operate. I spend about $5 a week on gas when I have a scooter. Vancouver is a good place to ride, but other cities that are colder in Canada are not as practical though.