CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

Planning to retire in Canada someday?

Then it’s important to get a handle on all the different sources of income available to retired Canadians.

I’ll focus on the more common ones I’ve seen from my days as an investment and insurance advisor.

Here are the crucial retirement income sources in Canada that you should be aware of.

Navigating Canada's Retirement Income System

Whether you plan on retaining your current lifestyle, upgrading, or downsizing, you'll need a steady source of retirement income to keep the bills paid during your "golden years."

From government pension plans to employer-sponsored pension plans and personal accounts, these are the top sources of retirement income you'll be able to choose from.

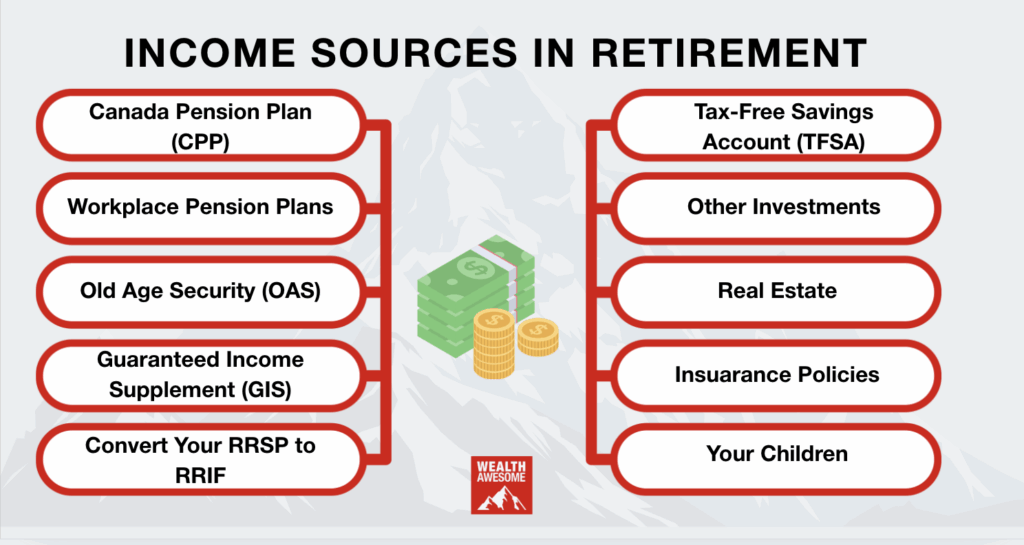

1. Canada Pension Plan (CPP)

The CPP tops this list because it is Canadians' most common source of retirement income. Most working Canadians should qualify for this payment, regardless of income level.

How Much CPP Can You Get?

It’s a bit tricky to forecast what your exact CPP payments will be, and the CRA doesn’t disclose it until you retire, but it gets easier as you approach retirement.

As of 2024, the average CPP payout is approximately $758.32/month, while the maximum is $1,364.60/month. Here’s a link to the YMPE amount for all prior years.

The YMPE (Yearly Maximum Pensionable Earnings) for 2024 is $68,500.

To learn more about how much CPP you can get, read this article.

What Age Should You Start Your CPP?

Deciding what age to start your CPP is crucial. You’ll be able to start it at any year between the ages of 60 to 70. Here are some quick facts you should know about making this decision:

CPP Age Decision:

-

If you start taking CPP at age 60: You will receive 0.6% less per month or 36% less if you start taking your CPP at age 60 vs. age 65.

-

If you start taking CPP at age 70: You will receive 0.7% more per month or 42% more than if you start taking your CPP at age 70 vs. age 65.

-

If you live past age 74: You will earn more money if you start CPP payout at age 65 then at age 60.

-

If you live past age 81: You will earn more money if you start CPP payout at age 70 then at age 65.

For a more in-depth breakdown of what age to start your CPP, read this guide.

CPP Disability Benefits

If you answer yes to this checklist:

-

Are suffering from a severe and prolonged disability.

-

Made enough contributions to the CPP.

-

Are under the age of 65.

You might qualify for CPP Disability Benefits, so check with the CRA. For more details, read this CPP disability eligibility guide.

The Quebec Pension Plan (QPP): For Quebec Residents Only

Similar to the Canada Pension Plan (CPP), which serves the rest of Canada, the Quebec Pension Plan (QPP) is funded by contributions from both employees and employers.

Although these two programs are very similar, there are a few key differences between the QPP and CPP.

For one, the QPP is managed by the Caisse de dépôt et placement du Québec, while the CPP is federally managed.

Rates for contributions and benefits may also vary between the two. For instance, the QPP has slightly higher contribution rates compared to the CPP, which could lead to higher future benefits for recipients.

Both plans are portable across provinces, meaning you can collect benefits even if you move from Quebec to another Canadian province or vice versa.

Both plans aim to provide a basic level of income during retirement, but they are meant to supplement, not replace, other retirement savings.

2. Workplace Pension Plans

If you’ve worked at a larger Canadian company for any period of your career, chances are you have a workplace pension plan that you can draw on for when you retire.

The pension amount you can receive will vary widely and depends on factors such as your income, the length that you worked at the company, and the performance of the pension investments.

An excellent perk of most workplace pension plans is the matching feature - this is where your employer will match a portion of how much you put into your pension plan. It's like getting free money and if offered by your employer, it should always be taken advantage of to its fullest.

There are two main types of workplace pension plans you can receive:

Type 1: Defined Contribution Pension Plan (DCPP - More Common Today)

The way this plan in Canada works is that you make contributions to the DCPP while you work for your company.

If you are a part of this plan, you can allocate a portion of your salary (before taxes) to the plan. The company you work for can potentially the contribution up to a specific limit that it sets, which is always recommended to do because who doesn’t like free money!

Your company does not manage the amount in your DCPP. As an employee, you have the power to choose where the contributions are invested, but you’re usually limited by the partners and investment options provided by your company.

With a DCPP, there is no guarantee of a fixed amount that you can receive when you retire. It all depends on how well your investments perform.

How to Extract Money From Your DCPP

By the time you retire, you can have options to take out your money and put it in one of three options:

-

A Locked-In Registered Retirement Savings Plan (RRSP) or Locked-In Registered Retirement Income Fund (RRIF)

-

An annuity, or:

-

A combination of these two.

For more info on the DCPP, check out this article.

Type 2: Defined Benefit Pension Plan (DBPP - Less Common Today)

According to this plan, the company you work for will pay you a predefined monthly income for life after you retire as an employee of the company.

The DBPP amount you receive after you retire can be calculated in various ways. Typically, the formula used to calculate the payments you receive is based on the average highest salary you made while you were at the company and the number of years of service you provided the company.

In this plan, the employer is responsible for guaranteeing a certain amount in payments to their employees. The benefit is already defined, regardless of the performance of the investment.

This is fantastic because the employer is entirely responsible for investing the funds and all the gains or losses that come with it. This shifts any investment decision and risk from you to your employer.

The DBPP is an Endangered Species

Companies don’t want the risk of having to pay a specific amount of employees anymore, so you’re seeing almost no new issuances of DBPPs in recent years in Canada.

The vast majority of companies today only issue the Defined Contribution type of pension plan.

For more info on the DBPP, check out this guide.

3. Old Age Security (OAS)

The OAS is an important provider of income for many Canadians.

The payment can be different depending on how long you have lived in Canada. You must have lived in the country for at least 40 years after turning 18 to receive the full OAS pension payment.

If you have not resided in Canada for 40 years after turning 18, you can receive partial pension benefits.

OAS Example: John arrived in Canada at the age of 45. He has been living in the country for 20 years. It means John has spent 20 years as an adult living in Canada. According to the requirements, John is eligible to receive 20/40th of the full benefit – half of what he would receive if he had been living in Canada for 40 years.

As of April to June 2024, OAS payments are:

-

$713.34/month for ages 65 to 74

-

$784.67/month for ages 75 and older

The OAS clawback threshold for 2024 is $90,997. You’ll lose 15% of every dollar above this threshold.

OAS Clawback

Be aware that the CRA will not give you your full amount of OAS even if you do qualify for it. To qualify for GIS in 2025:

If the partner does not receive OAS, the threshold rises to $51,408.

Single seniors must earn less than $21,624 annually.

Seniors with a spouse/partner (who also receives OAS) must have a combined income below $28,560.

Read this ultimate guide on the OAS clawback for more info.

4. Guaranteed Income Supplement (GIS)

The GIS is an additional benefit available to seniors with a low retirement income in Canada who either already receive or qualify for an OAS Canada pension. To qualify for GIS, you must:

-

Have an annual income lower than the maximum annual threshold, and:

-

Currently receive an OAS pension.

The government uses your Federal Income Tax and Benefit return to review your income information. Depending on how much you (or you and your spouse combined) earn, your benefit will automatically renew if you qualify.

Both OAS and the GIS are commonly referred to as government income-tested benefits, since the amount you receive depends on your income.

For low-income seniors already receiving GIS Canada can get a letter in the mail with either the notice that their benefit has been renewed or stopped. It could also state that you need to provide additional information so you can qualify for the benefit.

Check out if you qualify for the GIS here.

5. Convert Your RRSP to an RRIF

Contributions to Registered Retirement Savings Plans are tax-deductible, meaning you can subtract the amount you contribute from your taxable income, effectively lowering your taxable income while allowing you to invest in your retirement.

The funds within the RRSP grow tax-deferred, allowing your investment to compound over time without immediate tax implications.

Say you’re approaching retirement age, and you’ve built up a nice tidy sum in your RRSP. Now what?

Well, it’s time to convert that hard-earned RRSP money into a Registered Retirement Income Fund (RRIF) to start enjoying the fruits of your labour.

There are four main steps to converting your RRSP to an RRIF:

-

Choosing the investment institution: This is simply figuring out where you will hold your money.

-

Complete the RRIF application.

-

Choosing an RRIF beneficiary: Most commonly chosen are your spouse or children.

-

Figure out withdrawal schedule: This is by far the hardest step, and it can get quite complicated in the calculations. You have to start withdrawing by age 71, but you can start before that, also.

It’s a complicated decision of when to start converting an RRSP to an RRIF, which is why I recommend reading this updated 2025 RRIF minimum withdrawal guide for current rates and rules.

Keep in mind that although the funds were able to grow tax-deferred in your RRSP, your withdrawals from the RRIF are subject to income taxes. Over the course of your retirement, these income taxes can really add up and cost you more than you may have budgeted for.

This is one of the key reasons why I often recommend that younger Canadians maximize their TFSA contributions before investing in an RRSP.

TFSAs can hold the same investments as RRSPs and are excellent investment vehicles. Since contributions are made with post-tax dollars, you don't have to pay tax on your withdrawals, which can make your retirement budget simpler.

6. Tax-Free Savings Account (TFSA)

Tax-Free Savings Accounts are Canadians' most popular investment and savings accounts. It edges out the RRSP, with over 57% of Canadians owning a TFSA.

The limit is growing quite high for the TFSA, which is why many Canadians are planning to use it as a retirement income source.

The total TFSA contribution limit as of 2025 is $95,000, assuming you've been eligible since its inception in 2009. The annual limit for 2024 is $7,000.

It’s also the most versatile and flexible investment account. It has such a simple concept that it’s extremely easy to understand: (almost) everything that you invest inside this account will not be taxed on any of the income it earns.

You can plan to take out the TFSA in whatever way you choose as you retire; there are no withdrawal limitations.

Read more with this TFSA Ultimate Guide.

7. Investment Income (Non-registered and More)

All the previous sources of retirement income on this list have either been government payouts, pensions, or registered accounts.

Here are some other common retirement income sources that don’t fall into these categories or that you can hold in a non-registered account:

-

ETFs and Mutual Funds

-

Stocks

-

Bonds

-

Cash Equivalents: GIC, High-Interest-Savings-Account (HISA)

-

Robo-Advisors

-

Alternative Investments

Before opening a non-registered investment account, I recommend maximizing your contributions to a TFSA, where your funds can grow tax-free.

The biggest drawback to non-registered investment accounts is that you must pay capital gains tax once you withdraw the money.

This is a tax that's applied to 50% of the profits realized in an investment account.

For example, if you sell an investment for a $10,000 profit, only $5,000 would be added to your taxable income for that year.

This "inclusion rate" softens the tax blow compared to other forms of income like salary or interest. The tax rate applied to the taxable portion of the capital gain depends on your overall income, and it is taxed at your marginal rate.

That being said, the advantage of non-registered investment accounts is that you don't have to worry about annual or lifetime contribution limits, as you do with TFSAs and RRSPs.

This makes them a good alternative for those who've already maximized their contributions to registered accounts but still have money left over in their personal savings that they would like to invest.

Note that the returns on your investments are not guaranteed, and you need to manage your investments carefully to minimize risks.

Read more about the best investment options in Canada here.

8. Real Estate

Canadians love investing in real estate. And for many retirees today, this has definitely paid off (especially those in Toronto and Vancouver!) There are several ways that you can get retirement income from real estate:

-

Primary Residence - Can take out a Home Equity Line of Credit (HELOC). You can also sell your home and live in a smaller one when you retire. With the primary residence tax-free allowance, you get all the capital gains for free.

-

Rental Income - If you have a residential or commercial property, you can rent it out for extra income

-

Airbnb - You can rent out a room or two in your existing property. Not only can you earn some extra money, but you can meet interesting people from around the world.

To learn more, here’s a list of the best real estate investing options in Canada.

9. Insurance Policies

Here are some ways you can receive retirement income from insurance policies:

-

Term life insurance - if someone you know who has passed away has named you as a beneficiary

-

Whole life or Universal Life Insurance - There is an investment component to these policies, and you can draw out income as you get older. When I was a life insurance advisor though, I usually did not recommend these policies. It’s my opinion that you should keep your insurance and investments separate.

-

Critical Illness Insurance - You can get income from a policy such as this if you suffer from something like a stroke or heart attack. It’s usually given as a lump sum payment.

-

Disability Insurance - If you can’t work due to a disability, you can qualify for these monthly payments if you have the proper insurance in place.

10. Your Children (Or Parents!)

If you’re fortunate enough to have raised successful and kind children, they can help provide income and care for you in your golden retirement years if you’re in need.

Your parents can also provide for you. Sometimes it’s through an allowance, but unfortunately, it is usually through an inheritance when they pass away.

11. Business Income

If you own or are invested in a successful business, you can draw a salary, dividends, or a combination of both to fund your retirement.

If you pay yourself, your salary will be taxed at your marginal rate, while dividends are taxed more favourably due to the dividend tax credit. You may choose to combine both to get the best tax benefits.

If you already own a successful business by the time you retire, you might also consider selling it for a lump sum.

Choosing The Right Retirement Income Sources In Canada

If you’re worried about not having enough sources of income after you retire, you can rest assured that many options exist.

If you’re unsure how much money you need to retire in Canada, check out this guide here.

Frequently Asked Questions (FAQ)

What are the main sources of retirement income in Canada?

The main retirement income sources in Canada include the Canada Pension Plan (CPP), Old Age Security (OAS), Guaranteed Income Supplement (GIS), workplace pensions, RRIFs, TFSAs, and personal investments such as stocks, bonds, and real estate.

Is CPP enough to retire on in Canada?

For most Canadians, CPP alone is not enough to fund a comfortable retirement. It is designed to replace only about 25–33% of your pre-retirement income. It’s important to supplement CPP with other sources like RRSPs, TFSAs, or workplace pensions.

What is the difference between CPP and OAS?

CPP is based on your work history and contributions during your working years, while OAS is a government benefit available to most Canadians over 65, regardless of work history, based on residency and income.

At what age can I start collecting CPP and OAS?

You can start CPP as early as age 60, but your benefit is reduced if you take it early. The standard age for OAS is 65, but you can defer it up to age 70 to increase your monthly payments.

What is the OAS clawback threshold for 2024?

In 2024, the OAS clawback threshold is $90,997. If your income exceeds this amount, your OAS benefit will be reduced by 15 cents for every dollar above the threshold.

How much can I contribute to my TFSA in 2024?

The TFSA contribution limit for 2024 is $7,000. If you’ve been eligible since 2009 and have never contributed, your total available room is $95,000.

What is the difference between a DCPP and a DBPP?

A Defined Contribution Pension Plan (DCPP) depends on how much you and your employer contribute and the investment performance. A Defined Benefit Pension Plan (DBPP) provides a fixed monthly income based on your salary and years of service.

Is rental income considered a good retirement income source?

Yes, rental income from real estate can provide a steady cash flow during retirement, especially if the property is mortgage-free. However, it requires active management and comes with risks like vacancies and maintenance costs.

What is the best age to convert RRSP to RRIF?

You must convert your RRSP to an RRIF by December 31 of the year you turn 71. However, you can convert earlier if you need retirement income sooner.

Are non-registered investments taxed in retirement?

Yes, non-registered investment income (dividends, interest, capital gains) is taxable in retirement. Dividends and capital gains are taxed at lower rates than regular income, but it's still important to factor in the tax implications.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.