The Canada Pension Plan (CPP) is one of the most important sources of income for retired Canadians.

If you’re wondering when CPP is paid in 2024, you’ve come to the right place. I’ll also go over how to receive the maximum CPP payments you can get below.

CPP Payment Dates for 2024

Here are the upcoming pension payment dates for CPP:

- January 29, 2024

- February 27, 2024

- March 26, 2024

- April 26, 2024

- May 29, 2024

- June 26, 2024

- July 29, 2024

- August 28, 2024

- September 25, 2024

- October 29, 2024

- November 27, 2024

- December 20, 2024

Note that these days include your monthly CPP payments for the following:

- CPP retirement benefits (the most common one)

- CPP disability benefit (Find out if you qualify)

- CPP children’s benefits

- CPP survivor benefits

What Is The CPP?

The Canada Pension Plan is a social insurance program that provides financial assistance to Canadians during their retirement years. Canadian retirees can expect a steady monthly pension payment, providing they meet the requirements (see below).

CPP is what’s known as a contributory plan, which means that both employees and employers contribute to the fund through payroll deductions. Self-employed individuals are responsible for contributing both the employee and employer portions.

If you’re an employee, you should be able to view your CPP deductions on your paycheque stub.

Who’s Eligible To Receive CPP Pension Payments?

Eligibility to receive CPP pension payments is based on multiple factors, including:

- The retiree’s age

- Contributions to the plan

- Employment history

To be eligible, you must have made at least one valid contribution to the CPP during your working life. The amount you receive is directly tied to how much and for how long you’ve contributed.

Generally speaking, you must be at least 60 years old to apply for CPP.

Given that 65 is the standard retirement age, though, opting to receive a pension payment between 60 and 65 could reduce your monthly payments, preventing you from receiving the maximum CPP payment available.

In addition to the standard retirement benefit, CPP beneficiaries may also receive disability and survivor benefits.

What’s The Difference Between CPP And OAS?

The Canada Pension Plan is one of the most popular and widely received pensions in the country, and payments are issued alongside Old Age Security (OAS) via Service Canada.

However, these two pension plans are distinct from one another.

For one, the CPP is a contributory, earnings-based program. This means that your monthly CPP payment amount depends on how much you’ve contributed to the program over your lifetime.

All Canadians who’ve contributed to the program are eligible to receive at least some CPP contribution. OAS, on the other hand, is a non-contributory pension plan that’s funded by the government.

Unlike CPP, OAS is an income-tested benefit that is not tied to your previous employment history.

The amount you receive for OAS in retirement is largely dependent on your current retirement income, and if you earn more than the income threshold, these payments will be subject to OAS “clawback.” Conversely, lower-income OAS recipients may receive the additional Guaranteed Income Supplement (GIS).

Additionally, the amount of OAS you’re eligible for depends on the number of years you’ve lived in Canada.

- Read More: The Ultimate Guide To Old Age Security

What Is The Quebec Pension Plan?

The Quebec Pension Plan (QPP) is Quebec’s provincial counterpart to the CPP available in the rest of Canada.

Like the CPP, the QPP is a contributory, earnings-based social insurance program designed to provide financial assistance during retirement, disability, or the loss of a family breadwinner.

Both employees and employers in Quebec contribute to the QPP through payroll deductions, and self-employed individuals contribute both portions.

For the most part, the QPP and CPP are similar. However, there are a few key differences, including:

- QPP is managed entirely by the Quebec government

- Contribution rates and benefit amounts differ slightly from CPP

Average vs. maximum CPP received

The average CPP payout is around $760.07/month, but the CPP max amount for 2023 is $1,306.57/month if starting it at age 65.

How to calculate How Much CPP You Will Receive

How much CPP you receive will be based on two main things:

- How much was your income from age 18-65

- If you made the proper CPP contributions for those years

You can get an estimate of your CPP payments by signing into your My Service Canada Account on the Canada.ca website and requesting an estimate of your CPP benefits. You must register for the service and require a CPP personal access code from Service Canada.

Call Service Canada at 1-800-277-9914 if you’re having trouble, and they can help walk you through the process.

It’s a bit of a complicated process, but the easiest way to accurately figure out your CPP payments is if you are reasonably close to retirement. The farther away from retirement you are, the harder it will be to calculate since it’s hard to know what your income will be.

How to get the maximum CPP Payout

To receive the maximum CPP payments, you must have earned an income equal to or higher than the Yearly Maximum Pensionable Earnings (YMPE) for 39 out of the 47 years between the ages of 18-65.

The YMPE for 2023 is $66,600. Here’s a link to the YMPE list for all prior years so you can try to estimate how much CPP you will receive.

One way to estimate how much CPP payments you will receive is by comparing your income to your YMPE. If, for example, you had earned around 50% of the YMPE over 39 out of the 47 years between ages 18-65, you will receive about 50% of the max CPP payments.

Here are the two most common provisions that could boost your CPP payouts:

- Low-income years dropout – You can drop out 17% of the months of your career where you earned the least. Up to eight years of your lowest earnings can be removed from the CPP calculation.

- Child-rearing dropout – If you were the primary caretaker of a dependent child under the age of seven and your income was affected by it, you may be able to drop some of those years from the CPP calculation.

CPP contribution increase

The good news is that your CPP payouts will usually increase each year. The bad news is the amount that you contribute to your CPP will also increase. The CPP is now designed to replace one-third of your average lifetime earnings, an increase from 25% previously.

Employee and employer contribution rates for 2023 are 5.95%, and the maximum annual amount for either employee or employer is $3,499.80.

If you’re an employee, you don’t have to worry about these changes when filing for your taxes, as CPP should be deducted directly from your paycheque. If you’re self-employed, make sure you’re setting aside the extra amount every month for CPP.

Should you take your CPP at age 60, 65, or 70?

Knowing when to take your CPP payments is an important part of planning out your retirement. What age to start the CPP depends on your situation.

It’s confusing for many Canadians because of the wide age range of between 60-70 of when you can take it.

The main benefit of deferring your CPP benefits is that you’ll be eligible to receive a larger monthly payment. By applying for CPP at 65, you’ll receive a the standard payment. However, by applying early at 60, your payment will be reduced.

Related Reading: Should You Take Your CPP at 60, 65, or 70?

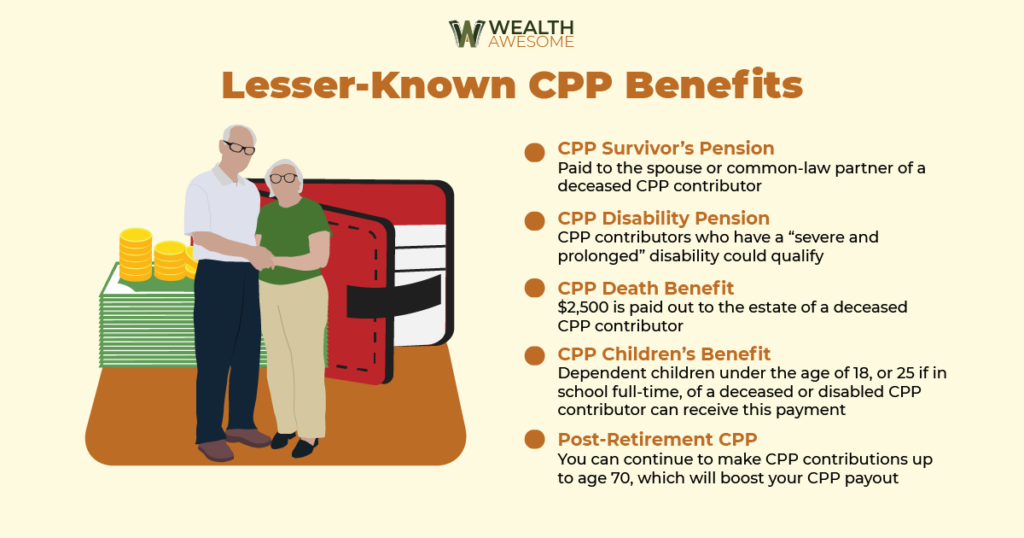

Lesser-Known CPP Benefits

Here are some under-the-radar CPP benefits that many Canadians aren’t aware of:

- CPP Survivor’s Pension – Paid to the spouse or common-law partner of a deceased CPP contributor.

- CPP Disability Pension – CPP contributors who have a “severe and prolonged” disability could qualify.

- CPP Death Benefit – $2,500 is paid out to the estate of a deceased CPP contributor.

- CPP Children’s Benefit – Dependent children under the age of 18 or 25 if in school full-time, of a deceased or disabled CPP contributor can receive this payment.

- Post-Retirement CPP – You can continue to make CPP contributions up to age 70, which will boost your CPP payout.

CPP FAQs

Is CPP Taxable?

Yes, your CPP is considered part of your taxable income after you start collecting payments.

Can Your CPP Get Clawed Back?

No, it can’t be clawed back. Unlike your Old Age Security (OAS), your CPP can’t be clawed back in retirement, even if you have a very high income after you start collecting your CPP payments.

Read about 13 simple ways to avoid the OAS clawback here.

How Can You Receive CPP Pension Disability?

If you are disabled, you might qualify for the CPP pension disability. Read my full guide here to see if you qualify for pension disability.

Can You Receive A CPP Pension Payout If You Move Away From Canada?

Yes. No matter what country you live in, you can receive your CPP pension payouts.

If you become a non-resident of Canada and a resident of another country:

– The CRA will keep a 25% withholding tax on your CPP payments, which could be waived depending on the tax treaties with Canada and the country you are living in.

– Payments can be made in the currency of the country you live in or in Canadian dollars.

CPP payment dates for 2024 are helpful to know. The CPP is a pillar of retirement income for all Canadians. Your Old Age Security (OAS) payments might get clawed back, but your CPP will get paid out no matter your income.

Knowing what age to start your CPP is crucial to planning out your retirement income in your golden years.

Still unsure about how the CPP works? Watch this video to learn more:

Pensions OAS And CPP Deposited

every Month is Payment for that month

or for the next month.

eg, Payment in January is for that month or

for the next month February?

Is it better to withdraw some of your RRSP and wait to take your CPP so you get a larger amount?

That’s a pretty common and sound strategy and one that you would have to analyze carefully though! It depends on a lot of factors like your health, how much is in your RRSP, and more.

When are we getting a raise I Pension

The government has been increasing CPP steadily almost every year

I turned 60 in April. Do I get my first CPP in April or May

Hi Heather, if you want to start receiving your CPP payments early at age 60, you have to apply for it. You can find out how here: https://www.canada.ca/en/services/benefits/publicpensions/cpp/cpp-benefit/apply.html

After you apply, you will receive written confirmation from the CRA letting you know when your CPP payments start. Also, be aware if you start at age 60, you will get significantly less than at age 65. You can read more about it here: https://wealthawesome.com/cpp-pension-take-your-cpp-at-age-60-65-or-70/