CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

The defined contribution pension plan (DCPP) in Canada is a tricky topic for many people.

A DCPP is the most common type of pension offered by employers today and can be one of your key sources of retirement income, so it's an important thing to understand.

This article will go over all the ins and outs of a DCPP and how it affects your retirement.

What is a Defined Contribution Pension Plan in Canada?

The DCPP in Canada refers to a registered pension plan you can get when you retire. The plan differs slightly based on the specific policies that your company employs, but it has the same essential principle.

The way a DCPP in Canada works is that you make contributions to the plan while you work for your company. Many companies will match their employees' contributions up to a certain amount.

If you are a part of this plan, you can allocate a portion of your salary (before taxes) to the plan. The company can match the contribution to a specific limit set.

You Make the Investment Choices

The key point is that your company does not manage the amount in your DCPP; you choose what you invest in. You can invest it in mutual funds or other plans to grow the amount.

As an employee, you have the power to choose where the contributions are invested. It can be in anything from mutual funds and money market funds, but your investments can also include specific stocks and annuities.

The funds you allocate to your DCPP will see tax-deferred growth until you withdraw the amount when you retire. There is a limit to how much you can contribute to your DCPP each year.

The amount is based on how much you earn and requires that you collapse the plan by the end of the year you turn 71. You can withdraw your funds and pay taxes on the income, transfer the assets to a Registered Retirement Income Fund (RRIF), or purchase an annuity.

How Much Money Can You Receive From a Defined Contribution Pension Plan?

With a Defined Contribution Pension Plan, there is no guarantee of a fixed amount that you can receive when you retire. The total amount you receive will depend on how well the plan is managed. Suppose you want to make the most of the pension plan so that you have a substantial amount by the time you retire.

You can work with a pension advisor or a qualified financial professional to determine how much return you will likely receive each year. If you are not satisfied with the returns, you can adjust your investments to make them more suitable for your goals.

The money in this plan is invested in one or more products on your behalf. By the time you retire or leave the company, you can have options to take out your money and put it in one of three options:

-

An annuity,

-

A Locked-In Registered Retirement Savings Plan or Locked-In Registered Retirement Income Fund, or,

-

A combination of these two.

Your company can ask you to take the money from your pension plan in cash if it is below a certain amount.

Example of a Defined Contribution Pension Plan (DCPP)

Let's consider Michael. Michael is an employee for a renowned business earning a good salary at the company. The organization employs the Defined Contribution Pension Plan for its employees, and Michael opts for it. According to the plan, he makes a contribution of $2,000 in a year. If the employer matches his $2,000 contribution by 100%, the total amount invested on Michael's behalf becomes $4,000 for that period.

If Michael does not contribute to the plan, the employer will not have to match the payment. The responsibility is more on Michael to make the contributions and control how the funds from his plan are invested. For Michael’s employer, the only thing they have to worry about is matching Michael’s contribution up to the predefined limit.

Let’s suppose that Michael leaves the company after working there a few years and goes to another organization that offers a DCPP. He can take the amount within his plan and move to the other company. Michael can continue building on that plan and retain his retirement nest egg.

Michael’s investments through his DCPP will continue to grow until he retires. Let’s assume that he amassed $450,000 by the time he turned 71. He can withdraw the amount in his plan after paying taxes on the income and then receive it in annuities, park it in a Locked-In Retirement Income Fund, or use a combination of the two methods.

Tax Considerations for Defined Contribution Pension Plans

Let's break down the tax side of things to help you make informed decisions about your DCPP.

One of the cool perks of a DCPP is that the contributions you make can often be deducted from your taxable income, giving you an immediate tax break. Plus, your investments can grow within the plan without being taxed every year.

However, the taxman will eventually want his share. When you take money out of your DCPP during retirement, it counts as taxable income for that year. This means you'll need to balance the benefits of tax deferral during your working years with the reality of paying taxes later on.

It's also important to consider the rules around contribution limits and withdrawals, as these can impact your taxes.

Defined Contribution vs. Defined Benefit

The Defined Contribution Pension Plan in Canada is one of Canada's two most popular pension plans. A Defined Benefit Pension Plan (DBPP) differs from a Defined Contribution Pension Plan in several ways:

-

The company offering DBPP guarantees a fixed amount of income for their employees after their retirement.

-

The DBPP is not a portable plan. In case an employee changes companies or is terminated from the company, they lose the DBPP. The DCPP is a portable plan that the employee can take with them when they change companies.

-

The DCPP sees employees contribute a portion of their salaries to their plan that the employer may match. Employees also have their individual accounts for the funds. In a DBPP, the employer has to ensure the growth of the funds that they will use to pay employees after they retire. The funds in this plan are managed professionally, and employees have no individual account.

-

Since the employee owns the DCPP, they can withdraw or transfer the funds from their plans as long as they are within the plan’s rules. The DBPP is owned by the company and does not entitle the employees to transfer or withdraw any amount from the plan.

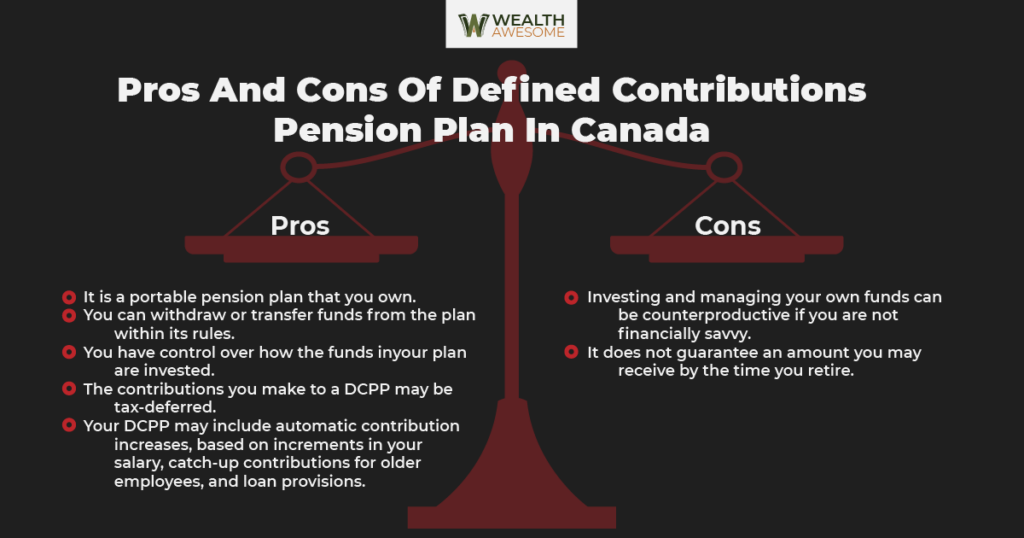

Pros and Cons of Defined Contributions Pension Plan in Canada

The Defined Contributions Pension Plan in Canada certainly has its advantages and disadvantages. I will discuss the pros and cons of using DCPP to help you understand better.

Pros

-

It is a portable pension plan that you own.

-

You can withdraw or transfer funds from the plan within its rules.

-

You have control over how the funds in your plan are invested.

-

The contributions you make to a DCPP may be tax-deferred.

-

Your DCPP may include automatic contribution increases based on increments in your salary, catch-up contributions for older employees, and loan provisions.

Cons

-

Investing and managing your own funds can be counterproductive if you are not financially savvy.

-

It does not guarantee an amount you may receive by the time you retire.

FAQs

Withdrawal Rules for a Defined Contribution Pension Plan in Canada

Generally, you can start taking money out of your DCPP when you reach the age of 71, at which point you'll have to make a decision on how to manage your plan. You can choose to withdraw funds as a lump sum, transfer them to a Registered Retirement Income Fund (RRIF), or opt for annuities.

Maximum Contribution Allowed for a Defined Contribution Pension Plan in Canada

In Canada, the maximum contribution allowed for a Defined Contribution Pension Plan (DCPP) is subject to annual limits set by the government. These limits are based on factors like your earnings and the contribution room available within the plan. Going beyond these limits can result in tax penalties.

Average Retirement Income from a Defined Contribution Pension Plan in Canada

The average retirement income from a Defined Contribution Pension Plan (DCPP) in Canada varies widely based on individual circumstances. The income you receive during retirement from your DCPP hinges on factors such as your contribution rate, investment choices, and the overall performance of your investments over the years.

Unlike a Defined Benefit Pension Plan, where a fixed amount is guaranteed, a DCPP's income is not predetermined. Many factors, including market conditions, your investment decisions, and the economy, can influence the final retirement income you receive from your DCPP.

Difference Between a DCPP and an RRSP in Canada

A key distinction between a Defined Contribution Pension Plan (DCPP) and a Registered Retirement Savings Plan (RRSP) in Canada lies in their origins and purposes. A DCPP is typically sponsored by your employer, allowing you and your employer to contribute to the plan. It's intended to provide retirement benefits and is often structured based on the company's policies.

On the other hand, an RRSP is an individual retirement savings account that you establish on your own. You contribute to an RRSP using your own funds and can invest in a range of assets.

RRSP contributions are tax-deductible, and the income earned within an RRSP is tax-deferred until withdrawal. In contrast, the contributions and withdrawals from a DCPP are subject to specific rules and regulations set by the pension plan and government guidelines.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.