CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

About to retire soon? You must learn the ins and outs of Old Age Security (also known as OAS Canada or OAS pension).

The OAS is one of the most important retirement income sources for Canadians.

I'll answer all of your questions in this complete OAS Canada guide.

Advertisement

What is OAS Canada

The Old Age Security Canada pension is one of Canada’s retirement income sources for its aging citizens.

The OAS is among the three main retirement income plans in Canada. The other two are the Canada Pension Plan (CPP) and the Employment Pensions Plan or Individual Retirement Savings.

Unlike the CPP and Employment Pensions Plan, your OAS does not depend on your employment history in any way.

You need to be a resident of Canada or a Canadian citizen aged above 65 to receive the monthly taxable income.

For the CPP, you must retire to begin receiving your pension. You can receive OAS pensions if you are still working or have not worked a day in your life.

If you earn too much income, you can get some or all of your OAS clawed back. Learn how to avoid the OAS clawback here.

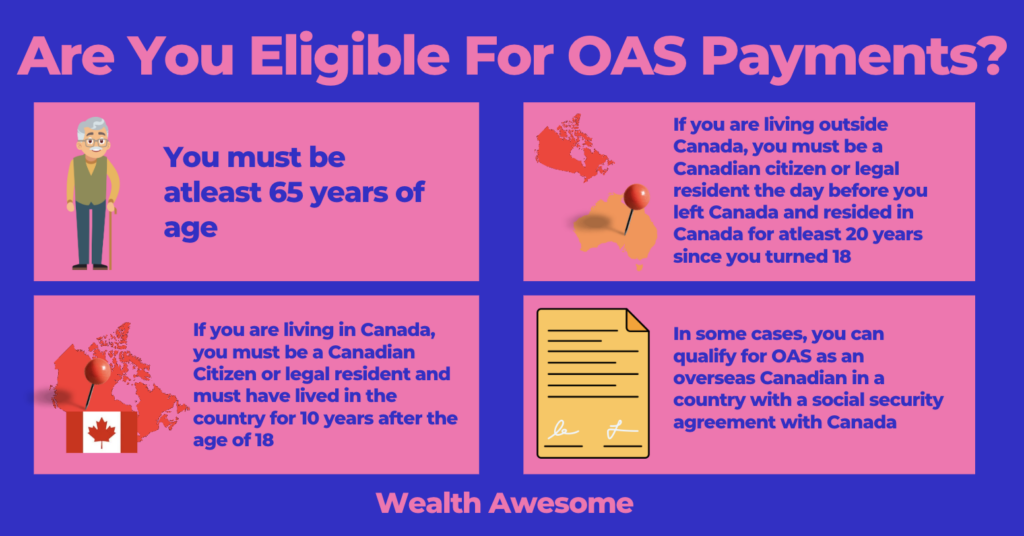

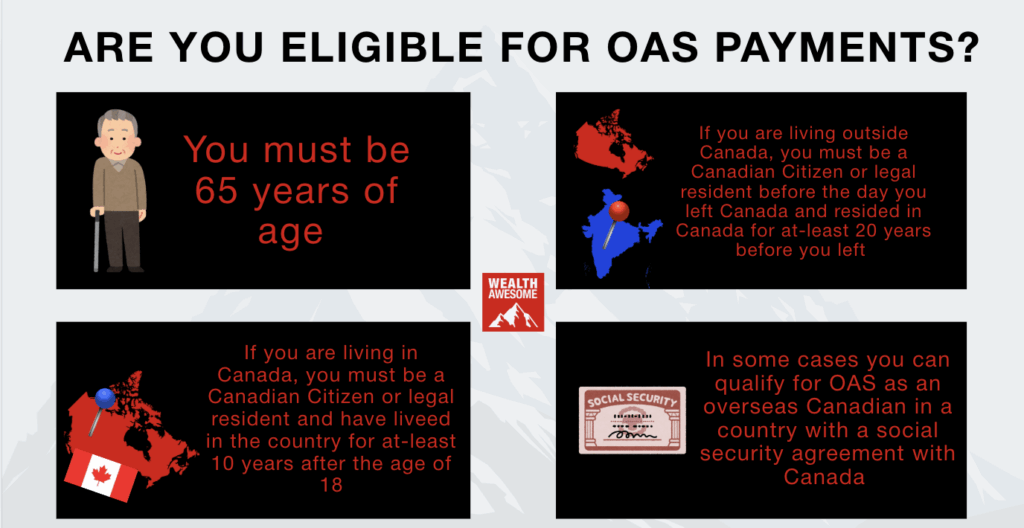

Do You Qualify for OAS?

As I mentioned above, your employment history does not matter when it comes to qualifying for the Old Age Security Canada pension. You may not have worked a day in your life or could still be working to receive the pension.

However, there are a few requirements you need to meet, so Service Canada can consider you eligible for the OAS pension. These requirements can differ if you are a Canadian still living in Canada and no longer living in Canada.

If you live in Canada:

-

You must be 65 years old or older.

-

You have to be either a legal resident or a Canadian citizen by the time Service Canada approves your OAS pension application.

-

You must have lived in Canada for at least ten years since turning 18 years old.

If you live outside Canada:

-

You must be 65 years old or older.

-

You must have been a Canadian citizen or a legal resident in the country on the day before you left Canada.

-

You must have lived in Canada for at least 20 years after turning 18 years old.

If you are a Canadian working outside Canada, but you work for a Canadian employer, you can qualify that time as a residence in Canada. For instance, people posted overseas while working for a Canadian bank or the Canadian Armed Forces can count the time they spend abroad because of their job as a resident in Canada.

To qualify the time you have spent working abroad as a residence:

-

You must have returned to Canada within six months of ending employment.

-

You must have turned 65 years old while employed by the Canadian employer overseas and maintained residence in Canada during your time outside the country.

Additionally, you need to provide two documents to qualify the time as residence in Canada:

-

Proof of employment from the employer.

-

A proof of physically returning to Canada. This does not apply if you turned 65 while you were still employed outside Canada.

Service Canada also allows considering the time that spouses, dependents, common-law partners, and Canadians working abroad for international organizations as residents in Canada meet certain conditions.

Canadians can still qualify for Old Age Security Canada if the conditions I described above do not apply to you. You can also be eligible for a pension from another country, or both. To be eligible for OAS Canada or the pension from another country, or both, you must:

-

Have lived in a country with which Canada has established a social security agreement, or

-

Have contributed to the social security system of one of the countries where Canada has established a social security agreement.

You can find out more about the conditions for overseas Canadians and pensions here.

How Much OAS Can You Receive in [currentyear]?

As of January [currentyear], the maximum monthly OAS payments are:

Ages 75+: $800.44 These amounts are subject to quarterly adjustments based on the Consumer Price Index (CPI) if you’re between 65 to 74 years old.

Ages 65–74: $727.67

Here’s a summary table:

Old Age Security (OAS) Pension Amounts – January to March 2023.

| Age Group | Maximum Monthly Payment | Eligibility: 2021 Annual Net World Income Must Be |

|---|---|---|

| 65-74 | $687.56 | Below $129,757 |

| 75+ | $756.32 | Below $129,757 |

OAS payments vary based on your residency in Canada as an adult. Service Canada adjusts the maximum monthly amounts every quarter (January, April, July, and October) according to the Consumer Price Index.

To be eligible for the full OAS pension, you must have lived in Canada for at least 40 years as an adult. Partial OAS pensions are available for those who have lived in Canada for fewer than 40 years since turning 18, calculated at 1/40th of the full amount for each full year lived in the country.

For Example: David arrived in Canada at the age of 45. He has been living in the country for 20 years. It means David has spent 20 years as an adult living in Canada.

According to the requirements, David is eligible to receive 20/40th (one half) of the full benefit for that time period.

OAS Payment Dates

The OAS payment dates for [currentyear] are as follows:

-

January 29

-

February 26

-

March 27

-

April 28

-

May 28

-

June 26

-

July 29

-

August 27

-

September 25

-

October 29

-

November 26

-

December 22 Payments are typically made on the same dates as the Canada Pension Plan (CPP) benefits.

Advertisement

Knowing when Service Canada pays out the OAS pension’s monthly payments can be essential for your financial planning during retirement. Remember that the OAS Canada pension is one of the two pension payouts you can receive from Service Canada.

Learn more about the OAS payment dates here.

OAS Supplement

The Guaranteed Income Supplement (GIS) provides additional monthly payments to low-income seniors receiving OAS. As of January [currentyear], the maximum GIS amounts are:

Spouse/common-law partner not receiving OAS: $1,086.88 Eligibility and payment amounts depend on your marital status and previous year's income. It is a program that can supplement your OAS but does not count as part of your taxable net income. You can qualify for GIS if:

Single individuals: $1,086.88

Spouse/common-law partner receiving OAS: $654.23

-

You are receiving the OAS,

-

Your income is lower than the annual OAS clawback threshold, and

-

You live in Canada.

You cannot qualify for GIS if you have been incarcerated for two or more years. The GIS amount you receive can depend on your income level and marital status. Your net income (excluding GIS and OAS) from the previous calendar year is used to determine how much you can receive.

You can check out my article on GIS Canada here to find out more about the supplementary program.

How to Apply for OAS Canada Pension

If you meet the requirements of being a Canadian resident and have lived in the country for the minimum period, you can begin receiving your OAS pension at 65 years old. If you want to begin collecting your monthly OAS payments, you can send your application a month after you turn 64.

Service Canada can sometimes enroll senior citizens for OAS pension automatically and send them a letter to notify them. If they do not enroll you automatically, you can complete the application and mail it to them.

Here is the link to the Application for the Old Age Security Pension Form. You can also apply for your OAS online using a My Service Canada Account (MSCA). You can check out the details for applying online here.

OAS Deferral Option

Since July 1, 2013, Service Canada has allowed Canadians to voluntarily defer their OAS pension for up to five years after they become eligible. Deferring your OAS can qualify you to receive a higher monthly pension later.

You can receive 0.6% more every month after you turn 65 years. The maximum you can defer your OAS is five years. It means you can receive 36% additional monthly OAS payments if you start collecting at 70 years old.

OAS Clawback

The OAS recovery tax (commonly known as the clawback) applies if your net annual income exceeds $93,454 in [currentyear]. For every dollar above this threshold, your OAS benefit is reduced by 15 cents. If your income surpasses $151,668 (ages 65–74) or $157,490 (ages 75+), your OAS benefit may be fully clawed back. You can see the clawback reduces this payment if your net income for the previous calendar year goes beyond a specified amount.

-

For 2018, the amount was $75,910,

-

For 2019, the amount was $77,580,

-

For 2020, the amount is $79,054.

-

For 2021, the amount is $81,761. (This income applies to July 2022 to June 2023 OAS pay periods)

Service Canada increases this amount each year, considering various factors. If your net income is more than the predetermined amount of net income for the previous year, you have to pay back 15% of the excess income up to a maximum of the total OAS benefit you received. Essentially, the OAS clawback is an additional 15% tax besides the current tax rate you are already liable to pay.

For Example: The income threshold for 2018 was $75,910, and David's net income was $85,000. The additional $9,090 would trigger an OAS clawback. It means that David will have to return 15% of the $9,090. David's OAS would be reduced by 15% x $9,090 = $1,363.5. The monthly reduction to David's OAS benefits would translate to $113.62 for the July 2019 to June 2020 period.

For the Jan to March 2021 quarter, a net income of more than $129,075 can reduce your monthly OAS benefit to zero.

How to Minimize OAS Clawbacks

There are a few ways you can minimize your OAS Clawbacks, including:

-

Deferring OAS: Deferring your OAS when you turn 65 increases the OAS pension you can receive, and it can increase your net income threshold.

-

Split your income: You can reduce the OAS clawback if your partner makes a significantly lower income than you do. You can split up to half of your retirement income with your partner to reduce your net income.

-

Defer your CPP: The CPP also counts as part of your net income in retirement. Deferring your CPP can reduce your net income and increase your CPP pension based on how long you defer collecting your CPP.

-

Use your TFSA: You can use your Tax-Free Savings Account (TFSA) to reduce your taxable income. Any increase in your investment in a TFSA does not count as part of your taxable net income. If you have any non-registered investments or savings and you still have some contribution room left in your TFSA, move them to the TFSA.

-

Take Your RRSP out before 65: If you take out the money you stored in your Registered Retirement Savings Plan (RRSP) before the age of 65 years, you can declare most of your RRSP income. Doing this can make you fall below the OAS clawback income threshold.

-

Use leverage to reduce net income: If you have ever borrowed money to earn investment income, you can use the loan's interest to reduce the net income. I would not advise taking on debt to do this, but you can use it if you already have borrowed money to make investment income.

You can check out my article on avoiding OAS clawbacks if you want a more detailed guide.

Conclusion

I hope my guide to explain Old Age Security Canada tells you everything you need to know. If you have questions about OAS Canada, you can get in touch with Service Canada.

-

For residents in Canada or the US, you can call their toll-free number at 1-800-277-9914.

-

For residents outside Canada and the US, the number is 1-613-957-1954.

Make sure you have your Social Insurance Number nearby when you call them.

Worried about not having enough money for retirement? Learn about all the other retirement income sources in Canada here.

❓ Frequently Asked Questions (FAQ)

Q1: What is the maximum OAS payment in [currentyear]?

As of January [currentyear], the maximum monthly OAS payments are $727.67 for individuals aged 65–74 and $800.44 for those aged 75 and over. Spring Financial+9Savvy New Canadians+9BUA 50+9

Q2: When are the OAS payments scheduled for [currentyear]?

OAS payments for [currentyear] are scheduled on the following dates: January 29, February 26, March 27, April 28, May 28, June 26, July 29, August 27, September 25, October 29, November 26, and December 22. Loans Canada

Q3: At what income level does the OAS clawback begin in [currentyear]?

The OAS clawback starts if your net annual income exceeds $93,454 in [currentyear]. BUA 50+4Art of Retirement+4The Motley Fool Canada+4

Q4: How is the OAS clawback calculated?

For every dollar your income exceeds the threshold, your OAS benefit is reduced by 15 cents. If your income is significantly higher, you may lose the entire OAS benefit. Art of Retirement

Q5: How can I apply for OAS?

You can apply for OAS online through your My Service Canada Account or by submitting a paper application. It's advisable to apply a month after turning 64 to ensure timely processing.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.