To most, the idea of retiring 15 to 20 years earlier than the average Canadian sounds like wishful thinking.

However, a select few individuals have managed to retire early, which means that you can too.

The catch is - it’s not easy.

Advertisement

Unless you’re the beneficiary of a sizable insurance payout or trust fund, retiring early will require lots of self-control, calculated budgeting, and smart investing. That being said, it is possible.

Below, I’ll share some of the best tips on how to retire early in Canada and outline how much you should save to guarantee a comfortable lifestyle when you do.

How To Retire Early In Canada: Achieve Financial Freedom

Wouldn’t it be nice to kick back at 50 and spend the rest of your days only working on things that bring you happiness? How about 40?

If you want to retire early, you’ll need to learn how to manage your time and money in a way that benefits your finances. Unfortunately, this may often mean abstaining from some of the “fun” things that you see your peers engaging in and focus on budgeting instead.

Buying expensive cars, going on fancy vacations, and dropping money at restaurants are all things you’ll need to put on hold until you achieve your early retirement goals.

Now, I’ll go through the list and explain how each of these tips can help you retire earlier and achieve your goal of financial independence at a younger age.

1. Negotiate Higher Pay Raises At Your Job

55% of workers are unwilling to ask for a raise, according to a study by People Management.

However, one of the simplest ways to increase your overall income is to negotiate a higher pay rate at your job. You can negotiate a higher weekly or hourly rate if you're paid on salary or hourly. If you’re paid on commission, then you can negotiate a higher commission rate.

While it may not sound like much, a 10-15% increase on each paycheque can have a dramatic effect on your total earnings at the end of the year.

For example, let’s say that you’re earning $60,000 annually today.

A 10% increase in your hourly wage would result in an extra $6,000, and a 15% increase would result in an extra $9,000 at the end of the year.

As long as you maintain your current budget and your monthly expenses don’t also increase with your raise (a common trap), this extra money can be invested or put into a high-interest savings account, where its value can further increase.

A key note here is that you should negotiate a raise rather than simply asking for a raise.

Approach the conversation like a business deal. Be confident and respectful, and outline the key reasons why you believe that your employer should invest more money in you. To facilitate this, asking about additional responsibilities you can take on to justify the pay raise may also be helpful.

2. Change Companies For A Higher Salary

Remaining in the same position for more than ten years can decrease your earning potential by up to 50%.

If your employer isn’t willing (or able) to offer you higher pay, then it may be time to move on.

As long as you possess in-demand skills, have a good work ethic, and come well-recommended, then you shouldn’t have a problem finding a similar position that’s willing to pay you more for what you do.

In fact, more than half of Canadian workers are planning on changing jobs in 2023, according to the latest Job Optimism survey by Robert Half.

While changing jobs can be uncomfortable, it’s often the best move financially. As much as you may enjoy your current position, there may be limits and glass ceilings preventing you from growing and earning as much as you could.

Your reputation is important, so make sure that you change companies the right way:

-

Offer a two to four-week notice to your employer

-

Offer to help train a replacement employee

-

Leave on good terms with your managers and coworkers

Don’t just walk into the office and quit one day, as this could burn a bridge and prevent you from using your former employer as a reference for future jobs.

3. Start A Passive Income Business

- How It Helps: It allows you to earn reliable income with little to no work on your end.

Many of the wealthiest people live on passive income earned from businesses that they own or helped start earlier in their life.

If you take the time to build a reliable, consistent passive income stream, then you can have others manage the business for you, allowing you to take a percentage of the profits while still retaining ownership.

Some great examples of passive income businesses include:

-

Commercial or residential rental properties

-

Income-generating properties (car wash, laundromat, gym)

-

eCommerce stores managed by a sales team

-

Trucking, logistics, and transportation (buy the trucks, hire drivers and managers)

Any business that allows you to earn money without having to actively sacrifice your time or energy fulfilling managerial duties is passive income. In other words, you could be sitting on a beach in the Caribbean while your business pays you a steady flow of profits every month.

4. Work Two Jobs

Adding a second source of income is one of the most straightforward ways to increase your income and prepare for early retirement. If you’re working less than 40 hours per week at your current job, then you could consider picking up an additional 10 to 20 hours per week.

There have even been reports of remote workers working two full-time jobs at the same time.

Working just 2 hours extra 5 days a week results in an extra 10 hours of work per week.

Over the course of a month, this effectively adds an entire additional work week. Over the course of a year, the extra 10 hours per week compounds to add an extra 3 months worth of 40-hour work weeks to your annual income.

Just think about what you could do with an extra 3 months worth of paycheques.

Your second job doesn’t have to be something complicated, either. Some great examples of side hustles could be:

-

Driving for Uber or Lyft

-

Delivering food with DoorDash or SkipTheDishes

-

Writing blog posts or helping a small business respond to emails

-

Waiting tables or bartending a couple of shifts per week

5. Adhere To A Tight Budget

- How It Helps: Controlling your spending allows you to put money into the right places.

This may go without saying, but creating a budget for yourself and sticking to it as closely as you can is the easiest way to save money. Most people are absolutely surprised to find out how much they spend on seemingly small items (coffee, fast food, lunch breaks, etc.) at the end of each month.

I’ve spoken to young college students who have approached me about how to save more. Then, I ask them a few questions, do the math, and show them that they’re spending $300 per month on coffee and breakfast from a cafe when they could cook their own breakfast and save money.

If you’re having trouble creating a budget, I recommend using one of these personal finance and budgeting tools.

6. Utilize Tax Deductions & Credits

- How It Helps: Paying less taxes allows you to save more

If you’re earning a significant amount of money then chances are that you’re paying more in taxes than you need to. A good accountant can work with you to help you apply for all of the tax deductions and credits that you’re legally eligible for.

This can help you pay less taxes, allowing you to save and invest more money into your own retirement.

See my full guide on how to pay less taxes in Canada for more info.

7. Invest In The Market

Advertisement

- How It Helps: Investing can result in a rate of return that can help accelerate your retirement time.

While it’s often unpredictable, investing in the stock market can potentially give you a fast track to retirement. A common way to achieve this is by investing in stocks or ETFs.

If you’re not a fan of investing yourself, you can use a robo-advisor service like Wealthsimple Invest.

All you need to do is deposit money into your account, set your risk/reward tolerance (from mild to extreme) and allow the platform to invest for you at a small fee.

8. Save Your Money In High-Interest Savings Accounts

- How It Helps: Your savings will grow quicker than they will in a traditional account.

High-interest savings accounts are special savings accounts that offer a far higher interest rate on your savings than a traditional big bank. For example, a major bank may only offer you 0.10% APR on your savings, while a small online bank like EQ Bank may offer you [sc name="eqbanksavingsrate"][/sc] APR paid on a monthly basis.

Some banks also allow you to use your TFSA savings to invest in ETFs and stocks.

9. Buy GICs

- How It Helps: Lend banks money in exchange for interest.

Guaranteed Investment Contracts (GICs) are agreements entered into between you and a financial institution. GIC terms typically range between two and ten years.

For example, a one-year GIC [is at a [sc name="eqbank-1-year-gic"][/sc] interest rate at EQ Bank currently.](http://[sc name="eqbank-1-year-gic"][/sc])

The upside to this approach is that you can usually get much higher interest rates than in a generic high-interest savings account.

This method often involves having your money held up for a certain amount of time, but it is an excellent choice for a no-risk investment for your shorter time horizon needs.

10. Avoid High-Interest Debt

- How It Helps: High-interest debt is money needlessly spent; it’s better saved and invested.

It may be tempting to grab that new sports car with your current salary. However, the 8% APR that comes along with the monthly payment may not be worth it. In some cases, high-interest credit card or installment loan debt can result in you being “upside-down” on your debt.

This occurs when the amount you owe for the loan exceeds the value of the item you’re financing.

For example, if you finance a new car at a high-interest rate only and only make your minimum monthly payments, then you could pay back 40% more than you paid for the car once interest compounds over the loan term.

Financing isn’t always bad. However, you should work on building your credit score and make a higher down payment to reduce your interest rates.

Trust me, the money that you’d otherwise waste on high-interest rates would be better invested into an RRSP, TFSA, or robo-advisor investment account.

11. Maximize TFSA Contributions

- How It Helps: Allows your savings to grow tax-free through investments

The TFSA Act was passed in 2009, allowing all Canadians to open up a tax-free savings account (TFSA) to help them save more money. Unlike an RRSP, a TFSA is not tax-deferred. However, you don’t have to pay any taxes on the income that you earn within a TFSA account.

Granted, there is a limit to how much you can contribute to a TFSA. The amount steadily increases each year. You can use RBC bank’s TFSA calculator here to see the maximum amount you could contribute.

12. Maximize RRSP Contributions

- How It Helps: Tax-deferred retirement savings/investment account allows your investment to grow faster.

A Registered Retirement Savings Plan allows you to divert a portion of your income before paying taxes into an investment account or high-interest savings account. This means that your contribution will be higher than it would otherwise be on a traditional investment account. Ideally, this would allow your portfolio to grow quicker.

Many businesses offer to match a percentage of your RRSP contributions (up to a certain amount). Find out the maximum that your employer is willing to match, and invest at least that much. After all, it’s free money, so you should take it.

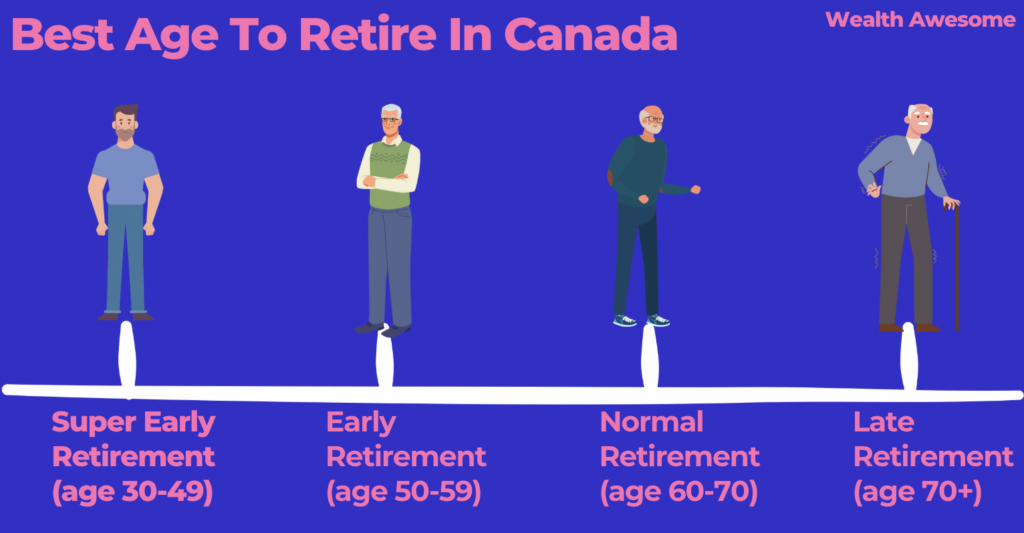

What Is The Average Retirement Age In Canada?

According to the latest data from Statistics Canada, the average retirement age in the country is 64.4.

For simplicity’s sake, let’s just call it 65.

Realistically, many individuals begin to slowly ramp down their work and responsibilities as they approach 65, ensuring that they’re fully retired and free from work obligations by the time they stop contributing to the Canada Pension Plan (CPP).

CPP contribution is mandatory for all working-age Canadians between the ages of 18 and 65. You’re allowed to continue contributing until age 70, but you are not allowed to stop contributions until 65.

If you happen to retire early, then you’ll still need to contribute to the CPP until 65, albeit at a slightly reduced rate. After 65, you can start receiving standard CPP payments based on the amount you contributed during your lifetime.

How Much Money You Need To Retire Early In Canada

All of the tips mentioned above are centred around one goal - ensuring that you have enough money to sustain your lifestyle for the rest of your life, after you stop working.

That’s what true financial freedom is.

Of course, we all have different lifestyles, different expenses, and different ways that we want to live in retirement. Some want to retire in a quiet mountain cabin, while others want to spend their retirement travelling. It’s all subjective.

The Financial Independent, Retire Early (FIRE) formula, sometimes referred to as the 4% rule, states that once your investments reach a certain value, you should be able to live off of your investment’s profits alone without ever running out of money.

Here’s how it works:

-

Calculate how much money you need per year to live the life you want to live

-

Multiply that number by 25

-

The resulting number, if invested with a steady return rate, should ensure that you don’t run out of money, providing you take out 4% of the amount every year.

For example, let’s say that you need $70,000 per year to sustain your current lifestyle:

-

$70,000 x 25 = $1,750,000

-

4% of 1.75 million = $70,000

Given the 4% rule, you should be able to continue taking out $70,000 per year indefinitely, regardless of your age.

Of course, this method is far from foolproof.

In theory, it’s a great idea. However, the 4% rule is based on the assumption that the stock market continues to follow similar historical growth. It doesn’t account for economic downturns or huge market collapses, or other "black swan" events.

So, while this is a good rule of thumb to follow, you should still have some traditional savings stashed away. BMO Harris has a detailed retirement planning calculator that can help you determine the exact amount you need to save to retire.

In addition to your income, the calculator also factors in your pension, retirement accounts, and other savings you may have.

How Much Savings Do You Need To Retire By 60?

Retiring early at 60 may not seem like a major difference, but that’s an extra five years that you get to spend with your family and spending your time on the things that matter most in life.

Another common financial recommendation is that your savings should be able to pay you at least 70-80% of your pre-retirement income for the rest of your life.

For example, if you’re currently earning $100,000 per year and plan on retiring at 60, try to have enough savings or income from sources such as your pensions to pay yourself $70,000 - $80,000 per year for the rest of your life.

Conclusion - Is It Possible To Retire Early?

Early retirement is possible if you commit yourself to a plan and refuse to deviate from it. Even if life gets in the way and prevents you from achieving your goal as soon as you hoped, following the steps I outlined above are guaranteed to put you in a better financial position.

As a wise man once said, the best time to start is now.

So what are you waiting for?

Keep on reading to see my ultimate guide to retirement planning!

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.