CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

If you are planning for your retirement and are wondering how to fit Old Age Security in the grand scheme of things, you are probably wondering: Is OAS taxable income?

OAS (Old Age Security) is considered a taxable income source in retirement and is part of your income for the year when you file your taxes at year-end. Taxes are not automatically deducted, so be sure to set aside cash for taxes.

If your income falls under a certain level, you will become eligible for the Guaranteed Income Supplement (GIS) in addition to the OAS. GIS is not taxed as income but is only available to low-income seniors.

Below, I will go over whether OAS is taxable and cover some additional key points to consider for your retirement.

What is Old Age Security (OAS)?

Old Age Security (OAS) is a pension program in Canada that is funded by the government. Canadians do not explicitly contribute to OAS.

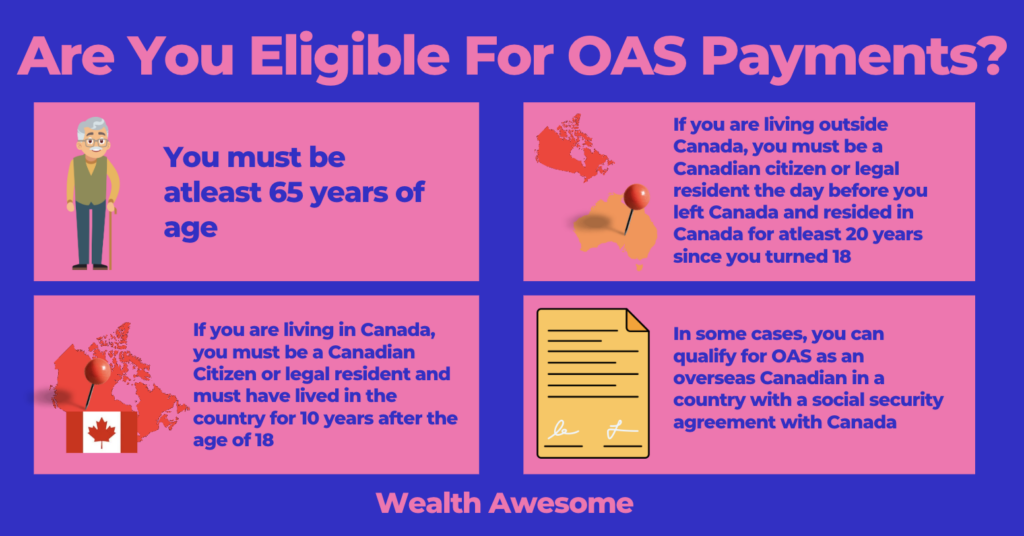

Canadians that are 65 or older qualify to potentially receive OAS payments. Another qualifying factor is that an individual must have lived in Canada for at least 10 years beyond the age of 18. The amount of your OAS payment will depend on how long you have lived in Canada after the age of majority.

A senior is eligible for full OAS payments once they have lived at least 40 years in Canada beyond the age of 18. Individuals that have spent less than 40 years in Canada will receive a fraction of the maximum payment.

Example: You have spent 20 years in Canada beyond the age of 18. The formula includes dividing the number of years beyond 18 (10-year minimum) by 40 (the maximum payment requirement. In this case, you will receive 20/40 of the maximum OAS payment or 50%.

OAS payments can be deferred for up to five years once you reach the age of 65 if you would like to receive higher payments once they are eventually started.

The payments received through OAS are usually not enough to support you entirely through retirement. OAS payments should be considered along with CPP payments, GIS (Guaranteed Income Supplement – only in some cases), and private assets.

What is the Guaranteed Income Supplement (GIS)?

If you receive OAS payments, you may also qualify for GIS payments if your income in a particular year is very low. If you choose to defer your OAS payments at the age of 65, you will be unable to qualify for GIS.

The GIS is income offered by the Government of Canada for seniors receiving OAS that fall under a certain income threshold. The amount of GIS payment that you can receive depends on whether you are married as well as how much income you are making.

As an example, in 2023, the maximum GIS monthly payment that you can receive if you are single, widowed, or a divorced pensioner is $1,026.96. Your annual income to qualify for GIS must be less than $20,832.

GIS payments are not taxed at year-end.

You can learn more about the Guaranteed Income Supplement by reading my GIS Canada guide.

How is Income Taxed in Canada?

When it comes to taxes in Canada, both the federal government as well as each individual provincial government charge taxes on income. Taxation is done progressively, meaning that higher levels of income are faced with a higher tax liability.

Your total income in a certain year is determined by adding up various different income sources. These can include:

-

OAS payments

-

CPP payments

-

Employment income

-

Rental income

-

Income from investments (fixed income in particular)

The CRA (Canada Revenue Agency) determines your taxable income by removing deductions and credits from an individual’s total gross income. Your income tax return has to be filed each year by April 30th. This is extended to June 15th for self-employed individuals.

Federal Income Tax Brackets

Despite your province or territory of residence, Canadians are required to pay income taxes at the federal level at a specified rate. Regardless of what province you live in, you will be responsible for paying federal income tax. The federal income tax brackets break down into:

| 2023 Federal income tax brackets | 2023 Federal income tax rates |

|---|---|

| $53,359 or less | 15% |

| $53,359 to $106,717 | 20.5% |

| $106,717 to $165,430 | 26% |

| $165,430 to $235,675 | 29.32% |

| Income over $235,675 | 33% |

The total amount of tax that you will be paying is the sum of the above federal tax rate as well as the provincial tax rate based on your province.

Here is an updated list of the provincial tax rates.

How is OAS Taxed in Canada?

Payments made through the OAS program are considered income and are added to an individual’s total income for the year. GIS payments, if you qualify for them, will not be considered part of your yearly income.

Your OAS payments are taxed at your personal marginal tax rate, along with other income for the year.

Your OAS payments will not have tax automatically deducted, so be sure that you have set aside enough money each year for taxes.

Typical Elements of a Retirement Income Stream

While it is unlikely that you will be able to live off of Old Age Security payments (and maybe even the combination of OAS and CPP), you will need to have a good retirement plan in place.

A strong and diversified retirement income stream usually consists of several elements:

-

OAS payments

-

CPP payments

-

An income-oriented investment portfolio

-

Other sources of income

-

Drawing down from a lump sum of money

Frequently Asked Questions

Does OAS Start at 65 or 67?

OAS payments can be started as early as 65. If you would like to receive higher payments, you can defer starting OAS (and GIS if eligible) by waiting up to five years to start payments.

You can choose to start Old Age Security payments at the age of 67, at which point they will be higher than if you had started them at age 65.

OAS Clawback?

If you are earning a very high level of income in retirement, usually from private sources of income (with the addition of CPP payments in most cases), you may experience what is called an OAS clawback.

An OAS clawback is the requirement to pay back a portion of your OAS amount if you are making above the OAS clawback starting threshold. For 2023, the OAS clawback starting threshold is $86,912. For every dollar of income earned beyond $86,912, you will have to pay 15% back to the government as an OAS clawback.

Keep in mind that if you exceed the maximum clawback threshold, which for 2023 is $141,917, you will not be eligible for any OAS payments.

An important aspect of retirement planning is keeping an eye on your income levels throughout the year to make sure that you are able to take advantage of as much in OAS payments as possible.

Conclusion

OAS payments from the government are considered a regular income stream by the government, and you will be responsible for paying taxes on them at year-end.

Choosing to defer OAS payments for up to five years can significantly increase the amount of OAS that you are receiving.

Keep in mind that this will also defer GIS payments, which cannot be received without OAS payments. You will want to consider your personal financial situation to see if it makes sense to defer OAS payments.

Be sure to have a combination of income streams ready for retirement in order to be able to afford the lifestyle that you will want to maintain once your working years are behind you.

For a thorough outline of the different streams of income that you may be able to access in retirement, make sure that you check out my guide to retirement income sources in Canada.

Best next step

Keep exploring this topic

If you want to go deeper, these are the most useful follow-up pages and tools for this topic.

Tax tool

Run the income tax calculator

Estimate take-home pay and tax impact before choosing software or planning contributions.

Registered account

Check your TFSA contribution room

Use excess cash more efficiently after filing by checking your tax-free savings capacity.

Cash management

Compare today’s savings rates

Find a better home for refunds, emergency savings, or short-term cash after tax season.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.