Note that Lending Loop has pivoted to a new business model, and they no longer provide peer-to-peer lending anymore. They are known simply as Loop now, and the company provides other services to small businesses such as payments and multi-currency accounts. You can read the full getloop.ca review here.

In Canada, where the banking institutions are strong, stable, and trusted, peer-to-peer lending hasn’t gained much traction yet.

The situation might change with platforms like Lending Loop gaining popularity. It was a first-of-its-kind, peer-to-peer lending platform in the country, which furnishes loans to small businesses.

Many small businesses have trouble securing a decent loan on favourable terms from traditional lending institutions, and Lending Loop is well-positioned to help them.

It also offers Canadian investors an amazing investment opportunity. Read this Lending Loop review to find out more.

Peer-to-Peer Lender

Lending Loop is a peer-to-peer lender in Canada that provides loans in every province.

Pros

- Furnish loans to small businesses that can’t secure capital from big banks.

- Loans are available for up to $500,000 (higher than alternative options).

- It’s regulated and available in all provinces and territories.

- An easy-to-reach minimum payout value

- It’s transparent with investors and lenders.

Cons

- The minimum loan qualification criteria are tough.

- Long-term loans can be very costly.

- It only furnishes loans to businesses, not individuals.

- Investors carry the risk of investment.

What is Lending Loop?

Lending Loop is a peer-to-peer lender for small businesses. It’s unique, not because it offers loans to small businesses, but because it uses the peer-to-peer lending model. There is only one other regulated lender of its kind currently operating in the country, goPeer, but it only makes personal loans.

Lending Loop Canada is Toronto based, but it offers lending services and investment opportunities to Canadians in all corners of the country. What sets it apart is that it provides loans to businesses that do not qualify for traditional business loans from banks, simply because they might have an unorthodox business model or unique (but legal) business practices.

Basically, a small business that might have trouble getting a loan from a traditional lender, or might find a conventional loan too expensive, or terms too constraining may find Lending Loop an amazing option.

But lending Loop doesn’t just cater to borrowers, and neither does it issue a loan itself. It finds investors that are willing to try this high-return investment option, creates investment products for them, and issue loans with the capital they invest.

How Peer-to-Peer Lending Works

Before we get into the specifics about Lending Loop, let’s develop an understanding of peer-to-peer lending.

Peer-to-peer lending, P2P lending, or as some people like to call it, person-to-person lending is when individual (or in some cases, institutional) lenders offer loans to borrowers, using a peer-to-peer or crowd-funding platform.

The platform acts as the “loan originator” and takes a minimal cut from both entities. From the borrower, it charges a loan origination fee (or something along similar lines). From investors/lenders, it takes a cut of the interest that the borrowers pay when they make their loan payments.

Different Peer-to-Peer Models

Traditionally peer-to-peer lending systems and platforms worked a bit differently. What used to happen was that peer-to-peer platforms made loan requests available for lenders/investors (while keeping the borrower’s personal details secure).

The loan requests had borrower profiles that included things like the reason behind asking for a loan, borrower’s credit score, and personal or business income. Lenders could choose which loans to make with their capital. Some investors chose to offer loans to low-risk borrowers with excellent credit, but for lower returns (interest on loans).

While others went for higher returns and lent to borrowers with relatively poor credit for high-interest rates, this model had its own pros and cons, but it has been replaced with a better system.

Now peer-to-peer lending works differently and is more akin to crowd-funding. The peer-to-peer platforms don’t directly connect a borrower to a lender, or a certain number of borrowers to a certain number of lenders. They mix things up.

They either pool the investors’ money or make loans to borrowers according to a predefined mix. This offers good returns to investors while mitigating the risks of default.

In the “one-borrower to one-lender” scenario, the risk of default is carried mostly by the lender. But in the peer-to-peer lending model where no one lender/investor is taking all the risk, the risk is minimal. This isn’t purely crowd-funding. In crowd-funding, lenders/investors are provided equity by the platform.

Peer-to-Peer Lending for Borrowers

For many borrowers, peer-to-peer loans might not look very different from bank loans. Since these platforms also have their requirements for loan consideration, like a traditional bank.

You may need a good credit score, a certain level of personal or business income, or something else, to qualify for a loan from a peer-to-peer lender.

But there is a crucial difference. Traditional banks have several ways of making money. They have set criteria for issuing loans, whether personal or business. If your loan requirement doesn’t pass those criteria, they will simply reject your loan request. They won’t make any special considerations or modify their rules, simply to pass a loan.

For a peer-to-peer lender, loans work as demand, and investments work as supply. Both things need to be in conjunction with the business model to work, which is why, a peer-to-peer lender might be more considerate, and ever more flexible about processing your loan, given that you fulfill their minimal financial criteria. And if you are a creditworthy borrower, you may even find better interest rates with a peer-to-peer lender.

Peer-to-Peer Lending for Investors/Lenders

For lenders, peer-to-peer lending is an amazing option. You have control over the risk of investments and returns, and the risk and reward ratio is significantly better than many other investment options. You can diversify your investment portfolio.

If you care about giving back to the community, peer-to-peer lending is an excellent way to help your fellow citizens.

But perhaps the best benefit of peer-to-peer lending is the time of returns. Most such platforms allow loans for a maximum of five years.

But borrowers rarely choose to extend the loan for such a long period, because the interest can really pile up. Most borrowers try to repay their loans within a year or two. So in most cases, you will have your capital and the accompanying interest back in a couple of years.

Very few investments, especially ones that carry so little risk and require relatively low starting capital, can offer high returns in a similar time frame.

P2P Lending Risks For Investors/Lender

Like any other investment, it has its own risks. But the current peer-to-peer lending model has mitigated the primary risk of borrower defaults. And you can lessen it even more by choosing a peer-to-peer lending platform with low default rates and stringent loan criteria. If the platform itself is strict about screening the loan requests and borrowers, the risk of default gets significantly lower.

Realistically speaking, the risk is there, but it can vary and you have a choice over how much risk you want in your loans. And the risk is mostly tied to the credibility and performance of the platform itself.

How Lending Loop Works and Products Offered

As a peer-to-peer lender, Lending Loop connects borrowers with lenders through their platform. The process starts with borrowers applying for a loan. If the application passes, it’s assigned a “loan grade” by the credit team of Lending Loop.

It isn’t shared how exactly they grade the loans, but they are assigned grades ranging from A+ and A to E+, and E. Simple logic tells us that the loans are graded based on their credit-worthiness and risk of delinquencies.

With the best grades carrying the low risk and relatively low returns and lower grades carrying higher risks and relatively higher returns.

The loans are then placed on the platform’s marketplace in the form of notes (fractions of the loan), to be “funded.” Investors/lenders don’t directly fund the loans themselves. They buy securities (in the form of notes), which include fractions of these loans.

Lenders can manage their risks and returns and diversify their portfolio by choosing corresponding notes from different borrowers. As the borrowers pay back the money they borrowed, the lenders are paid according to the corresponding notes of the loans they have.

That’s the snapshot of how Lending Loop’s platform works. Let’s see how it works for the borrowers and the lenders individually.

For Borrowers

Borrowers need to fulfill minimum borrowing criteria before they can qualify for the loan.

The business needs to be registered in Canada and may have any of the three business structures: Sole proprietorship, partnership, or corporation. These terms reflect the credit-worthiness of the borrower. They also put lenders/investors at ease, as they’ll know that even the least graded borrowers are legit and functional businesses with a dependable revenue history. And they are less likely to default.

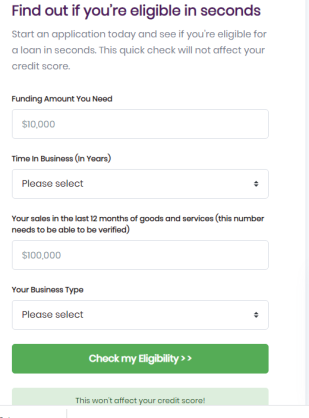

Borrowers can check their eligibility. If they are eligible, they can fill out a quick application, with details about the business and its performance. After it’s done, the application is reviewed by the credit team, assigned the relevant grade, and allotted a spot on the platform’s market place.

Some documents that borrowers may need to present are:

- Detailed business plan and reason for requesting the loan.

- Fiscal-year end statements. (Usually for two years, but they may ask for records going back further, based on how long you have claimed to be in business)

- Notice of assessment by CRA

- Balance sheets

- Last year’s income statements

- If incorporated, articles of incorporation.

Once there, it’s funded by the investors. The application sits there until it’s completely funded i.e., all of its fractions are taken up by investors and are part of their portfolios. This process may take up to several weeks, depending upon the grade that has been assigned to the loan and general investor interest.

The interest rates that a borrower can qualify for, fall somewhere between 5.9% and 26.5% every year. The loan origination fee is deducted automatically before the funds are released. The loan duration can vary from three months and five years.

When the lenders fully fund the loan, the loan amount is transferred to the borrower’s bank account. The portal has furnished loans of about $72,444,350 since 2015, to hundreds of small business owners. Lending Loop also claims to make the process easier for both lenders and borrowers, and that a dedicated account manager is assigned to every loan application.

For Lenders

Lending Loop has tried to make the process as easy for investors/lenders as possible. Individuals and investors can both become lenders with Lending Loop.

Lending Loop claims that 11,164 lenders have invested with the portal to date. One possible reason behind this can be Lending Loop’s flexibility for investors. Many exempt market securities (like debt) are offered only to sophisticated and accredited investors. As relatively fewer people fit that bill, the investor pool for such securities remains relatively small.

Lending Loop allows practically anyone to invest with them. But they classify their investors/lenders into three categories.

- Accredited Investors (Top Tier): Individuals or corporations with considerable net assets, one million and five million respectively, and a net income of more than $200,000 a year ($300,000 with the spouse) usually qualify as accredited investors. There are some other criteria as well. Accredited investors virtually have no investment limits. Corporate investors also don’t have a maximum limit.

- Eligible Investors: Individuals with net assets (alone or with a spouse) of $400,000, net income of $75,000 alone, or $125,000 with the spouse for the previous two years are considered eligible investors. They have a cap of $100,000 a year in loans/investments.

- Non-eligible Investors: They don’t need to meet any criteria, and can invest up to $10,000 a year with the platform.

Investors can start with as low as $200. This is the minimum amount to fund the account. After that, lenders can add or withdraw any amount exceeding $50. Though, the minimum loan commitment a lender can make (buy a note of a loan’s fraction) is $25. Since notes are available in the increments of $25. That’s the minimum amount of a loan you can buy.

One thing that lenders need to understand that they can’t sell a note, which is the fraction of a loan until the term of the loan is up. The portal doesn’t have that feature, and there is no other similar market to trade that note in. Once you buy a note, your investment is tied up to the term of the loan.

Lender Fees

Lenders typically only need to pay a servicing fee, at an annualized rate of 1.5% of the outstanding principal. A lender’s stake in the principle is calculated based on the notes they have of a particular loan. In case a borrower defaults and Lending Loop “collects” the outstanding debt from the borrowers, the collection fee may go up to 35% of the recovered amount.

There are a few products offered by Lending Loop, mostly focused on lenders. The prominent ones are:

The Marketplace

The marketplace is where all the “lender magic” happens. It’s the place where lenders find the loans (notes) that are available, already graded. The investors can choose which loans to buy in, and how much to buy in, staying within their limits. You can find the details of the loan and relevant details of the borrowers by clicking on any particular loan.

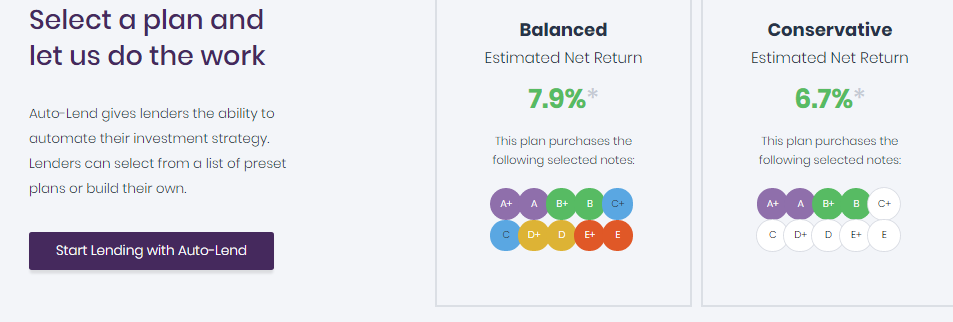

Auto-Lend Tool

The Auto-Lend tool is available on the lender dashboard. This is ideal if you don’t want to take out any cash from the portal, and just let it grow.

You can either select a premade plan to invest your capital or create one for yourself according to your risk tolerance and return expectations.

You can either select a premade plan to invest your capital or create one for yourself according to your risk tolerance and return expectations.

As you can see that a balanced plan, which is an equally weighted mix of all loan grades, offers higher returns compared to a conservative plan, which has less risk (high-grade loans) and, consequently, fewer returns.

Ideally, you can make a custom plan for yourself and choose the option to reinvest. It will put your Lending Loop investments on autopilot, and the Auto-Lend tool chooses the notes to buy, using the monthly returns you get when the borrowers repay their loans.

Tools for Borrowers

Three tools Lending Loop offers for borrowers are:

Credit check: A free credit check with Equifax that won’t impact your score.

Business loan calculator: You can check your repayment details by putting in your loan amount, term, and the interest rates you qualified for.

Loan comparison calculator: You can compare the loan offered by Lending Loop to other online lenders, side by side. It allows borrowers to make sure that they are getting the best possible terms and rates.

Statistics

Transparency is one of the key selling points of Lending Loop. In their statistics sections, they provide several graphs that can offer insights to both borrowers and lenders.

They are very clear about their default rates and projections as well.

Lending Loop Cost and Fees

The lending loop charges a fixed lender servicing fee. An additional collection fee can be charged against the outstanding amount (35% at max), in case of a default and in lieu of efforts expanded to recover the debt.

For borrowers, the one fee charged by Lending Loop is the loan origination fee, which is 2.99% to 9.99% of the principal amount. This fee is deducted before the loans are released. In case borrowers are late with their monthly payments, they might need to pay a late fee.

How to Sign up For Lending Loop

For Borrowers

The process of borrowers starts with finding out their eligibility.

1. Check eligibility.

2. If you are eligible, you have to fill in some basic information details.

3. Fill out details about the payments your business can make every month and the purpose of your loan. You may need to reduce your loan amount.

4. After that, you have to fill business details, financial details, personal details, and a few other details.

5. Once your application is reviewed and placed in the market place, you will be informed.

For Lenders

1. Choose if you want to open a personal account or a corporate account.

2. Then you have to sign-up, fill, and fund your account.

3. Once it’s verified, and you have been allotted the adequate investor status, you can either start investing by visiting the marketplace or use the Auto-Loan feature.

Is Lending Loop Legit and Safe to Use?

Lending Loop is a registered, exempt market dealer in all provinces and territories. It worked with Ontario Securities Commission in marking out the guidelines for the peer-to-peer lending model. The OSC allowed Lending Loop to operate as a peer-to-peer business. The website comes under Loop Securities Inc., which is registered with the securities regulatory authorities of all the provinces.

The website is not accredited by BBB and has one review on Trustpilot. But, none of the over 70 Google reviews, or lending loop reviews found on other places reflect any frauds.

Yes, Lending Loop is legit and safe to use. Though the risk associated with investing in the peer-to-peer model should be taken into account.

Lending Loop Alternatives and Competitors

No other peer-to-peer lending platform offers loans to small businesses in the country.

You Should Use Lending Loop If:

- You are a small business that can’t get approved for a better loan.

- You are an investor looking for alternate investments.

- Want to have thorough control over the risk and returns of your investments.

- You have weighed the tax implications of investing with Lending Loop against other investments.

Don’t Use Lending Loop if:

- You can get a conventional business loan at lower rates.

- You don’t want to invest in illiquid securities.

- You think you can find better returns with less risk.

- You think their underwriting and grading process is flawed.

Conclusion

Peer-to-peer lending is an outstanding service for both lenders and investors. Since Lending-Loop is one of its kind, it’s hard to compare.

It’s a great portal for borrowers if their loans are furnished fast and easy and on generous terms. For investors, if the defaults stay low, grading is accurate, and they know how to balance their portfolios properly, it can be a powerful investment option.