CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

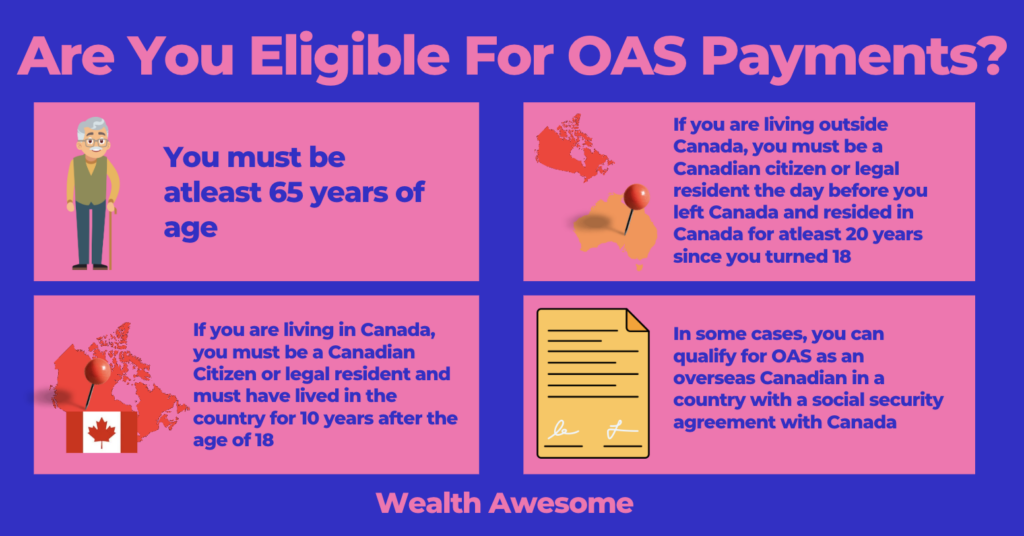

If you soon qualify for Old Age Security payments from the government, you may be wondering if it is worth it to defer OAS to a later date to receive higher payments.

The choice to defer OAS payments until 70 will mainly depend on both your personal financial circumstances as well as your health.

If you do not necessarily need OAS payments during retirement and you are healthy with a family history of longevity, it may make sense to defer OAS to 70.

Advertisement

If you have severe health issues and need OAS payment support in the short term, it would not make sense to defer payments.

I will cover OAS deferral to 70 below and explain when it would likely make sense to push back your payments.

The Math behind Deferring Payments

The math behind deferring OAS (or CPP) payments to a later age for a higher payment all depends on mortality tables. Mortality tables outline the probability of death for individuals at various ages and are often used for “income-for-life” products or payment streams.

While pushing back OAS payments may seem attractive because you will eventually receive larger payments, you will also be older and have less time to take advantage of the income.

The government is also aware of this when they calculate how much more you can get in OAS payments at a more advanced age.

By using mortality tables, the government is actually indifferent between offering a lower payment at 65 or a higher one at 70. They expect to pay the same amount of money in both cases based on statistical life expectancies.

Should you Defer OAS to 70?

Deferring your OAS payments to 70 should depend on two main factors:

-

How urgently do you need additional income in retirement

-

Your overall health condition and how long you expect to live relative to the average lifespan

Although these are the two most important factors, several other things must also be considered when making the decision to defer OAS payments to a later time. I will cover these two key considerations below, as well as several other things to keep in mind.

The Need for Additional Income

If you need additional income in retirement at age 65, this would be a situation in which you will want to start payments early. There is no need to defer OAS payments until a later date (especially until the age of 70) if you need the income stream today.

If you don’t need income urgently at the age of 65, you can start to consider whether it would make sense to defer OAS payments until age 70 to get a higher payment stream.

Deferring OAS and the Impact on GIS

The Guaranteed Income Supplement (GIS) is a supplement to the OAS that is reserved for seniors that fall into an extremely low-income bracket. The annual income to qualify for the GIS for single, widowed, or divorced pensioners are less than $20,832 in annual income.

GIS payments can be quite substantial (in most cases, higher than OAS payments) and are also not considered as income for income tax purposes at year-end.

If you fall in a low-income bracket, you will want to avoid deferring OAS payments because you will not be able to receive GIS payments. At the same time, if you are in a low-income bracket, you will likely need OAS support sooner rather than later, making it unlikely you would want to defer payments.

Your Overall Health Condition and Life Expectancy

Your family’s health history, as well as your individual health history, are both very important factors behind the decision to defer OAS payments or not.

It all comes down to thinking about the average life expectancy of an individual of your gender and age and whether you expect to live more or less than this amount.

It can be extremely difficult to estimate your life expectancy based on the general average. Family genetics and your overall lifestyle and health, especially compared to the average for an individual like you, can help with making your estimate.

Factors that can affect your life expectancy include:

-

Severe illnesses

-

Family history of health complications

-

Smoking

-

Alcohol consumption

-

Physical activity

-

Diet

-

Sleep

-

Stress

If you estimate a below-average life expectancy for yourself, you will want to start OAS as early as possible (at age 65). If you are expecting an above-average life expectancy and you don’t require income until the age of 70, you will want to consider deferring OAS to age 70.

If you think that your life expectancy is roughly in line with the average, you will be receiving roughly the same amount of money whether you defer payments or not.

How do Regular vs Deferred Payments Compare?

Advertisement

OAS payments increase by 0.6% each month, and they are deferred after the age of 65. If you choose to start your OAS payments at age 70, this represents an increase of 0.6% x 60 months (five years) = 36%.

Each year of deferral increases OAS by 7.2%.

As of early 2023 (January to March), the maximum OAS amount that can be obtained at age 65 is $687.56 per month ($8,250.72 per year). Accounting for the 7.2% increases each year, here is how much yearly income you would earn by deferring payments:

| Age OAS started | Monthly OAS maximum | Annual OAS maximum |

|---|---|---|

| 65 | $687.56 per month | $8,250.72 per year |

| 66 | $737.06 per month | $8,884.77 per year |

| 67 | $786.56 per month | $9,438.72 per year |

| 68 | $836.07 per month | $10,032.84 per year |

| 69 | $885.57 per month | $10,626.84 per year |

| 70 | $935.08 per month | $11,220.96 per year |

The average life expectancy in Canada for 2023 is roughly 83 years of age (the actuarial figure is probably much more specific). If you calculate the OAS payments started at either age 65 or 70, you will soon find that total payments actually become equal at an age slightly above 83. The government’s actuaries have calculated this to be the exact life expectancy.

| Life expectancy | Higher total income if OAS is started at: |

|---|---|

| 65 | Age 65 |

| 66 | Age 65 |

| 67 | Age 65 |

| 68 | Age 65 |

| 69 | Age 65 |

| 70 | Age 65 |

| 71 | Age 65 |

| 72 | Age 65 |

| 73 | Age 65 |

| 74 | Age 65 |

| 75 | Age 65 |

| 76 | Age 65 |

| 77 | Age 65 |

| 78 | Age 65 |

| 79 | Age 65 |

| 80 | Age 65 |

| 81 | Age 65 |

| 82 | Age 65 |

| 83 | Roughly the Same |

| 84 | Age 70 |

| 85 | Age 70 |

| 86 | Age 70 |

| 87 | Age 70 |

| 88 | Age 70 |

| 89 | Age 70 |

| 90+ | Age 70 |

Following the above calculations, if you expect to live to the age of 82 or less, you should be inclined to start OAS payments early.

If you expect to live to the age of 84 or more and do not require OAS payments in the short term, it makes sense to defer them.

Considering Taxes and OAS

OAS payments are considered as income for income tax purposes in the year that they are received. The amount of income that you are expecting to receive going forward can also help to decide when to start OAS payments.

If you are anticipating being in a lower income tax bracket in the future, you will get additional value by deferring OAS payments in the form of tax savings. Taking OAS income now, when your income is higher, may cause you to pay a higher percentage of your OAS payments towards income tax.

Keep in mind that while you are considering the tax impact of OAS payments, you will also want to consider the tax impact of CPP payments, which are usually paid around the same time as OAS.

Although it’s important to think about how OAS payments will be taxed, your life expectancy and need for income are usually more important factors to consider when making the decision to defer OAS.

OAS Clawbacks

Once OAS payments have started, you will have to be very careful to monitor your income levels in any given year to make sure you are minimizing OAS clawbacks (or avoiding clawbacks altogether).

As of 2023, you will want to try and keep your total income within a year below $86,912, which is the OAS clawback starting threshold. Every dollar of income earned beyond this threshold, if you are currently receiving OAS payments, will face a 15% tax.

Beyond the maximum threshold of $141,917, your entire OAS payments for the year will be “clawed back” or repaid to the government.

As OAS payments are a free government aid available to almost all Canadian seniors, it is important to strategically plan your income in retirement to avoid OAS clawbacks as much as you can.

Frequently Asked Questions

OAS Deferral Form?

Before you turn 65 years of age, you will want to start planning when to start OAS payments. The process for requesting changes and submitting an application for OAS is all available on the Government of Canada website.

Keep in mind that submitting an online application will require you to sign up for (or already have) a My Service Canada Account (MSCA).

Can you Defer OAS After Receiving It?

If you have recently started receiving OAS payments, the good news is that there is a chance you may be able to cancel payments and defer them instead. You can stop OAS payments within the first six months of payments starting if you are hoping to push them forward to a later date.

How to Defer OAS Payments?

OAS payments can be deferred before the age of 65 or within the first six months of payments starting by submitting an application through your My Service Canada Account.

OAS Increase for Seniors over 75?

Once you have reached your 75th birthday, your OAS payments will increase by 10% automatically in the month immediately after turning 75 years of age. This increase is substantial and can help cover some additional costs in retirement.

OAS Deferral Calculator

If you are looking for an interactive calculator online to help you analyze multiple OAS payment scenarios, TriDelta Financial offers a great calculator on their website.

Conclusion

Deciding whether to defer OAS payments until age 70 or to start taking them immediately at age 65 will depend on quite a few factors. The two most important ones are your life expectancy as well as your need for income immediately at age 65.

You will want to closely monitor your income levels throughout your whole retirement. CPP, OAS, and other income streams all add up to your final taxable income figure at year-end. This can have implications when it comes to GIS eligibility or OAS clawbacks.

If you are looking for additional pointers when it comes to thinking about retirement, be sure to read my more in-depth guide on retirement planning in Canada.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.