Looking at buying some index funds and wondering if Tangerine’s are any good?

I generally like to invest in ETFs over mutual funds, mainly due to the much lower fees.

Still, mutual funds net assets in Canada are over six times more popular than ETFs. This is likely due to the big banks selling mutual funds aggressively. However, the tide is turning, and more people are abandoning mutual funds for ETFs.

But Tangerine investment funds are not mutual funds per se. They are A-series mutual fund equivalents and an interesting option to consider for many investors. Let’s go over all of this in this Tangerine investment funds review.

Investment funds, mutual funds

Tangerine offers a generic variety of investment funds and eight portfolios at an MER that is too expensive. They are more affordable than mutual funds but expensive compared to robo-advisors.

- Easy, hands-off investing

- Well-diversified portfolios

- Costs are lower compared to mutual funds

- Low-cost ETF fund option

- Decent international exposure

- More expensive than robo-advisors and DIY

- No regular-income fund option

- Hefty transfer fee

- Very high Trading Expense Ratio (TER)

What Are Tangerine Investment Funds?

Tangerine investment funds are, in a way, mutual funds made up of index funds. An index fund is simply a fund that aims to replicate a broad market segment/index.

Take the S&P 500 as an example; arguably one of the most copied indexes in the world. An index fund that will replicate the S&P 500’s performance would essentially follow the performance of the 500 largest companies in the US.

Index funds are well diversified, so Tangerine investment funds made up of these funds (and bonds, based on which portfolio you choose) are diversified by extension.

These are passively-managed funds, which means that the good people at Tangerine who manage these funds don’t actively change the ratios at which different elements (like index funds) are allocated within the fund.

The funds progress and grow based on an indexing strategy, which means that different segments that make up the portfolio you choose will each be following a particular index.

High Fees – The Portfolio Killer

It’s a passive, almost hands-off approach to portfolio management, which is why the relatively high Management Expense Ratio (MER) of 1.06% is one of the major cons of Tangerine investment funds, a sentiment you might find common in most Tangerine investment funds reviews.

The MER is made up of investment management fees and operating expenses. That’s the fee for core portfolios that Tangerine offers. The fee for three global ETF portfolios is lower (0.77%).

1.06% MER is still about half the 2.0% average MER of series-A mutual funds (the asset classed Tangerine investment funds are equivalent to), but higher than robo-advisors like Wealthsimple that charge between 0.4% – 0.5% of your portfolio a year.

It gets even worse when you compare Tangerine fees to other ETFs like all-in-one portfolios that charge a fraction of the cost for a very similar product (around 0.20%-0.25%).

The True Cost Of Tangerine Investment Funds

It’s important to understand the impact of fees over the cost of decades and how much money DIY investment and managing your own portfolio can save you over the years.

The core portfolios of Tangerine cost you about 1.07% a year in fees, and global ETF portfolios cost about 0.77%. If you buy the ETFs yourself using a commission-free trading platform, this cuts down costs even more.

The MER for ETFs in Canada (for most index ETFs that Tangerine investment funds invest in) is usually between 0.07% to 0.15%. In many cases though, it’s under 0.1%.

But even if you take the extreme example, i.e., 0.15%, and compare it against the MER of 1.07% and 0.77%, the results are quite eye-opening.

Let’s assume you’ve created an ETF portfolio following the indexing strategy of the Tangerine investment fund, and you expect similar returns (for example let’s assume a high 10% a year).

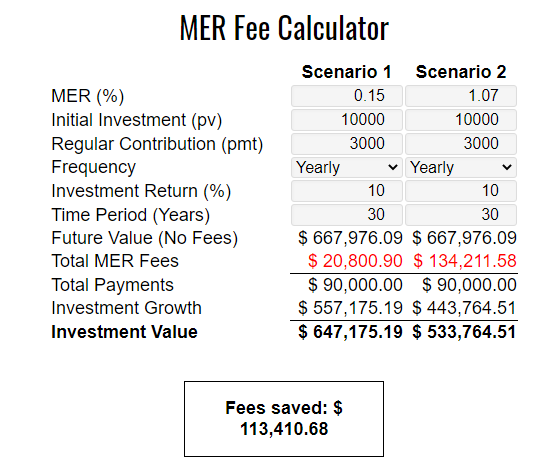

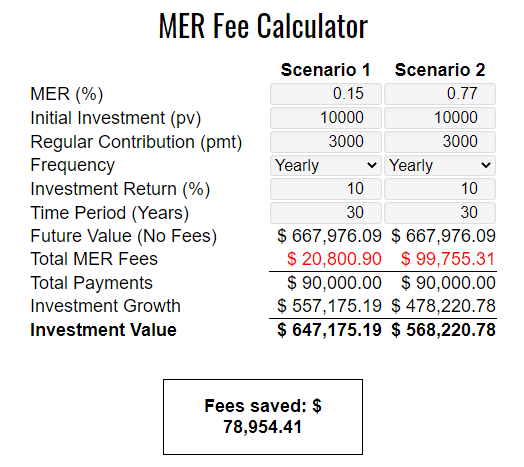

You invest $10,000 in the beginning, and after that, you invest $3,000 every year (that’s less than half of the total contribution room of your TFSA). Then following is how much the “expenses” would cost you in three decades for both approaches, i.e., Scenario 1 (DIY) and Scenario 2 (Investment fund).

For core portfolios (MER 1.07%)

For global ETF portfolios (MER 0.77%)

You can find the calculator used for these scenarios (Learningtofi) here.

It might be an oversimplification, but even if you take more granular variables to the equation, the results would be the same.

The higher the fees, the more they will eat into your portfolio’s profits. The lower the fee, the more you will be able to grow your investments.

Tangerine Investment Funds Review: Core And Global ETF Portfolios

When you choose to invest in Tangerine investment funds, you have the option to choose from:

- Five core portfolios (MER: 1.06%)

- Three global ETF portfolios (MER: 0.77%)

The five core portfolios are:

Balanced Income Portfolio

Total Fund AUM: $540 million

Risk: Low to Medium

This portfolio won the FundGrade award in 2020 and got an A+ grade. Its conservative portfolio is heavily invested in bonds (70%). The rest of the fund is distributed equally between Canadian, US, and International equities.

That’s where Tangerine’s indexing strategy comes into play. Instead of creating a portfolio from scratch and actively managing it, the fund tracks the performance of four index funds:

- E-FTSE Canada Universe Bond Index

- S&P 500 index for US securities

- S&P/TSX 60 Index for Canadian securities

- MSCI EAFE Index for international securities

The total fee of the fund adds up to 1.07% if you add the “Trading Expense Ratio,” or TER of 0.01% to the MER.

But these relatively low returns also come with the advantage of low risk. This bond-heavy portfolio is comparatively sheltered from market fluctuations, primarily because of the bond index formulation.

Over 70% of the bond index is composed of federal, provincial, and municipality bonds, which are rock solid. The rest is composed of corporate bonds, which offer better returns, albeit at more risk.

Balanced Portfolio

Total Fund AUM: $1.6 billion

Risk: Low to Medium

The balanced portfolio leans a bit more toward stocks. Its composition is 40% Canadian bonds, 20% Canadian equities, 20% US equities, and 20% international equities. The relatively heavier equity concentration reflects in its returns as well.

Still, the portfolio carries a low-to-medium risk rating, thanks to the fact that it’s two-fifth Canadian bonds. It has the highest total value of all the funds under Tangerine, so we can assume that it’s the most popular choice among Tangerine investors.

Another benefit of this portfolio is its diversification. Thanks to its distribution, your investment would be better diversified in this portfolio compared to the last bond-oriented portfolio.

It comes with a Trading Expense Ratio of 0.01%, making the total yearly cost of the portfolio 1.07%.

Balanced Growth Portfolio

Total Fund AUM: $1.4 billion

Risk: Medium

If you are looking for a portfolio that is even more evenly distributed, you might consider a balanced growth portfolio. It allocates 25% to the four indexes: Canadian bonds, Canadian equities, US equities, and international equities, respectively.

Since three-fourths of the portfolio is equities, the portfolio has a medium risk rating, making it relatively riskier relative to more bond-heavy funds.

But the diversification and broad-market indexing strategy neutralize most of the risk anyway. If you look at the actual asset allocation, the portfolio leans a bit more heavily toward Canadian equities (or the numbers work out that way). Six out of the top ten equities in the portfolio are Canadian.

Dividend Portfolio

Total Fund AUM: $199 million

Risk: Medium

Tangerine’s dividend portfolio is one of the latest funds this online bank has created. It has been around since 2016, and it’s an entirely equity-focused portfolio.

If you want to invest in a secure, well-diversified, dividend-oriented portfolio, this might be it. Its composition of dividend-based index funds is one of the reasons why it carries a medium risk rating, despite being an all-equity portfolio.

It has three components:

50% of the portfolio is made up of Canadian dividend equities. This component tracks the performance of the MSCI Canada High Dividend Yield Index.

25% of the portfolio is allocated to US dividend equities and tracks MSCI USA High Dividend Yield Index.

The remaining 25% is allocated to international equities, via the index fund MSCI EAFE High Dividend Yield Index.

Distributions are made annually. A problem with this fund is the cost. Even though its MER is the same as others (1.06%), the TER is higher (0.07%), bringing the total cost to 1.13% a year.

Equity Growth Portfolio

Total Fund AUM: $1.2 billion

Risk: Medium to High

If you have the risk tolerance for it, Tangerine offers another 100% equity-based portfolio with a more powerful growth potential than all the core portfolios.

The portfolio is made up of three segments: Canadian stocks, US stocks, and international stocks (equally distributed). But since these are growth stocks, not dividend stocks, the risk rating is higher.

The stock performed exceptionally well in 2013 and spiked to about 22.4%, and the loss in 2018 was higher than other portfolios (-4.2%), which points towards a simple fact that you should consider before investing in choosing the right portfolio, and it’s that with higher growth potential, the loss potential also becomes considerably significant.

Thanks to this distribution, the Big Five banks are among the top 15 holdings in this portfolio, along with Shopify, Enbridge, Amazon, and Apple. The fund expenses are in line with most other portfolios, i.e., 1.07%.

In addition to five core portfolios, Tangerine investment funds also include three relatively lower-cost global ETF portfolios that offer you geographic diversification (in addition to asset-class/type), and the lower fee makes them relatively more profitable against comparable growth. All three funds carry an MER of 0.77%.

Balanced ETF Portfolio

Total Fund AUM: $59 million

Risk: Low to medium

The portfolio is supposedly “balanced” between bond and equity ETFs, in a 40:60 ratio. It’s made up of five ETFs and cash. There is one bond ETF, i.e., Scotia Canadian Bond Index Tracker ETF which makes up almost 40% of the portfolio and is invested quite heavily in the government of Canada bonds, making it a low-risk ETF.

The portfolio is also heavily invested in US equity (35% of the portfolio) through Scotia US Equity Index Tracker ETF which is invested heavily in the US tech sector, primarily in the “big-five tech companies in the US: Apple, Microsoft, Amazon, Facebook, and Alphabet.

Two international equity ETFs (one for the broad equity market and the other focused on emerging markets) make up about 23% of the portfolio. Which leaves just under 2% for Canadian equity.

So even though the balanced portfolio gives you more exposure to equity, it doesn’t add a lot of Canadian equity to your portfolio (hence the name, global ETF portfolios).

This fund started in Nov 2020, and there isn’t enough data to calculate its growth potential and we can’t look at the underlying funds for guidance as well, since the Scotia Bank funds (which owns Tangerine) were only created a month before the Tangerine fund’s inception (Oct 2020).

Since these are index ETFs, you might consider looking into ETFs with similar compositions for a vague idea about how they might grow in the future.

Balanced Growth ETF Portfolio

Total Fund Value: $245 million

Risk: Medium

Annualized 5-Year Returns: N/A

If you are looking for an ETF portfolio that relies more heavily on equities than bonds (but is still safer compared to a pure equity ETF), this might be the one for you. 25% of the portfolio is made up of bonds and the rest of international equity.

It’s made up of the same five ETFs as the balanced ETF fund. The most significant element of the fund is Scotia US equity tracker, which makes up about 44%. It tracks the performance of the largest 500 companies in the US, so the performance will ultimately track the S&P 500 index.

One-fourth of the fund is made up of a Canadian bond index, which is the peak of local exposure you’ll get from this fund.

Scotia International Equity Index Tracker, which makes up about 19% of the fund, tracks the performance of about 85% of the large and mid-cap companies in both the developed and emerging markets, excluding North America. This particular index has grown about 50% in the last five years.

These three ETFs make up 88% of the fund and will guide its returns.

Equity Growth ETF Portfolio

Total Fund AUM: $149 million

Risk: Medium to High

Annualized 5-Year Returns: N/A

For investors looking for a diversified and “non-Canadian” equity exposure, without bonds for capital safety and growth weigh-down, an Equity Growth ETF portfolio might be ideal.

About 58% of the portfolio is made up of Scotiabank’s US equity index ETF, tracking the performance of the S&P 500. 25% is made up of global markets excluding North America, and about 13% is made up exclusively of emerging markets “exposure.”

The portfolio is well-diversified, and even if it’s not well-balanced (since it leans quite heavily on the US), it’s ideal for adding a significant amount of international exposure to your portfolio.

The fund itself and other global ETF funds from Tangerine are young and you might think that they offer no data to draw upon, to gauge their growth/performance potential, but that’s not true.

The underlying indexes that the ETFs in these funds are tracking offer decades’ worth of performance data. And based on the composition of the fund, you can get a relatively clear idea of how a particular ETF fund will perform in the coming years.

Investment Process

Minimum Investment

To start investing with Tangerine, you need a minimum investment of $25. This means that you can start investing with a small amount of money, making it accessible for everyone. The low minimum investment also means that you can start investing without having to commit a large amount of money upfront.

Automatic Contributions

With automatic contributions, you can set up a regular contribution to your investment account, which means that you don’t have to remember to make a contribution every month. This is a great option for people who want to make investing a habit and want to ensure that they are contributing to their investment account regularly.

Are Tangerine Investment Funds Safe And Legit?

Legit – Yes. Tangerine is one of the oldest, most well-established digital banks in the country and is a wholly-owned subsidiary of one of the big five (Scotia bank).

The company that manages these funds, i.e., Tangerine Investment Management is the wholly-owned subsidiary of Tangerine. So these funds come from “thoroughbred” financial institutions.

Safe – Yes and No. Depends on how you define safe. Mutual funds, even when they are following a safe indexing strategy and give you exposure to the market in a well-diversified way, are not inherently safe.

That’s because you can’t predict market conditions, and even though past performance is a good indicator, it’s not a surety of future returns.

So Tangerine investment funds are as safe as any other mutual funds in this regard, and you might not find a lot of complaints when you read online Tangerine investment funds reviews.

Tangerine Investment Funds Alternatives And Competitors

Any financial institution that offers passive or even actively managed mutual funds might be considered a viable alternative or a competitor to Tangerine investment funds.

So instead of comparing it against a specific bank or investment company, we can compare it against three alternative categories.

Here is a summarized comparison table for Tangerine Investment Funds, the Big Five Banks Mutual Funds, Robo-Advisors, and DIY Investing:

| Tangerine Investment Funds | Big Five Banks Funds | Robo-Advisors | DIY Investing | |

|---|---|---|---|---|

| Variety of Funds | Low (8 options) | High (hundreds of options) | Medium to High (varies by provider) | Very High (depends on individual choices) |

| Fees (MER) | Medium (around 1.07%) | High (1-2.5% for most funds, lower for e-series and others) | Low (around 0.5%) | Very Low (cost of trade commissions, varies by broker) |

| Rebalancing | Automatic | Depends on the fund | Automatic | Manual, depending on investment choices |

| Extra Perks | Convenience if you bank with Tangerine | Broad selection, potential convenience if you bank with them | May offer ESG portfolios, automatic investing features | Full control, potential for higher returns and lower costs |

| Ease of Use | High (fully managed, automatic investing) | Medium (may require active management or advisor consultation) | High (automatic investing, user-friendly interfaces) | Low to Medium (requires understanding of investments, regular monitoring) |

| Best For | Novice investors seeking convenience | Investors seeking variety and don’t mind higher fees | Investors seeking automated, low-cost options with variety | Investors willing to spend time managing their investments and learning the market to reduce costs and potentially increase returns |

Tangerine Investment Funds vs. The Big Five Bank Funds

If we compare Tangerine to the mutual funds offered by the big five, the most significant difference is variety. The big five offer a wide variety of funds (with the total number reaching hundreds), whereas Tangerine only offers eight.

The MER for balanced portfolios (at least from RY and TD) is significantly higher than Tangerine. But more comparable funds, like TD’s e-series which is passively managed and follows an indexing strategy, offer relatively lower fees compared to Tangerine.

Tangerine Investment Funds vs. Robo-Advisors

Robo-advisors usually offer a slightly better portfolio selection, and the fees are relatively lower than Tangerine. Most robo-advisors in Canada cost about 0.5% at max.

And they also throw in portfolio rebalancing and additional incentives like ESG portfolios. The Tangerine portfolio will have an edge if you already use Tangerine for your banking needs, and you wouldn’t have to move money around between your bank account and your investment account.

Tangerine Investment Funds vs. DIY Investing

Tangerine investment funds are an interesting option for novice investors who know nothing about investment. They can help you grow your savings on autopilot without any active participation from your end.

But if you can invest a little bit of time and resources in learning how to invest, DIY investing can save you several thousand dollars over a few decades by cutting down the “fees” to a mere fraction.

Conclusion

For beginner investors who already use Tangerine for their banking needs, Tangerine investment funds offer an easy, hands-off way to invest and grow your money.

The funds sit neatly between high-cost mutual funds and low-cost robo-advisors, offering a decent selection of well-diversified stocks with proven track records. I don’t see why you wouldn’t choose a robo-advisor, though, or an all-in-one ETF instead of these Tangerine funds, as they are much cheaper in fees.

And to that end, Tangerine investment funds don’t get my recommendation, and for such a high MER you should consider alternatives. Still, they are potent investment products, and I hope this Tangerine investment funds review will help you realize whether or not they are the right assets for you.

Tangerine, though has the added benefit of offering a full-fledged suite of banking products, including a savings and chequing account. Check out Tangerines other product lineup here, which I personally think holds more benefit than these investment funds.

The trading expense ratios on their ETF funds are posted in their Fund Facts documents as 0.36% so when you add that to the management fees the ETFs have been more expensive than the core funds (at least in the first half of 2021). Hopefully the TERs go down, otherwise Tangerine will be continuing with false advertising about these being low cost.