When it comes to RRIF withdrawal strategies, there are a few different tactics you can use. Which one is right for you will depend on a number of factors, including your age and how long you expect to live.

The life expectancy in Canada is 79 years for men and 84 years for women. Strategic financial planning for retirement is more important than ever.

In fact, some members of Parliament support reforming the RRIF altogether, namely by eliminating the minimum payment requirement.

Until then, there are several ways to get the most out of your retirement savings and payments, as seen below.

RRIF Basics

A Registered Retirement Income Fund (RRIF) is an account that Canadian residents can open to have income from their registered savings plan during retirement.

There are a few key differences between RRIFs and RRSPs:

- Your RRSP must be transferred to an RRIF by the end of the year you turn 71.

- You must make a minimum withdrawal from your RRIF each year, which is based on your age and the balance of your fund.

- Here is the percentage you must withdraw each year once you hit a certain age from your RRIF:

| Age of the RRIF annuitant or spouse or common-law partner | Pre-March 1986 | Qualifying RRIFs | All other RRIFs |

| 71 | 5.26% | 5.26% | 5.28% |

| 72 | 5.56% | 5.40% | 5.40% |

| 73 | 5.88% | 5.53% | 5.53% |

| 74 | 6.25% | 5.67% | 5.67% |

| 75 | 6.67% | 5.82% | 5.82% |

| 76 | 7.14% | 5.98% | 5.98% |

| 77 | 7.69% | 6.17% | 6.17% |

| 78 | 8.33% | 6.36% | 6.36% |

| 79 | 9.09% | 6.58% | 6.58% |

| 80 | 10.00% | 6.82% | 6.82% |

| 81 | 11.11% | 7.08% | 7.08% |

| 82 | 12.50% | 7.38% | 7.38% |

| 83 | 14.29% | 7.71% | 7.71% |

| 84 | 16.67% | 8.08% | 8.08% |

| 85 | 20.00% | 8.51% | 8.51% |

| 86 | 25.00% | 8.99% | 8.99% |

| 87 | 33.33% | 9.55% | 9.55% |

| 88 | 50.00% | 10.21% | 10.21% |

| 89 | 100.00% | 10.99% | 10.99% |

| 90 | 0.00% | 11.92% | 11.92% |

| 91 | 0.00% | 13.06% | 13.06% |

| 92 | 0.00% | 14.49% | 14.49% |

| 93 | 0.00% | 16.34% | 16.34% |

| 94 | 0.00% | 18.79% | 18.79% |

| 95 or older | 0.00% | 20.00% | 20.00% |

Unlike an RRSP, you don’t get a tax deduction for money you contribute to an RRIF. In fact, contributions to RRIFs are not allowed. In addition, income from an RRIF is taxed as regular income.

Canadians are living longer and, as a result, are increasingly turning to registered retirement income funds (RRIFs) to provide them with a steady stream of income in retirement.

Such funds have also become Canada’s primary asset accumulation tool, with the number of pension plans declining. This is due, in part, to the fact that RRIFs offer more flexibility and control than pensions when it comes to withdrawing funds.

For example, you can choose the frequency of your payments, and you can vary the amount of each payment depending on your needs.

RRIF Withdrawal Strategies

You’ve saved for retirement and now you’re ready to start withdrawing money from your RRIF. But how much should you take out each year and how should you divvy it up between taxable and tax-free income?

When it comes to withdrawing money from your RRIF, you have a few options.

1. Defer Payment Until Year-End

If you don’t need the money from your RRIF to meet your financial needs, you may want to receive the annual minimum payment at the end of the year. This way you can take full advantage of the RRIF’s tax-deferral feature.

Keep in mind that you cannot withdraw less than the annual minimum, no matter what time of year you make your withdrawal.

You also have the option of withdrawing more than the minimum, but the excess amount cannot be applied as part of your minimum for the next year.

Finally, you can choose to receive your RRIF payments monthly, quarterly, semi-annually, or annually, depending on your income requirements.

2. Contribute RRIF Payments To TFSA

Another option is to transfer money from your RRIF to a Tax-Free Savings Account (TFSA). If you take money from your TFSA after age 65, there is no clawback of your Old Age Security (OAS) payments.

In addition, moving investment assets into the TFSA also means that a household may qualify for additional government benefits in the future.

For these reasons, it’s often a good idea to continue to grow your investment assets in a tax-advantaged account such as the TFSA.

This can provide you with more flexibility as you’ll be able to withdraw the money at any time without having to pay tax on it. You’ll also be able to reinvest the funds back into the TFSA, so you can continue to grow your savings.

3. Split Income With Spouse

If you are over the age of 65, the income you withdraw from your RRIF can be split. This means that you can avoid paying more tax on your withdrawal by splitting it with your spouse.

The income will be taxed at his or her rate, rather than at the potentially higher rate you would pay if the entire withdrawal was taxed in your name.

If you want to take money out of your RRSP or RRIF before you turn 65, the money you take out will not be eligible for splitting.

If you are over the age of 65, money that you take out of a Registered Pension Plan (RPP), a Registered Retirement Income Fund (RRIF), or a Life Income Fund (LIF) is considered to be eligible pension income.

This could result in significant tax savings, so it’s worth investigating if you’re eligible.

To apply this strategy, you must make a joint election on your income tax returns with form T1032.

4. Use Spouse Age For Withdrawals

While we’re on the spouse topic, here’s another strategy. If you’re married and your spouse is younger than you, you can use their age as your minimum withdrawal factor.

Here’s how it works: let’s say you’re 72 years old and your spouse is 60. You can use your spouse’s age (60) instead of your own to calculate the minimum amount you have to withdraw from your RRIF each year.

This option can be a good way to keep your money in your RRIF for as long as possible if you don’t need the income from it right away or if you have other sources of income that will cover your day-to-day expenses.

To use your spouse’s age for withdrawals, there is no need to open a spousal RRIF or name them a beneficiary, just request the age adjustment with your financial institution.

5. Consolidate RRIF Accounts

Another popular RRIF withdrawal strategy is to consolidate your RRIF accounts if you have multiple RRSPs or RRIFs. By consolidating your RRIF accounts, you can streamline your investment policy and make it easier to track your progress.

You’ll also benefit from reduced fees, as many investment firms offer lower fees on accounts that have a higher balance. And finally, by consolidating your accounts you’ll achieve a better-diversified portfolio, which can help reduce overall risk.

This will make the transition to retirement much easier and help you avoid any unnecessary confusion.

6. Consider Estate Planning

One important thing to consider when planning your RRIF withdrawals is the estate tax implications. If you don’t plan carefully, the taxman could end up taking a sizeable chunk of your retirement savings.

If you die before withdrawing all the funds, you will relinquish a significant portion of your retirement savings to taxes.

That’s because Canada imposes estate taxes that are due immediately upon your death.

However, there is a way to avoid this. If you can, transfer your registered investment portfolio to a surviving spouse or dependent child.

The surviving spouse or dependent child would then become the new account holder and would be responsible for making RRIF withdrawals based on their own life expectancy.

The Importance of Withdrawal Strategies

When the time comes to start withdrawing funds from your RRIF, it’s important to think about the tax implications.

The general rule of thumb is to withdraw as little as possible from your RRIF in order to allow the money to grow tax-deferred. However, this isn’t always the best strategy.

You need to take into account the tax consequences of withdrawing money and your life expectancy.

For example, if you’re in a high tax bracket and don’t expect to live much longer, it may be better to withdraw more money from your RRIF and pay the taxes now.

On the other hand, if you’re in a lower tax bracket and expect to live for many years, it may be better to withdraw less money so that the funds can continue to grow tax-deferred.

It’s important to have a withdrawal strategy in place so you can make the most of your RRIF, after all, you spent years saving for retirement!

There are a few different things to keep in mind when creating your strategy.

- You’ll want to think about how much money you’ll need each year to cover your expenses. This will help you determine how much you can safely withdraw from your RRIF without running out of money.

- You’ll also want to consider your current age and life expectancy. This will help you decide how long your RRIF will last and how much money you can safely withdraw each year.

- You’ll want to make sure you have a plan for what to do with the money you won’t need right away. This could include investing it, putting it into a savings account, or using it to cover immediate expenses.

Having a withdrawal strategy in place is an important step in making the most of your RRIF. By considering these things, you can ensure that your retirement savings will last as long as possible.

When Can I Withdraw From My RRIF?

You have to transfer your RRSP into an RRIF once you turn 71 and start taking payments the following year.

Your RRIF withdrawals will be taxed as regular income, so it’s important to think about your needs and tax situation when making your decision. It’s essential to plan your withdrawals accordingly so that you don’t end up paying more tax than necessary.

Ideally, you want to contribute to your RRSP when you’re in a higher tax bracket and withdraw from your RRIF when you’re in a lower tax bracket. That way, you’ll pay less tax overall.

Keep in mind that tax rates can change over time, so it’s important to plan ahead. Many people assume that they will be in a lower tax bracket in the future – but that’s not always the case.

How Much Should I Withdraw From My RRIF?

How much you withdraw from your RRIF each year will depend on a few different factors, such as your age, life expectancy, and your lifestyle.

There’s no one-size-fits-all answer when it comes to RRIF withdrawals, so it’s important to speak with your financial advisor to create a plan that’s right for you. The one thing to keep in mind is withholding taxes.

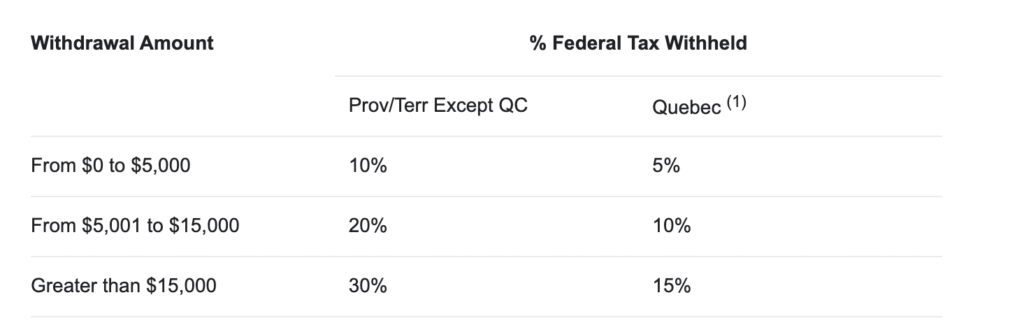

Withholding Taxes

If you take out more than the minimum withdrawal, you’ll be charged with withholding tax on the surplus. On your behalf, your financial institution will hold back an amount equal to the applicable withholding tax rates and send it to the government.

The withholding tax rates for Canadian residents are the same for all provinces and territories except Quebec, where a different rate applies.

RRIF Withdrawal Mistakes to Avoid

Making the most of your RRIF involves not just understanding its potential benefits but also being aware of potential pitfalls. Here’s a more detailed look:

- Withdrawing Too Early: The allure of accessing funds at the onset of retirement can be tempting. However, an early withdrawal can severely affect the compounding potential of your investments. By drawing down too soon, you limit the time for the remaining funds to grow, which can significantly reduce the overall value of your RRIF in the later stages of retirement.

- Ignoring Tax Implications: The funds you withdraw from your RRIF are taxable. Making large withdrawals in a particular year might push you into a higher tax bracket, meaning you’ll owe more in taxes.

- Forgetting Minimum Withdrawal Limits: The government mandates a minimum withdrawal amount based on age and RRIF value. Not adhering to this can result in a hefty penalty, which is 50% of the amount you should have withdrawn.

- Lack of Diversification: Relying heavily or solely on RRIFs can be a gamble, given market uncertainties. Complement your RRIF with other investment avenues, like stocks, bonds, or real estate, to create a well-rounded retirement portfolio.

RRIF and Estate Planning

Your RRIF plays a significant role in estate planning. Here are some in-depth considerations:

- Taxation Upon Death: At the time of your death, unless the RRIF is passed on to a surviving spouse or a dependent child, its entire value is considered income for that year. This can potentially push the estate into a higher tax bracket, leading to a substantial tax liability. Proper planning can mitigate this.

- Beneficiary Designations: Directly naming a beneficiary, preferably a spouse, can ensure the continued tax-deferred growth of the RRIF. It’s vital to revisit and possibly update these designations periodically, especially after major life events like marriage, divorce, or the birth of a child.

- Spousal RRIF: Basing your RRIF minimum withdrawals on a younger spouse’s age can be a strategic move. This not only reduces the annual mandatory withdrawal amounts, preserving more of your capital, but also provides a larger financial cushion for your spouse if they outlive you.

- Charitable Giving: Naming a charity as a RRIF beneficiary can be both philanthropic and strategic. Upon death, any funds given to a registered charity can be used to claim charitable tax credits on the final tax return, potentially offsetting some of the taxes owed by the estate.

Conclusion

It’s important to plan your RRIF withdrawals strategically in order to make the most of your savings.

Withdraw too much too soon, and you could run out of money before you retire, but withdraw too little, and you may not be able to cover your costs in retirement.

There are a variety of withdrawal strategies to choose from, so take the time to see which option is best for you. To keep on track with retirement planning, check out Retirement Income Sources In Canada: 10 Great Options (2022)

My OAS has been cut by 50%. Need a strategy to recover some of it at least

Hi there, my question is : If my RRIF has all 5-year non-cashable/non-redeemable GICs in it, how does one withdraw the minimum needed annual amount of money out of it ? Thanks.

It depends on your RRIF – do you have other assets in it other than that GIC?

Credit Unions allow you to withdraw your minimum RRIF amount from the term that has the lowest interest rate. Does not matter if it is locked into a term.

That’s interesting Amanda! Do you have a link to a website source for this? If I can link to a good source I will update the article. Thank you.