CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

Even if you’re paying a monthly fee for your chequing account, the costs of using ATMs, getting money orders, sending e-transfers, and safety deposit boxes can really add up each year.

If you find yourself dishing out extra dollars each year for extra fees, it might be worth getting a premium banking account such as the TD All-Inclusive Banking Plan, which includes several different features under a single umbrella fee.

Today’s post will detail whether or not the $30 monthly fee of the TD All-Inclusive account is worth it, all of the features and benefits, the potential alternatives on the market, and how you can sign up.

Advertisement

Hint: depending on your transaction habits, the TD All-Inclusive Account can actually save you money per year, despite its high price tag!

[affiliatable id='78349']

Pros

-

Free and unlimited transactions

-

Free and unlimited Interac e-transfers

-

No ATM usage fees worldwide

-

Free money orders and certified cheques (usually $5-$8 each)

-

Free safety deposit box (usually $60 per year)

-

Annual credit card fees for select cards waived (save up to $140 per year)

-

Free personalized premium cheques

Cons

-

Monthly fees come to $359.40 per year

-

Sending wire transfers still costs $50, and receiving costs $17.50

-

The minimum balance for the monthly fee rebate is quite high ($5,000), especially given that it’s not making interest

Introduction: What Is the TD All-Inclusive Account?

The TD All-Inclusive Banking Plan is one of TD Canada Trust’s most premium chequing account options.

It offers its users free and unlimited transactions, great banking perks, waived fees, and travel-friendly benefits to make your day-to-day banking seamless.

This will especially be the case if you’re a frequent user of your debit card/chequing account and find yourself dishing out hundreds of dollars per year in various fees.

As hinted at by the name, the account is truly “all-inclusive.” But, what is the cost to you?

The TD All-Inclusive Banking Plan costs $30 per month, totalling nearly $360 each year in fees.

I know the price tag might sound steep, but there is actually a chance you could end up saving money each year.

This depends on how much you end up taking advantage of the account’s perks. If you’re already paying for most of these transactions out of pocket per month, this account can really be helpful to you.

Let’s get into the features and benefits to figure out what to expect from this account and whether it might actually save you money in the long run.

Features and Benefits: What To Expect From The TD All-Inclusive Account

Here are all of the features of this “all-inclusive” chequing account.

Unlimited Transactions

This feature is pretty straightforward and is usually sported by digital accounts in Canada, such as Tangerine.

TD’s All-Inclusive Banking Plan includes free and unlimited chequing account transactions, such as debit card purchases, pre-authorized payments, Interac e-transfers, bill payments, withdrawals, cheque deposits, etc.

In short, you will not be paying individual transaction fees with this account regardless of how many transactions you make per month, which is great.

No TD ATM Fees for All Canadian or Foreign ATMs

Most of us are familiar with the fees associated with using an ATM that is not affiliated with your bank or an ATM in a foreign country. Luckily, TD’s All-Inclusive account waives all fees regarding ATM use, at least on their end.

This means that TD will not charge you for using a non-TD ATM or any other ATM when you’re travelling abroad. Usually, banks charge anywhere from $2 to $5 for these transactions.

However, do note that the ATM provider may still charge fees, and if you’re withdrawing money in a foreign country, you may be charged foreign exchange fees, even with this account.

Nonetheless, this card can save you money and time if you’re a frequent user of ATMs.

Free Safety Deposit Box, Certified Cheques, Money Orders and Personalized Cheques

This is where your savings can really start to skyrocket.

With the TD All-Inclusive Account, you get access to:

-

A free small safety deposit box (which usually has an annual cost of $60)*,

-

Free and unlimited certified cheques (usually $8 each)

-

Free and unlimited money orders (usually $5 each)

-

Free personalized cheques in any style, including premium cheques.

If you’re regularly paying for the above features out of pocket, I recommend considering the TD All-Inclusive account. If you rarely pay for such services, however, the high price tag of the account may not be worth it.

*Please do note that the safety deposit box feature is dependent on availability. In my personal experience in banking, these boxes get filled up rather quickly and there ends up being a waiting list.

You may have to visit various TD branches in your area to find an available one.

Annual Credit Card Fee Rebate on Select TD Credit Cards

If you open a TD All-Inclusive Account, you may be eligible to get the annual fee of your credit card, along with an additional user’s, waived (up to a $140 value.)

This offer applies to the following credit cards:

-

TD Aeroplan Visa Infinite Card,

-

TD Aeroplan Visa Platinum Card,

-

TD Platinum Travel Visa Card,

-

TD First Class Travel Visa Infinite Card,

-

TD Cash Back Visa Infinite Card.

That’s an annual saving of more than $140 right off the bat, lowering the fee of this chequing account by a third.

TD Borderless Plan Discount

The All-Inclusive account already gives frequent travelers the perk of waived ATM fees abroad.

But if you’re a regular US traveller, you may be able to reap another advantage.

TD All-Inclusive Account holders get a refund of USD $3 on the Borderless Plan monthly fee, bringing the account’s monthly fee to $1.95. That’s savings of another $40 per year in the process.

In case you’re interested, TD’s Borderless account is an all-inclusive U.S. dollar account. You can find out more about it here.

Account Fees Explained: TD All-Inclusive Account

It’s clear that you can get many perks, discounts and rebates for holding this account. Now let’s go through the costs in detail.

The account costs $29.95 per month for regular account holders and $22.45 for seniors (60+.) That comes out to $359.40 or $269.40 per year, respectively. Below is a detailed breakdown of the costs associated with this account.

TD All-Inclusive Account Minimum Balance

The monthly account fee of $29.95 ($22 for seniors) can be waived if you keep a minimum balance of $5,000 in your account.

This means that you must have $5,000 or more in your TD All-Inclusive Account at the end of each day in the month. If you have $4,999 at the end of even just one day, your fee will not be rebated for that month.

I know this is harsh, but unfortunately, this is the case with most “minimum balance” rules in the country.

If you make a big purchase and forget to replace your balance by the end of the day, you will be charged $30 for that month. That’s why I rarely recommend trying to stick to the minimum balance rule to save on fees, especially if it’s as high as $5,000.

If you don’t have the budget to pay the $30 per month, I would not recommend signing up for this account.

Advertisement

At the end of the day, the $5,000 is your money, and you should be able to have frequent access to it without worrying about a $30 monthly account fee.

Does TD Waive Annual Fees?

By holding a TD All-Inclusive Account, you can get the annual fee of one of five premium credit cards waived.

This can save you more than $140 per year upfront in credit card fees, in addition to the perks you get with the card itself, such as travel rewards, insurance, or cashback.

To be eligible for this program, you must apply and be approved for one of the following credit cards: TD Aeroplan Visa Infinite Card, TD Aeroplan Visa Platinum Card, TD First Class Travel Visa Infinite Card, TD Cash Back Visa Infinite Card, or TD Platinum Travel Visa Card.

As always, credit cards are a huge opportunity for banks to make money by charging you high interest on carried-over balances.

Therefore, I would recommend being careful about not overspending to remain in good standing with the bank and avoid high-interest rates.

Otherwise, if you are interested in getting one of these credit cards anyways, coupling it with the TD All-Inclusive account may be a smart move.

Rewards

One of the most attractive features of the TD All-Inclusive Account is the rewards program. With this account, you can earn TD Rewards points for every dollar you spend on your TD credit card. You can redeem these points for travel, merchandise, and other rewards.

Additionally, you can earn bonus points for setting up a Pre-Authorized Debit for your TD credit card payments or for signing up for a TD credit card with an annual fee.

Additional Benefits

Here are some of the key benefits you can enjoy with the TD All-Inclusive Account:

TD App

The TD App is a mobile banking app that allows you to manage your accounts, pay bills, transfer money, and more, all from your smartphone or tablet. With the TD App, you can also deposit cheques using your mobile device, view your account balances and transaction history, and set up alerts to stay on top of your finances. The app is available for both iOS and Android devices, and it's free to download.

TD MySpend

TD MySpend is a feature within the TD App that helps you track your spending and stay within your budget. With TD MySpend, you can see how much you're spending on different categories, such as groceries, dining out, and entertainment. You can also set up notifications to alert you when you're getting close to your budget limit.

Simply Save Program

The Simply Save Program is a feature that helps you save money automatically. With the Simply Save Program, you can set up automatic transfers from your chequing account to your savings account, so you can save money without even thinking about it. You can choose the amount you want to transfer and the frequency of the transfers, and the money will be transferred automatically on the dates you specify.

Alternatives and Competitors Of The TD All-Inclusive Account

Although pretty good, TD’s All-Inclusive Account is not a one-of-a-kind account. Let’s compare it to some other similar options on the Canadian market, as well as other types of chequing accounts, to see if you really need an “all-inclusive” account like this one.

Competitor: TD All-Inclusive Plan Vs. RBC VIP Banking

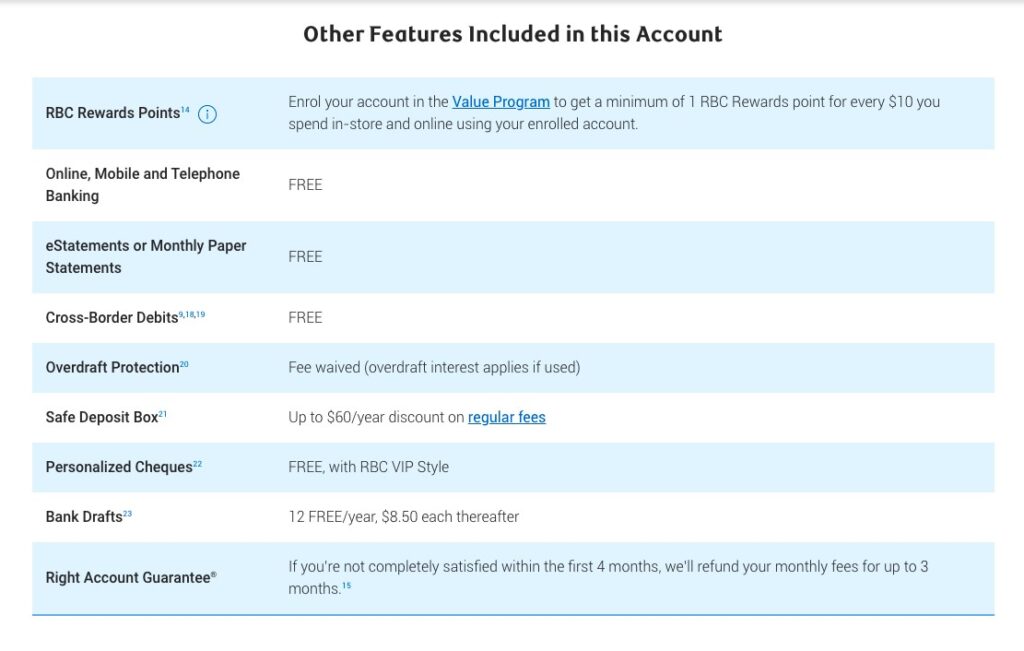

RBC is another banking giant in Canada and offers similar perks in their RBC VIP Banking package.

Some of this account’s features include:

-

$30 for regular account holders, $22.50 for seniors (account fee rebates available with the RBC Value Program - no minimum balances involved)

-

Unlimited debit transactions worldwide

-

Free Interac e-Transfer transactions

-

No RBC fee to use ATMs worldwide

-

Up to a $120 rebate on the annual fee of an eligible credit card

-

RBC Direct Investing maintenance fees waived

Other features associated with this account are:

All in all, this RBC account is very comparable to the TD All-Inclusive. However, I would choose the RBC account if you find yourself paying quite a lot in RBC Direct Investing maintenance fees each year.

Otherwise, you should do a breakdown of how much you are paying out of pocket for the features offered by this account and figure out whether it would be worth it.

Alternative: TD All-Inclusive Account Vs. TD Unlimited Chequing Account

The TD All-Inclusive Account is great if you frequently use your debit card/chequing account, regularly need money orders/certified cheques, and are on the market for a premium credit card with no fees.

If you only make a few chequing account transactions per month, then you might be just fine with a less “inclusive” chequing account. Let’s compare the TD All-Inclusive account with the TD Unlimited Chequing Account, which is just one step “down” from the former.

The TD Unlimited Chequing Account offers, you guessed it, unlimited transactions per month at $16.95 for regular account holders and $11.95 for seniors (60 years or older.)

The main differences between the two accounts are that you only get your first year’s annual fee rebated for your credit card and have a $3-$5 charge for foreign ATM use. This account, however, is half the cost of the All-Inclusive account.

Depending on your needs and transaction habits, you might be able to save just as much or even more through the TD Unlimited Account.

Alternative: TD All-Inclusive Account Vs. Tangerine Chequing Account

Tangerine is a fully-digital bank that has no physical branches. If this is okay with you, then you can get great perks with them for absolutely no cost or minimum balance.

As a Tangerine customer, you also get access to all Scotiabank ATMs, which is a great bonus.

Here are some of the features of the Tangerine Chequing Account:

-

No fees for daily transactions such as debit purchases, bill payments, pre-authorized payments, Tangerine Email Money Transfers and Interac e-Transfers

-

Up to 0.10% interest rate on your balance

-

Non Scotiabank ATM use: $1.50

-

First chequebook of 50 cheques free ($50 per chequebook afterwards)

-

$10 draft cheques (includes courier)

Do note that certain things such as safety deposit boxes and prompt certified cheques require in-person exchanges and thus cannot be satisfied by Tangerine.

If these things are important to you, I would recommend going with a traditional bank, such as TD or RBC.

Nonetheless, you can save hundreds per year with Tangerine as you don’t have to pay a single penny in monthly fees.

How To Sign Up for the TD All-Inclusive Account

As I said, the TD All-Inclusive Plan can very much so be worth it if you’re paying for most of its free features out of pocket each year. If that’s the case, you should certainly consider signing up for this account.

Here’s how:

-

Head to the product page for the TD All-Inclusive Plan.

-

Click “Open Account.”

-

Choose whether or not you’d like to also apply for additional accounts or features, such as the USD Borderless Account, a Savings Account, or overdraft protection. Click continue.

-

Complete your application by filling out your details.*

*Please note, you must be the age of majority in the province or territory of your residence and have a valid email address at the time of your application.

Final Verdict

Fees for ATM use, bank drafts, cheques, credit cards, and safety deposit boxes can really add up each year. And the thing is, you may still be paying a monthly fee for your chequing account on top of all of these fees.

An “all-inclusive” account like this one by TD can be a solution. By paying a set monthly fee for everything, you don’t have to worry about going above your banking budget each month.

All in all, I would recommend the TD All-Inclusive Account, but on one condition: that you actually need and will take advantage of the account features.

That is, if you've never used a safety deposit box and don’t feel like you need one, or you don’t travel enough to take advantage of the free ATM withdrawals, then it may not be worth it to pay the high monthly fee for this account.

The same thing applies if you don’t need or want a new “premium” credit card or rarely buy money orders or certified cheques.

If your banking needs are met by a digital bank, or even a pay-as-you-go or simple chequing account, then I would not recommend an all-inclusive account like this one.

At the end of the day, it’s all about your banking needs. Like I said earlier, there is certainly value in this account, but only if you will be taking advantage of them!

And hey, if you don’t have to worry about keeping $5,000 in your account every month to satisfy the rebate requirement, you could invest that money instead. Check out this review on TD Direct Investing to explore your options at this bank.

Best next step

Keep exploring this topic

If you want to go deeper, these are the most useful follow-up pages and tools for this topic.

Banking next step

Compare high-interest savings rates

Move from banking basics into current cash rates and safer places to park your money.

Safe cash option

See the best GIC rates in Canada

Compare guaranteed rates if you are choosing between keeping cash liquid or locking it in.

Savings tool

Estimate your TFSA room

Work out how much tax-sheltered room you still have before you move extra cash into savings.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.