CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

For Canadian families looking to secure their children's academic future, Registered Education Savings Plans (RESPs) offer a powerful savings tool.

This comprehensive guide will walk you through RESP contribution limits, government grants, and strategies to optimize your education savings.

Advertisement

Want to see how much the goverment will give you with the Canada Education Savings Grant ? Skip here instead

Lazy to read - Check this out instead:

https://youtube.com/shorts/X2S3fFqV4tI?si=yaGXlieWBRjnlxEg

What is an RESP?

An RESP is a government-registered plan designed to help you save for a beneficiary's post-secondary education. Before diving into the specifics of contribution limits, let's review the key benefits of an RESP:

-

Tax-deferred growth: Your investments grow tax-free within the plan until withdrawal.

-

Government grants: Eligibility for federal and some provincial education savings grants.

-

Flexibility: Freedom to decide contribution amounts and investment options.

For more detailed information on RESPs, visit the official Government of Canada RESP page.

RESP Contribution Limits: What You Need to Know

Understanding RESP contribution limits is crucial to maximize your savings and avoid penalties. Here are the key points to remember:

Lifetime Contribution Limit

-

The lifetime RESP contribution limit is $50,000 per beneficiary.

-

This limit applies across all RESPs for a single beneficiary, regardless of the number of plans or contributors.

Annual Contribution Limit

-

There is no annual contribution limit for RESPs.

-

However, to maximize the Canada Education Savings Grant (CESG), it's recommended to contribute up to $2,500 per beneficiary per year.

Contribution Period

-

You can contribute to an RESP for up to 31 years.

-

The plan can remain open for a maximum of 35 years.

For a detailed breakdown of contribution rules, check the Canada Revenue Agency's RESP contribution guidelines.

Government Grants: Boosting Your Savings

One of the most attractive features of RESPs is the government grants available to supplement your contributions. Let's explore the primary grant and other programs:

Canada Education Savings Grant (CESG)

[CP_CALCULATED_FIELDS id="9"]

-

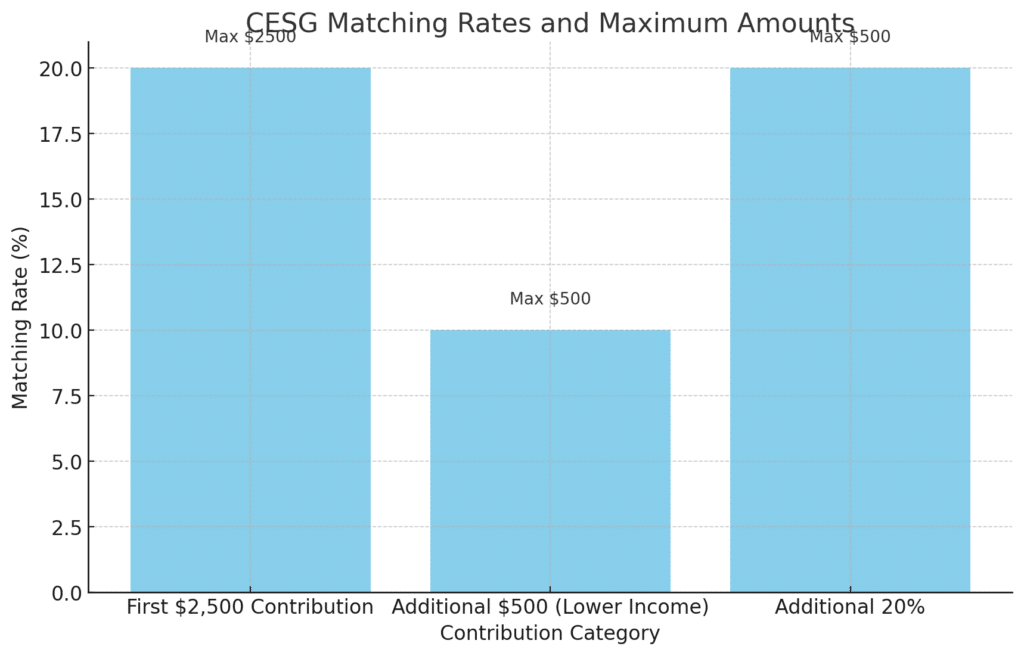

Basic CESG:

-

The government matches 20% of your annual contributions, up to $500 per year.

-

To receive the full $500, you need to contribute $2,500 annually.

-

The lifetime maximum CESG per beneficiary is $7,200.

-

-

Additional CESG:

- Middle- and low-income families may qualify for an extra 10% or 20% on the first $500 contributed annually.

-

CESG Eligibility:

-

Available until the end of the calendar year in which the beneficiary turns 17.

-

Special eligibility requirements apply for beneficiaries aged 16 and 17.

-

-

Carry Forward of CESG Room:

-

Unused CESG amounts can be carried forward, allowing you to catch up on contributions in future years.

-

You can receive up to $1,000 in CESG in a single year when catching up.

-

For more information on the CESG, visit the official CESG information page.

Additional Government Programs

Depending on your province and income level, you may be eligible for other programs:

-

Canada Learning Bond (CLB):

-

Provides up to $2,000 for low-income families.

-

No personal contributions are required to receive the CLB.

-

Learn more about the Canada Learning Bond.

-

-

Quebec Education Savings Incentive (QESI):

- Available for Quebec residents.

Advertisement

- Matches up to 10% of your annual contributions, with a maximum of $250 per year.

- Visit [Revenu Québec's QESI page](https://www.revenuquebec.ca/en/citizens/tax-credits/quebec-education-savings-incentive/) for details.

5. British Columbia Training and Education Savings Grant (BCTESG): - One-time $1,200 grant for eligible B.C. residents.

- Check your eligibility on the [BCTESG information page](https://www2.gov.bc.ca/gov/content/education-training/k-12/support/scholarships/bc-training-and-education-savings-grant).

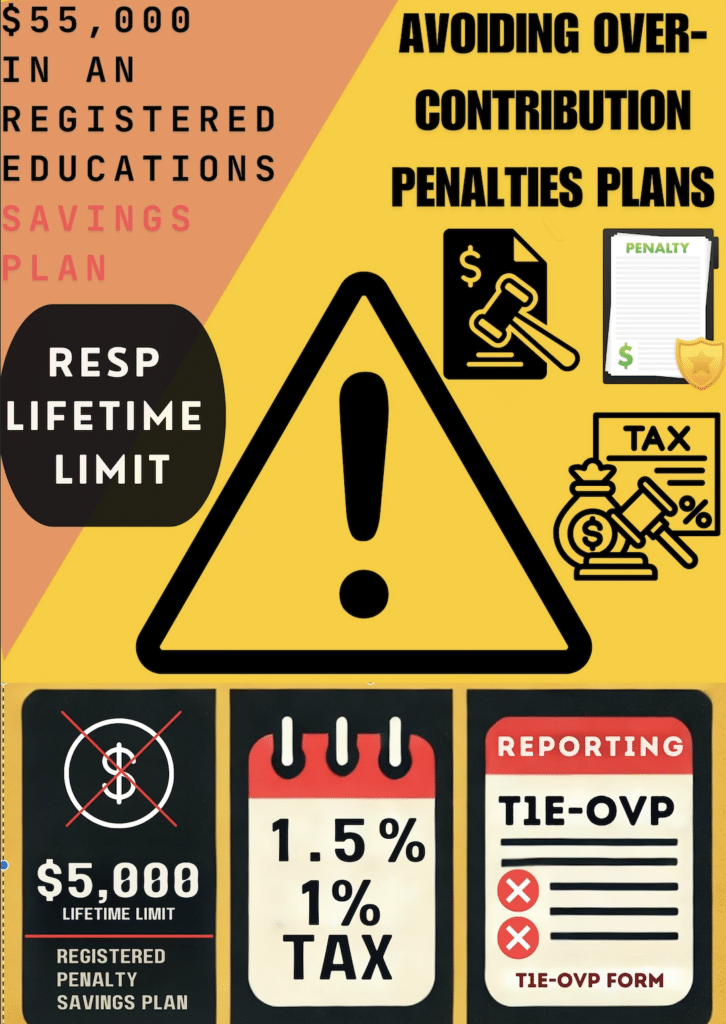

Avoiding Over-Contribution Penalties

While maximizing your contributions is important, it's crucial to avoid exceeding the lifetime limit:

-

Over-Contribution Definition:

- Occurs when total contributions across all RESPs for a beneficiary exceed the $50,000 lifetime limit.

-

Penalty:

-

1% per month tax on the subscriber's share of the excess contribution.

-

Applies until the excess amount is withdrawn.

-

-

Reporting:

-

Subscribers must report their share of excess contributions using Form T1E-OVP.

-

The tax is payable within 90 days after the end of the year in which the excess contribution occurred.

-

For more information on over-contributions, consult the CRA's guidelines on RESP excess contributions.

Strategies for Maximizing RESP Benefits

To get the most out of your RESP, consider these strategies:

-

Start Early

-

Contribute Regularly

-

Catch Up on Missed Contributions

-

Consider Family Plan Flexibility

-

Involve Family Members

-

Reinvest Child Benefits

-

Educate Older Children

-

Avoid Over-Contributing

-

Explore Alternative Savings Vehicles

For more savings tips and strategies, check out the Government of Canada's education savings tips.

Conclusion

RESPs offer a powerful combination of tax-deferred growth and government grants to help you save for your child's education. By understanding contribution limits, maximizing government grants, and implementing smart savings strategies, you can build a substantial education fund for your child's future. Remember to start early, contribute regularly, and stay within the contribution limits to make the most of this valuable savings tool.

With careful planning and consistent contributions, you can give your child the gift of education and set them on the path to a bright future.

For comprehensive information on managing your RESP, visit the Government of Canada's RESP management page.

Frequently Asked Questions (FAQ) about RESP Contribution Limits

Q: What does contribution limit mean?

A: The contribution limit refers to the maximum amount of money that can be contributed to a Registered Education Savings Plan (RESP) for a beneficiary. This limit is set by the Canadian government to ensure fair use of the tax advantages and grants associated with RESPs.

Q: What is my contribution limit?

A: Your personal contribution limit depends on how much has already been contributed to RESPs for the beneficiary. The key limits to remember are:

-

Annual limit: There is no annual limit, but contributing $2,500 per year maximizes the Canada Education Savings Grant (CESG).

-

Lifetime limit: $50,000 per beneficiary across all RESPs.

Q: What is the total contribution limit?

A: The total lifetime contribution limit for each RESP beneficiary is $50,000. This limit applies regardless of how many RESPs are opened for the beneficiary or how many people contribute. It's important to keep track of all contributions to avoid exceeding this limit.

Q: What is the maximum contribution limit for 2024?

A: For 2024, there is no set annual contribution limit for RESPs. You can contribute up to the lifetime limit of $50,000 per beneficiary, minus any contributions made in previous years. However, to maximize the CESG, it's recommended to contribute $2,500 per year, or up to $5,000 if you're catching up on unused grant room from previous years.

Remember, while you can contribute more than $2,500 annually, you won't receive additional CESG on contributions beyond this amount in a given year. Always consider your overall contribution strategy to maximize benefits while staying within the lifetime limit.

For more FAQs about RESPs, visit the Government of Canada's RESP FAQs page.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.