CIBC Investor's Edge

Transfer your investments to CIBC Investor's Edge and get rewarded with an offer of up to $3,000.

- ✓$6.95 flat-rate commissions

- ✓Backed by Big Five bank security

- ✓Transfer bonus offer up to $3,000

Trusting in robo-advisors to help you achieve substantial long-term returns on your investment can be challenging. There are several robo-advisor products in Canada, and the number keeps increasing.

For someone entirely new to the world of robo-advisors, establishing trust in relatively new institutions can be a challenge. However, more traditional financial institutions are also entering the market.

The Bank of Montreal is a name you likely already know. It has also entered the market for robo-advisor products for Canadians.

In this BMO SmartFolio review, I will discuss a robo-advisor that is backed by a well-known bank. \

Pros

Cons

How to Choose the Right Robo-Advisor

When you are considering robo-advisors, here are a few crucial factors you need to consider:

-

Fees: The goal is to make the most of your investment to make more money. Getting a low-fee product that helps you grow your wealth is the most important factor.

-

Portfolios Offered & Performance: When it comes to investment, you need to have various options that align with your goals. You need a robo-advisor that offers you several types of portfolios suitable for various investment goals and risk tolerance.

-

Accounts Offered: There are various types of accounts available, and each offers its own features. You need to choose a robo-advisor that presents you with several account types to store your investment.

-

Customer Service: Gauge the kind of customer support you can get from the platform. The level of customer support is crucial to help you make the most of your investment experience with a robo-advisor.

What is BMO SmartFolio?

BMO SmartFolio is a robo-advisor highlighting The Bank of Montreal’s online investing offerings. The oldest bank in the country, BMO, is among the first traditional banks to offer an online investment management service.

BMO Nesbitt Burns manages your account, and your portfolio of Exchange-Traded Funds (ETFs) primarily consists of BMO Global Asset Management. Despite being the oldest bank, BMO has been at the forefront of integrating technological innovations.

It was the first among Canadian banks to create its own ETFs and launch its proprietary online ETF portfolio management service through BMO SmartFolio.

Unlike many typical robo-advisor products, your portfolio is managed by a team of expert portfolio managers. The team of experts consists of 17 financial experts with over 300 years of combined experience.

Available in all Canadian provinces and territories, this is not the cheapest option for online investing, and it does not feature several standard features other robo-advisors may have.

However, it offers you the security of BMO itself and the comfort of the human touch of industry experts, which may be worth the premium fees.

Features and Benefits

We will discuss several key features and benefits that BMO SmartFolio offers to help you better grasp what you can expect from this robo-advisor product.

BMO SmartFolio Accounts Offered

BMO SmartFolio offers you several types of accounts you can open with the robo-advisor to meet various investment goals using the robo-advisor, including:

-

Individual Registered Retirement Savings Plan (RRSP)

-

Spousal RRSP

-

Tax-Free Savings Account (TFSA)

-

Individual Registered Retirement Income (RRIF)

-

Spousal RRIF

-

Individual Registered Education Savings Plan (RESP)

-

Family RESP

-

Joint Account

-

Non-registered TaxableAccounts (Individual, Family, and Corporate)

BMO SmartFolio Portfolios Offered

In this section of my SmartFolio review, I will discuss the various ETF portfolios you can opt for with the robo-advisor. BMO SmartFolio offers five model ETF portfolios designed to cater to investors with different investment goals and risk tolerance. Here are the portfolios that the robo-advisor offers you:

-

Capital Preservation portfolio: The most conservative portfolio comprises 10% Equities and 90% fixed-income target allocation.

-

Income portfolio: A more growth-oriented portfolio comprising 30% equities and 70% fixed-income assets.

-

Balanced portfolio: This ETF portfolio is balanced between 50% equities and 50% fixed-income assets.

-

Long-Term Growth portfolio: A portfolio slightly inclined towards growth that consists of 70% equities and 30% fixed-income assets.

-

Equity Growth portfolio: BMO’s most high-risk and high-reward portfolio consists of 90% equities and 10% fixed-income assets.

BMO uses its in-house ETFs provided through BMO Global Asset Management in various combinations to create the portfolios above. The ETFs this robo-advisor uses to create these portfolios include:

-

BMO S&P/TSX Capped Composite ETF (ZCN)

-

BMO MSCI USA High-Quality ETF (ZUQ)

-

BMO Mid Federal Bond ETF (ZFM)

-

BMO Equal Weight US Banks ETF (ZBK)

-

BMO Low Volatility US Equity ETF (ZLU)

-

BMO MSCI EAFE ETF (ZEA)

-

BMO Mid Provincial Bond ETF (ZMP)

-

BMO Short Corporate Bond ETF (ZCS)

-

BMO Mid Term US IG Corporate Bond Hedged to CAD ETF (ZMU)

-

BMO Long Federal Bond ETF (ZFL)

-

BMO Mid Corporate Bond ETF (ZCM)

-

BMO Equal Weight US HealthCare Hedged to CAD Index ETF (ZUH)

-

BMO Global Infrastructure ETF (ZGI)

-

BMO Aggregate Bond Index ETF (ZAG)

-

BMO S&P 500 ETF (ZSP)

-

BMO High Yield US Corporate Bond Hedged to CAD (ZHY)

-

BMO Equal Weight REITs Index ETF (ZRE)

When you create an account, you will have to answer a series of questions designed to determine your risk tolerance level. The robo-advisor matches you to a recommended portfolio based on your responses to the questions. I think it is better to know what you want before you go into it.

BMO SmartFolio Performance

I will discuss the performances of each of the portfolios offered to you by BMO SmartFolio since its inception. It will give you a better idea of what to expect. Each of these accounts for the performance of the portfolio with a presumed $100,000 in the account.

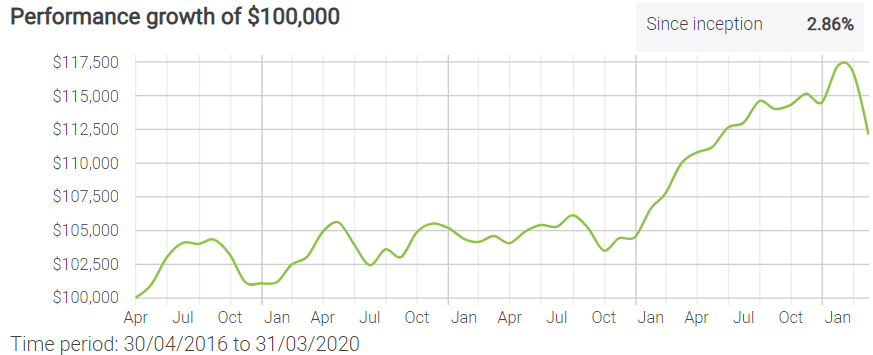

Capital Preservation Portfolio:

This is a portfolio designed for investors who cannot tolerate too much risk. It is recommended for investors with a short-term investment plan for around a couple of years since it does not offer much in terms of growth.

Growth since inception: 2.86% (per annum) - March 2020

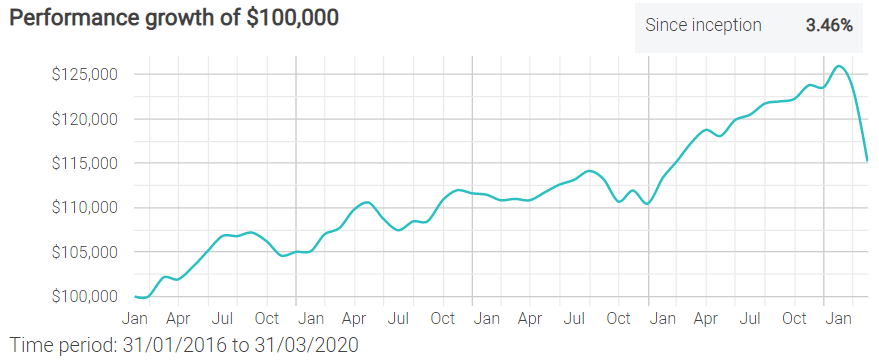

Income Portfolio:

The income portfolio can produce more earnings from your investment without losing too much stability in the long run.

Growth since inception: 3.46% (per annum) - March 2020

Balanced Portfolio:

If you are looking for both income and substantial long-term growth, you might feel inclined to take on a slightly higher risk. The balanced portfolio splits between equities and fixed-income assets to cater to balanced risk tolerance.

Growth since inception: 4.12% (per annum) - March 2020

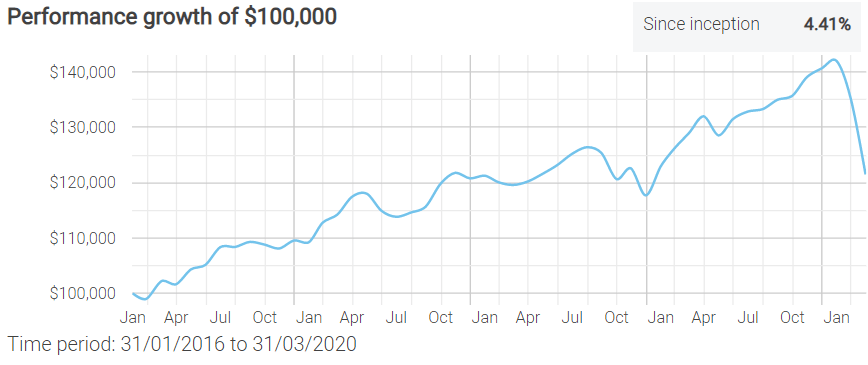

Long-Term Growth Portfolio:

If you are more inclined towards the growth of your investment but you can also bear to tolerate more significant risk to your capital, this portfolio can offer you the chance to capitalize on the market movement with some ups and downs.

Growth since inception: 4.41% (per annum)

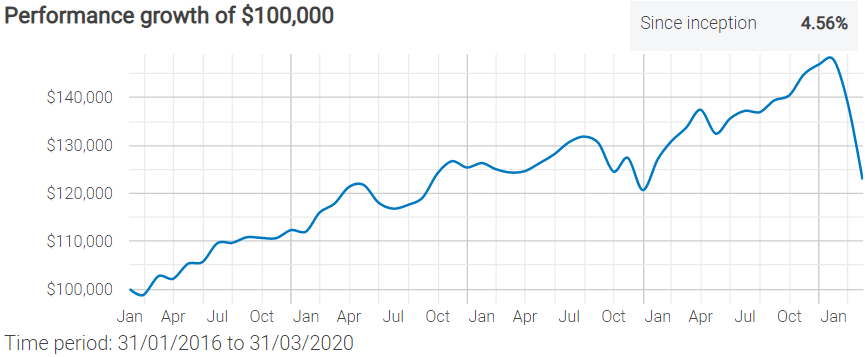

Equity Growth Portfolio:

By far, this is the riskiest option you can go for when it comes to BMO SmartFolio portfolios. It has the most substantial potential for growth and the risk to reflect it.

Growth since inception: 4.56% (per annum)

While the riskier options might seem more attractive in terms of returns, you also have to remember that they primarily consist of equities. The more equities that make your portfolio, the more substantial the risk to your capital.

Related Reading: Wealthsimple Review, Questrade Review

BMO SmartFolio Fees

BMO SmartFolio Management Fees

The BMO SmartFolio is a robo-advisor with relatively higher fees than its peers. Like many others, its fee structure has a tier-based system that depends on the balance in your account. The minimum amount you need to invest in BMO SmartFolios is $1,000, and its pricing begins from there.

-

First $100,000 0.70% per year

-

Next $150,000 0.60% per year

-

Next $250,000 0.50% per year

-

$500,000 and above 0.40% per year

If the balance within your investment account with BMO SmartFolio falls in any of these ranges, the robo-advisor will charge you with the corresponding rate. I’ll give you an example to help you understand how it works better.

For Example: If you have an investment of total $275,000, your annual fee would be $1,725. Here’s a breakdown:

- 0.7% for the first $100,000 = $700

- 0.6% for the next $150,000 = $900

- 0.5% for the remaining $25,000 = $125

The total charge based on this tier system that BMO SmartFolio uses will come around to 0.62%

The more substantial your investment will be, the lower fees this robo-advisor will charge you. However, the fees will always be slightly higher than its lowest charge of 0.40%.

Management Expense Ratio (MER)

In addition to its already high tier-based fee structure, standard MERs apply to underlying ETFs in every portfolio. Unlike most online investment management services, BMO is less open about these fees. However, BMO SmartFolio states that its MER will likely be a weighted average within the range of 0.25% to 0.35% of the value of your SmartFolio account.

Transaction Fees

If you transfer your account from BMO to another financial institution, the platform applies a $135 fee for non-registered accounts and up to $100 for registered accounts. The TFSA and RRIF are excluded from these fees. If you request a paper statement, BMO charges you $15 per statement.

I will give you another example of the BMO SmartFolio fee, including its MER.

For Example: If you have an investment of total $150,000, your annual fee would be $1,450. Here’s a breakdown:

- 0.7% for the first $100,000 = $700

- 0.6% for the remaining $50,000 = $300

- Total Management fee = $1,000

Using an ETF MER of an average 0.30%, you will pay an additional $450, bringing your total up tp $1,450.

The BMO Guarantee

Perhaps the most substantial advantage of BMO SmartFolio is the financial institution's reputation, which backs the robo-advisor. Seeing a name that you are familiar with can give you a sense of reassurance for your capital. BMO is among the Big Five Banks of Canada, with over $880 billion in assets as of January 31, 2020, and it has more than 900 branches across the country.

Human Portfolio Managers

BMO SmartFolio differs from other robo-advisor products you can use in how it manages the ETF portfolios. BMO has a substantially higher degree of human touch behind the scenes than other options you can consider. BMO’s website states that it has a team of 17 professionals with over 300 years of combined experience in the world of finance.

For many investors, this is a benefit. This feature is beneficial if you do not trust mathematic algorithms and rely more on human expertise. However, robo-advisors generally are more popular due to reduced human intervention. Some investors might feel more inclined to trust algorithms without human error being a factor.

Family Account Links to Lower Fees

If several people in your family invest in the BMO SmartFolio, you can link the accounts together and benefit from lower fees. This might not bring your annual fees lower than most other robo-advisors, but it can substantially lower your cost of using the service if you are in a higher bracket.

For Example: If you and your spouse each invest $60,000 in separate accounts with BMO SmartFolio, you can link your accounts for a total investment of $120,000.

This means the first $100,000 will be charged with 0.70%, and the $20,000 will be charged with a lower fee of 0.60% based on its fee structure.

Is BMO SmartFolio Safe and Legit?

Safety is implied when you use a robo-advisor product offered by the oldest bank in the country. Standard high-level encryption and 2-Factor Authorization are expected security measures available.

Additionally, investors with BMO SmartFolio are protected under the Canadian Investor Protection Fund (CIPF) regulated by the Investment Industry Regulatory Organization of Canada (IIROC).

BMO SmartFolio is also registered as a fiduciary. It means that the advisors for BMO SmartFolio do not work for commissions. The professionals have to keep only your best interests in mind, not their own.

Alternatives

When I think of alternatives to BMO SmartFolio, several robo-advisors come to mind, including Wealthsimple, Questrade, and Tangerine.

BMO SmartFolio vs. Wealthsimple

Wealthsimple is the most popular robo-advisor in Canada for several reasons. Regarding differences with BMO SmartFolio, the most substantial difference is that Wealthsimple has a simple fee structure.

Instead of varying fees on the first $100,000 and the next $150,000 like with BMO, Wealthsimple relies on straightforward fees. The corresponding fee will apply to the entire amount if your account balance is within a certain range.

Wealthsimple also offers investors Socially Responsible Investment (SRI) options and is a true robo-advisor with minimal human intervention compared to BMO SmartFolio.

You can learn more about this robo-advisor in my Wealthsimple review.

BMO SmartFolio vs. Questwealth

Questwealth is another substantial product in the robo-advisor market in Canada brought to you by Questrade. It offers investors some of the lowest fees among its peers despite having actively managed portfolios. Questrade also has a team working for you behind the scenes to manage your ETF portfolio.

Questrade has a more straightforward fee structure compared to BMO SmartFolio. It offers SRI options and tax-loss harvesting. While Questrade also has a minimum of $1,000, you can keep adding small amounts to the account until you hit $1,000 so the robo-advisor can begin investing your capital.

You can find out more about Questwealth in my Questwealth review.

BMO SmartFolio vs. Tangerine

Tangerine is a solely online bank that offers several savings accounts, checking accounts, and mortgage products. Tangerine offers several pre-designed portfolios based on various risk tolerance levels and investment goals. While most robo-advisors use ETFs to create portfolios, Tangerine uses its in-house mutual funds.

Unlike BMO SmartFolio and other robo-advisors, Tangerine does not offer a robo-advisor product. It is a digital bank with investment mutual funds that are designed in a manner to robo-advisors that investors can use to purchase globally diversified funds.

| BMO SmartFolio | Wealthsimple | Questwealth | Tangerine | |

|---|---|---|---|---|

| Management Fees | 0.40%-0.70% per year | 0.40%-0.50% per year | 0.20%-0.25% per year | 01.07% |

| MER | 0.25% - 0.35% | Around 0.2% | 0.11%-0.23% | - |

| Minimum Balance | $1,000 | None | $1,000 | $10 |

Final Verdict on BMO Smartfolio

BMO SmartFolio offers you the advantage of a big-name backer and actively managed portfolios with fees lower than most Canadian mutual funds. It guarantees a reputable institution and human investment managers if you don’t trust your capital with mathematical algorithms.

However, its fee structure is complex and substantially higher than most online investment managers. It also lacks several key features like SRI and tax-loss harvesting.

You can check out BMO SmartFolio here. As for our verdict, BMO SmartFolio does not get the Wealth Awesome recommendation mainly due to its fees, but if you need a big bank for peace of mind, it’s a decent option.

An alternative to BMO's robo advisor is its all-in-one ETF portfolios.

If you’re looking for lower fees for your robo-advisor, check out this Questwealth review. If you’re looking for a robo-advisor with a great overall product offering, check out this Wealthsimple review.

Best next step

Keep exploring this topic

If you want to go deeper, these are the most useful follow-up pages and tools for this topic.

Stocks tool

Check Canadian stock movers

See the latest TSX and TSXV winners and losers before digging deeper into a sector.

Research hub

Browse Canadian stock research

Use the stock section to jump from a theme article into individual company pages.

Diversification

Compare stocks with ETF options

If you want exposure to a theme without single-stock risk, screen matching ETFs instead.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.