CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

Looking to invest using a robo-advisor and want to learn more about Questwealth? You've come to the right place.

There are a plethora of robo-advisor products available in Canada. Choosing the right one can be a challenge with so many options.

I have used many robo-advisors myself in the past, and I’ve extensively researched and ranked the top Canadian ones.

My Questwealth review will hopefully help you understand whether this robo-advisor is suitable for you.

[affiliatable id='26703']

Pros

Cons

What is Questwealth?

Questwealth is the robo-advisor product that Questrade manages. Questrade is an investment management firm based in Canada that started in 1999. Questrade has over $30 billion in assets under management and has over 250,000 new accounts opened each year.

Questwealth Portfolio IQ was rebranded to simply Questwealth Portfolios in November 2018. It offers Canadians a platform to invest in a actively managed portfolio of ETFs at a very low cost.

Questwealth can be ideal for investors who are not ready for DIY investing and want to enjoy low fees for their wealth management services.

Questwealth Fees

Questwealth offers the most competitive fee structure you will see in the market for robo-advisors in Canada. That is one of the main qualities that drew me to it.

The charges for using the robo-advisor and the management expense ratio (MER) for the ETFs that its portfolios consist of are attractive:

Management Fees:

| Managed Amount | Management Fee |

|---|---|

| $1,000 - $99,999 | 0.25% |

| $100,000 and above | 0.20% |

ETF MER:

| Portfolio Type | MER Fee Range |

|---|---|

| Normal portfolios | 0.17% to 0.22% |

| Socially Responsible Investing (SRI) Portfolios | 0.21% to 0.35% |

Questwealth Fees vs. Industry Average:

| Robo-Advisor | Total Fees for Normal Portfolios (Management + MER) |

|---|---|

| Questwealth | 0.37% - 0.47% / Year |

| Industry Average | 0.55% - 0.7% / Year |

Questwealth's fees are exceptionally low compared to the rest of Canada's robo-advisors.

**Fee Savings Example with Questwealth:

**If you invest $100,000 with Questwealth (non-SRI portfolio), expect to pay all-in fees of around $370 - $470 per year. For most of the other robo-advisors in Canada expect to pay around $550 - $700 per year. Those hundreds of dollars will add up over the years.

Questwealth does not charge any hidden fees. There are no fees for trading, fund transfers, or for making regular contributions. The lower fees allow you to save up each year gradually.

Saving a few dollars each year might not seem attractive at first. However, the savings accumulate over time to help you a significant sum over time.

The MER can reach up to as high as 0.35% for an SRI portfolio, and these fees are mentioned in the portfolio section when you are selecting the type at Questwealth.

Questwealth Active Management Approach

Most robo-advisors in Canada passively manage your investments, meaning they don't actively trade the ETFs inside your portfolio.

Questwealth Portfolios takes a different approach and actively manages your investments. It employs a team of expert portfolio managers who keep tabs on movements in the market.

Using their experience and research, the portfolio managers at Questwealth rebalance your portfolio to mitigate losses and seek opportunities to boost your returns.

Actively managed portfolios typically mean higher management fees, which often leads to market underperformance in the long term. That is not the case for the fees with Questwealth.

The company can impressively offer active management at a much lower fee than its passively managed competitors. This doesn't guarantee Questwealth will outperform its passively managed peers, but it's a good start.

Questwealth Portfolios and ETFs Offered

Currently, the robo-advisor offers five standard portfolios you can consider:

-

Aggressive: Aggressive portfolios are designed for investors with a high tolerance for risk. The portfolio consists entirely of equity.

-

Growth: This portfolio is made for investors with a medium to high-risk tolerance. It holds 20% in fixed-income ETFs and 80% in equity.

-

Balanced: Designed for investors with medium tolerance to risk, it holds 40% fixed-income ETFs and 60% equity.

-

Income: Designed for investors with a low to medium risk tolerance. The portfolio consists of 40% equity and 60% fixed-income ETFs.

-

Conservative: For investors who want to minimize the risk to their capital. It contains only 20% in equity and 80% in fixed-income ETFs.

Each Questwealth portfolio available comprises a combination of the following low-cost ETFs:

-

iShares Core Canadian Short-Term Bond Index ETF

-

iShares Core Canadian Universe Bond Index ETF

-

iShares Core MSCI EAFE IMI Index ETF (CAD-Hedged)

-

iShares Global REIT ETF

-

SPDR Portfolio Emerging Market ETF

-

WisdomTree Canada Quality Dividend Growth Index ETF

-

SPDR Portfolio Total Stock Market ETF

The portfolios consist of a varying combination of these ETFs. Each portfolio can have five to seven of these ETFs to create the ideal ratio of equity and fixed-income ETFs to reflect the risk and reward for the corresponding portfolio.

Socially Responsible Investing (SRI)

A feature that I like about Questwealth is its offering of Socially Responsible Investing (SRI) portfolios. SRI portfolios allow investors to invest their capital in ETFs that align with their moral values and beliefs.

SRI portfolios consist of social and corporate governance ETFs, low-carbon ETFs, and cleantech ETFs. These also include ETFs of companies with excellent track records for labour practices, renewable energy companies, and other socially and environmentally responsible ETFs.

Questwealth combines these ETFs to create five types of SRI portfolios that are suitable for investors with varying risk tolerance. These include:

-

Aggressive Growth SRI

-

Growth SRI

-

Balanced SRI

-

Income SRI

-

Conservative SRI

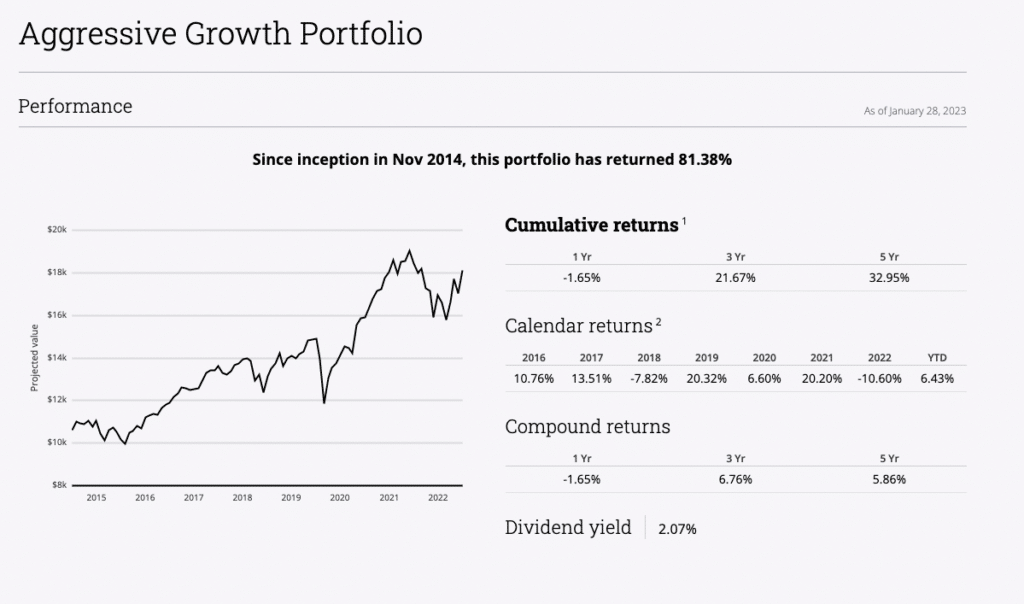

Questwealth Performance

Questwealth offers you transparency when it comes to the performance of its portfolios.

It publishes the performance of its ETF portfolios on its website. Here is the performance of its Aggressive Portfolio as of Jan 28, 2023:

Questwealth Dividend Yield

Questwealth offers a dividend for each of its portfolios. As typical of most robo-advisors, it isn't a huge dividend, but at least it's something. For example, as of Jan 28, 2023, the Aggressive Portfolio offers a 2.07% dividend yield.

Questwealth Accounts Offered

Questwealth offers Canadians the following account types they can use with the platform:

-

Tax-Free Savings Account (TFSA)

-

Registered Retirement Savings Plan (RRSP)

-

Spousal RRSP

-

Locked-in RRSP

-

Locked-in Retirement Account (LIRA)

-

Registered Education Savings Plan (RESP)

-

Registered Retirement Income Fund (RRIF)

-

Life Income Fund (LIF)

Most Popular Accounts

1. Questwealth TFSA

-

Easy access to your capital

-

Save for short- and long-term financial goals

-

Tax-free growth of wealth

-

Tax-free dividend and capital gain income

2. Questwealth RRSP

-

Save for long-term retirement goals

-

Set up regular contributions

-

Save more by starting early

-

Leverage tax deductions on annual contributions

-

Set yourself up for a comfortable life in retirement

3. Questwealth RESP

-

Enjoy government grants

-

Tax-deferred growth of capital

-

Tax-sheltered environment for gains

-

Withdraw with taxes on a lower tax bracket

-

Boost your child’s chances for better education

Questwealth Customer Service

Questwealth Portfolios operates as a solely online robo-advisor service. It means you cannot go into their office if you want to talk to a financial expert or advisor from the company face-to-face.

The contact with Questwealth is limited to social media, chat, email, and telephone. I have contacted Questwealth a few times that I’ve been using their service to get more information about the ETF portfolios.

I don't usually feel the need to call or email them. I contact Questwealth through chat and found that they are prompt and helpful. Getting on the phone with them is not hard either if customers want that human element.

Questwealth also has a useful self-help function that provides information on a wide array of topics. Questrade, its parent company, received the DALBAR Seal for Service Excellence.

It is a prestigious award that acknowledges leaders within the financial services department for excellent performance. Unfortunately, meeting the financial advisors is never a possibility with Questwealth like it is with traditional investment firms or banks, but you can call them for some basic help with things like portfolio selection.

Free Tax-Loss Harvesting

This is a feature available if you choose taxable accounts at Questwealth. Tax-loss harvesting essentially lowers your taxes on investment gains by using any investment losses to offset them.

The portfolio managers at Questwealth use tax-loss harvesting to lower the capital gains tax in cash accounts – and they do it without any additional fees.

Automatic Rebalancing

Once you have selected the portfolio and Questwealth invests your capital, you can simply “set it and forget it” without worrying about making changes manually.

The financial experts at Questwealth constantly monitor the mixture of assets in each portfolio. They adjust to the changing market conditions to maximize profits and minimize the risks to your capital.

Is Questwealth Safe and Legit?

Questrade is a member of the Canadian Investor Protection Fund (CIPF). It means that your account with Questwealth Portfolios is adequately insured. In case Questwealth ever goes bankrupt, your capital is protected up to a value of $1 million.

Questrade also offers free private insurance of an additional $10 million. The company is also a member of the Investment Industry Regulatory Organization of Canada (IIROC). You can consider your investment quite safe with Questwealth Portfolios.

User Reviews for Questwealth

If you search Reddit for reviews from customers who have used Questwealth, there are plenty of happy customers out there.

I scoured through the internet to find reviews from customers who have been using Questwealth to see what they have to say so you can have an unbiased look at Questwealth.

Most people have good things to say about their experience of using Questwealth. However, I do share the concerns about an actively managed portfolio compared to a passively managed portfolio and the results it yields:

Bad Review

Questwealth Alternatives

Questwealth vs. Wealthsimple

Wealthsimple is the most popular robo-advisor product in Canada. Wealthsimple enjoys its reputation due to an excellent combination of features, benefits, and low fees for clients. Questwealth also offers excellent features and benefits.

However, Questwealth offers substantially lower fees than Wealthsimple, which is an extremely important benefit. In the Wealthsimple vs. Questwealth comparison, Wealthsimple beats Questwealth regarding minimum balance. Questwealth has a minimum balance of $1,000, while there is no minimum balance limit with Wealthsimple.

Read my full comparison of Wealthsimple vs Questrade here.

Questwealth vs. Vanguard

Vanguard is known for its pioneering presence in the world of low-cost index investing. Note that Vanguard does not offer a traditional robo-advisor product in Canada.

It offers a hybrid solution called Vanguard Personal Advisor (for the U.S. only). It uses a portfolio selection that consists of Vanguard’s line of low-cost ETFs.

Vanguard is currently moving forward with an online-only robo-advisor called Digital Advisor (again, in the U.S. only, so the comparison to Questwealth is not valid).

Questwealth vs. Self-Directed Investing

Self-directed investing is another alternative you can choose. If you think you have a knack for investing, understand how ETFs work, and understand how different funds can have varying risks, you can create your portfolio.

Questrade also operates as an online brokerage that allows you to trade and create your own investment portfolio. The discount broker enables you to solve the problem of paying too much for investing, which could be ideal for a DIY approach to investing.

You can learn more about Questrade in my Questrade Review.

Questwealth Verdict

If you are searching for a robo-advisor in Canada that charges you an extremely low fee and is actively managed, Questwealth could be the right fit for you.

I think Questwealth is a fantastic robo-advisor that can help you achieve a variety of investment goals, from aggressive growth to a more conservative approach. It also offers most accounts that Canadians can ask for.

After doing this Questwealth review, it gets a big thumbs up from Wealth Awesome.

If you want to try it out, you can get $10,000 managed free by Questwealth Portfolios here.

Best next step

Keep exploring this topic

If you want to go deeper, these are the most useful follow-up pages and tools for this topic.

Stocks tool

Check Canadian stock movers

See the latest TSX and TSXV winners and losers before digging deeper into a sector.

Research hub

Browse Canadian stock research

Use the stock section to jump from a theme article into individual company pages.

Diversification

Compare stocks with ETF options

If you want exposure to a theme without single-stock risk, screen matching ETFs instead.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.