CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

Contribution Margin Ratio

The Contribution Margin Ratio is a pivotal financial metric that assesses a company's profitability by determining how much of each sales dollar contributes to covering fixed costs and generating profit. It provides valuable insights into the profitability of individual products or services and helps in making informed business decisions.

Advertisement

Why the Ratio is Important

The Contribution Margin Ratio is crucial for businesses to understand because it highlights the proportion of sales revenue that remains after variable costs are deducted. This leftover revenue is what covers fixed costs and contributes to profits. A higher ratio means more revenue is available to cover fixed costs, enhance profitability, and support strategic decisions regarding pricing, production levels, and cost management.

What a Typical Contribution Margin Ratio Includes

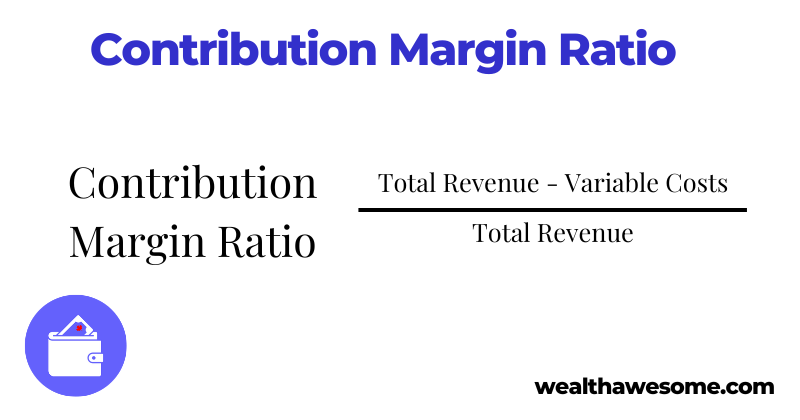

The formula for the Contribution Margin Ratio is: Contribution Margin Ratio=Sales Revenue - Variable CostsSales Revenue\text{Contribution Margin Ratio} = \frac{\text{Sales Revenue - Variable Costs}}{\text{Sales Revenue}} This ratio is expressed as a percentage, showing what portion of each dollar of sales contributes to covering fixed costs after variable costs are paid. The simplicity of this calculation allows managers to quickly gauge the impact of sales and costs on profitability.

Examples

-

Example of a High Contribution Margin Ratio:

-

Consider a software company that has very low variable costs but high sales revenue. The company's Contribution Margin Ratio might be significantly high, indicating that a large portion of each sales dollar contributes to profit.

-

This high ratio not only shows efficient cost management but also provides the company with substantial leeway to handle fixed expenses and invest in growth opportunities.

-

-

Example of a Low Contribution Margin Ratio:

-

A typical example could be a restaurant where variable costs like ingredients and labor consume a large portion of sales revenue. If this restaurant has a low Contribution Margin Ratio, it indicates that less revenue is left over to cover fixed costs and profit.

-

This scenario necessitates careful management of variable costs and pricing strategies to ensure sustainability and profitability.

-

Further Insights

-

Adjusting Costs: Businesses can influence their Contribution Margin Ratio by managing variable costs or adjusting pricing strategies. For instance, reducing direct material costs or optimizing operational efficiencies can improve the ratio.

-

Industry Variances: The typical Contribution Margin Ratio can vary widely among different industries due to inherent differences in cost structures. For example, tech companies generally have higher ratios than manufacturing firms due to lower variable costs.

Frequently Asked Questions about the Contribution Margin Ratio

What is the contribution margin ratio formula?

The formula for the Contribution Margin Ratio is: Contribution Margin Ratio=Sales Revenue - Variable CostsSales Revenue\text{Contribution Margin Ratio} = \frac{\text{Sales Revenue - Variable Costs}}{\text{Sales Revenue}}Contribution Margin Ratio=Sales RevenueSales Revenue - Variable Costs This calculation shows what percentage of sales revenue is left over after variable costs have been subtracted, indicating how much contributes towards fixed costs and profits.

Advertisement

What is a healthy contribution margin ratio?

A healthy Contribution Margin Ratio varies by industry due to differing cost structures and pricing strategies. Generally, a higher ratio indicates better performance, as it means more revenue is available to cover fixed costs and profit. Ratios of 30% or higher are often considered healthy, especially in industries with high variable costs.

What does a contribution margin of 40% mean?

A contribution margin of 40% means that 40% of each dollar of sales contributes towards covering fixed costs and generating profit, after variable costs have been paid. This indicates that for every dollar generated in sales, 40 cents is available to cover fixed costs and contribute to net profit, which is typically a strong position for a company.

What is the formula for CM ratio with example?

The formula for the Contribution Margin Ratio, as mentioned, is: Contribution Margin Ratio=Sales Revenue - Variable CostsSales Revenue\text{Contribution Margin Ratio} = \frac{\text{Sales Revenue - Variable Costs}}{\text{Sales Revenue}}Contribution Margin Ratio=Sales RevenueSales Revenue - Variable Costs For example, if a company has sales revenue of $100,000 and variable costs of $60,000, the contribution margin ratio would be calculated as: Contribution Margin Ratio=$100,000−$60,000$100,000=0.4 or 40%\text{Contribution Margin Ratio} = \frac{\$100,000 - \$60,000}{\$100,000} = 0.4 \text{ or } 40\%Contribution Margin Ratio=$100,000$100,000−$60,000=0.4 or 40% This means 40% of the sales revenue remains after variable costs are covered, which can be used to pay fixed costs and contribute to profits.

Thank you for providing the links. Here's a draft of the section you can add to the bottom of each ratio-related article to guide readers to explore more on financial ratios:

Explore More Financial Ratios

Understanding different financial ratios can significantly enhance your insights into business performance and investment decisions. Explore our detailed articles on various financial ratios to deepen your knowledge and improve your analytical skills:

Discover how each ratio can provide unique perspectives on financial health and strategic planning to enhance your portfolio or business strategy!

Best next step

Keep exploring this topic

If you want to go deeper, these are the most useful follow-up pages and tools for this topic.

Tax planning

Estimate your take-home pay first

Use the tax calculator before choosing software, moving cash, or making a savings plan.

Banking next step

Compare high-interest savings rates

Move from banking basics into current cash rates and safer places to park your money.

Savings tool

See how compound growth adds up

Turn a practical money question into a long-term plan with a quick growth projection.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Qayyum Rajan, CFA

Qayyum is the CEO of Wealth Awesome, a leading Canadian personal finance publication. As a CFA charterholder with extensive experience in fintech, data science, and quantitative finance, he brings a unique analytical perspective to investing and wealth management.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.