CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

Why the Ratio is Important

The Sortino Ratio is a modification of the Sharpe Ratio that differentiates harmful volatility from overall volatility by focusing only on the downside deviation. It is important because it provides investors with a measure of the risk-adjusted return that considers only the risk of negative returns, which is more relevant to many investors. This ratio helps in assessing the performance of investments that have asymmetrical distributions of returns or that are skewed.

Advertisement

What a Typical Sortino Ratio Includes

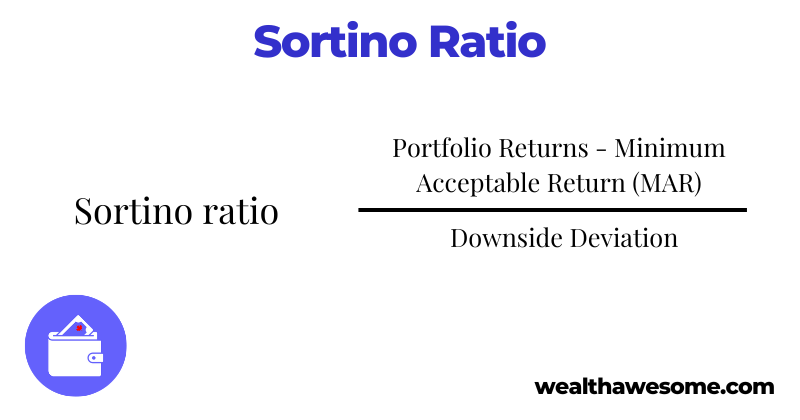

The Sortino Ratio is calculated using the formula: Sortino Ratio=Portfolio Returns - Minimum Acceptable Return (MAR)Downside Deviation\text{Sortino Ratio} = \frac{\text{Portfolio Returns - Minimum Acceptable Return (MAR)}}{\text{Downside Deviation}} The Minimum Acceptable Return (MAR) is the return threshold below which is considered undesirable by the investor. Downside Deviation is a measure of the variability of returns below the MAR, giving a view of the risk of negative returns.

Examples

-

Example of a High Sortino Ratio:

- Consider a mutual fund that targets conservative investors, focusing on steady income with minimal negative variation. If this fund has consistently generated returns above the MAR with very few negative returns, it would exhibit a high Sortino Ratio, indicating efficient performance with respect to the downside risk.

-

Example of a Low Sortino Ratio:

- An aggressive hedge fund might aim for high returns but experiences significant drops during market downturns. If these negative returns frequently fall below the MAR, it results in a low Sortino Ratio, highlighting greater vulnerability to downside risks.

Further Insights

-

Discuss the implications of using the Sortino Ratio compared to other risk-adjusted measures like the Sharpe Ratio, especially for portfolios prone to negative skewness or where the timing of losses is crucial.

-

Explain how investors can use the Sortino Ratio to compare the performance of portfolios or funds with similar objectives but differing risk profiles.

Frequently Asked Questions about the Sortino Ratio

What is a good Sortino Ratio?

A good Sortino Ratio depends on the context of the investment and the specific objectives of the investor. Generally, a higher Sortino Ratio is better as it indicates a greater return per unit of downside risk. Ratios above 2 are often considered excellent, showing that the investment has achieved high returns while managing downside risks effectively. However, the acceptable level can vary depending on the market conditions and the type of investments being analyzed.

Sortino vs Sharpe Ratio: What's the difference?

The Sortino Ratio and the Sharpe Ratio are both risk-adjusted performance measures, but they differ in how they define risk:

-

Sharpe Ratio measures the excess return per unit of total volatility (standard deviation of portfolio returns), considering both upside and downside volatility. Sharpe Ratio=Portfolio Return - Risk-Free RateStandard Deviation of Portfolio Return\text{Sharpe Ratio} = \frac{\text{Portfolio Return - Risk-Free Rate}}{\text{Standard Deviation of Portfolio Return}}

-

Sortino Ratio focuses only on downside risk (the standard deviation of negative portfolio returns) rather than total volatility. It specifically measures the excess return over the minimum acceptable return (MAR) per unit of downside deviation.

This focus makes the Sortino Ratio particularly useful for portfolios expected to avoid downside risks or for investors who are more concerned about negative fluctuations than positive ones.

How is Sortino Ratio calculated?

Advertisement

The Sortino Ratio is calculated with the following formula: Sortino Ratio=Portfolio Returns - Minimum Acceptable Return (MAR)Downside Deviation\text{Sortino Ratio} = \frac{\text{Portfolio Returns - Minimum Acceptable Return (MAR)}}{\text{Downside Deviation}}

-

Portfolio Returns: The actual return of the portfolio.

-

Minimum Acceptable Return (MAR): The investor's minimum threshold for acceptable returns, below which is considered undesirable.

-

Downside Deviation: The root mean square of returns falling below the MAR, focusing only on negative volatility.

What is the main disadvantage of the Sortino Ratio?

The main disadvantage of the Sortino Ratio is its dependency on the correct specification of the Minimum Acceptable Return (MAR). Choosing an inappropriate MAR can lead to misleading results. For instance, setting the MAR too low may make the investment appear less risky than it actually is. Additionally, the Sortino Ratio only considers downside risk, which might overlook other aspects of volatility that could be important to certain investors, particularly those who might also be concerned about the volatility of positive returns.

Explore More Financial Ratios

Understanding different financial ratios can significantly enhance your insights into business performance and investment decisions. Explore our detailed articles on various financial ratios to deepen your knowledge and improve your analytical skills:

Discover how each ratio can provide unique perspectives on financial health and strategic planning to enhance your portfolio or business strategy!

Best next step

Keep exploring this topic

If you want to go deeper, these are the most useful follow-up pages and tools for this topic.

Tax planning

Estimate your take-home pay first

Use the tax calculator before choosing software, moving cash, or making a savings plan.

Banking next step

Compare high-interest savings rates

Move from banking basics into current cash rates and safer places to park your money.

Savings tool

See how compound growth adds up

Turn a practical money question into a long-term plan with a quick growth projection.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Qayyum Rajan, CFA

Qayyum is the CEO of Wealth Awesome, a leading Canadian personal finance publication. As a CFA charterholder with extensive experience in fintech, data science, and quantitative finance, he brings a unique analytical perspective to investing and wealth management.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.