CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

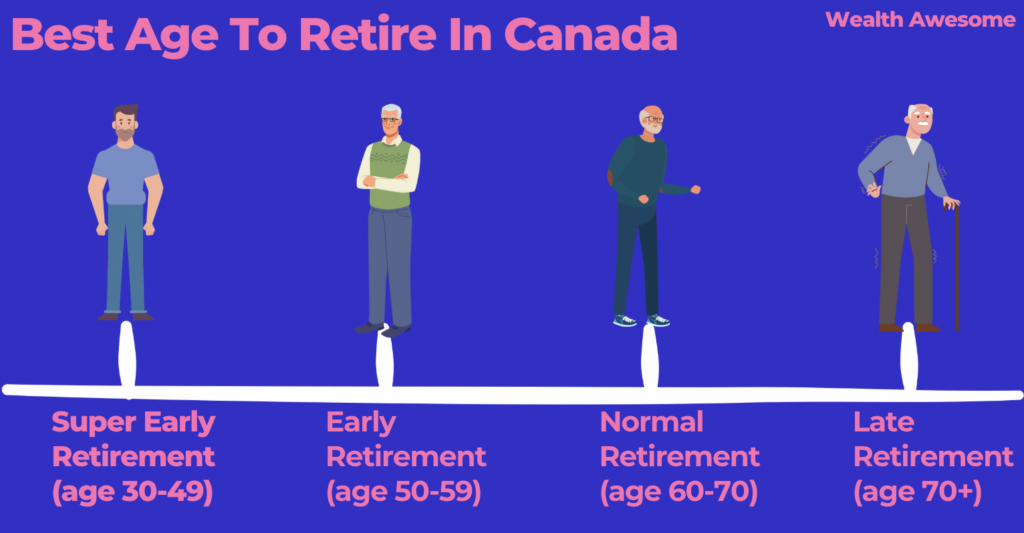

Looking at retiring early, perhaps at the age of 55 in Canada? You'll be ahead of many other Canadians if you can reach this goal.

46% of Canadians expect to retire between 60 and 70, while the average retirement age was 64 years old, according to this survey. My parents also retired in this age range, but I’ve always felt that it is too old an age to retire.

Retiring at a very old age is not an ideal scenario, considering that you get to enjoy only a few years of retirement in exchange for decades of hard work.

I know that, like me, many people are also planning to retire earlier. Fortunately, it is possible to retire early, provided that you have a well-formulated retirement plan.

Many people consider 55 to be an ideal age to retire. If you’re wondering how to retire at 55 in Canada, this guide outlines the steps and mindset shifts needed to make early retirement in Canada at 55 a reality.

Steps To Achieve Your Financial Goals For Retirement By 55

1. Understand Your Financial Needs for Retirement

By determining how much you'll require annually post-retirement, you set a clear financial target. This involves accounting for basic living expenses, potential health care costs, leisure activities, travel ambitions, and any existing or anticipated debts.

Remember, inflation and changing costs of living can significantly impact these numbers over time.

Note that this section is crucial, and I go into more detail on this after these tips.

2. Leverage the Power of Compound Interest

The earlier you begin saving, the more time your investments have to grow. Compound interest, where interest earns interest, becomes more powerful over extended periods.

So, by starting your retirement savings plan early, you allow your investments to work harder for you.

3. Optimize Investment Vehicles: TFSA and RRSP

Canada offers unique tax-efficient investment tools like the Tax-Free Savings Account (TFSA) and the Registered Retirement Savings Plan (RRSP). Both can be instrumental in building your retirement fund.

While RRSP contributions provide a tax deduction, TFSA allows for tax-free growth and withdrawal.

Related Reading: TFSA vs RRSP 2023: Which One Is Right For You?

4. Become Debt-Free Before Retirement

Aim to clear all significant liabilities, like mortgages and car loans, before you retire. Being debt-free minimizes financial stress and reduces the monthly expenditures you'll face during your retirement years.

5. Maximize Employer Pension Plans

If your workplace offers a pension plan, especially a defined benefit scheme, it can be a substantial pillar for your retirement strategy. Engage fully, understand its nuances, and ensure you're contributing enough to optimize this benefit.

6. Stay Updated on Tax Implications

Being aware of the tax ramifications related to your retirement savings and withdrawals can save you a significant amount in the long run. For instance, knowing the tax rules around RRSP withdrawals can help in the strategic planning of your retirement income.

7. Access Government Programs Strategically

Canada's CPP and OAS are essential facets of retiring at 55 in Canada and play a critical role in planning your income for the long term. While these programs have age restrictions, knowing when to initiate them can help maximize your retirement benefits. For instance, delaying the CPP or OAS can lead to a higher monthly payout.

Related Reading: When to Apply For CPP? Age 60, 65, or 70?

8. Establish Passive Income Streams

Diversifying your income sources, especially with passive ones, can provide added financial security. Investments like rental real estate, dividend-paying stocks, or online ventures can offer regular income without the need for daily active involvement.

9. Prioritize Your Health

Maintaining good health is not just about the quality of life; it's also a financial strategy. Regular exercise, a balanced diet, and preventive health care can help you avoid hefty medical bills and enjoy your retirement years to the fullest.

10. Earn More Money In Your Career

Invest in continuous education to stay relevant and gain a competitive edge. Seek mentorship to navigate your career trajectory more effectively and specialize in high-demand areas to enhance your market value.

Actively network, both online and through professional associations, to uncover higher-paying opportunities.

This is a key point - Don't shy away from negotiating your salary by highlighting your achievements and understanding market rates. Consider strategic job hopping for significant pay increases and try to aim for leadership roles which generally command higher salaries.

How Much Money Do You Need to Retire at 55 in Canada?

The amount of money you need to retire at 55 in Canada depends on your lifestyle, expected retirement length, and how well you’ve optimized tax-free and passive income streams. This section will help answer the question many people ask: how much money do I need to retire at 55 in Canada?

Here's a step-by-step guide to help you determine how much you might need:

1. Estimate Annual Living Expenses

To begin, calculate your anticipated yearly expenses in retirement. This includes:

-

Housing (rent, mortgage, property taxes, maintenance)

-

Utilities

-

Groceries

-

Health care (not covered by provincial health plans)

-

Transportation (car maintenance, insurance, public transport)

-

Leisure activities and travel

-

Any other personal expenses (like gifts, donations, etc.)

2. Factor in Inflation

Over time, the cost of living will rise due to inflation. Historically, the average inflation rate in Canada has hovered around 2%. Therefore, an expense of $50,000 today might be significantly higher 20 years from now.

3. Determine the Number of Years in Retirement

If you retire at 55, and the average life expectancy is around 82 years in Canada, you're looking at potentially 27+ years in retirement (or more, given medical advancements).

4. Account for Government and Other Pension Benefits

Even if you retire at 55, some government benefits like the Canada Pension Plan (CPP) and Old Age Security (OAS) don't kick in until later:

-

CPP can be taken as early as age 60 (though at a reduced rate) or as late as 70 (with an increased rate).

-

OAS starts at age 65 for those who qualify.

Subtract anticipated yearly amounts from these sources from your annual living expenses.

5. Consider Other Income Sources

Do you expect to receive income from other sources during retirement, such as rental properties, part-time work, or dividends from investments? Deduct these amounts from your yearly expenses.

6. Calculate the Total Amount Needed

Multiply your adjusted annual living expenses (after accounting for pensions and other income) by the number of years you expect to be retired.

For example, if you need $50,000 a year for 27 years, that's $1,350,000. However, remember that due to the effects of inflation, you might need a lot more than this over time.

7. Account for Return on Investments

Your retirement savings will likely be invested, earning a return over time. Therefore, you might not need the entire sum on the day you retire. A financial advisor can help you forecast the growth of your investments versus your withdrawals.

8. Plan for Unexpected Costs

It's always wise to have a buffer for unforeseen expenses, such as medical emergencies or major repairs.

Use a Rule of Thumb

If you don't want to do all those calculations, a general rule of thumb that some financial planners use is the "25x Rule," which suggests you need 25 times your first year of retirement expenses to retire comfortably. So, if you expect to spend $50,000 in your first year, you'd need approximately $1,250,000 saved by age 55.

FAQs

What are the best investment strategies for retiring at 55 in Canada?

Start by saving and investing early, taking advantage of tax-sheltered accounts such as RRSPs (Registered Retirement Savings Plans) and TFSAs (Tax-Free Savings Accounts).

Diversifying investments across asset classes like stocks, bonds, real estate, and perhaps even alternative investments can help manage risk and provide potential growth.

As the retirement age approaches, gradually shift towards more conservative investments to protect the accumulated wealth.

What are the tax implications of retiring at 55 in Canada?

Retiring at 55 in Canada comes with specific tax considerations. Firstly, if you choose to withdraw from your RRSP before age 71, the withdrawn amount is treated as income and is taxable at your marginal tax rate for the year. Early withdrawal may push you into a higher tax bracket, increasing your tax liability.

Additionally, any investments outside of tax-sheltered accounts may lead to capital gains taxes upon sale. While the principal amount in a TFSA can be withdrawn tax-free, any non-registered investments will have tax implications. Plan your withdrawals strategically, possibly spacing them out to manage the tax hit better.

Can I apply for Canada Pension Plan (CPP) at 55, and how will it affect my retirement income?

You cannot apply for CPP benefits at 55; the earliest age to start receiving CPP is 60. However, starting your CPP payments before the standard age of 65 means a reduction in the monthly benefit amount.

Specifically, your CPP retirement pension will be reduced by 0.6% for each month you receive it before age 65, which translates to a 7.2% reduction per year. By starting at 60, your pension would be 36% less than if you had waited until 65.

Can you retire at 55 in Canada?

Yes, you can retire at 55 in Canada, but it requires careful planning. You won’t have access to government benefits like CPP and OAS until age 60 or 65, so you'll need to rely on savings, TFSAs, RRSPs, pensions, or passive income during the early years of retirement.

What is Freedom 55 in Canada?

Freedom 55 is a term that became popular from a financial marketing campaign and refers to the idea of retiring at 55 with financial security. While it’s an aspirational goal, it's achievable for Canadians who start saving early, live below their means, and invest wisely.

How much do I need to retire at 55 in Ontario?

To retire at 55 in Ontario, you’ll need to factor in higher living costs in urban areas like Toronto versus more affordable towns. A common target is at least $1 to $1.5 million in savings or assets, depending on your lifestyle and whether you have access to employer pensions.

Are there any benefits for seniors 55 and older in Canada?

While most senior benefits begin at 60 or 65, some programs and private discounts are available to Canadians 55 and over. These may include discounts on transportation, insurance, or early pension payouts from certain employer plans.

Conclusion

Learning how to retire at 55 in Canada is not the easiest thing in the world, but you should know that it’s not impossible. It is worthwhile to take the time to formulate a comprehensive retirement plan and adjust your financial practices to achieve those goals.

The real key is to have the discipline to stick to your retirement plan as strictly as possible. Unforeseen circumstances might require you to tweak your plan, but you should reposition your strategy and try your best not to let go of your goal of retiring at 55.

Check out my guide on how much you need to retire if you want to get a more detailed but simplified plan to calculate the amount you will need. Meanwhile, this guide is perfect if you want to learn about retirement income sources you can rely on to earn more money in your golden years.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.