CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

If you’ve ever wondered how CPP is calculated in Canada, you’re among those who are proactively planning for a comfortable retirement.

In 2018, A staggering 90% of Canadians did not have a formal retirement plan, according to CIBC study.

While the CPP alone is likely not enough to fund your retirement, it is an important source of income for most retired Canadians.

Retirement is a huge life change, thus it's important to make sure you're ready to make the most of those golden years.

In this blog post, we’ll take a look at how is CPP calculated in Canada and how you can maximize your benefits.

What is CPP?

The Canada Pension Plan (CPP) is a monthly, taxable benefit that replaces part of your income when you retire.

It is a contributory, earnings-related social insurance program, which means that both employees and employers contribute to the CPP, as do self-employed workers.

It is one of the largest social security programs in Canada and provides retirement, survivors, and disability benefits to millions of Canadians.

The Canada Pension Plan Investment Board (CPPIB) is a crown corporation of the Government of Canada, created in 1997 to manage the assets of the Canada Pension Plan (CPP).

The CPPIB is one of the largest pension fund managers in the world, with net assets of 497.2 billion as of March 2021.

The CPPIB's mandate is to "provide long-term returns that are sufficient to pay current and future benefits from the Canada Pension Plan." The CPPIB does this by investing the contributions to CPP in a broad range of assets, including public equity, private equity, real estate, infrastructure and fixed income securities.

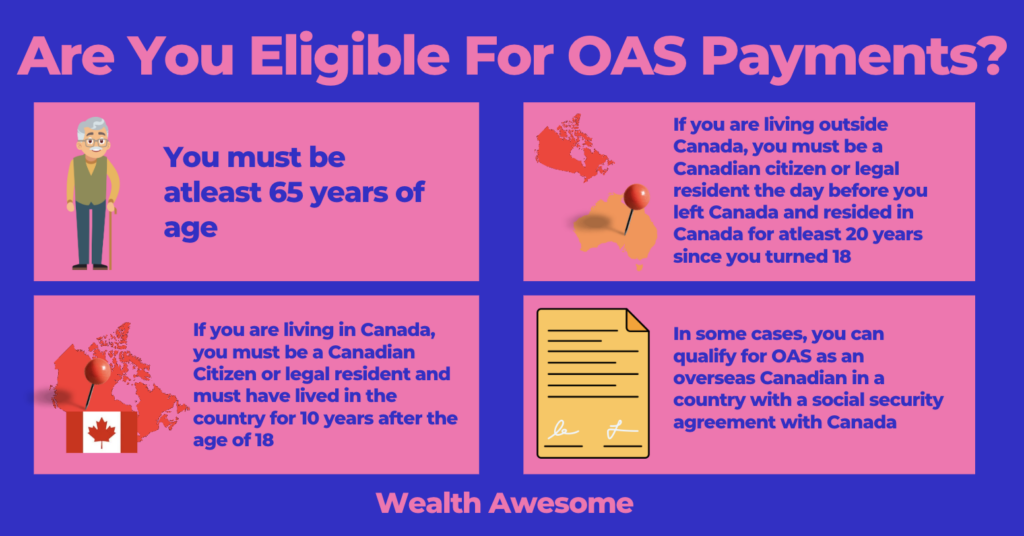

If you qualify, you’ll receive the CPP retirement pension for the rest of your life. To be eligible, you must meet all of the following conditions:

- Be at least 60 years old have made at least one valid contribution to the CPP

Valid contributions refer to work performed in Canada or credits received from a former spouse.

The maximum CPP benefit amount payable at age 65 is $1,364.60 per month (as of January 2025), although the average benefit is $758.32.

Unlike some other government benefits, you don't automatically receive CPP retirement pension payments.

You must apply for them. You can apply for the CPP by filling out an application and mailing it in, or by filling out an application online.

If you're not sure whether or not you're eligible for the CPP, or if you have any other questions about the process, we recommend contacting Service Canada for more information.

How is CPP calculated in Canada?

One of the best ways to make sure you're getting the most out of your CPP contributions is to understand how they're calculated.

In 2025, CPP contributions are based on a two-tier earnings structure introduced under the CPP enhancement.

The first ceiling, called the Year's Maximum Pensionable Earnings (YMPE), is $68,500. The contribution rate up to this ceiling is 11.9%, equally split between employer and employee (5.95% each).

The second ceiling, the Year’s Additional Maximum Pensionable Earnings (YAMPE), is $73,200. An additional 8% contribution applies on income between the YMPE and YAMPE, also split equally between employer and employee (4% each).

Self-employed individuals pay both halves of the applicable rates.

Here’s a step-by-step process to calculate your CPP contribution amounts

-

Determine your total pensionable income, which is your gross pay along with taxable allowances or benefits.

-

Determine your basic exemption amount, which is the basic exemption of $3,500 divided by your pay period, you can use this chart to find it easily.

-

Deduct your basic pay-period exemption amount from your total pensionable income

-

Multiply the result by the contribution rate which is 5.7% (50% split of 11.4% contribution rate)

Here’s an example:

Total pensionable monthly income: $4,000

Basic exemption monthly amount: $291.66

4,000 - 291.66 = 3,708.34

3,708.34 x 0.057 = $211.37 monthly CPP contribution

What factors into the calculation of CPP benefits?

CPP benefits are calculated based on several factors:

-

the number of contributions you've made

-

your average annual earnings

Your contributions to the CPP can come from work you've done in Canada or from receiving retirement credits from a former spouse at the end of a relationship.

How much will I get from CPP?

When you're ready to start collecting your CPP, you'll need to contact Service Canada.

They will provide you with a statement of estimated benefits and an estimate of how much your monthly payments will be. The closer you are to retirement, the more accurate the estimate will be.

You can also use the Canadian Retirement Income Calculator, which includes both CPP and Old Age Security (OAS) payments.

This calculator will give you a good idea of how much money you can expect to receive each month in retirement from the CPP and OAS.

Another great tool to help you calculate your CPP benefits is the Sunlife CPP/QPP Calculator.

When should I start collecting CPP?

When it comes to CPP, there are three main things to consider:

-

when you should start collecting

-

how much it will be reduced if you start early

-

how much it will be increased if you wait until later

The standard age to start collecting CPP benefits is 65. You can elect to start receiving as early as 60, which will reduce your payments, or as late as 70, which will increase your payments.

The decrease for starting early is 0.6% each month, or 7.2 % per year. This means that if you start taking CPP at age 60, your CPP benefit will be 36% lower than if you waited until age 70.

Alternatively, if you start later your benefits will increase at a rate of 8.4% each year. At age 70, your CPP benefit will be 42% higher.

It's important to consider all aspects of your life when making this decision - your health, your financial situation, and your retirement plans. Ultimately, the choice is up to you!

How can I make sure I'm getting the most out of my CPP contributions?

If you're looking to maximize your Canada Pension Plan (CPP) payout, you must contribute to the CPP for at least 39 of the 47 years from ages 18 to 65.

You must also contribute the maximum amount to the CPP for at least 39 years based on the yearly annual pensionable earnings (YMPE) set by the Canada Revenue Agency (CRA). The YMPE for 2022 is $64,900.

If you continue to work after you turn 65 and aren't receiving the CPP retirement pension, any periods where you earned a lower amount of money before the age of 65 will automatically be replaced with periods of higher earnings after the age of 65.

This in turn will increase your overall pension amount.

The Canadian Government automatically excludes up to eight years of your lowest earnings. This is done to ensure that your CPP benefits are based on your best years, rather than your lowest ones.

Child-care

During periods where you were caring for children under the age of 7, you can claim child-rearing provisions. This is to help increase your CPP benefits.

Disability

Any month in which you received a disability payment is also excluded from the calculation of your CPP contributions. This is done to ensure that you're not penalized for being unable to work.

Pension sharing

As CPP benefits are taxable, sharing the benefits with a spouse may be a good option. While it won’t necessarily increase your benefits, it may result in tax savings.

Other CPP benefits

In addition to pension benefits, the CPP offers the following:

-

Disability pension

-

Death benefit

-

Post-retirement benefit

-

Post-retirement disability benefit

-

Survivor’s pension

-

Children’s benefit

Conclusion

CPP is an important part of retirement planning in Canada. It's calculated based on your earnings over your working life, so it's important to keep track of your income and make sure you're contributing as much as you can.

Planning will help ensure you have a comfortable retirement. Next, check How Much Do I Need To Retire In Canada: 5 Simple Steps

Frequently Asked Questions (FAQ)

1. How do I calculate my CPP contribution for 2025?

To calculate your CPP contribution:

-

Subtract the basic exemption ($3,500) from your total pensionable income.

-

Apply the 5.95% contribution rate on income up to the Year’s Maximum Pensionable Earnings (YMPE), which is $68,500 for 2025.

-

If you earn between $68,500 and $73,200 (the Year’s Additional Maximum Pensionable Earnings or YAMPE), apply an extra 4% contribution.

Self-employed individuals must pay both the employee and employer portions.

2. What is the CPP contribution rate for 2025?

For 2025:

-

5.95% (employee) + 5.95% (employer) on income up to $68,500.

-

4% (employee) + 4% (employer) on income from $68,500 to $73,200.

-

Self-employed: 11.9% up to $68,500 and 8% from $68,500 to $73,200.

3. How is the CPP retirement benefit calculated?

Your CPP benefit is based on:

-

Your average earnings over your working life.

-

How much and how long you contributed.

-

The age you start taking CPP (between 60–70).

To maximize benefits, contribute the maximum for 39 of the 47 years between ages 18 and 65.

4. When should I start collecting CPP?

You can start as early as age 60 or delay until 70:

-

Starting early reduces benefits by 0.6% per month (7.2% annually).

-

Delaying increases benefits by 0.7% per month (8.4% annually).

5. How much CPP will I get in 2025?

The maximum monthly CPP benefit at age 65 is $1,364.60 as of January 2025. The average monthly benefit is $758.32, depending on your contribution history.

6. Do self-employed Canadians contribute differently to CPP?

Yes. Self-employed Canadians must pay both the employee and employer portions, totaling 11.9% up to $68,500 and 8% on the next $4,700.

7. Is there a CPP calculator I can use?

Yes. The Canadian Retirement Income Calculator and the Sun Life CPP Calculator are helpful tools to estimate your benefits based on age, income, and contribution history.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.