CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

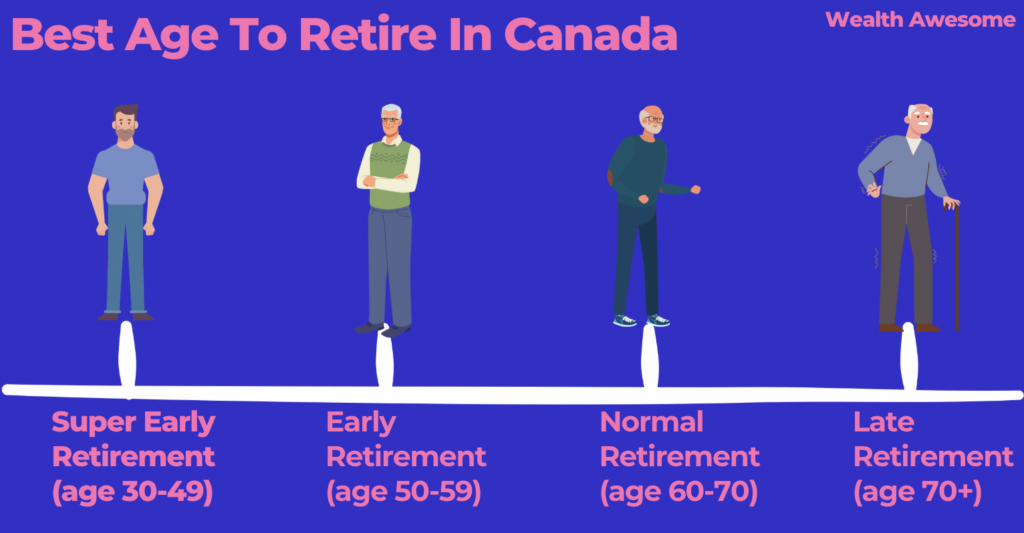

We have excellent retirement plans in Canada. Yet, Despite our strength in retirement planning, the pandemic has significantly impacted 23% of Canadians’ timeline for officially entering their golden years. More than half of them will need to continue working for longer.

It’s more important than ever to make sure you are making the most of the plans available.

In this post, we’ll take a look at fantastic options for retirement plans in Canada. So whether you’re just starting in your career or getting close to retirement age, there’s sure to be an option suited for you!

What Is A Retirement Plan?

A retirement plan is a financial arrangement that will provide money throughout your retirement years. Retirement plans can be set up by employers, financial institutions, or individuals.

Retirement plans typically have specific eligibility requirements, contribution limits, and withdrawal rules. Employers may set up plans or offer matching contributions to encourage employees to save for retirement.

Plans may also offer tax advantages, such as deferred taxes on contributions and earnings.

Retirement plans can be a key part of financial security in retirement. It is important to consider all aspects of a retirement plan before making any decisions.

Employees should consult with their employer about their specific plan. Financial professionals can also help individuals understand the different types of retirement plans and make informed decisions about which plan is best for them.

There are several types of retirement plans available in Canada, each with its own set of rules and regulations. The most common type of retirement plan is the Registered Retirement Savings Plan (RRSP).

Other types of retirement plans include private plans such as Employer-Sponsored Pension Plan and the Deferred Profit-sharing Plans and public plans such as the Old Age Security. Each type of retirement plan has its unique benefits and drawbacks.

You should also consider the investment options available under each type of plan. For example, some plans may only invest in certain types of assets, such as stocks or bonds.

It is also important to compare the costs associated with different types of retirement plans. Some plans may have higher fees than others.

You should also consider the type of customer service offered by the plan provider. Some providers may offer more personalized services than others.

Lastly, consider the impact of inflation on your retirement savings. Inflation can eat into your purchasing power over time.

As a result, you may need to save more money than you originally planned to maintain your standard of living in retirement.

Why You Need A Retirement Plan

There are several important reasons why you need a retirement plan. A retirement plan can help ensure that you have enough money to cover your expenses in retirement and live the lifestyle you want. A retirement plan can also help reduce your taxes.

Another important reason to have a retirement plan is to provide yourself with peace of mind. Knowing that you have a plan in place to secure your financial future can help reduce stress and anxiety.

Finally, a retirement plan can help ensure that you leave a legacy for your loved ones. If you have a plan in place, you can rest assured that your loved ones will be taken care of after you're gone.

No matter what your reason is for needing a retirement plan, it's important to start planning early and make regular contributions to ensure a comfortable retirement.

There are many retirement plans available in Canada, each with its own unique set of benefits. Here are six of the most popular options:

- Registered Retirement Savings Plans (RRSPs)

- Tax-Free Savings Accounts (TFSAs)

- Employer-Sponsored Pension Plans

- Deferred Profit Sharing Plans (DPSPs)

- CPP/QPP

- OAS

- GIS

- Annuity

1. Registered Retirement Savings Plans (RRSPs)

One of the most popular retirement savings options in Canada is the Registered Retirement Savings Plan (RRSP). RRSPs offer many benefits, including the ability to deduct your contributions from your taxable income.

The money in the plan grows tax-free until it's withdrawn.

When it's time for you to retire, your RRSP is converted into a Registered Retirement Income Fund or RRIF. This is a great way to ensure you have a steady income stream in retirement.

In fact, you can convert as early as 55. Once your RRSP becomes an RRIF, you are required to start withdrawing the minimum payments.

RRSPs are a good option for people who want to save for retirement and reduce their taxes. However, it's important to remember that you'll eventually have to pay taxes on the money you withdraw from your RRSP.

2. Tax-Free Savings Accounts (TFSAs)

A Tax-Free Savings Account (TFSA) is an account that allows you to save money without having to pay taxes on its growth. This account is perfect for those who want to save for retirement, as the money you save will compound tax-free.

You can contribute up to $6,000 per year to a TFSA, and there is no maximum age, so you can continue contributing even after you retire.

Another great thing about TFSAs is that you can access your money at any time, without having to pay any penalties. This makes it a great option for Canadians who want to have some flexibility with their savings during retirement.

Withdrawals from a TFSA are also tax-free, so they can be a good way to supplement your retirement income.

TFSAs are another great option for people who want to save for retirement and reduce their taxes. However, it's important to remember that you won't be able to deduct your contributions from your taxes.

3. Employer-Sponsored Pension Plans

An employer pension plan is a retirement savings program that an employer offers to its employees. Employer pension plans are either defined benefit plans or defined contribution plans.

In a defined benefit plan, the amount of your pension benefits is based on your years of service and salary.

In a defined contribution plan, the amount of your pension benefits is based on how much you and your employer have contributed to the plan.

Employer pension plans are usually tax-deferred, which means you don't have to pay taxes on the money you contribute to the plan until you withdraw it in retirement.

If you're a Canadian worker, you may be able to contribute to an employer pension plan. If you're a member of a union, you may also be eligible for a union pension plan.

4. Deferred Profit Sharing Plans (DPSPs)

A Deferred Profit Sharing Plan, or DPSP, is a Canadian employer-sponsored profit-sharing plan used for retirement savings among employees.

Unlike a registered retirement savings plan (RRSP), where employees contribute their own funds, employees in a DPSP receive a pro-rata portion of the company's profits, which are then invested in a tax-free account.

This allows employees to share in the company's success and can be used in conjunction with other retirement plan options like RRSPs and pensions.

The benefits of a DPSP are that contributions are tax-deductible to the employer. as income, the funds grow tax-free, and withdrawals during retirement are taxed as income. This makes them a popular choice for retirement planning.

Another benefit of DPSPs is that they foster a sense of partnership between the company and the members of the plan. Employees often feel more invested in their company when they have a financial stake in its success.

5. CPP/QPP

The Canada Pension Plan (CPP) is government-sponsored. It's designed to provide income for retired workers and their families. CPP and QPP payments are indexed to inflation, meaning that the value of your payments will stay the same (or increase) over time.

To be eligible for the CPP, you must have worked in Canada and made contributions to the plan. The amount of your pension benefits is based on your contributions and your earnings.

The CPP is funded by contributions from workers and employers. Self-employed people also make contributions to the CPP.

The Quebec Pension Plan (QPP) is similar to the CPP, but it's administered by the province of Quebec.

If you're a Canadian worker, you'll need to decide whether to contribute to the CPP or the QPP. If you live in Quebec and work in another province, you may need to contribute to both plans.

6. OAS

The Old Age Security (OAS) pension is a government-sponsored pension plan. It's designed to provide income for retired workers and their families.

To be eligible for the OAS pension, you must be 65 years of age or older and a Canadian citizen or legal resident. The amount of your pension benefits is based on your residency and citizenship status.

The OAS pension is funded by taxes. All Canadian workers and residents are required to pay taxes into the plan.

The OAS pension is the largest of the three government-sponsored pension plans. The other two are the Canada Pension Plan (CPP) and the Quebec Pension Plan (QPP).

7. GIS

The Guaranteed Income Supplement (GIS) is a government-sponsored supplement for low-income seniors. It's designed to help cover the cost of basic living expenses.

To be eligible for the GIS, you must be 65 years of age or older and receive the Old Age Security (OAS) pension. The amount of your GIS benefits is based on your OAS pension and your income.

The GIS is funded by taxes. All Canadian workers and residents are required to pay into the plan.

The GIS supplement is paid monthly, along with your OAS pension. You can receive the GIS even if you don't work or if you're retired.

If you have a spouse or common-law partner, they may also be eligible for the GIS supplement. To receive the supplement, you and your spouse or common-law partner must both be 65 years of age or older and meet the income requirements.

8. Annuity

When it comes to retirement planning, there are a few different options you can explore.An annuity is one of the most common options that are frequently overlooked.

An annuity is a contract between you and an insurance company, which is agreed upon at the time of purchase. In return for making regular payments (known as premiums), the insurance company agrees to pay you a fixed income for the rest of your life.

There are a number of benefits to choosing an annuity for retirement planning. For one, an annuity provides a guaranteed income for life, which can be helpful if you're concerned about outliving your savings.

An annuity can also be helpful in estate planning, as it can provide your loved ones with a steady stream of income after you're gone.

Annuities are a great option for those who want to retire but are worried about outliving their savings. They're also ideal for those who want to ensure they have a steady income even if markets take a downturn.

Tips For Retirement Savings

There are various different ways to save for retirement, and it's important to choose the right option for you. Here are some tips to help you make the most of your retirement savings:

1. Start saving early. If you start saving money early, you will have more time for it to grow.

2. Make regular contributions. Consistent contributions will help you reach your retirement savings goals sooner.

3. Invest in a mix of assets. Diversifying your investments will help protect your savings from market volatility.

4. Consider using tax-advantaged accounts. Accounts like RRSPs and TFSAs offer significant tax advantages, which can help boost your retirement savings.

5. Stay disciplined with your spending. It's important to live within your means and avoid unnecessary debt in order to make the most of your retirement savings.

following these tips will help you make the most of your retirement savings and enjoy a comfortable retirement.

Tips For Choosing A Retirement Plan

There are a few different factors to consider when choosing a retirement plan. Here are some tips to help you make the best decision for your retirement planning needs:

1. Consider your current and future income needs. Will your current income be sufficient in retirement, or will you need to supplement it with other sources of income?

-

Think about how long you expect to live in retirement. This will help you determine how much money you'll need to have saved.

-

Consider your risk tolerance. Some retirement plans are riskier than others, so it's important to choose an option that's comfortable for you.

4. Compare the fees and expenses associated with different retirement plans. Higher fees can eat into your savings, so it's important to choose an affordable plan.

5. Talk to a financial advisor. A professional can help you assess your needs and make the best decision for your circumstances.

Conclusion

When it comes to retirement planning, Canada is a great place to be. We have a range of options that can fit nearly any budget and lifestyle.

No matter which retirement savings option you choose, it's important to start saving early and make regular contributions to ensure a comfortable retirement.

Next, check out How To Retire At 50: The Exact Steps And Amount Needed.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.