CIBC Investor's Edge

Transfer your investments to CIBC Investor's Edge and get rewarded with an offer of up to $3,000.

- ✓$6.95 flat-rate commissions

- ✓Backed by Big Five bank security

- ✓Transfer bonus offer up to $3,000

With inflation skyrocketing in Canada, 1 million dollars isn't what it used to be.

It has a lot of people wondering if 1 million is even enough to retire these days.

The answer is that it depends on your lifestyle and many other factors. Here's what we'll go over below to help you try to figure this out:

-

How long you'll be retired for

-

What your monthly “income” will be from government pensions and assets

-

How much money you will spend each year

-

If you invest your money, how well it performs

Things to Consider During Retirement Planning

Here are four questions to consider when you start your retirement planning.

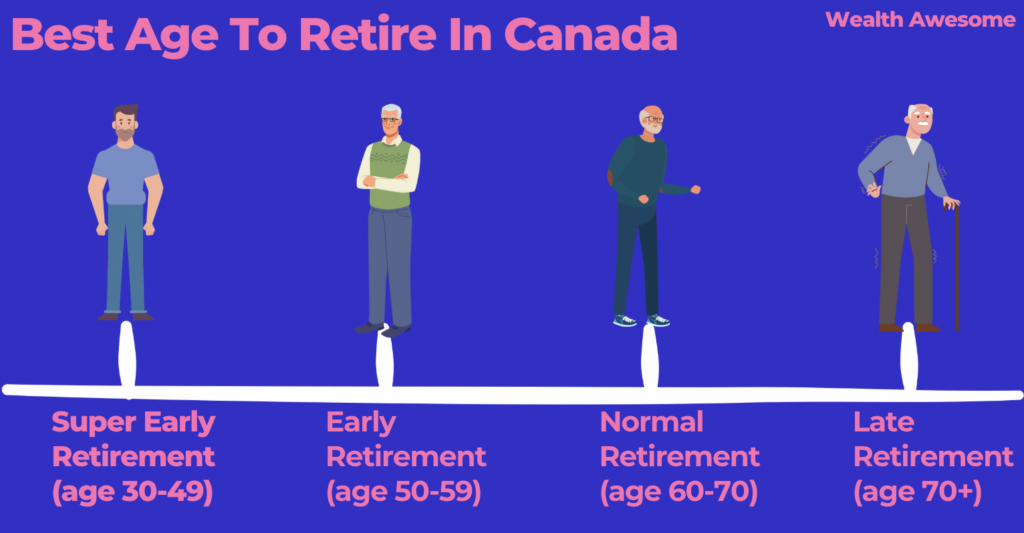

1. When Do You Plan to Retire?

The age at which you would like to retire can make a big difference in how much you should have saved.

As a rule of thumb, the earlier you retire, the more money you will need to have saved up for your retirement years.

The later you retire, the lower your savings factor will be, mostly because your savings will have a longer time to appreciate, and you will also have fewer years in retirement.

In addition, your Canada Pension Plan (CPP) payments will be higher the longer you delay your retirement, making it even “easier” to retire later.

According to the most recent data from Statistics Canada, the average retirement age of Canadians was approximately 64.6 years old in 2023, showing a slight increase from previous years. This continues to vary by employment type: private sector workers retired at 64.8, public sector at 62.3, and the self-employed at 67.4

Below you can see further details of this statistic and how retirement age changes in different classes of workers in Canada.

| Class of Worker | Average Age of Retirement, 2021 |

|---|---|

| Private Sector (those who work as an employee of a private firm or business) | 64.8 |

| Public Sector (those who work for a local, provincial or federal government, government service or agency, a crown corporation, or a government-funded establishment such as a school or hospital) | 62.4 |

| Self-employed (incorporated and unincorporated working owners, self-employed persons who do not have a business and persons working in a family business without pay) | 67.6 |

If you plan to retire before the average (around 64 years old), you might want to consider saving up more than $1 million for retirement.

If you plan on retiring after the average (perhaps around 70 years old or later), you may need less than $1 million for your retirement.

Related Reading: Best Age to Retire in Canada: 55, 65, or Never?

2. How Do You Plan to Live When you Retire?

How you plan to live after your retirement is just as important as when you plan to retire.

What kind of life do you plan to be living as a retired person? Do you expect to spend less, the same, or more than the amount you were spending pre-retirement?

Do you have travels and experiences you’ve been putting off for retirement? Do you want to be spoiling your grandkids?

What kind of life do you plan to be living as a retired person? Do you expect to spend less, the same, or more than the amount you were spending pre-retirement?

Do you have travels and experiences you’ve been putting off for retirement? Do you want to be spoiling your grandkids?

Do note that according to the StatCan Survey of Household Spending, according to the 2023 Survey of Household Spending, Canadians aged 65 and older spent an average of approximately $71,000 annually, including taxes, reflecting rising living costs over time.

Taking inflation and rising costs of living over the years, we can expect this number to be around $64,000 now.

3. How Much Government Income Will You Receive?

The third most important thing to consider when you are thinking about retirement planning is your monthly CPP payment and other “asset” incomes (such as rental income.)

CPP payments are different for everyone as things such as your income before retirement, type of income, and the number of “low earning” years will have an effect on it.

According to StatCan, however, as of January 2025, the average CPP payout is approximately $758.32 per month, although this can vary based on your individual contribution history and retirement age

CPP payments are different for everyone as things such as your income before retirement, type of income, and the number of “low earning” years will have an effect on it.

4. Your Investment Returns

This will be the hardest factor to predict, but it's an important one. How you decide to invest your nest egg will be a big factor in how long your retirement income will last. It's important to do a full financial plan, see how much risk you can take on in your portfolio, and invest accordingly.

Can You Retire With $1 Million in Canada Calculation

When you have an estimate of these numbers, you can use the following equation to figure out whether $1 million will be enough:

(Annual expenditure X predicted number of years in retirement) - total income you’ll receive in retirement.

Based on these three notions regarding your retirement age, retirement lifestyle and CPP income, you can do a quick calculation to figure out whether you can retire on $1 million in Canada.

For instance, let’s say that Adam wants to retire at the age of 65. To be safe, he would like to plan his retirement until he’s 90 years old. That’s 25 years in retirement.

Adam currently spends about $50,000 per year and plans to spend about the same during his retirement years (do note that this is about $10,000 less than the average expenditure for his age demographic.)

He expects that his monthly CPP income will be around $700, which amounts to $210,000 over the course of his 25 years of retirement ($700 x 300 months in retirement.)

By simply calculating ($50,000 x 25) - $210,000, he can find that $1,040,000 will be enough for his retirement years.

If this example is on par with the type of retirement you are planning to have, then, yes, you can retire on $1 million in Canada!

Do keep in mind that this is an incredibly basic calculation but can be a great starting point for you to figure out how much money you will need for your retirement.

Although it does not take things such as inflation, returns on investment (ROI), or lifestyle increases into account, it can lead you in the direction of an accurate ballpark.

You can also use these two free retirement calculators: the Wealthsimple Retirement Income Calculator and Sun Life Retirement Income Calculator.

Can I Retire at 60 With 500k in Canada?

It may not be easy to retire at 60 years old with $500,000 in Canada for your entire household. Why? Take this simple calculation:

If you retire at 60 and plan for 30 years in retirement, spending the average amount spent by senior households in Canada, you will need about $1,800,000 (30 years x $60,000 per year.)

Let’s say that you receive $700 each month as part of your CPP (though it may be less than that if you retire at 60). You will get about $252,000 throughout your retirement ($700 per month for 360 months.)

Even if you take returns on investment into account, you will need about $1,500,000 to retire at the age of 60 in Canada (spending the average amount until you are 90.)

But this isn’t to say that it can’t be done. I know that planning until 90 is generous (given that life expectancy in Canada is 82), and some seniors are comfortable living on about $40,000 or even less each year (especially if they’ve already paid off their mortgage!).

It really all depends on your lifestyle, investment returns, and years spent in retirement.

FAQs

How much does a single person need to retire comfortably in Canada?

Retiring comfortably in Canada as a single individual involves various factors, primarily based on the lifestyle one aims to maintain. On average, financial experts often suggest that retirees will need about 70% of their pre-retirement income to maintain their current lifestyle. For a modest lifestyle, a ballpark figure suggests that a single person might need between $25,000 to $30,000 annually after taxes.

This amount includes government pensions like the Old Age Security (OAS) and the Canada Pension Plan (CPP). However, if one aims for a more comfortable or luxurious retirement, factoring in travel, hobbies, and other leisure activities, this number can significantly increase.

How much money does a couple need to retire in Canada?

For couples in Canada looking to retire comfortably, the combined annual requirement can be estimated to be between $40,000 to $70,000 after taxes for a modest lifestyle. This calculation assumes both parties are receiving full Old Age Security (OAS) and Canada Pension Plan (CPP) benefits, and it covers basic expenses such as housing, healthcare, transportation, food, and a few leisure activities.

For couples desiring a more luxurious retirement—perhaps including regular travels, dining out frequently, or engaging in high-end hobbies—the annual requirement can exceed these estimates. It's also crucial to account for the potential of increased medical expenses in later years.

Can I retire on 1 million dollars in Canada?

Yes, you can retire on 1 million dollars in Canada, depending on your lifestyle, retirement age, and other income sources like CPP and OAS. A modest lifestyle with controlled spending and smart investing can help stretch your retirement savings across decades. However, for those with higher living costs or plans for frequent travel, 1 million may not be sufficient.

Is a million dollars enough to retire in Canada comfortably?

For many Canadians, $1 million can provide a comfortable retirement, especially when combined with CPP, OAS, and possibly private pensions. The key is careful budgeting and understanding your expected annual expenses and income sources. Using tools like a retirement income calculator can help estimate whether your savings align with your goals.

How do I go about investing 1 million dollars in Canada for retirement?

Investing 1 million dollars in Canada should be guided by your risk tolerance, timeline, and income needs. A diversified portfolio including RRSPs, TFSAs, and non-registered accounts can help reduce taxes and generate steady returns. Consider low-cost ETFs, dividend-paying stocks, or GICs depending on your risk appetite. Consulting with a financial planner is also recommended.

Can a couple retire on 1 million dollars in Canada?

A couple can retire on 1 million dollars in Canada if they manage expenses carefully and supplement their savings with government benefits. Factors such as mortgage status, desired lifestyle, and healthcare costs play a big role. Downsizing or relocating to lower-cost areas can also extend retirement savings.

What is the difference between retiring in Canada with 1 million dollars and investing it for income?

Retiring in Canada with 1 million dollars gives you flexibility, but how you invest it determines whether it lasts. If invested wisely, your $1 million could generate $35,000–$50,000 annually in income, depending on market conditions and risk profile. Not investing it—or investing too conservatively—may cause your savings to run out sooner.

Can you retire at 60 with $1 million in Canada?

Yes, retiring at 60 with $1 million in Canada is possible, but it’s tighter than retiring at 65 or 70. You’ll need to budget more carefully and may receive reduced CPP benefits. Planning for 30+ years in retirement means ensuring your investments provide reliable long-term returns while guarding against inflation.

Conclusion

It is certainly possible to have a comfortable retirement in Canada with $1 million.

As I said, things such as lifestyle, retirement age, and pension payments make a big difference, so it’s best not to take the word of others and do your own calculations instead.

If you have a financial planner, they’ll be able to help you with this kind of thing. It never hurts to ask for assistance from a professional who can point you in the right direction and give you a good depiction of what your retirement might look like.

Want more tools to calculate how much you’ll need to retire? Check out this post!

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.