CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

Looking to invest responsibly by adding renewable energy stocks to your portfolio?

Hydroelectricity is Canada's most critical energy source, making up 59.3% of the country’s electricity generation.

Investing in renewable energy is not only a sound way to help protect your environment but is also likely a good way to grow your money over a long period of time.

Advertisement

We will discuss some of the best Canadian renewable energy stocks further below.

Understanding Renewable Energy

With climate change becoming a growing concern, a large focus has been placed on developing and maintaining renewable energy sources.

The common sources of renewable energy include:

-

Solar Energy

-

Wind Energy

-

Geothermal Energy

-

Hydropower

-

Ocean Energy

-

Bioenergy

Generating renewable energy typically has large up-front costs (in terms of setting up infrastructure) but can lead to clean, long-term energy generation.

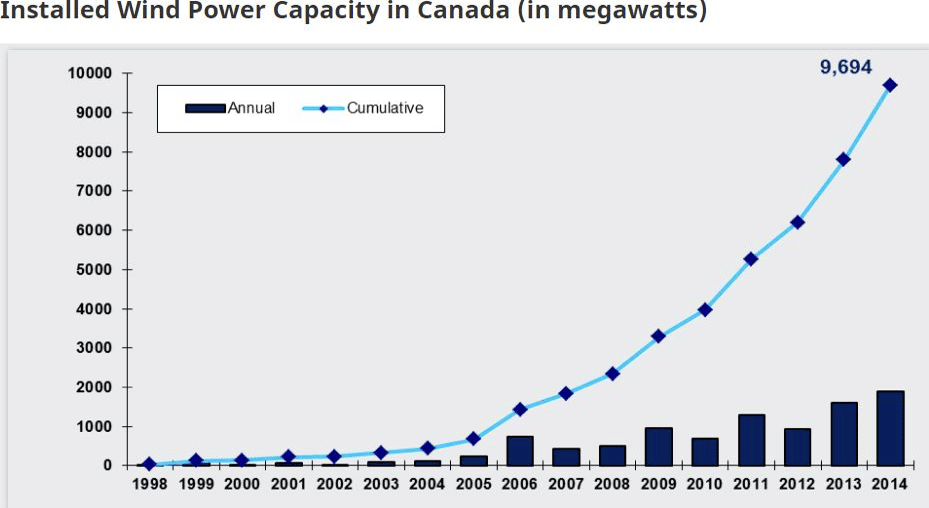

As an example, wind power capacity in Canada, measured by the number of operating wind turbines, has grown exponentially since the start of the 21st century.

Additional facts about renewable energy in Canada include:

-

Renewable energy makes up about 18.9% of Canada’s total energy supply

-

Wind and biomass are the 2nd and 3rd most important sources, respectively

-

Canada is a world leader in the production and use of renewable energy

Pros and Cons of Canadian Renewable Energy Stocks

Like all other investments, renewable energy stocks have advantages and disadvantages. The fundamental pros and cons of renewable energy stocks are directly tied to the pros and cons of renewable energy as a whole.

Despite renewable energy disadvantages, dependency on renewable energy sources will probably increase in the future as we transition away from fossil fuels.

Pros

-

Cleaner future energy generation

-

Investing in a young industry with immense future growth potential

-

Renewable energy sources are abundant and self-sufficient over the long term once set up

Cons

-

Business seasonality and dependence on ideal environmental conditions

-

High upfront costs

-

Company operations typically require significant land space.

Best Canadian Renewable Energy Stocks

-

Brookfield Renewable Partners (BEP-UN.TO)

-

Northland Power (NPI.TO)

-

Innergex Renewable Energy (INE.TO)

-

Algonquin Power & Utilities (AQN.TO)

-

Ballard Power Systems (BLDP.TO)

-

Spark Power Group (SPG.TO)

1. Brookfield Renewable Partners

-

Ticker: BEP-UN.TO

-

Forward Dividend Yield: 5.32%

-

Dividend Payout Ratio: 649.02%

-

Dividend Yield (12-Month Trailing): 3.36%

-

Upcoming Dividend Date:

-

Market Cap: $21.66B

Brookfield Renewable offers its investors access/exposure to a geographically diversified portfolio of renewable companies and assets.

It has a portfolio of about 32 GW across the globe, about 57% of which is in North America and the remaining in three other markets (South America, Europe, and Asia).

The projected operating capacity, much of which is expected to come online by 2030, is massive - 132 GW, 87% of which will be solar and wind. Geographic and asset diversity are the company's major strengths.

It has grown its revenues consistently and at a compelling pace. Between 2013 and 2022, its revenues grew by over 2.7x, and its Funds From Operations (FFO) by about 70%.

It carries a massive amount of debt. However, since 97% of its financing is fixed rate, the debt management is highly predictable (no nasty surprises). The average debt maturity term also gives the company some breathing room.

It's a powerful investment for both its dividends and growth because, in the last ten years (between Aug 2013 and Aug 2023), the stock returned over 300% to its investors, divided half and half between dividends and capital appreciation.

Apart from its solid fundamentals, the thing I like most about this company is its vision, reflected in its partnership with Cameco, the uranium giant.

Despite a focus on pure renewables, Brookfield Renewable management probably understands the value of nuclear power as the transitional fuel for reducing emissions.

Its current price and valuation discounts are reason enough for you to look into this stock, but you should understand the risks it carries - debt and the nature of revenue.

About 90% of its revenues come from long-term merchant contracts that are vulnerable to power price fluctuations (as opposed to contracted prices).

2. Northland Power

-

Ticker: NPI.TO

-

Forward Dividend Yield: 5.31%

-

Dividend Payout Ratio: 76.92%

-

Dividend Yield (12-Month Trailing): 4.84%

-

Upcoming Dividend Date:

-

Market Cap: $5.62B

Northland Power is a renewable company with a geographically diverse portfolio of renewable assets, both operational and under development.

With 40% and 30% of its assets in Europe and North America, respectively, and the remaining in Asia and America, it has adequate exposure to both mature markets with steady demand and emerging markets.

The current portfolio leans heavily towards offshore wind (60% of the output), and the development portfolio will sway the proportions even more in this direction.

An offshore wind portfolio carries several advantages, including even more (and consistent) power output with fewer turbines required, but the cost of maintenance is the flip side.

The company grew its operating capacity by 115% and operating income by about 100% between 2017 and 2022. The capital appreciation over that period was roughly 60%, though dividends over that period may push the number significantly higher.

Institutions have over 43% stake in the company, which partially shelters it against panic movements by retail investors.

Despite its unsteady growth in the past, the overall return potential of the company seems promising, and though you might find its debt (higher than its current market capitalization), it sticks to the pattern of other renewable companies in Canada.

If you are planning on buying it as soon as possible, its attractive valuation and low beta are also factors worth taking into account.

3. Innergex Renewable Energy

-

Ticker: INE.TO

-

Forward Dividend Yield: 7.49%

-

Dividend Payout Ratio: 868.75%

-

Dividend Yield (12-Month Trailing):

-

Upcoming Dividend Date:

-

Market Cap:

Innergex Renewable has its roots in the first, properly harnessed renewable source, i.e., water.

It started out in 1990 as a hydroelectric company and has now expanded its portfolio to include other renewable energy sources, primarily wind and solar. Its installed capacity represents both assets that it owns and assets it has a stake in.

The total 4.2 GW capacity is enough to power over a million homes. The bulk of its assets are in Canada and the US, though about 26% of its net capacity is in Chile and France.

One major financial strength the company has is that about 88% of its output is contracted and virtually immune to market price variations.

Its debt structure is precarious, as 77% of its $1.4 billion debt (short-term) is expected to mature within the next two to four years.

It won't be a problem if the company keeps growing its revenue as it has in the past - over 4x between 2013 and 2022, though the operating income has shifted from profit to loss over this period.

Advertisement

Despite the financial challenges, the company has grown and, for the last few years, sustained its payouts.

It also offers modest capital appreciation potential, though part of it is associated with the massive slump the company has yet to recover from (which has made its yield quite attractive).

If you are looking for a hefty yield, Innergex may look more appealing than most other picks on this list. However, you should strive to see its capital appreciation potential without the current slump obstructing the view.

4. Algonquin Power & Utilities

-

Ticker: AQN.TO

-

Forward Dividend Yield: 6.96%

-

Dividend Payout Ratio: N/A

-

Dividend Yield (12-Month Trailing): 3.03%

-

Upcoming Dividend Date:

-

Market Cap: $6.61B

Algonquin Power and Utilities offers two types of diversity - geographic and operational.

Unlike other stocks on this list, Algonquin is not just a renewable power generation company; it's also a major utility company that offers electrical power, natural gas, and water utility services to over 1.24 million consumers, primarily in North America. In 2022, about 83% of its revenues came from the US alone.

It has a net generation capacity of about 1.4 GW and a gross installed capacity of about 2.5 GW, which shows that the company can accommodate hundreds of thousands of new electric utility consumers without the need to grow its power generation assets. It has about 44 renewable facilities in its portfolio right now.

After experiencing over a decade of bullish momentum, the company lost over half of its market value in just two years (2021 and 2022). One of the factors behind this massive fall was the decision of this aristocrat to slash its payouts by roughly 40%.

It hasn't had the desired impact yet (dividends becoming more financially sustainable), but investors may see payout ratios go down in the future.

A major problem Algonquin faced in the past was mismanaged debt, but cutting its dividends and giving up a billion dollars worth of assets were strong decisions and showed indications of a committed management team ready to make tough choices.

Over 63% of the company is held by institutions, and the big five Canadian banks alone own about 14% of the company.

Despite the dividend cut, the yield has remained attractive because of the stock slump, and it might still be considered a good buy for dividends.

You should keep the risk associated with the company’s dividend history in mind when investing in the company. But its current valuation and discount make it a very lucrative buy, especially if it manages its debt more efficiently in the future.

5. Ballard Power Systems

-

Ticker: BLDP.TO

-

Forward Dividend Yield: N/A

-

Upcoming Dividend Date:

-

Market Cap: $1.06B

Ballard Power Systems is not a "conventional" renewable company. In fact, its fuel cell technology focuses on a non-renewable source, i.e., hydrogen, but it overlaps with the renewable market for a single reason - zero emissions.

In fact, compared to other renewable sources like solar, which relies on batteries that come with a massive carbon footprint, Ballard’s fuel cells are far cleaner and greener. They rely upon hydrogen as a fuel to generate clean electricity.

Their primary market is EV, but Ballard has massive growth potential in the stationary power market as well, where its fuel cells can be used to power any space or industrial/commercial installation as an alternative to grid power or renewable power like wind or solar.

The only major challenge the company faces right now is that the global hydrogen extraction, storage, and transportation infrastructure is barely in its infancy.

However, a single breakthrough in hydrogen extraction or safe transportation can radically change the outlook of the renewable market, and companies like Ballard Power might experience explosive growth.

Financially, the revenue and net income of the company are dismal, to say the least, but it carries minimal debt and has a massive cash position.

You should know that at this point, Ballard Power is mostly a good prospect, even though it has worked hard to carve a place for itself in the global market.

But if a hydrogen revolution joins in the renewables one or a breakthrough happens that makes hydrogen readily available as a fuel source, you may consider snapping up Ballard Power right away.

6. Spark Power Group

![]()

-

Ticker: SPG.TO

-

Forward Dividend Yield: N/A

-

Upcoming Dividend Date:

-

Market Cap:

Spark Power Group is a nano-cap company with a revenue (2022 annual) that’s six times its current market capitalization.

It’s basically an electrical service provider that caters to the needs of a wide range of industrial and commercial clients and has now expanded its services into the renewable sector.

In 2022, roughly a third of its revenues came from renewables, a decent growth from 28% in 2020.

The idea is that with so many renewable sources joining the grid, Spark Power Group will start leaning more heavily towards renewable services.

You should know that there are several reasons not to invest in this stock, starting with the fact that it has lost over 80% of its market value since its inception (from Sep 2018 to Aug 2023).

It's also an asset/resource-heavy business. It has a massive fleet and over a thousand employees. It also has a significant amount of debt (compared to its market capitalization) and almost no cash reserve/small investments.

The three main reasons you should consider buying this stock are its massive undervaluation, improving financials, and geographic reach. Its EV to sales is currently 0.5x, and it started generating a positive income in 2022.

Considering its reach and credibility, it's very well-positioned to help a wide range of industrial and commercial clients turn to renewables.

The Role of Technology in Renewable Energy

Innovations in solar panel efficiency, wind turbine design, and battery storage have drastically reduced the cost per megawatt-hour of these renewable sources. Take, for example, the advent of AI in managing renewable energy grids. Machine learning algorithms can predict the demand and supply, optimizing the energy distribution in real-time, thus making the entire system more efficient.

Technological advancements aren't just limited to the core generation technology. They extend to secondary systems like grid management, storage, and even investment analytics.

Blockchain is another technology that promises to revolutionize the renewable energy sector by enabling secure and transparent peer-to-peer energy trading platforms.

Impact of Climate Change and Environmental Factors

As the world grapples with the impacts of climate change—rising temperatures, sea-level increases, and more frequent and intense weather events—the need for clean energy sources becomes more pressing.

Environmental policies are getting stricter, and the social demand for sustainable energy is increasing, both of which can directly influence the valuation of renewable energy stocks.

However, the sector is not without its environmental challenges. For instance, the production and disposal of solar panels and wind turbines involve some environmental pollution and waste. Also, hydropower and bioenergy projects can have significant impacts on local ecosystems.

Financial Analysis of Renewable Energy Stocks

When looking at the financials of renewable energy stocks, one of the most critical factors to consider is the cost of capital. Given the significant up-front investment required for renewable energy projects, companies often rely on a blend of equity and debt financing.

The interest rates and the credit ratings can dramatically affect a company's profitability and risk profile.

Investors should also look into the company’s income streams. For example, companies like Brookfield Renewable Partners have long-term power purchase agreements, which guarantee a steady revenue stream.

On the other hand, companies like Spark Power Group rely more heavily on the fast-evolving renewable service sector, which might be less stable but offers higher growth prospects.

Should You Invest in Renewable Energy Stocks?

Renewable energy stocks are involved in an industry that will likely grow in scale and application in the future. Currently, fossil fuels still make up a significant portion of our energy consumption.

With that said, renewable energy stocks are likely a great investment for investors that:

-

Are looking for an ESG investment or to invest responsibly

-

Have a long-term investment time horizon

-

Can accept a relatively lower dividend yield (especially versus oil and gas stocks)

Before investing in renewable energy stocks, make sure that equities are appropriate within your investment portfolio.

FAQs

Which Canadian energy stocks are investing the most in renewable energy?

Leading the way in renewable investments are companies like Suncor Energy, which has been diversifying into wind energy, and TransAlta Corporation, known for its transition towards renewables like wind, hydro, and solar.

Which Canadian renewable energy ETFs have shown strong returns?

Examples include the iShares S&P/TSX Capped Utilities Index ETF, which covers a broad spectrum of utility companies, including those in the renewable sector.

Another noteworthy mention is the Invesco Solar ETF, which, although not exclusive to Canada, has a focus on the solar industry and includes Canadian companies.

Is There More Wind or Solar Power in Canada?

Wind power generation is much more widely developed within Canada than solar power. It is the second largest source of renewable energy in the country after hydropower.

What Country is Leading in Renewable Energy?

In terms of renewable energy production, China is the largest producer of both wind and solar energy in the world. As a share of total energy consumption, Norway has the highest share of renewable energy usage globally.

Conclusion

Renewable energy stocks allow you to invest in companies that will likely be crucial to the energy supply of the world in the near future.

Since investing is a long-term endeavour, it aligns well with the long-term growth potential of the renewable energy industry.

If you are looking for additional diversification, make sure to consider the best ESG ETFs in Canada within a responsible investing context.

Best next step

Keep exploring this topic

If you want to go deeper, these are the most useful follow-up pages and tools for this topic.

Stocks tool

Check Canadian stock movers

See the latest TSX and TSXV winners and losers before digging deeper into a sector.

Research hub

Browse Canadian stock research

Use the stock section to jump from a theme article into individual company pages.

Diversification

Compare stocks with ETF options

If you want exposure to a theme without single-stock risk, screen matching ETFs instead.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.