CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

At the big five banks in Canada, you will find that most of them advise their clients to invest in mutual fund products.

However, mutual fund fees in Canada happen to be some of the highest in the world.

So are mutual fund fees in Canada a rip-off? Are financial advisors worth trusting with your money?

Advertisement

As a former financial advisor at one of the largest investment firms in Canada, I have a few things to say that could shed some light on this issue.

Are Mutual Fund Fees In Canada A Rip-Off?

Canada’s mutual fund market boasts some of the highest fees among global mutual fund markets. A 2017 Morningstar report showed that Canada received the lowest score regarding investment fees and expenses from 25 different countries when it comes to mutual funds.

It means that Canadian investors pay some of the highest investment fees compared to investors in developed countries elsewhere.

The average 2017 Management Expense Ratio (MER) for equity mutual funds in Canada is 2.23%. It means that if you have a portfolio of $200,000, you could be paying $4,460 in fees each year to the fund manager.

The US scores among the best in terms of investment fees, and the average MER for similar mutual funds in the country is 0.66%. It means that the same portfolio in the US would cost you $1,320.

Until recently, Canadian investors typically did not know what accounted for the high mutual fund fees they had to pay to fund managers. The MER is also one of the several fees you might have to pay on your investment portfolio.

Depending on multiple factors, you could end up paying far more than the MER because of other fees that accumulate over time. Many of these fees were hidden until regulatory bodies in Canada emphasized the need for transparency.

Check out this video to see why I think mutual funds in Canada are awful (mainly due to its unnecessarily high fees):

Mutual Fund Fees Expenses - What Are you Paying For?

Here’s a better look at the expenses you can expect to pay when you are investing in mutual funds:

1. Management Expense Ratio

The MER is the major chunk of the expenses you can expect to pay when purchasing shares in a mutual fund. This is an annual fee charged to your portfolio, and it comprises management fees, operating expenses, and trailing commissions.

You can check out the MER of any particular mutual fund product by studying its prospectus or ‘fund facts’ to see the MER it boasts.

Fund managers charge the MER directly from the fund, which means the total investment returns of the mutual fund will be lower over time. Depending on how actively managed the specific mutual fund is, the MER could be higher or lower.

Typically, MER fees compensate the investment managers, legal fees, administrative fees, marketing costs, trailing commissions, taxes, and several other costs.

2. Sales Commissions

Sales commissions are expenses beyond the MER that you can expect to cover when investing in mutual funds. These are the commissions you pay to investment dealers when you buy or sell a fund from them. Also called sales loads, sales commissions come primarily in three different forms:

I. Initial Sales Charge (Front-End Load)

The investment firm you work with might charge this cost when they sell you the fund. You can expect this cost to be up to 5% of your initial investment, and all the money you pay in this fee goes towards the financial advisor’s firm.

It might be possible to negotiate the initial sales charge to get more favourable terms for yourself. The initial sales charge has become less common in the Canadian mutual fund market due to the competitive nature of the investment landscape here in a bid to attract more investors.

II. DSC Fees in Canada (Back-End Load)

Deferred Sales Charge (DSC), or the back-end load, is something you can expect to pay when investing in some mutual fund products in Canada.

The DSC fees in Canada essentially infer that the fund manager is paying the financial advisor’s firm a commission out of their pockets when they initially purchase the fund. A DSC-based fund does not charge you an initial sales charge.

Depending on how long you hold onto the mutual fund and when you sell it, the fund manager can charge you up to 7% of your portfolio’s value in DSC fees in Canada. The longer you hold onto the fund, the lower the DSC fees you will incur. You can hold onto the mutual fund for long enough to reduce the DSC fees to 0%.

The DSC fees in Canada are one of the biggest reasons that mutual fund fees in Canada are a rip-off, in my opinion. Fund managers essentially charge this fee to ensure that you remain invested in the mutual fund for several years or end up paying hundreds or even thousands of dollars in penalties.

Securities regulators placed an outright ban on DSC-based mutual funds in Canada in December 2019 across all provinces except Ontario.

III. Low-Load Sales Charge

Initial Sales Charge- and Deferred Sales Charge-based mutual funds are understandably falling out of favour among Canadian investors as they become more aware of these arguably unfair expenses. Some firms have now started using a low-fee approach.

With Low-Load Sales Charges, the firm will not charge you an upfront commission for the sale of mutual fund products, and you do not have to pay penalties if you hold your investment for longer than 24 months if you redeem or sell your investment.

Even if you choose to sell or redeem your investment, the penalty is traditionally around 2%.

There are mutual funds that do not charge any fees for buying and selling their funds. It means that you can find funds that do not require paying sales commissions on them.

3. Trailing Commissions

Also called trailer fees, trailing commissions are a part of the MER. However, this fee warrants a comprehensive definition. Trailing commissions are the ongoing payments made by investment firms to the financial advisors who provide them with their services.

Trailer fees are usually high, and you can expect them to account for up to 1% or more of the total MER.

Suppose that you have invested $100,000 in a mutual fund product, and its MER includes a 1% trailer fee. In that case, you will end up paying $1,000 or more each year in just trailing commissions.

4. Short-Term Trading Fee

The short-term trading fee is an expense you can expect the fund manager to charge you if you redeem or switch out a fund within a month of purchasing it. Investment firms can charge you this fee to discourage short-term trading and encourage you to hold onto your investment for a longer period.

You can expect to pay 1-2% in short-term trading fees if you redeem or switch out a fund within 30 days of your purchase.

5. Other Expenses

Your expenses for owning mutual funds in Canada do not end with the exorbitant fee structure charged between the fund managers and by financial advisors through them.

You might also have to contend with other investment fees. You might have to pay fixed administration fees for registered accounts, full or partial deregistration fees, expenses for unscheduled withdrawals from RRIFs, and expenses for transferring your assets from one financial institution to another.

Are The Mutual Fund Fees In Canada Bad?

A better question to ask is, “Are the high fees for mutual funds I pay worth the expense?”

When you pay far more than investors in other developed countries for services provided by fund managers and financial advisors, you expect them to provide you with more value.

If you pay more in investment fees but get more bang for your buck than similar funds with lower expenses, it could make the exorbitant fees seem worth it. If higher mutual fund fees do not come with greater returns than low-cost products with similar benefits and features, the expenses are not worth it.

Advertisement

Unfortunately, the sad reality is that you cannot expect mutual fund products to outperform the broader markets to provide greater returns on your investment that can cover the expenses and leave you with a decent profit margin compared to low-cost investment products with similar benefits and features.

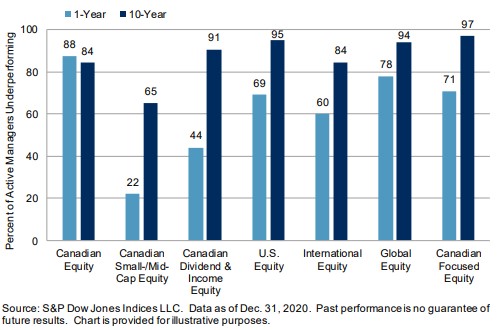

The SPIVA Canada Year-End 2020 Scorecard above shows that Canadian investors do not have much to gain by paying higher MERs to active equity fund managers based on how the funds perform relative to their benchmark indices.

Suppose that you are interested solely in the Canadian equity market index. According to the chart above, 88% of actively managed funds underperformed their benchmark indices in 2020, and 84% of them underperformed between 2010 and 2020.

Almost 70% of actively managed US equity funds underperformed in 2020, and a staggering 95% of these actively managed funds underperformed the benchmark index between 2010 and 2020.

Are Investment Management Fees Tax-Deductible In Canada?

Some investment fees in Canada are tax-deductible, while others are not. There are different types of investment management fees that you end up paying for owning mutual funds and using financial advisors’ services.

Any brokerage and investment fees that you pay in a non-registered account are tax-deductible. These are some of the most overlooked tax deductions in Canada.

These charges can include management fees, fees for specific investment advice, and even the fee you might pay a professional to complete your tax returns for you.

However, savvier Canadian investors choose to invest in registered and tax-sheltered accounts like RRSPs, TFSAs, and RRIFs. Any investment management fees on assets held within those accounts are not tax-deductible.

This might seem a little confusing, but it makes sense. Registered accounts are investment accounts through which the government encourages you to invest by offering you preferential tax treatment.

Since your investment returns through these registered accounts are not taxable, you cannot claim those costs for tax deductions either.

Whether you pay the fund manager the investment fee separately or if these expenses are embedded in your investment returns does not matter. The fees are simply not tax-deductible. You also cannot deduct any annual administration fees for registered accounts or financial planning fees in these accounts.

Any transaction fees you pay to buy and sell investments are never tax-deductible, regardless of the investment account type. The commission and sales charges on any investments in registered or non-registered accounts are also not tax-deductible.

The Issue With Financial Advisors

Considering the expenses involved with mutual fund investing and how the additional cost does not translate to better returns, it might make you wonder why financial advisors direct you towards these expensive products in the first place?

After all, it is their job to give you sound financial advice to help you make the most of your investment capital.

The term financial advisor is unregulated throughout most of the country, and many of them are effectively salespeople who have been provided short training, and you will find most of them working at retail banks promoting the banks’ own investment products to give the financial institutions the highest profit.

I was one myself, I would know, and this is the reason why my career as a financial advisor was short. Purposefully giving financial advice to clients only to focus on benefitting from commissions is not what I signed up for. I do not mean to imply that your financial advisor is also doing this, but they could be doing it.

How Do You Tell If Your Financial Advisor Is Ripping You Off?

Not all financial advisors are providing their services to rip you off.

Provided that you can identify the good ones from the greedy ones, you can find decent financial advisors who give you the sound advice you need to get the most bang for your buck instead of pushing you towards products that provide them incentives through commissions.

Here are a few warning signs that should tell you whether the financial advisor you are working with is trying to rip you off:

I. No Transparency On How They Are Paid

They do not explain how they get paid. Many financial advisors make you feel like they are providing you with a free service because you do not pay any out-of-pocket expenses for their expert advice.

The truth is that many of them who are not transparent about how they earn money are going to push you towards investment products that result in commissions through trailing fees and DSCs in addition to MERs.

II. They Do Not Seem Interested In Your Wellbeing

A sincere financial advisor will take the time to truly understand you, your financial goals, and your economic circumstances and provide you with financial advice based on your situation.

They will give you advice based on your concerns about short- and long-term returns, your time horizon for retirement, and other factors that concern your well-being. If you feel that your financial advisor actually cares about your financial success, you should look elsewhere.

III. They Make Tall Promises

If you come across a financial advisor who is confident that they can help you beat the market, you should look elsewhere.

Even when highly paid mutual fund managers cannot outperform the markets when it’s their job, how would you expect to entertain the claim of a professional whose job is to manage your client and portfolio?

IV. They Push Their Own Products

When you are buying mutual funds or ETFs, you should look for investment vehicles with low costs and proven track records.

If your financial advisor only offers funds from their company, you are likely paying more than you need to and possibly getting a worse-performing financial instrument. It is a clear sign that their focus is to increase their bonuses and profits regardless of the costs you will have to bear.

V. They Try To Mask The Investment Returns

A financial advisor trying to rip you off can trick you into thinking that you are getting massive returns on your investment. Just because you see investment returns does not mean that you are doing well.

Financial markets are cyclical and go through periods of significant growth and decline. Even the poorest assets can look amazing during bull market environments.

The best way to determine whether you are getting the best bang for your buck is to compare the results with a similar benchmark. Suppose your financial advisor is confident enough to show you how the performance of your investments compares with equivalent benchmark indices.

In that case, they are likely trying to trick you into thinking a subpar performance is providing you decent returns.

Alternatives to Mutual Funds

Fortunately, there are far better methods to lower your investment expenses in Canada. Exchange-traded funds, index funds, and no-load funds are becoming increasingly popular in Canada.

You can also pay for low-cost management advice through Robo-Advisors in Canada which offers you significantly cheaper advice than traditional financial advisors.

Check out my guide on How to Start Investing in Canada if you want to invest but don’t know where to begin.

Conclusion

Mutual fund products have been falling out of favour among Canadian investors in recent years, and I hope this post gives you a better perspective on why that is happening.

Mutual fund fees in Canada are a rip-off for the most part, in my opinion. Financial advisors pushing these high-priced products are professionals you should be very weary of if you want to make the most of your investment capital.

Best next step

Keep exploring this topic

If you want to go deeper, these are the most useful follow-up pages and tools for this topic.

ETF hub

Browse ETF categories by goal

Jump into core, dividend, fixed-income, and sector ETF clusters from one place.

ETF tool

Use the Canadian ETF screener

Filter ETFs by yield, AUM, and performance when you are narrowing a shortlist.

Popular guide

Start with our top ETF roundup

Start with a broad ETF guide if you want a quick shortlist across the main fund categories.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.