Buying life insurance is one of the most selfless acts that you can do for your loved ones.

Millions of Canadians opt for life insurance for the financial security of their dependents in case something happens to them. About 58.5% of Canadians (22 million) own over $4.8 trillion in life insurance.

As a former life insurance advisor with over 80 clients, I’ve seen insurance payouts that keep families afloat when tragedy strikes.

In this PolicyAdvisor review, we will cover what it is, how it works, its strengths and weaknesses, and, hopefully, help you understand it better.

Online Life Insurance Quotes and Purchase

Comparison tool and search engine for life insurance, critical illness, mortgage insurance, and disability insurance.

Pros

- It’s completely free to get a quote

- Wide range of products.

- Advisors aren’t pushy (non-commission incentives).

- Easy application process.

- Compare similar products from 20 different companies.

Cons

- Only for Ontario, Alberta, BC, and Manitoba residents.

What is PolicyAdvisor?

At its core, PolicyAdvisor is a search engine and comparison tool for different life insurance available in the country. It’s similar to what Loanconnect is for personal loans. It’s a proprietary digital tool that helps you find the perfect life insurance based on your current situation, personal finances, and your insurance needs.

It can save you hours and hours of sitting with different insurance advisors and then comparing your options. It was created to simplify the insurance buying process for Canadians.

How PolicyAdvisor Works

PolicyAdvisor replaces the need to run an “apples-to-apples” comparison of multiple life insurance quotes in Canada manually and helps you choose the product that fits the bill for you. If the digital tool the company has created isn’t working for you, you can consult their licensed advisors over a call.

Once you have chosen the right policy (from one of the 25 insurance companies whose products PolicyAdvisor offers), you can submit your application with the insurance company through PolicyAdvisor’s website.

From another perspective, PolicyAdvisor is a digital life insurance agent with a significantly larger portfolio of products and companies. Since it’s independent, you can be relatively sure that it won’t push you towards a certain product.

It’s licensed to offer insurance brokerage services in Ontario, BC, Alberta, and Manitoba. And the best part is that it’s completely free. It makes money off of the insurance policies you buy through its website.

Features & Benefits

It’s important to understand that PolicyAdvisor, by itself, doesn’t offer any products. It’s a search and comparison tool that allows you to find the right insurance product for you.

It is more than just a quoting tool and operates as a broker. So the key features of the website are the different types of insurance policies they offer and their life insurance calculator.

Life Insurance

The basic/core insurance product that PolicyAdvisor helps you search is life insurance. The website clearly states that its primary focus is term policies, but it offers whole life insurance policies as well.

Once you complete a basic profile, you are provided with the lowest possible rates you qualify for.

The rates will depend upon your age, whether you smoke or not, and the amount you are aiming for as the insurance payout.

The process for non-medical, term life insurance is fairly simple. You can apply for the product you like directly from the website; the prices are exactly the same if you apply directly with the insurance provider.

Term insurance is perfect for individuals who carry a lot of debt (mortgage, student loan, etc.) and are in the process of paying it off. Premiums are low, and in case you don’t make it, the death benefit will help your family clear up your debt.

Whole Life Insurance

For whole life insurance, you have a relatively diverse range of policies, and the resulting product can be customized for your particular needs. The website also offers you to book/attend a session with their in-house professionals if you need guidance with your whole life insurance policy.

Other benefits of whole life insurance include fixed premiums for life, the option to access the cash value of your particular product (after you surrender your policy), a variety of riders to cover unconventional insurance needs, and tax-free growth.

This is especially suited for people who want to cover their funeral and other end-of-life expenses themselves and wish to transfer a sizeable chunk of their inheritance tax-deferred.

Critical Illness Insurance

Long-term critical illnesses have the power to turn your life upside down. Apart from health and lifestyle repercussions, critical illnesses can also be a significant drain on your financial resources. This product is designed specifically for individuals who want financial protection/help in case they are diagnosed with a critical illness.

Plans available on PolicyAdvisore cover 26 different illnesses, including cancer, heart attack, stroke, kidney failure, MS, and Alzheimer’s/dementia. Unlike life insurance that’s payable in the event of your death during your insurance period, critical illness insurance is payable when and if you are diagnosed with the disease.

You pay monthly premiums, and if the payout is triggered, you get a one-time lump-sum amount. You are not bound to use the money for treatment.

Mortgage Protection

Mortgage protection is insurance that pays off your outstanding mortgage in case you die without paying it off. It’s different from mortgage default insurance that’s mandatory for homeowners with down payments of less than 20%, and which protects the lender in case the borrower defaults.

Even though it’s sold as a separate product, it offers the same incentive as term insurance, i.e., a lump sum in the event of your death, and there are several reasons why it’s better to choose a term policy instead.

Disability Insurance

Instead of paying off a one-time lump sum, disability insurance pays the policy-holder monthly dividends, in case they lose their primary source of income due to a disability. The reasons for the disability can be a serious illness, mental illness, serious injury, or hospitalization.

It’s usually divided into two categories, short-term (from 6 to 26 weeks) or long-term disability insurance, which generally lasts up to two years, five years, or until you turn 65. Typically, it covers between 60% and 85% of your primary income.

Life Insurance Calculator

If you haven’t figured out how much insurance you need, there is a calculator to help you. It’s pretty neat and covers basics like your mortgage, children’s education, beneficiary support, etc. Given that the number it comes up with is based on averages, it can give you a baseline to work with.

There are several benefits of using PolicyAdvisor as your premier insurance policy research tool:

- You don’t need to run the numbers yourself.

- It replaces the time-intensive method of comparing different policies to find the cheapest/right one for you.

- You only get policies/plans from 16 of the best insurance providers.

- As independent insurance providers, their tools and advisors are unbiased.

- It’s free.

Travel Insurance

You can get quotes from over 30 companies for travel insurance at PolicyAdvisor, which keeps rates extremely competitive.

Key offerings include:

- Single Trip Insurance: This policy is ideal for one-time trips, providing coverage for medical emergencies, trip cancellations, and other unforeseen events. The policy duration can be customized according to the trip length.

- Multi-Trip Insurance: Designed for frequent travellers, this policy covers multiple trips within a specified period, typically a year. It offers similar benefits as single-trip insurance but with the added convenience of not having to purchase a new policy for each trip.

- Long-Term Travel Insurance: This policy is designed for travellers embarking on extended trips, such as gap years, working holidays, or long-term vacations. Coverage includes emergency medical treatment, trip interruption, and baggage loss.

- Group Travel Insurance: Ideal for groups of travellers, such as corporate teams or organized tours, this policy offers a cost-effective solution to protect multiple individuals under a single policy.

- Student Travel Insurance: Tailored for students studying abroad or international students studying in Canada, this policy covers medical expenses, trip cancellations, and other travel-related risks that may arise during their academic stay.

- Family Travel Insurance: This policy is designed to provide coverage for families travelling together, offering comprehensive protection for both adults and children.

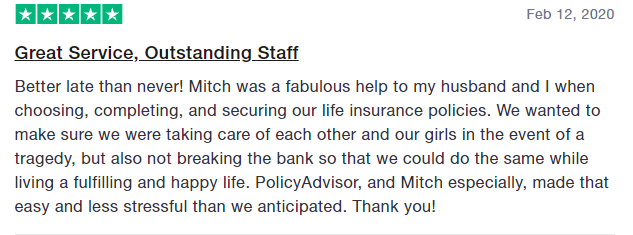

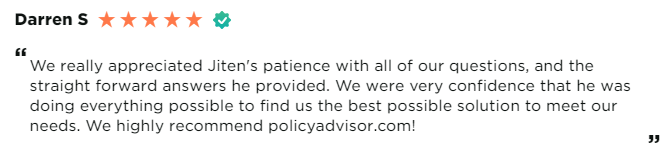

Social Proof

PolicyAdvisor has over 500 reviews on its Google business page with an average of 4.9/5.0. There’s also over 500 reviews on Reviews.io, with a 5/5 rating.

Some testimonials include:

The ratings are very similar on Trustpilot as well, where the website has a 4.8/5 rating with 38 reviews.

I wasn’t able to find a significant negative review or comment about the website/company that tells me they are either too good at fighting bad reviews or really good at their jobs.

Is PolicyAdvisor Safe and Legit?

The company is licensed to offer insurance brokerage services in Ontario, and it’s regulated by the Financial Services Regulatory Authority of Ontario (FRSA). It’s incorporated under the name PolicyAdvisor Brokerage (PAB) Inc.

Yes, PolicyAdvisor is safe to use and legit.

Alternatives

There are no true alternatives to Policyadvisor currently available. The next best thing might be ratehub.ca. You need to insert relevant details, and one of the agents from the company calls you for consultation.

Things to Consider Before Buying Life Insurance

It’s true that by life insurance, we generally mean that when we pass on, our loved ones are not left behind destitute. Even though money can never make up for human life, life insurance can ensure that death’s emotional pain doesn’t come with a major financial burden. That’s especially true if you have debt that will be passed on to your loved ones if anything happens to you.

But that’s not all that life insurance is for. Based on your chosen product, life insurance can also be a smart financial tool, i.e., an investment vehicle separate from your other savings and investments. There are insurance policies that you can borrow from (or against) if need be.

The two most common types of life insurance policies are:

Term Life Insurance

A term life insurance is where you pay a fixed premium for a set number of years, most commonly five or ten years. If you pass away within the policy duration, the insurance company will be an agreed-upon sum to your family (called a death benefit). If you outlive your insurance policy term and don’t renew or extend it, the insurance company gets to keep all your money.

Because of this business model, term life insurances are very cost-friendly, though they still depend upon the age you buy the policy in. For example, a typical 10-year term warranty that will pay $100,000 upon your death will cost about $16 a year (if you are a non-smoker, $31 if you are). That’s based upon typical term insurance rates in Canada.

$16 a month amounts to $1,920 for ten years. Once your term ends, you either forfeit your investment, extend your insurance for another decade (at higher premiums), or roll it into a whole-life insurance policy (if your term-insurance policy allows it).

Whole Life Insurance

As the name suggests, you typically pay a monthly premium for a whole life insurance policy until your last days (or a predetermined age). Upon your death, the insurance company will pay a set amount to your family. Premiums are significantly higher, but they remain the same for life, and you have limited control over the investments of your premiums (which accumulates tax-free returns to your beneficiary).

There are a few things you need to consider:

- Which insurance type is the best fit for you?

- Are you buying life insurance as a protection against unexpected death and family destitution or as an investment?

- How much can you afford to pay each month in premiums, and can you keep paying them in your low-income retirement days?

- How much will your family need to cover funeral costs, and to pay off your debt once you’ve passed away?

Not everyone may need a life insurance policy. If you don’t have any debt, and you are leaving a significant amount of assets for your loved ones (paid off house, investments, substantial sums), etc., life insurance may not be necessary for you. Your investments will be enough.

But if you are a young individual that is starting a family and have two kids and a mortgage, a decently valued term insurance might be imperative for you. So that your kids are taken care of (At least until they are 18), your mortgage and other debts can be paid off if you die unexpectedly.

Conclusion

If you are curious about life insurance, unsure about your current plan, or looking for life insurance for the first time, you may want to give PolicyAdvisor a try.

It’s a comprehensive digital tool that can help you find the perfect life insurance policy and much more, such as critical illness and disability.

Despite its morbid “triggers” (i.e., death and disabilities, etc.), life insurance is a very efficient way to provide for your loved ones.

Whether you are the primary breadwinner of your family or a loner who only wishes to cover its funeral expenses, there might be a life insurance product that’s the perfect fit for you. And PolicyAdvisor is a great tool for finding that product.

If you are curious about life insurance, unsure about your current plan, or looking for life insurance for the first time, you may want to give PolicyAdvisor a try, especially if you live in Ontario, where the website is licensed to sell life insurance products.

It’s a comprehensive digital tool that can help you find the perfect life insurance policy and much more, such as critical illness and disability.

You can check it out here.