Exploring the realm of online lending in Canada reveals Fairstone as a prominent alternative lender, offering a range of financial products tailored to meet various needs. Since its establishment in 1923, Fairstone has grown to provide a blend of both traditional and innovative lending solutions, positioning itself uniquely in the financial landscape. With a mission to fill the gap between conventional banking and payday loans, Fairstone’s offerings include unsecured personal loans, secured loans, mortgage refinancing, and more, aiming to cater to those who may not qualify for traditional bank loans.

Fairstone distinguishes itself with a diverse portfolio of loan products, including unsecured personal loans for those without collateral and secured loans leveraging assets like homes or cars for better interest rates. Their product range extends to mortgage refinancing options and specialized loans for car and auto purchases, reflecting their adaptability to various financial needs. With loan amounts varying from $500 to $50,000 and terms spanning from 6 to 120 months, Fairstone provides flexibility and accessibility, positioning itself as a reliable option for near-prime borrowers across Canada. The interest rates, while higher than some traditional banking options, offer a competitive alternative to payday loans, making Fairstone a viable choice for those looking to consolidate debt, manage unexpected expenses, or fund home improvement projects.

One of the critical advantages of Fairstone is its comprehensive approach to lending, offering both online and in-person application processes across its extensive network of branches. This dual-channel approach ensures accessibility and convenience for borrowers, allowing for personalized service and support. Fairstone’s commitment to transparency and customer support is evident in its straightforward application process, which includes online quotes that do not affect the applicant’s credit score and the opportunity for early loan repayment without penalties.

However, potential borrowers should exercise due diligence, as Fairstone’s interest rates can be substantial, especially for unsecured loans. While Fairstone provides a necessary service for those with limited borrowing options, it’s essential for applicants to carefully consider their ability to manage the loan terms and interest rates offered. Furthermore, the lender’s mixed reviews highlight the importance of customer service and the need for potential borrowers to weigh both the benefits and drawbacks of entering into a loan agreement with Fairstone.

Fairstone stands out as a significant player in Canada’s alternative lending market, offering a range of loan products designed to meet diverse financial needs. Its history, spanning nearly a century, underscores its resilience and commitment to serving Canadians. However, like any financial decision, obtaining a loan from Fairstone or any other lender should be approached with careful consideration of the terms, interest rates, and the borrower’s financial situation. For those exploring alternative lending options, Fairstone presents both opportunities and challenges, making it crucial for potential borrowers to thoroughly research and understand their options before proceeding.

Lazy to read? Here is a short summary, Fairstone offers a range of loans in Canada, catering to various credit profiles with quick application and funding, albeit with higher interest rates.

About Fairstone Financial

Since its inception in 1923, Fairstone Financial has carved out a niche as a premier alternative lending institution in Canada, bridging the gap between traditional banking solutions and payday lenders. Recognizing the diverse financial landscape, Fairstone offers an innovative approach to lending, tailored for individuals with fair to good credit profiles. With an extensive network of 235 locations nationwide, coupled with a dynamic online application platform, Fairstone ensures accessibility and convenience for Canadians seeking financial support. As a non-bank lender, Fairstone emphasizes flexibility and accessibility, aiming to provide personalized loan solutions that cater to the varied needs of Canadian borrowers.

Top Features of Fairstone Financial

Fairstone Financial stands out with its comprehensive range of loan products, offering unsecured personal loans up to $25,000 and secured loans reaching up to $50,000. This flexibility is further enriched with the availability of mortgage products, designed to meet the specific needs of homeowners. Fairstone’s loan repayment plans are tailored for a period of up to five years, featuring a variety of payment frequency options to suit different financial situations. A hallmark of Fairstone’s service is the ability to apply for a loan online, receiving a preliminary quote on loan amount and interest rate without the need for a hard credit check, thereby safeguarding applicants’ credit scores. Furthermore, Fairstone champions financial flexibility, allowing borrowers the option to repay loans early without incurring any penalties or fees. For those looking to benefit from lower interest rates, Fairstone offers the possibility to secure loans with assets, enhancing the affordability and accessibility of their financial products. Through these features, Fairstone underscores its commitment to providing versatile and consumer-friendly financial solutions, reinforcing its role as a key player in Canada’s alternative lending sector.

Types of Fairstone loans

Fairstone Financial has developed a diverse portfolio of loan products designed to cater to a wide range of financial needs across Canada, enhancing its status as a versatile and responsive lender in the alternative lending space. The offerings extend beyond traditional loan structures, providing personalized solutions to borrowers through a meticulously curated selection of loan categories.

Personal Loans

At the heart of Fairstone’s offerings lie its personal loan services, which are segmented into unsecured loans, secured loans, and specialized debt consolidation loans. Unsecured personal loans offer the flexibility of borrowing without the need for collateral, suitable for individuals looking for quick financial assistance without tangible assets. Secured loans, on the other hand, require an asset as collateral, such as a home or a vehicle, offering lower interest rates in return for the added security. The debt consolidation loans are designed for individuals aiming to streamline their financial obligations, allowing them to combine multiple debts into a single, more manageable loan with potentially lower overall interest rates.

Home Equity Loans

Fairstone’s home equity loans capitalize on the equity built up in a borrower’s home, providing a secured loan option that can be used for a variety of purposes, including home renovations, major purchases, or further investments. This category includes straightforward home equity loans, offering a lump sum at a fixed interest rate; second mortgages, which provide additional funding without disturbing the original mortgage setup; and mortgage refinancing options, which allow homeowners to adjust their mortgage terms to potentially lower their monthly payments or tap into their home equity for additional funds.

Retail Financing

In collaboration with leading retail partners, Fairstone offers retail financing solutions that enable consumers to make purchases directly in-store through a variety of point-of-sale financing options. This convenient service partners with well-known brands such as Best Buy, Timber Mart, and End of the Roll, among others, allowing customers to finance their purchases seamlessly at the time of sale. This type of financing is designed to make large or unexpected purchases more accessible by spreading the cost over time, making it easier for consumers to manage their budgets without compromising on their immediate needs or desires.

Additional Loan Services

Expanding its financial services further, Fairstone also provides car and auto loans, catering to individuals looking to purchase vehicles. With competitive rates and terms, these loans are designed to accommodate a range of credit profiles, ensuring accessibility for a broad spectrum of borrowers. Furthermore, online loans have been introduced to meet the digital age’s demand, offering an expedited application and funding process that can be completed from the comfort of the borrower’s home, emphasizing convenience and efficiency.

Through these varied loan categories, Fairstone Financial demonstrates its commitment to offering financial solutions that are accessible, flexible, and tailored to meet the unique needs of Canadians. Each loan type is structured with the consumer in mind, providing options that help bridge financial gaps, whether for personal use, home improvement, or retail purchases, thereby reinforcing Fairstone’s position as a comprehensive and consumer-friendly lender in the Canadian market.

Comparing Fairstone Loans: Unsecured Loans vs Secured Loans

| Feature | Unsecured Loans | Secured Loans |

|---|---|---|

| Collateral | No | Yes, usually a car or home |

| Loan amount | $500-$25,000 | $5,000-$50,000 |

| Interest rate (interest rates may vary by province) | 26.99%-39.99% | 19.99%-24.49% |

| Loan term | 6-60 months | 36-120 months |

| Payments | Fixed | Fixed |

| Fees | None | Some (depends on your province of residence) |

| Early repayment fees | None | Yes |

| Processing time | Less than one day | 3 or more days |

For more information on Fairstone’s loan options, visit Fairstone’s Official Website.

Fairstone Unsecured Loans

Fairstone’s unsecured loan offering stands as the primary gateway for borrowers without collateral to access funds. These loans depend on the borrower’s creditworthiness, which Fairstone evaluates based on credit score, income level, and other financial details. This form of lending allows for a quick and efficient way to secure funds for those who may not have, or prefer not to use, an asset as collateral. However, it’s important for potential borrowers to understand that the interest rates on these unsecured loans can be significantly higher compared to other lenders, such as Borrowell, making them a suitable option primarily for individuals with lower credit scores who might find it challenging to secure loans from more conventional sources.

Fairstone Secured Loans

As an alternative to unsecured loans, Fairstone provides secured loans, requiring an asset such as a vehicle or property to back the loan. This collateral reduces the lending risk for Fairstone, enabling the borrower to benefit from lower interest rates. Secured loans are an excellent option for those who have significant assets but perhaps do not have an optimal credit score. By offering something of value as security, borrowers can access more attractive loan terms. It’s noteworthy that, similar to unsecured loans, the interest rates are relatively high compared to industry averages, positioning Fairstone as an option for those who might not qualify for lower-cost lending alternatives.

Fairstone Mortgage Refinancing

Mortgage refinancing options at Fairstone offer homeowners the opportunity to adjust their current mortgage terms. By evaluating the borrower’s credit history, repayment capacity, and property value, Fairstone crafts refinancing solutions that can provide cash for home improvements, debt consolidation, or other significant financial needs. This option is particularly valuable for homeowners looking to leverage their property’s equity to consolidate debts under a potentially lower interest rate, thereby streamlining their financial obligations and improving cash flow.

Fairstone Second Mortgage Loans

Fairstone’s second mortgage loans allow homeowners to further leverage their property’s equity. Taking out a second mortgage with Fairstone can be a strategic move for those looking to reset their financial status, perhaps by consolidating high-interest debts or funding large projects that can increase the property’s value. It’s a viable path to accessing additional funds, with the secured nature of the loan typically ensuring more favorable interest rates than unsecured lending options, although it’s essential to compare these rates with those of other financial institutions.

How to Apply for a Fairstone Loan

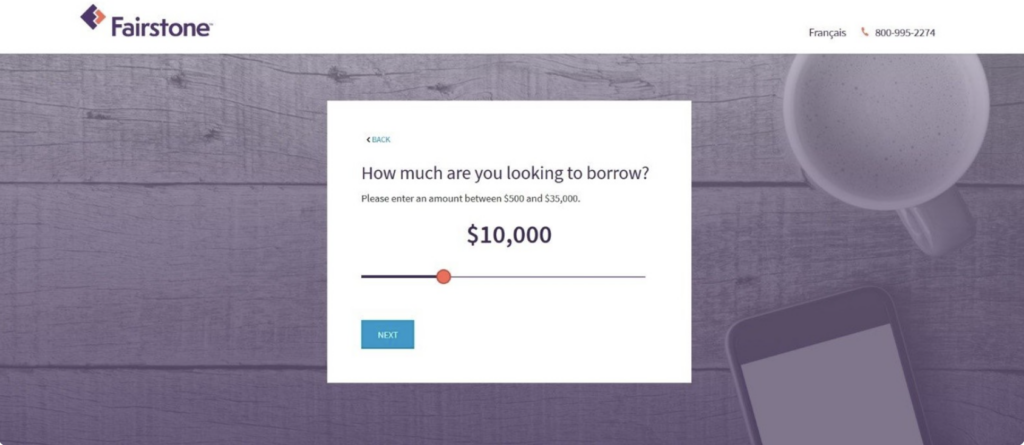

The application process for a Fairstone loan is designed with convenience in mind, available both through their extensive network of 235 branches across Canada and via an online platform. Opting for the online application process involves a straightforward questionnaire, estimated to take about 10 minutes to complete. This process is obligation-free, meaning applicants can see their loan options without committing to a loan and without impacting their credit score. Through the use of a sliding scale, applicants can specify the exact amount of funding they are seeking, tailoring the loan to meet their precise needs.

When considering applying for any Fairstone loan product, it’s crucial for potential borrowers to thoroughly review all terms and conditions, and possibly consult with a financial advisor. This ensures they are making informed decisions that align with their financial goals and capabilities. For more detailed information and to start the application process, visit Fairstone’s official website: Fairstone.ca.

You’ll be able to choose exactly the size of the loan you’re looking for using a sliding scale.

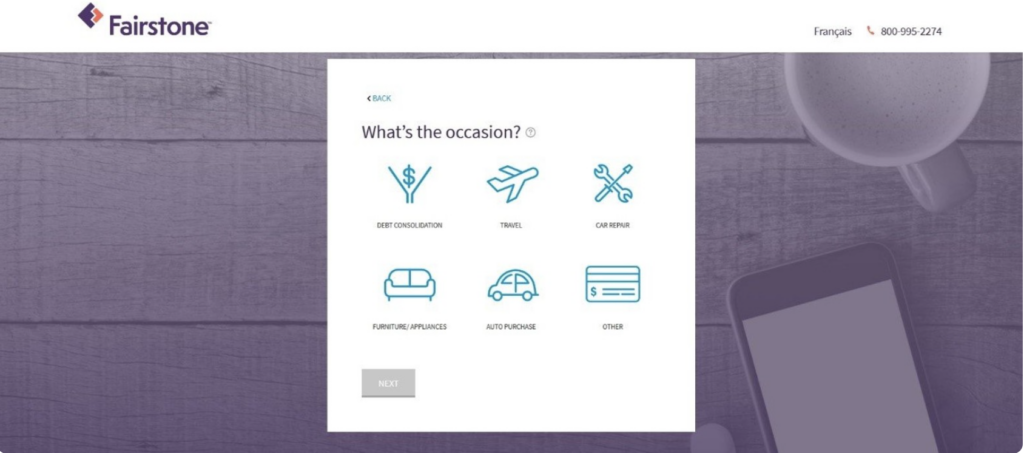

You’ll also be asked for the purpose of the loan. Fairstone says they use this information to customize your loan offer.

As you embark on the journey to secure financial assistance through Fairstone, the initial step involves providing comprehensive personal details to craft a tailored loan application. This intricate process ensures that Fairstone can accurately assess your financial situation and offer the most suitable loan options available to you.

Personal Information Collection

Your journey with Fairstone begins with the submission of a detailed application form that seeks essential personal and financial information. This includes:

- Your Full Name: As it appears on your government-issued identification, ensuring that your loan application is accurately tied to your legal identity.

- Your Date of Birth: To confirm you meet the age requirement for obtaining a loan, which is crucial for legal and regulatory compliance.

- Residential Address Details: Whether you are a homeowner or a renter, along with the duration of your residence at the current location, to establish stability and permanence.

- Monthly Housing Expenses: A breakdown of your rent or mortgage payments, along with any associated costs, provides insight into your financial obligations and helps in determining your loan affordability.

- Contact Information: Including a current phone number and email address, to maintain open lines of communication throughout the loan process.

- Income Verification: Details about your source of income, frequency, and amount, to assess your ability to repay the loan. This may include pay stubs, tax returns, or other documentation that verifies your income stream.

Application Review and Approval Process

Following the submission of your comprehensive application, a detailed review process ensues:

- Credit Score Check: With your consent, Fairstone conducts a soft credit inquiry. This is a non-invasive check that does not impact your credit score, designed to assess your creditworthiness without leaving a mark on your credit report.

- Application Processing: This step involves a thorough analysis of the information provided, which typically takes a few minutes. Fairstone’s sophisticated algorithms and experienced financial professionals work together to evaluate your application promptly.

- Loan Offer Review: Upon reaching the approval page, you are presented with a personalized loan offer. This offer includes detailed terms, such as the loan amount, interest rate, and repayment schedule. At this juncture, you are given clear instructions on how to accept the loan offer should it meet your financial needs and expectations.

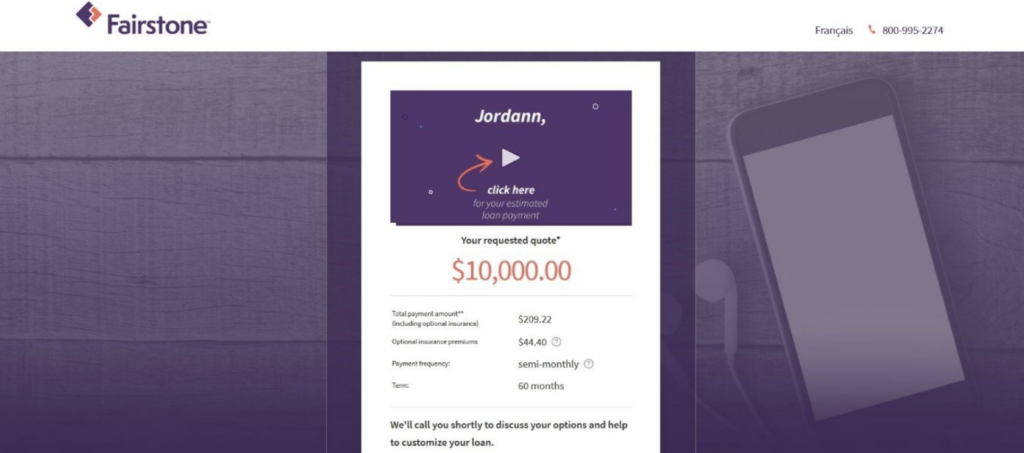

In my personal experience with the application process, I initially applied for a loan amount of $10,000 but was pleasantly surprised to receive a pre-approval for $20,000. This practice is not uncommon in the lending industry, as lenders often extend a higher credit offer based on their assessment of your financial health and repayment capacity. However, it’s crucial to borrow only what you need and can comfortably repay, to avoid overextending your financial commitments.

The entirety of this process underscores Fairstone’s commitment to providing a seamless, transparent, and user-friendly loan application experience. By meticulously gathering and analyzing your personal and financial information, Fairstone aims to offer loan solutions that are not only accessible but also aligned with your individual financial landscape.

Let’s delve deeper into the intricacies of the loan approval process and the financial components involved in obtaining a loan from Fairstone, highlighting the structured repayment plan, the impact of optional creditor insurance, and the variables affecting interest rates.

Understanding Your Loan Structure

Upon approval for a personal loan with Fairstone, borrowers might find themselves navigating a structured repayment plan meticulously designed to accommodate their financial capabilities. For instance, if a loan is approved with a bi-monthly payment scheme of $209.22, extending over a term of 60 months, this setup translates to a cumulative monthly cost of approximately $418.44. This repayment structure is carefully crafted to ensure manageability and consistency, aiding borrowers in aligning their financial planning with their loan obligations.

The Role of Optional Creditor Insurance

Included within this repayment framework is the consideration for optional creditor insurance, valued at $44.40 per payment. This insurance plays a pivotal role in providing a safety net for borrowers, offering coverage in the event of unforeseen circumstances such as job loss, disability, or death. While this insurance is not mandatory for securing a loan, it introduces an added layer of financial security, ensuring that borrowers or their families are not burdened by loan repayments during challenging times. Subtracting the cost of this insurance from the quoted bi-monthly payment, the core cost of borrowing is effectively reduced, highlighting the insurance’s impact on the overall loan cost.

Interest Rates and Their Influences

The interest rates associated with unsecured personal loans from Fairstone can peak at 39.99%, a figure that underscores the premium placed on unsecured borrowing. However, it’s crucial to recognize that the actual rate applied to a loan is the result of a confluence of factors, including the borrower’s creditworthiness, as reflected in their credit score, and the provincial regulations governing loan interest rates. This dynamic interest rate mechanism ensures that the rate is tailored to the borrower’s specific financial profile and the local legal framework, offering a personalized borrowing experience.

Additionally, the choice to include optional creditor insurance adjusts the monthly repayment amount, reflecting the cost of securing this financial safeguard. This option underscores the flexibility afforded to borrowers, allowing them to customize their loan terms to best fit their needs and financial planning strategies.

Expanding on Loan Approval and Management

When delving into the financial commitment entailed in securing a loan from Fairstone, it’s essential to explore beyond the surface-level numbers. The decision to opt for creditor insurance, while optional, merits consideration for its potential to offer peace of mind and financial stability in times of uncertainty. The comprehensive analysis of the interest rates, alongside the factors influencing these rates, offers borrowers a deeper understanding of the financial landscape of their loan, enabling informed decision-making and strategic financial planning.

Through a thorough examination of the loan structure, the optional creditor insurance, and the nuances of interest rate determination, borrowers are better equipped to navigate their financial journey with Fairstone, ensuring a balanced approach to loan management and repayment. This extended analysis not only sheds light on the immediate financial implications of securing a loan but also underscores the importance of strategic financial planning and risk management in achieving long-term financial well-being.

The table below illustrates how, according to the Fairstone personal loan calculator, your monthly payment for a 5-year, $5,000 loan can change depending on your location and credit score.

Monthly Loan Payments by Credit Score Across Provinces

| Province | Monthly Payment for a Fair Credit Score | Monthly Payment for a Good Credit Score | Monthly Payment for an Excellent Credit Score |

|---|---|---|---|

| British Columbia | $167 | $167 | $167 |

| Ontario | $188 | $185 | $182 |

| Alberta | $188 | $185 | $182 |

| Quebec | $177 | $177 | $177 |

What We Appreciate About Fairstone Financial

Versatile Loan Offerings

Fairstone Financial is noted for its wide array of loan products, including both secured and unsecured options. This versatility ensures that borrowers with varying financial needs and circumstances can find suitable solutions, whether they require large amounts for significant expenditures or smaller sums for immediate needs.

Streamlined Application Procedure

One of the standout features of Fairstone is its user-friendly application process. Prospective borrowers can navigate the procedure smoothly, with minimal paperwork and without the need for in-person visits, making it convenient for individuals with busy schedules or those who prefer online transactions.

Credit-Friendly Application

Another significant advantage of opting for Fairstone is the soft credit check involved in the application process. This approach means that inquiring about a loan does not negatively impact the applicant’s credit score, allowing for a stress-free exploration of potential financial options.

Areas for Improvement in Fairstone Financial

Elevated Interest Rates

While Fairstone offers financial solutions that bridge the gap between traditional banks and payday lenders, its interest rates are on the higher side. This aspect can be a drawback for individuals seeking cost-effective borrowing options, as the accumulated interest over time can significantly increase the total repayment amount.

Initial Loan Quote Transparency

The process for obtaining an initial loan quote could be more transparent. Potential borrowers might find it challenging to get detailed information about the interest rates upfront, which is crucial for making informed financial decisions.

Customer Service Experience

Feedback from the Better Business Bureau, where Fairstone holds a low rating, along with various online reviews, points to challenges in customer service. Enhancing the customer service experience could significantly improve borrower satisfaction and trust in Fairstone Financial.

Ideal Candidates for a Fairstone Loan

Individuals with Limited Borrowing Options

For those who find themselves unable to secure loans from traditional lenders due to stringent criteria or who have already utilized available credit without success, Fairstone offers a viable alternative. This is especially relevant for individuals in urgent need of financial assistance who have exhausted other avenues such as family loans or credit card options.

Fairstone can serve as a bridge for individuals facing immediate financial hurdles, enabling them to manage until a more stable financial situation is achieved. This option is particularly beneficial for those who have liquidated accessible assets but still find themselves short of funds.

Who Should Consider Alternatives

Individuals with Access to Prime Lending Options

Those who have maintained good credit scores and can avail of prime lending rates from traditional banks or other online lenders might find Fairstone’s offerings less appealing due to the higher interest rates.

Alternatives to High-Interest Loans

Exploring low-interest or balance transfer credit cards, personal loans from friends or family, or tapping into non-registered investments, RRSPs, or selling physical assets could offer more financially prudent solutions than opting for a high-interest loan.

Concluding Thoughts

Fairstone Financial emerges as a noteworthy option for individuals who have exhausted conventional borrowing avenues. It’s crucial, however, to thoroughly understand the financial implications, including interest rates and repayment terms, before proceeding. Analyzing your financial situation and considering all available options will ensure that you make the most informed decision possible.

How Fairstone compares to other lenders

We’ve compared Fairstone to two other lenders below to see how they stack up.

How Fairstone Compares to Other Lenders

| Province | Fairstone | Borrowell | Mogo |

|---|---|---|---|

| Loan amounts | $500 to $50,000 | Up to $35,000 | $300 to $35,000 |

| Term | 6 to 120 months | 3 or 5 years | 6 to 60 months |

| Interest rate | 19.99%-39.99% | 5.6%-29.9% | 9.9%-46.96% |

| Type of loan | Secured and unsecured | Unsecured | Unsecured loans (also offer lines of credit under different terms) |

| Early payoff penalties | No | No | No |

| Credit required | Fair/Good | Good | None |

In Canada, those in need of personal loans have a plethora of options beyond the conventional pathways provided by banks and credit unions. Among the various alternatives, Loans Canada stands out as a prominent choice for borrowers. Renowned for its stellar reputation, Loans Canada distinguishes itself by partnering with a diverse array of financial institutions, ensuring clients are matched with the lender best suited to their unique financial circumstances. This matchmaking service takes into account the varied needs and credit profiles of its clientele, providing a personalized approach to loan procurement.

Another viable option for individuals facing challenges securing loans due to less-than-ideal credit scores is Mogo. Mogo caters to a broad spectrum of borrowers, including those with poor credit histories, by offering online personal loans with interest rates that range from 9.9% to 46.96%. This range is achievable through a partnership with Lendful, another financial entity. It’s crucial for borrowers to recognize that the more attractive rates at the lower end of this spectrum are generally reserved for applicants boasting excellent credit. In contrast, those with lower credit scores might find themselves confronting the higher threshold of Mogo’s interest rate offerings. The impact of interest rate variances, even minor ones, cannot be understated, as they can significantly influence the overall cost of the loan through increased interest payments over time.

Comparing Fairstone Loans

Understanding the intricacies of loan agreements, especially the interplay between interest rates, repayment periods, and their collective impact on both monthly payments and the total interest paid over the loan’s duration, is crucial for borrowers. To illustrate, consider the scenario of securing a $15,000 loan through Fairstone in British Columbia at an interest rate of 31.99%. Evaluating this option across various repayment timelines showcases the significant influence of term length on both the monthly financial commitment and the cumulative interest charged throughout the loan’s lifespan.

Expanding on this analysis involves a detailed breakdown of repayment scenarios under Fairstone’s terms, juxtaposing them against alternatives offered by other lenders such as Loans Canada and Mogo. This comparison not only highlights the differences in financial obligations over time but also underscores the importance of meticulously reviewing loan terms, assessing personal financial capacity, and considering long-term implications on one’s financial health. Borrowers are encouraged to utilize online calculators and tools provided by lenders for a more personalized assessment, enabling informed decision-making tailored to their financial situations and objectives.

The Canadian personal loan landscape offers a variety of options suited to diverse financial needs and credit backgrounds. Whether through Loans Canada’s extensive network of lending partners, Mogo’s inclusive criteria for borrowers with varying credit scores, or Fairstone’s tailored loan solutions, individuals have the opportunity to explore and select the financial product that best aligns with their personal and financial goals. Prospective borrowers are advised to conduct thorough research, consider the full spectrum of available options, and meticulously plan their repayment strategy to ensure they choose the most appropriate and sustainable loan option.

How Fairstone Compares to Other Lenders

| Loan Term | Loan Amount | Interest Rate | Monthly Payment | Total Interest Paid |

|---|---|---|---|---|

| 1-year payback | $15,000 | 31.99% | $1,477.03 | $2,724.35 |

| 5-year payback | $15,000 | 31.99% | $503.79 | $15,227.67 |

| 10-year payback | $15,000 | 31.99% | $417.65 | $35,117.44 |

For detailed comparisons and more information, visit Fairstone’s Loan Comparison Page.

Bottom line on Fairstone Loans

Of the many options for the best personal loans in Canada, you should only consider Fairstone as an option after exhausting all other resources. The main reason you should hesitate to choose Fairstone is that the interest rates offered by this company are very high.

In the competitive landscape of personal loan providers in Canada, Fairstone emerges as a considerable option under specific circumstances. While it’s crucial to explore the myriad of lending solutions available across the market, Fairstone should ideally be approached with caution and considered primarily as a lender of last resort. The pivotal factor underpinning this recommendation lies in the notably high interest rates that Fairstone imposes on its loan products. Such elevated rates can significantly impact the overall cost of borrowing, making loans from Fairstone potentially less favorable compared to other financial institutions or lending platforms that might offer more competitive terms.

Before deciding on Fairstone, individuals should thoroughly investigate alternative sources for personal loans. This investigation should include a comprehensive review of offerings from traditional banks, credit unions, and other online lenders known for providing loans with lower interest rates and more favorable terms for borrowers. Engaging in this due diligence will ensure that individuals are making informed financial decisions, leveraging the best possible terms for their personal loan needs. It’s also advisable to consider consulting with financial advisors or using online loan comparison tools to gain a clearer understanding of the lending landscape and identify options that align more closely with one’s financial goals and capabilities.

Moreover, potential borrowers should take into account not only the interest rates but also other pertinent factors such as loan repayment terms, fees, and the lender’s customer service reputation. These elements collectively contribute to the overall borrowing experience and can influence the long-term financial impact of taking out a personal loan. Understanding the full scope of one’s loan agreement, including the implications of high interest rates on monthly payments and the total interest paid over the life of the loan, is crucial for maintaining financial stability and avoiding undue financial strain.

In essence, while Fairstone provides a valid solution for Canadians in search of personal loans, especially those who may not have access to traditional lending resources due to credit constraints, it’s imperative to approach this option with a strategic mindset. Carefully weighing the pros and cons of Fairstone’s loan offerings against those of other lenders will enable borrowers to secure the most advantageous financial arrangement, ensuring that their decision to borrow is both judicious and sustainable in the long term.

FAQ Section on Fairstone Financial Loans

Is it hard to get a loan from Fairstone?

Getting a loan from Fairstone can be considered less challenging compared to traditional banks, especially for those with fair to good credit scores. Fairstone caters to a wide range of credit profiles and offers both secured and unsecured loans. Applicants with lower credit scores might be eligible for secured loans, using assets like a car or home as collateral. The application process is straightforward, with the option to apply online or in person.

How much interest rate does Fairstone charge?

Fairstone’s interest rates vary depending on the loan type, your credit profile, and other factors. For unsecured personal loans, interest rates can range from 26.99% to 39.99%. Secured loans typically have lower interest rates, ranging from 19.99% to 23.99%. It’s important to get a personalized quote to understand the specific rate you would be offered.

How long does it take for Fairstone to deposit money?

Once a loan is approved, Fairstone is relatively quick in disbursing funds. For many loan types, the money can be deposited into your bank account as soon as the next business day following loan approval. The exact timing can depend on the verification process and the time of your loan approval.

What credit score is needed for Fairstone?

Fairstone does not strictly publicize a minimum credit score requirement, as they evaluate loan applications based on a variety of factors including income, employment, and credit history. However, a fair to good credit score (typically around 660 or higher) improves your chances of approval and may result in better loan terms. That said, Fairstone also considers applicants with lower scores, particularly for secured loans.

How long do Fairstone loans take?

The duration of Fairstone loans varies depending on the type of loan and your specific agreement. Personal loans from Fairstone can have terms from 6 to 60 months, while secured loans offer terms up to 120 months. The application process itself can be quick, with the possibility of receiving a decision shortly after submitting your application.

How much credit do you need to get approved for a loan?

The amount of credit you need for loan approval varies by lender and loan type. With Fairstone, there isn’t a publicly specified minimum credit score, as they consider various factors for loan approval. Generally, a higher credit score can increase your chances of approval and secure more favorable terms. For specific requirements and to assess your eligibility, it’s best to contact Fairstone directly or submit an application for a personalized assessment.

For more detailed information and to apply for a loan, visit Fairstone’s official website: Fairstone.