CIBC Investor's Edge

Transfer your investments to CIBC Investor's Edge and get rewarded with an offer of up to $3,000.

- ✓$6.95 flat-rate commissions

- ✓Backed by Big Five bank security

- ✓Transfer bonus offer up to $3,000

These days, people are becoming cautious of credit cards due to high-interest rates. Many want a way to make purchases without accumulating debt and significant fees. That’s where KOHO comes in.

As a prepaid card, KOHO allows you to control your spending and stay within budget. It’s straightforward, with no hidden fees, and the amount you save and spend is within your control.

If you’ve struggled with poor credit in the past and need a way to track your finances, the KOHO card could be a solid choice.

Want to learn more about KOHO? Read on as I explain the benefits of this prepaid card.

How Does KOHO Work?

After setting up an account online, you can fund your card via Interac e-Transfer or through payroll direct deposit with your employer.

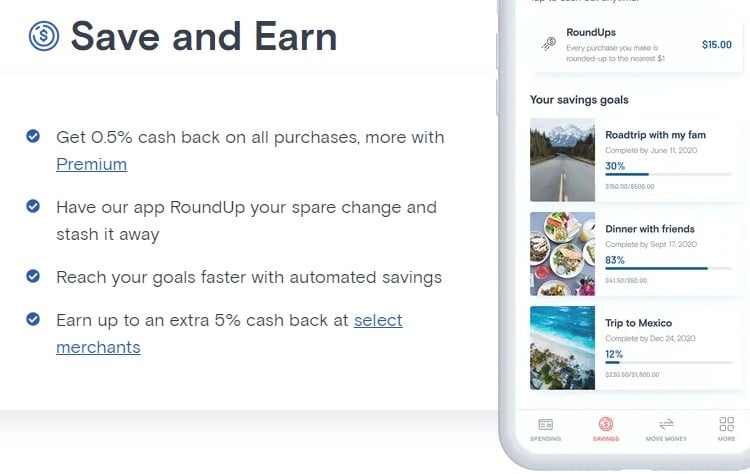

KOHO is accepted anywhere Mastercard is, allowing you to make purchases both online and in person. You can set savings goals and earn cashback on every purchase.

What Is So Good About KOHO?

KOHO enables customers to budget, spend, and save, all in one app. Unlike credit cards with high limits and interest rates, KOHO is a prepaid solution that helps users avoid debt traps.

The KOHO Essential Plan now offers 3.5% interest (previously 5%) on balances, while the KOHO Extra Plan offers 4% (previously 5%). The Everything Plan continues at 5%, providing the highest rate for those focused on maximizing their savings.

KOHO offers a cashback reward program and an optional RoundUP feature, where purchases are rounded up to the nearest dollar, and the extra is saved. By setting up direct deposit, you can also earn competitive interest rates, better than most traditional banks.

While KOHO is not a credit card and won’t improve your credit score directly, they offer a separate Credit Building feature for $7/month. This program reports your payment activity to major credit bureaus, helping build credit over time.

Other Features

KOHO integrates with Apple Pay, allowing you to make purchases without needing your card in hand.

KOHO integrates with Apple Pay, allowing you to make purchases without needing your card in hand.

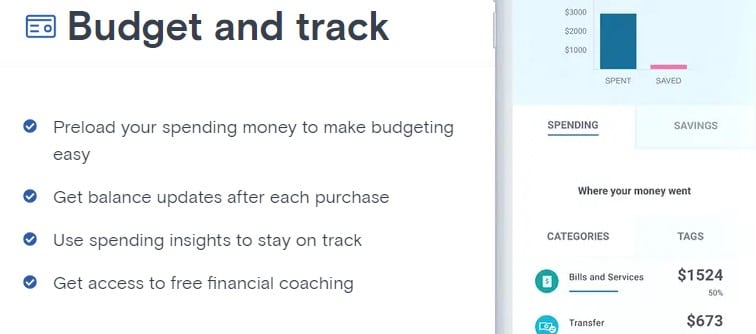

KOHO's financial coaching feature is a big plus for users, offering tools to create budgets, track spending in real-time, and receive tips on debt management and savings.

The KOHO Extra account (formerly KOHO Premium) charges $84 annually or $9 per month, giving users additional perks such as increased cashback rewards on transportation, grocery, and restaurant purchases, price match guarantees, and no foreign transaction fees.

Easy to Use App

The KOHO app is user-friendly, helping you manage payroll deposits, bank transfers, and bill payments. With easy access to your balance, savings goals, and budgets, it’s a helpful tool for managing your finances.

Customer service is accessible through in-app live chat, making it simple to get questions answered in real-time.

Is KOHO Trustworthy?

KOHO partners with Peoples Trust Company, a federally regulated institution and member of the Canada Deposit Insurance Corporation (CDIC), where deposits are generally insured up to $100,000.

KOHO is also backed by leading financial institutions, including Greyhound Capital and the National Bank of Canada.

Is KOHO a Good Idea?

KOHO’s reloadable prepaid card provides a balance of credit and debit card benefits, helping customers manage their spending without accumulating debt.

Understanding the Advantages and Disadvantages

One of KOHO’s main advantages is its no-fee spending and savings account. With no added fees or interest, it’s an affordable alternative to traditional banking options.

KOHO also offers cashback rewards. Through PowerUps, you can earn up to 2% cashback on select purchases, which adds up over time, especially for everyday expenses like groceries.

With its digital-first approach, KOHO is ideal for users who prefer online management over traditional banking. Budgeting tools allow you to set goals and track expenses in real-time.

However, KOHO may not be the best choice if you prefer in-person banking, as it’s primarily digital with support offered through the app or email. Additionally, the optional credit-building service costs between $7 to $10 per month, which may be a consideration for those looking to improve credit.

Frequently Asked Questions

How does KOHO make money?

KOHO earns revenue through interchange fees paid by merchants when you make transactions. They also offer a KOHO Extra account with additional benefits for a monthly fee, but they avoid high-interest charges or excessive fees

What is the point of KOHO?

KOHO’s goal is to offer a consumer-friendly alternative to traditional banking, allowing Canadians to control spending, avoid debt, and stay on budget. With features for saving, building credit, and earning interest, KOHO aims to promote financial wellness.

Final Thoughts - What is the catch with KOHO?

KOHO’s reloadable card offers transparency with no fees, cashback rewards, and tools to budget and track finances, making it a solid option for users focused on financial control.

If you’re looking for more options, check out these top virtual credit cards in Canada.

Best next step

Keep exploring this topic

If you want to go deeper, these are the most useful follow-up pages and tools for this topic.

Mortgage rates

Compare today’s mortgage rates

Move from mortgage education into current fixed and variable rate comparisons.

Mortgage tool

Run the mortgage calculator

Estimate payments and affordability before contacting a lender or broker.

Special case

Use the self-employed mortgage calculator

If your income is variable, use the calculator built for self-employed borrowers.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.