There might even be fraud on your account, or you might want to travel with the peace of mind of not being exposed to too much credit card fraud.

Are you in search of a better alternative to a regular credit card? You might have bad credit and can’t get a credit card, or you need something to help you shop without affecting your credit score.

KOHO Mastercard and the KOHO app are potential solutions for you.

Read this KOHO card review to learn whether it can genuinely offer you the advantages you’re looking for and help you meet your financial goals.

Prepaid Mastercard

- 1% Cashback on Groceries, Billing & Services

- 1.5% Foreign Exchange Transaction Fee

- Earn High-Interest Savings

- Credit Build Option

- No Credit Check Needed

- Accepted worldwide (wherever Mastercard is accepted)

- Choose your own card colour combination

- 1% cashback on groceries, billing & services

- Roundup your purchases and stash extra money away

- Zero-interest rates

- 3rd party e-transfers are available

- FX fees for free users

- Cannot handle every type of transaction

What is KOHO?

KOHO is a prepaid Mastercard launched in 2017 that you can use with its app available for both iOS and Android to manage your finances. You can load money onto your KOHO card and use the card to pay for anything that you would use on your Mastercard.

The KOHO card and app together is like a hybrid between a credit card and a debit card that is attached to a high-quality personal finance app.

KOHO Canada is not a bank, but it has partnered with Peoples Trust (a federally regulated company) and Mastercard to hold the funds you load onto your card.

KOHO Features And Benefits

There are several reasons why I think you should consider KOHO, including:

1% Cashback on groceries, billing & services

Using the services of a traditional bank does not reward you when you use your debit card. The concept of earning any cash-back rewards when you spend nothing more than your hard-earned cash is surprising but one that KOHO makes possible.

There is a 1% cashback on groceries, billing & services when you use your KOHO card. Each time you spend money in those categories, you can earn loyalty rewards without using a credit card.

You can even earn an additional 40% in cash back for using your KOHO card for Foodora orders. If you sign up for KOHO Premium services, your cash-back goes up to 2% for those categories.

Zero Monthly Fees

One thing I love about KOHO Canada is the lack of having to spend any money on banking charges. Canadians, on average, pay $220 for banking fees each year.

There are zero charges for using KOHO for your account, getting a new card, or a replacement card. You do not need to pay any fees for ATM withdrawals within the KOHO ATM network, electronic fund transfers, Interac e-Transfer, and much more.

With over 8,500 ATMs in KOHO Canada’s network, free ATM withdrawals are an easy option to leverage.

Automated Savings

One of the best things about KOHO Canada is that you can use its app to set savings goals and help you achieve them. For instance, if you want to save $2,000 to make a down payment for a new car six months away, the app will show you how much you need to save on a daily, weekly, or monthly basis.

It will debit the amount to your savings each day to help you reach that target. Additionally, it also has a fantastic savings strategy. Called the RoundUp, you can use the KOHO app to save money each time you make a purchase using the card. It can round up your expenses to the nearest $1, $5, or $10 and saves the difference.

This is quite similar to what Moka offers and is a handy savings strategy. For instance, if you buy a cup of coffee for $1.75, the app will automatically save $0.25 (if rounding up to the nearest $1), $3.25 (if rounding up to the nearest $5), or $8.25 (If rounding up to the nearest $10).

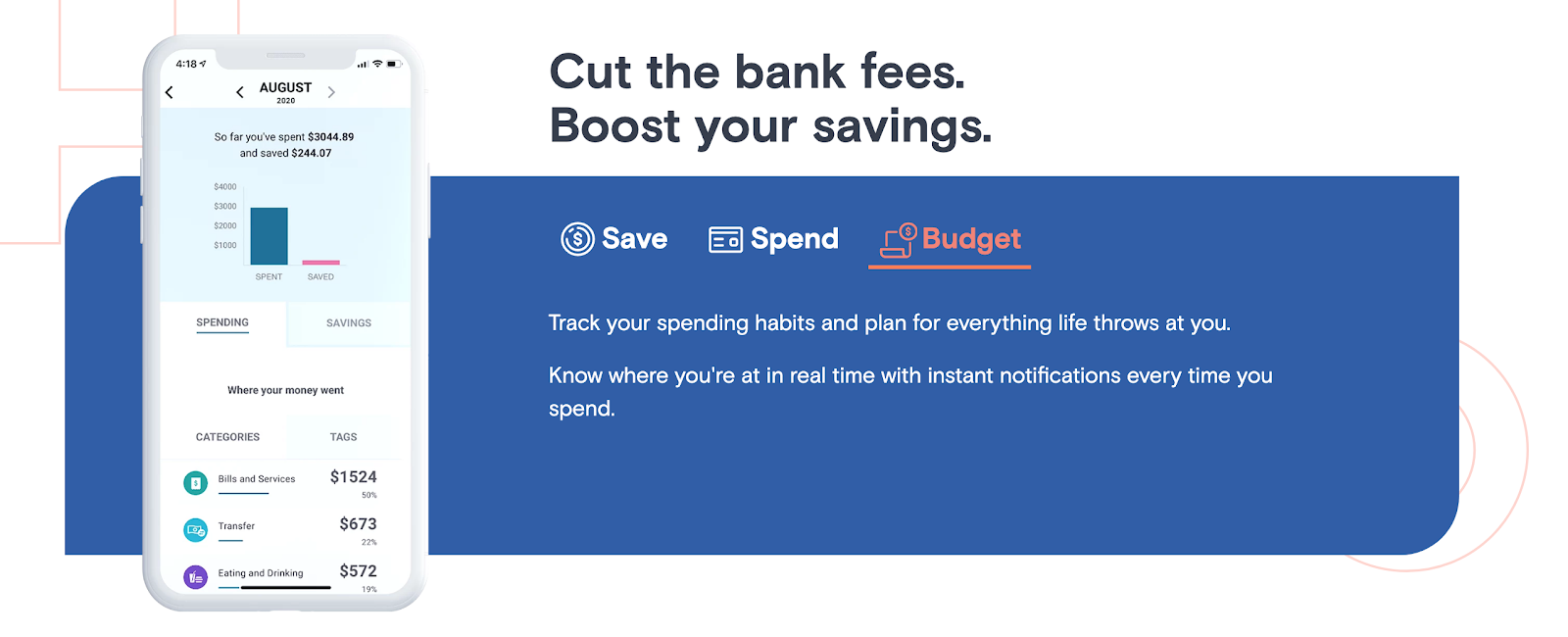

Real-Time Insights

You do not need to be in the dark about where you spent all your money. Many people wonder where all their money went when the end of the month approaches. KOHO helps you keep track by showing you the categories and how much you spent in each.

It also shows you how your spending compares to other KOHO users.

Having these facts in hand, you can tweak your budget and make crucial financial decisions to help you achieve the financial goals you have set for yourself.

Versatile App

The KOHO app is not simply a savings app. It allows you to achieve several tasks you might expect to use a bank for.

You can use this intuitive app to automate your bill payments, transfer money into any investment accounts you have, and even set up payroll deposits, along with much more.

Apple Pay Compatibility

You can also use your KOHO app with Apple Pay on any iOS device. All you need to do is add KOHO to your Apple wallet.

Whenever you shop in-store, you no longer need to bring your KOHO card. You can use your phone’s Apple Pay to access the funds you have loaded onto your KOHO app.

You might have questions regarding setting up KOHO in your Apple Wallet. Call them at 1-833-793-3372 or reach out for support through the app itself.

Financial Coaching

KOHO gives you access to free financial advice straight from the KOHO app when you have a direct payroll deposit setup.

If you want to know anything about debt, savings, budgeting, or investing, you can find all the answers right there in the app.

Referral Program

KOHO loves helping its customers and helping them help others. KOHO Canada has a generous referral program you can leverage to your benefit as well as the people you refer to KOHO.

Whenever you refer a friend to sign up to KOHO, both of you receive a bonus of 1% cash-back reward on all purchases for 90 days.

3rd Party E-Transfers

KOHO users can now accept Interac e-Transfers from friends, family, and business accounts to their KOHO accounts.

Similar to every other email transfer you’ve ever done, the third-party sender will send the e-Transfer to the user’s unique email address found in-app (ex. [email protected]). Steps to find this email address can be found here.

Does The KOHO Mastercard Build Credit?

Building your credit is important if you want to apply for a mortgage, auto loan, or business loan in the future. One of the best ways to build credit is to responsibly use your credit cards.

The traditional KOHO Mastercard does NOT help you build credit.

Even though you can use it like a credit card, it’s technically a prepaid debit card. This means that transactions and payments made to KOHO are not reported to any credit bureaus.

The upside of this is that you don’t need a good credit score (or any pre-existing credit, for that matter) to apply for a KOHO card. KOHO offers some of the same cash-back benefits of a traditional credit card without the credit liability.

Build Credit With KOHO’s New Credit-Building Feature

KOHO’s standard Mastercard is a simple prepaid card that offers cashback rewards. KOHO has launched a product that is designed to help you build your credit, though!

The KOHO credit-building feature is an easy and safe way to build credit, even if you have no credit or a poor credit score.

Here’s how it works:

- Open the KOHO app, click the ‘Credit’ tab, and then ‘Register.’

- KOHO will perform a soft credit check that shouldn’t impact your score and won’t show up on your credit history as an inquiry (hard inquiries can stay on your credit for up to two years).

- Once approved, KOHO will issue you a line of credit from one of their affiliated banks. This credit can’t be used or spent, and you won’t receive a separate credit card for it.

- Every month, you’ll pay $10 to KOHO for the service, which will help you “pay off” the “loan” that they gave you.

- Every time that you pay the $10 monthly fee on time, it will be reported to credit bureaus. This makes it look like you’re making monthly payments on a legitimate bank loan, which can boost your credit score and help you build good credit history.

KOHO’s credit-building feature isn’t like most credit cards or loans. You won’t actually have access or be able to spend the money, as KOHO technically holds the money for you. Your $10 monthly payment goes towards this balance.

The great thing about KOHO’s credit builder is that it’s hands-off and doesn’t require any effort on your part. Once you sign up and start making your monthly payments, just sit back and watch your score increase.

How Long Will It Take For My Credit Score To Improve After Using KOHO?

When you register for KOHO’s credit-building feature, your score probably won’t change at first. Your score may even drop by a couple of points, which is completely normal whenever you open a brand-new line of credit.

However, after a month or two of making successful payments, you should see a noticeable increase in your credit score. Some users may only see their score increase by 5 or 10 points, while others may get a 15 to 20-point boost or more.

Your credit score is determined by a number of different factors, so using KOHO’s credit builder isn’t necessarily the only thing contributing to your score.

The great thing about credit building with KOHO is that it’s good credit. The way that they set it up makes it easy to make payments and doesn’t involve any risk or liability on your end, since they’re not actually giving you spendable money.

Keep in mind that it depends on your total credit score behaviour. If you’re making other poor credit decisions such as missing credit card payments or defaulting on loans, your credit score could still drop.

KOHO Credit Builder vs. Secured Credit Cards

The main difference between KOHO’s credit builder and a secured credit card is that you’ll actually be able to spend the money that you have on a secured credit card.

That being said, secured credit cards often come with monthly or annual fees and usually involve a hard credit check.

Secured credit cards and KOHO credit builder are both safe, reliable ways to improve your low credit score. The main advantage of KOHO’s credit builder is that it’s super simple to apply for, doesn’t require money upfront (other than $10), and won’t ping your credit with a hard inquiry.

If you’re looking for an introductory credit card that will help you build your credit score, I recommend checking out one of these secured credit cards as well. These prepaid credit cards allow you to build credit, even if you have poor credit or no credit.

Koho Premium

KOHO is a free service that offers you all the fantastic features to help you reach your financial goals easily. Beyond its free features, KOHO added its premium service for those who want to take advantage of additional features, including and not limited to:

- No foreign currency transaction fees: Just like STACK’s Mastercard, KOHO Premium users can save the 2.5% to 3% FX fee that credit card providers typically charge them.

- 2% Cash-Back: KOHO Premium users can enjoy a 2% cash-back reward on their expenses on transportation, groceries, and while they are dining out.

- Price matching: KOHO Premium helps you get the best deals on anything you buy. If there is a better deal available anywhere, KOHO will credit your account with the cashback.

- Free Financial Coaching: When you sign up for KOHO PRemium, you can get incredibly helpful weekly tips and one-on-one coaching sessions for pressing financial queries without any additional cost.

- Higher Limits: You can take out a higher amount of $400 in an ATM per transaction of a maximum of $800 per day. You can have your account balance up to $40,000 instead of the $20,000 limit with the KOHO free account.

- KOHO Premium 30-Day Trial: KOHO Premium is free to use for 30 days after you sign up for it. It costs $9 each month you use it. If you sign up for a year-long package, you will pay $84 and save $24.

KOHO Fees

KOHO has two tiers: KOHO Regular and KOHO Premium. The structure for their fees varies from each other. I will go over both of them to help you get a better idea of what you can expect from KOHO fees.

KOHO Regular

- Annual Fee: $0

- Rewards: 0.5% Cash-Back on every purchase

- Foreign Exchange Fees: 1.5% (1% lower than typical FX fees)

- International ATM Withdrawal: $2 to $3 for each transaction

- Daily Transaction Limit: 15 transactions

- Account Balance Limit: $20,000

- ATM Withdrawal Limit: $300 per withdrawal and $600 per day

- Price Matching: No

- Free Financial Coaching: No

KOHO Premium

- Annual Fee: $84 with a 30-day free trial

- Rewards: 2% cash-back on groceries, eating, transportation, and drinking. 0.5% on everything else.

- Foreign Exchange Fees: 0%

- International ATM Withdrawal: 1 free transaction per month

- Daily Transaction Limit: 20 transactions

- Account Balance Limit: $40,000

- ATM Withdrawal Limit: $400 per transaction and $800 per day

- Price Matching: Yes

- Free Financial Coaching: Yes

KOHO Joint Accounts

KOHO also offers a free KOHO Joint Account and Prepaid Mastercard service for people who want to use its services with a friend, spouse, sibling, or roommate.

You can open a KOHO Joint Account without the need to visit any physical bank branch and complete any sophisticated forms. Each of the shared account holders gets a personal KOHO account along with the joint account. There are several benefits of using a KOHO Joint Account:

- A Joint Account reloadable prepaid Mastercard

- Expense tracking

- Real-time Joint updates and expense notifications

- Zero fees

- RoundUps

- Cashback

- Shares savings goals

- Free e-Transfers

- Privacy of personal account

- Free and instant KOHO-to-KOHO transfers

RBC Visa Debit Vs. KOHO Mastercard

KOHO Mastercard offers you the benefits of both a credit card and a debit card. The RBC Visa Debit card is something you might consider slightly comparable to the KOHO card in terms of features. RBC also operates on the Visa network to facilitate fast, easy, and secure transactions.

It is accepted at the same number of locations where your KOHO Mastercard will be accepted. It allows you to get cash at ATM machines where the Mastercard symbol is there.

The RBC Visa Debit card allows you to make payments online. There is no annual fee on the RBC Visa Debit card and no interest charges. If you use the RBC Visa Debit card to make purchases at local merchants, there are no additional charges.

The KOHO Card, on the other hand, offers you the same benefits along with much more, as discussed earlier in the review. Besides this, you do have to pay your fees to RBC for using its Visa Debit card. With KOHO Card, there is no underlying bank that you need to pay for its services.

KOHO Login And Register

You can sign up for KOHO here, and it is a convenient and straightforward process. All you need to do is go to their website or download the app and select the Get KOHO option to start.

Choose the type of KOHO account you want as you register yourself and log into your account once you have entered all the details.

FAQs

Here are answers to some of the most common questions people have regarding KOHO.

Is KOHO Safe?

KOHO partners with the Peoples Trust Company to hold your funds. The Vancouver-based bank is CDIC-insured, and that is a sign of a worry-free company you can trust to keep your funds safe.

In the event of fraud or theft, KOHO is not directly liable for your money. Instead, your case will be handled by representatives from the Peoples Trust Company (operating as the Peoples Group) since they’re the financial force backing KOHO.

Additionally, since KOHO is a Mastercard, it’s part of Mastercard’s network and is protected by the credit card processor’s zero liability protection policy. This provides further protection against credit card fraud and ensures you’ll never be held liable for fraudulent purchases.

What’s The Best Prepaid Credit Card In Canada?

There are several prepaid credit cards in Canada. KOHO happens to be the best among them:

- KOHO Prepaid Mastercard

- Scotiabank Prepaid Reloadable Visa

- CIBC Air Canada AC Conversion Visa Prepaid Card

- CIBC Smart Prepaid Visa

- Canada Post Prepaid Reloadable Visa

- Home Trust Secured Visa

- Refresh Financial Secured Visa

Is There A KOHO Bank?

KOHO is a fintech company. KOHO does not have any physical bank branch or underlying banking structure.

That being said, they are partnered with the Peoples Group, which is a large bank based out of Vancouver. This CDIC-insured bank acts as the primary holder for any funds that you deposit into your KOHO account.

How Can I Redeem My KOHO Cashback Rewards?

Once your purchases are settled (which can take up to three business days), your cashback rewards will be applied to your KOHO account. Your cashback will be automatically applied to increase your existing KOHO balance.

Most KOHO users keep their cashback rewards on their card balance and apply them to future purchases. However, you could also opt to withdraw the surplus amount by using your KOHO card at an ATM.

Does KOHO Offer Contactless Cards?

If you sign up for the KOHO Premium account, you’ll be issued one of the company’s high-end metal Mastercard. These cards are also equipped for contactless tapping payment, so you don’t have to worry about scratching your card up inside of card processing machines.

Does KOHO Work With Google Pay?

Yes. KOHO works just like any other major credit or debit card in your wallet. You can add your credit card number and information to your Google Pay or Samsung Pay wallet and use your phone to make contactless KOHO purchases wherever you go.

You Should Get KOHO Card If:

- You struggle when it comes to qualifying for a traditional credit card

- You want to manage your finances better.

- You need help budgeting.

- You need a better way to save more money.

- You need help in achieving specific financial goals.

- You want to consolidate your savings goals and credit card benefits

- You want an excellent prepaid travel card to help protect you from fraud

Don’t Get KOHO Card If:

- You plan to use it where Mastercard does not work

- You don’t want to pay FX fees while you continue using the free KOHO regular service (the premium card provides no FX fees)

Conclusion

Koho is a fantastic option for those who want to learn how to manage their finances better and to help with budgeting.

No matter what your credit score is, you can get a Koho card, make Mastercard purchases with it, and even collect cash back. Check out the Koho savings account, which gives you a decent interest rate on your money.

It looks like refresh financial is better, there limit is $200 to $10000 on their secured card, 17.99% interest, $3.00 monthly fee. Includes credit rebuilding, the amount you secure you dont touch, you pay off your balance in full monthly to avoid interest & build credit.

So monthly fees would be $3.00 plus $12.95 annual fee.

Its reported monthly to credit bureaus.

Thanks Linda, these are two pretty different products, as Koho is a prepaid card. Refresh is more similar to the Neo secured card.