Experts recommend saving for college when your child is young so your money has the opportunity to grow. Deciding where to put that money often makes all the difference.

Knowledge First RESP is a large government education savings plan, but is it one of the best places for your money?

Knowledge First has been embroiled in some controversial lawsuits, with many people wondering if it is a scam or if the company is legit.

After doing thorough research on the company, I’ve found that it does have some benefits but might not be the right fit for everyone.

I cover the controversy of Knowledge First and more below.

Government Education Savings Plan

Knowledge First helps you save money for college, all while being tax-free.

- Tax-deferred growth

- Eligible for government grant money

- High sales charges to pay upfront before any contributions get invested

- More fees than RESPs offered at other financial institutions

- Has a complicated legal history

About Knowledge First

Knowledge First is Canada’s largest registered education savings plan (RESP). The company’s been around since 1965 and manages over $7 billion in assets.

The company manages RESPs for more than 60,000 students planning for their higher education.

Knowledge First’s Complicated History

Group RESPs have recently been in the spotlight, but not in a good sense. The Heritage Group, another RESP, had its reputation tarnished because of customer complaints.

Several provincial security commissions also found significant deficiencies throughout the company.

In 2018, Knowledge First purchased the Heritage Group. The Toronto Star reported that the number of complaints after the sale decreased significantly.

However, that didn’t stop other troubles from following the company.

Knowledge First Financial Lawsuit

In March 2021, a class-action lawsuit was filed against Knowledge First and other group RESPs, alleging that sales charges and enrollment fees are unlawful and abusive.

Knowledge First responded in a press release that stated, “We pride ourselves on acting with integrity in all that we do and hold ourselves to the highest ethical and regulatory standards in order to better serve our customers.”

While the lawsuit is only limited to Quebec, it could provide a precedent for other provinces to file similar lawsuits. It could also allow security regulators across the country to review group RESPs fee structures.

Features and Benefits

While Knowledge First has had its share of issues over the years, many people still invest in group RESPs. Here’s what the company has to offer.

Plan Choices

Knowledge First includes plan choices from the Heritage Group and its own. The Flex First RESP plan allows families to pick how much they want to contribute and how often.

With this plan, you can set up a one-time contribution or an ongoing one – the flexibility makes it an attractive option.

The Family Single Student Plan (FSSP) is no longer available for new customers, but during the acquisition of the Heritage Group, those plans automatically transferred to an FSSP.

Tax Benefits

A huge benefit to a RESP is its tax savings. While you can’t deduct your contributions from your income, your gains made on the investment aren’t subject to capital gains tax.

When you withdraw the money, it’ll be taxed as income for the student. However, students tend to be in the low or no tax bracket, making the amount due on the small side.

Most students will also be able to offset the income against other education credits.

You can find yourself with a huge tax bill if you prematurely withdraw from the plan or close the account altogether.

At that point, you’ll forfeit any grants you received. In addition, you’ll need to pay tax on your gains, as well as a 20% penalty.

Government Grants

When you have an RESP, you’re eligible for government grants. More specifically, you can receive 20% of the first $2,500 you contribute annually. That’s $500 per year, up to the lifetime limit of $7,200.

There are additional grants available, many focused on low-income families, as well as specific provincial grants. Do your research ahead of time, so you know what to expect before opening an RESP.

Educational Uses

The money in your plan isn’t just for tuition. You can use it for room and board, books, transportation, and other expenses.

Universities, colleges, technical schools, and other post-secondary institutions all qualify for RESP fund usage.

Qualified programs need to be at least full or part-time, a minimum of three consecutive weeks in duration, and provide a minimum of 10 hours of instruction per week.

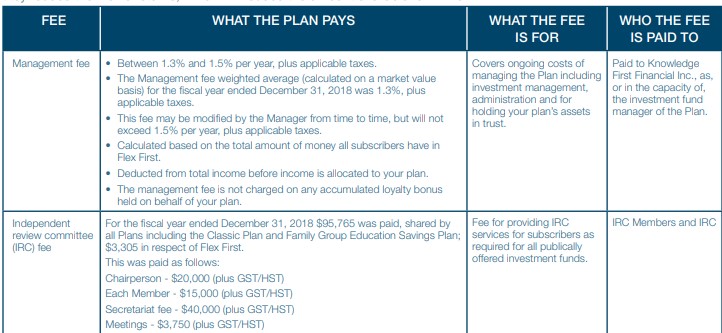

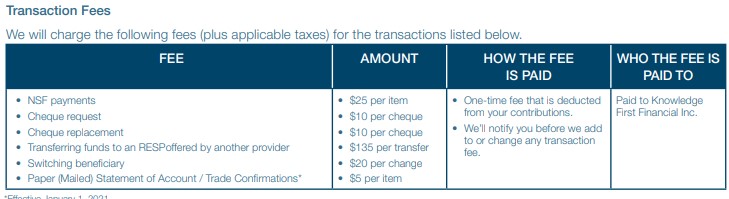

Sales Charges and Other Fees

The downside to Knowledge First’s RESP is its fees. The plan immediately charges a sales fee needed to pay your sales rep’s commission.

According to Knowledge First, all of your contributions go towards paying off that charge first, with 0% going towards investments.

In addition to the sales charge, there are other fees added by the company.

These fees could cut a big chunk out of your regular contributions and are part of the reason for the class action lawsuit against them.

Knowledge First vs Banks

Many big banks like Scotiabank, RBC, and TD offer RESPs for much lower prices than a private scholarship plan dealer like Knowledge First.

As stated above, Knowledge First will hit its customers with a large sales charge that gets paid upfront before investing any contributions. That’s not so with banks.

There aren’t usually any annual fees associated with opening a RESP at one of the financial institutions. However, you may have to pay certain investment fees when you buy or trade a stock or mutual fund.

Customer Reviews

One look at any website with user reviews, and you’ll see that Knowledge First isn’t a customer favourite. In fact, there are very few positive reviews out there about the company.

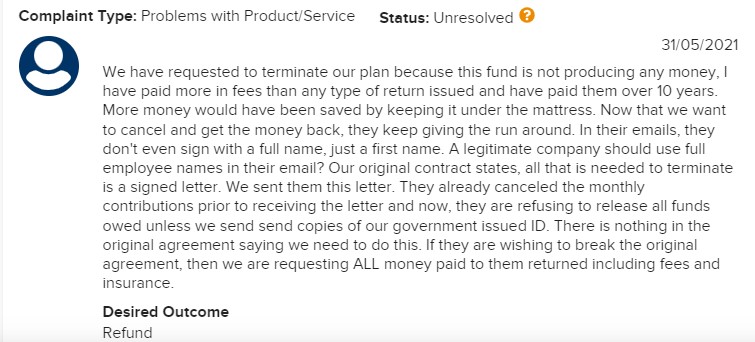

To get started, many users are furious that their plans have made little money after years of contributing. Most cite astronomical fees as the reason. One user even said they would’ve saved more money by “keeping it under the mattress.”

Other reviewers advise getting a RESP, just not a group RESP and not from Knowledge First.

There are testimonials on Knowledge First’s website, and most deal with their customer service and sales representatives. The reviewers seemed pleased with their experiences dealing with these experts.

So while their website gives gleaming reviews, other sites suggest that Knowledge First isn’t exactly a fan favourite.

Many reviewers find themselves aggravated by the company’s sales charges and its lack of investment growth.

Customers of the company said they had a hard time transferring or closing their accounts and lost a good chunk of their money in the process.

Is Knowledge First a Scam?

Knowledge First has been around for years and isn’t a scam. The issue many people seem to have with the company is the fee structure.

It’s typically higher than most banks, and customers have argued that the returns on their investments are lower than expected.

Conclusion

While Knowledge First can help you set money aside for college, the reviews for the company aren’t sparkling. I suggest doing your own research and learning about the company before investing.

If you want to learn more about the Heritage Group, the group RESP Knowledge First purchased, check out that story here.

I have been trying to transfer my funds to another financial institution for months now and KFF/Embark have only released 2/3’s of the funds. They keep throwing up roadblocks and are not easy to deal with. Still waiting for the rest of my money….

Not impressed, do not recommend them at all.

KFF and now embark has a big management fee/sales charge that is taken in the beginning of investment. I have two plans for my son. One started for regularly monthly contributions after he was born and another for annual contributions after he turned 7. And these should maximize the 50k max RESP contribution. When I decided to contribute more, I had to open a new plan. These plans are not flexible. They have charged almost 5k for both plans (not including insurance fees which is another ~$300). There is not much income earned and the government grants are the only things that offset the management/sales fee. This is also bad for financial investment 101 because you lose the compounding interest of the investment that is taken away from you at the beginning of the plan. Instead of you earning from that contribution, they use it to invest on them. If I had to redo this, I would invest in RESP in banks that has minimum fees but I already paid these with KFF and no point to transfer the RESP now. If only I knew better… They sell you the government grants and the potential income on contributions but hasn’t really done well on these incomes. But you still lose on the opportunity to generate more income from the big amount they charge on your first investments (<5k).

Thanks for sharing this, this sounds terrible!

I had the plan for my elder son. We paid to the plan 12000, received back 20000. I think it was a very good investment at the time. I also compared this to the banks, and I would not receive such money from them due to MER and other fees. Also, this company investing in the government bonds and other securities which are less risky, meaning it is way less likely you can lose your money. I don’t see any proof in this article of the company performing not well, except for angry comments from those who did not even matured the plan! When I signed the contract, I’ve been explained about all the fees and missing payments, so I knew exactly what was going to happen in case of cancellation or missing deposits. Also, the plan included death insurance for free, in case of death of any parent. Banks did not offer such option at all. Do your own research, talk to others, and do not trust this website to make your decision.

LIARS AND CROOKS! Sales rep looked me right in the eye and said upfront sales fee would be deducted if my son went to post-secondary. Then this suddenly changed a few years later. CROOKS!

In the first week after coming home from the hospital, I began to receive calls. The Heritage sales agent repeatedly contacted me after a nurse gave her my number so that she could sign up my son for the plan. Neither the company nor its plans were familiar to me. I signed up because of her persuasion. This is a HUGE misstep.

Big scammers. After my first son was born

I started receiving calls the first week I returned from the hospital. A nurse had shared my phone no with the Heritage sales representative and she called me numerous times wanting to visit me and sign my son up for the plan. I didn’t have any knowledge about the company nor these type of plans. she convinced me to sign up. BIG mistake. I could have saved more money on my own then with these people. their charges are outrageous

What kind of a company does these type of scams?

This is a horrible company. The returns are minimal and now that we are trying to get OUR money back, they are throwing up roadblocks at every turn. The people who answer the phone barely speak English and are unable to help. I wish I’d never heard of them. Invest with someone else!

i Noelle tayler has also been having this problem company ended up changing to embark… we still havent received our money back

Knowledge first is definitely a scam. Do not under any circumstances use this company. they told us all along right to the last invoice that there was ~26000 dollars in the account but when the kids took the money out the had about ~16000 available. we started paying in 2003 and had put in 14000 so we would have been further ahead just putting the money in their savings account. Again it may be a legal scam but it is 100% a scam.

It is not a scam!!!! The issue many people have is simply not taking the time to read and understand it, as they are all just focused on the end result but forget you must put work in it and have patience, but instead they expect everything to be done for them. Everything can be done efficiently and clearly understood without even calling a sales representative after you’ve signed up, it just requires a little it of an open mind to learn and understand, and a positive attitude.

My parents set up a Knowledge First account for me as soon as i was born and unlike banks, they only have ONE FOCUS which is on the children and ensuring we have money to peruse our dreams and goals after post secondary. Not only this, unlike any other financial group or bank Knowledge First is the only one to provide the most flexibility, as they understand not every family is the same, thus the accounts for everyone will differ, but always benefit. I am currently going into my second year of university and i would never have been able to achieve the piece of mind and amazing grants knowledge first helped me and my family reach.

it is a scam. We lost a lot of money when they transferred the existing heritage plan into a family single student plan. We have twins so we can compare and know the difference. The 1st twin graduated from university in 2022 so she was still in the heritage plan when she got the EAP fund in 2021 and the second twin took 1 year late so she will graduate in 2023 and her plan was changed by the company without our notice. When we applied EAP fund for the 2nd twin in 2022 and found out her fund amount is 50% off compared to her sibling.

Customer service of Knowledge First Financial told me our plan was changed so my daughter’s fund will be that amount. Once they changed we got 50% hair cut and maybe the second change will be another 50% cut again and again…..

You never know in the future what they will do to steal your children’s education money.