CIBC Investor's Edge

Transfer your investments to CIBC Investor's Edge and get rewarded with an offer of up to $3,000.

- ✓$6.95 flat-rate commissions

- ✓Backed by Big Five bank security

- ✓Transfer bonus offer up to $3,000

Planswell is a controversial financial planning company. The Toronto startup was forced to completely halt all operations in November 2019 due to a harassment claim from one of its employees.

The company lost $20 million in funding and was forced to declare bankruptcy. This Global News article contains details about the incident. This Betakit article also has a look into the situation, along with details about the company's financials before the bankruptcy claim.

The 2019 rise and fall at Planswell reminds me of this quote:

"It takes 20 years to build a reputation and five minutes to ruin it.” - Warren Buffett

Planswell has now picked up the pieces and started up again in 2020.

For this Planswell review, I’ll give my take on the financial planning service they provide, give details about what has changed with Planswell since relaunching and share some insight from my conversation with Planswell’s CEO.

[affiliatable id='26958']

Pros

Cons

What is Planswell?

Planswell, established by CEO Eric Arnold in 2016, is a Canadian fintech company that initially boasted a team of over 40 employees. Following a shutdown in late 2019 due to financial and internal challenges, the company was repurchased by Arnold and other partners. It relaunched in the first half of 2020 with a leaner team of fewer than 10 employees

Planswell entered the Canadian financial planning segment with a unique approach to differentiate itself from most of its peers. Its main selling point is its online software, where investors can fill out a relatively short survey and get a free financial plan.

How Does Planswell Work

Planswell's primary service is offering a free online financial plan to Canadians. To obtain your plan, simply:

-

Visit the Planswell website and click 'Start Now'.

-

Complete approximately 30-40 questions.

-

Verify your email. You'll gain access to your free financial plan shortly after these steps. Within 24 hours of completing the questionnaire, you'll receive a phone call from a Planswell advisor. This call provides an opportunity to discuss your financial plan and ask any questions you might have, all without the pressure of a sales pitch

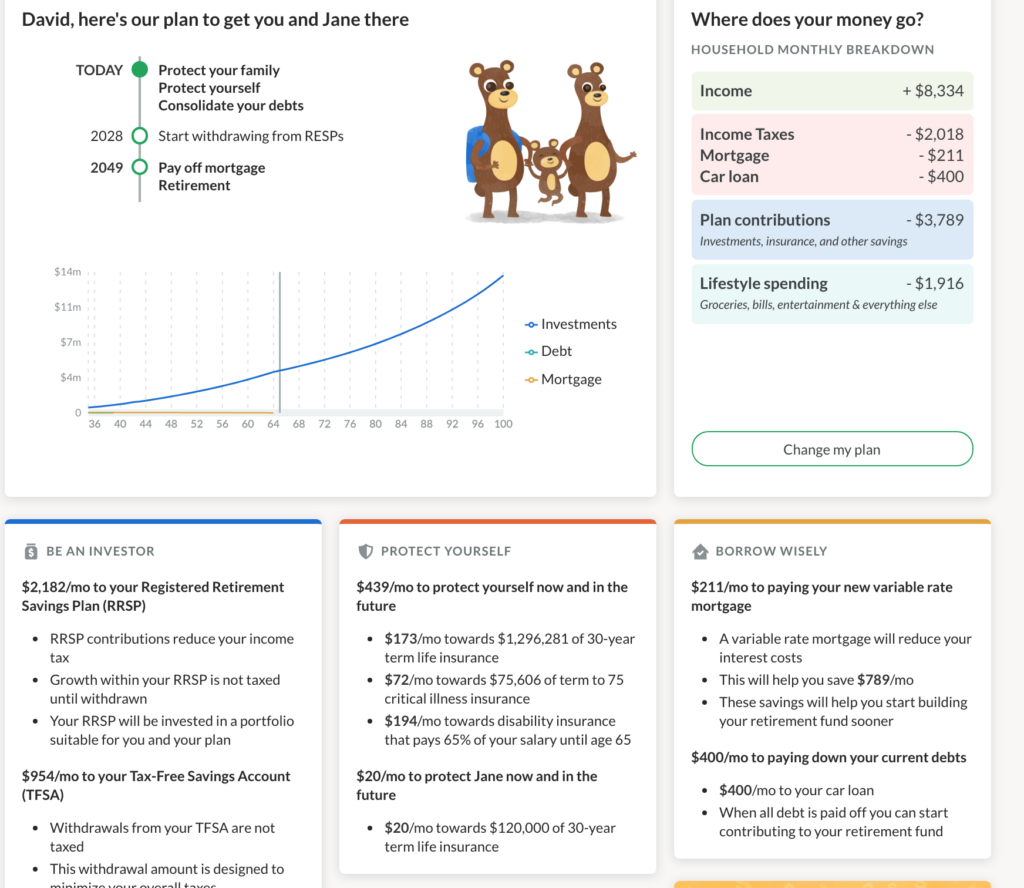

After signing up for the service, I took a look at the financial plan. I plugged in some fake data because I wanted to include everything, such as a spouse, children, mortgage, and loans, to see what the financial plan recommended. Here’s what the plan looks like:

I wouldn’t say it’s a full financial plan, it’s more like a financial cheat sheet or checklist. It gives you a birds-eye view of your current financial situation, with quick recommendations for investment accounts such as your RRSP, TFSA, and RESP if you have children, insurance, mortgages,

You have the option of just using this free financial plan forever. You can even get free human support from a licensed advisor, who will walk you through your plan. But they will likely try to have you sign up with one of Planswell’s advisors. I’ll go over this more in the next section.

Planswell Advisors

After its relaunch, Planswell significantly altered its business model. Whereas previously many services were managed in-house, including licensed insurance and mortgage operations with investments handled by Higgins Investment Group, Planswell now operates differently. Currently, Planswell collaborates with numerous advisors across various firms throughout Canada. When you engage with a Planswell advisor for investments, mortgages, or insurance, the specific terms, fees, and guidance will be directly dependent on the individual advisor assigned to you

It’s tough to do a review of the human financial planning services that Planswell provides because that will vary by each individual financial advisor. Planswell Investing, Planswell mortgages, and Planswell insurance will now all be dependent on the individual advisor, and whatever company they work for.

Planswell Fees

Accessing Planswell’s online financial plan and support remains free of charge. Should you choose to engage with a Planswell advisor for further services, the applicable fees will be set by the individual advisor. The fees for mortgages and insurance typically align with standard brokerage commissions, which are incorporated into the product pricing. As for investment fees, these vary by advisor but generally start at around 0.8% annually.

Example: For instance, if an advisor charges a management fee of 0.8% and you invest $100,000, the annual fee would be $800

How Does Planswell Make Money

Planswell generates revenue by charging a flat monthly fee to the financial advisors in its network. This fee grants advisors access to potential clients through the Planswell platform, functioning much like a lead generation service with additional planning tools. The fee also covers the use of Planswell's financial planning software, enabling advisors to offer more sophisticated services

Planswell Investment

The specific investments you're placed in through Planswell will vary depending on the advisor you're paired with. While it's common for financial advisors to recommend a variety of investment products, including potentially higher-cost mutual funds, many now also consider lower-cost options like ETFs or individual stocks, tailored to align with your financial goals and risk tolerance.

Planswell Insurance

After completing a financial plan with Planswell, you'll have the opportunity to explore insurance options tailored to your investment style and financial needs. Planswell's advisors can guide you on how different insurance plans might impact your current and future financial situation. Once your plan is finalized, you have the flexibility to connect with an insurance representative directly through Planswell or opt for an external provider, ensuring you get coverage that best suits your needs.

Planswell advisors should provide you with three types of insurance that you can choose from:

-

Disability insurance

-

Term-Life insurance

-

Critical illness insurance

All three can play a vital role in your financial plan. Most Canadians do not have insurance, according to a study conducted by investment firm Edward Jones. Not having the appropriate insurance in case you experience unforeseen life events can critically hamper your financial wellbeing.

Planswell Mortgages

When you fill the questionnaire provided by Planswell, you will also answer questions regarding your mortgage and other debt you may be carrying. Planswell collects the information and devises a strategy to help you pay down the high-interest debt you owe more quickly.

You will also get a mortgage plan appropriate for you based on your financial goals and situation. You can choose to apply for a mortgage using one of their advisors after that point, or take the information and use it yourself.

Safety and Security

Your personal information is stored and protected using bank-level encryption to ensure your privacy. BBS Securities Inc. is a third-party custodian that takes on the responsibility of storing your funds.

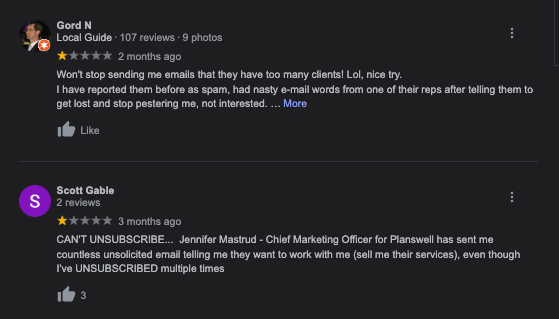

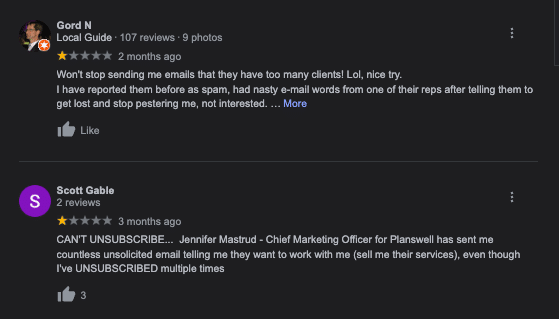

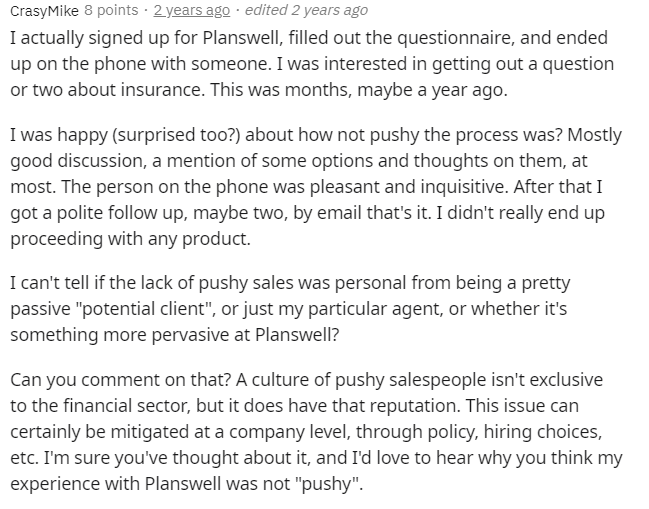

Social Proof

I scoured the internet to find reviews of customers who have been using Planswell for their financial planning needs. I found several positive reviews on Reddit and a few that were not so good. Google reviews show an overall score of 4.7 out of 5; however, if you look at the latest reviews, they are not flattering and seem to confirm my idea that Planswell has become an aggressive lead source for advisors:

The Good

The Canadian Investor Protection Find (CIPF) insures BBS Securities Inc. In case it goes bankrupt, BBS is also insured by Lloyd’s of London with coverage of up to $10 million per account.

This review is from someone who signed up for Planswell and did not end up using the insurance they were providing. What caught my attention was a lack of pushy sales pitches that you might usually expect with insurance providers. This was part of the Reddit AMA by the CEO of Planswell.

The Not So Good

One Reddit review on the not-so-good side was a client who did not have an outstanding initial experience, but her financial expertise managed to help her get good use from the robo-advisor.

I’d also like to point out that any reviews I could find were mostly from a year ago, before the company had to shut down and reopen. If they can maintain this level of customer satisfaction going forward, Planswell might have a good chance at recovery.

Financial Planning and Updates

Planswell has a more hands-on approach. After it helps you come up with a complete financial plan from your home’s comfort when you open an account, it takes things a step further.

Planswell reminds you to update your plan twice each year to make sure that the plan remains relevant to your financial needs as they change.

Planswell Alternatives

I wanted to compare Planswell traditional financial advisor investing with Canadian robo-advisors. Note that this is only for investing and not insurance and mortgages. Generally, robo-advisors should cost at least less than half the cost of a traditional financial advisor model that Planswell is providing. If you’re interested in investing for cheaper, you must look at robo-advisors also.

Planswell vs. Wealthsimple

Wealthsimple is the most popular robo-advisor product in Canada. It is among my favourites in the market. It provides you with an excellent combination of benefits, features, and low fees.

Read my full Wealthsimple Review here.

Planswell vs. Questwealth

Questwealth is among the latest entrants in the robo-advisor product market in Canada. Its parent company, Questrade, has been around in Canada for more than two decades, and it is not a newbie in the world of wealth management.

Questwealth came into the market with the increasing popularity of robo-advisors. It offers several benefits you can expect from robo-advisors, and it provides you with the option of choosing Socially Responsible Investment portfolios.

Read my full QuestWealth Review here.

Planswell vs. CI Direct Investing

CI Direct Investing (Formerly WealthBar) was the first robo-advisor to enter the market in Canada. Founded in 2013, its AUM grew to more than $225 million within five years. It offers a wide variety of accounts like Planswell and several features and benefits.

Read my full CI Direct Investing review here.

A Conversation With Eric Arnold, Planswell’s CEO

After I wrote my initial review, Planswell’s CEO Eric Arnold reached out to me. I had made an error in classifying Planswell as a robo-advisor. With its new business model of partnering with financial advisors, Planswell no longer even resembles a robo-advisor.

Eric also wanted to tell his side of the story of what happened during the company’s harassment controversy last year. He wanted to express that he was going to correct the culture going forward to make sure something like that would not happen again.

He also wanted me to consider not writing about what had happened since it is now a new company. I decided to include it because I believe you can’t tell the full Planswell story without detailing why it went bankrupt. I think it will pose a series of problems for Planswell going forward, and also some questions such as:

-

Can Planswell maintain the same level of customer satisfaction with much less staff on board now?

-

Can Planswell gain back the reputation it once had?

-

Will Planswell customers and clients be able to look past what happened with the bankruptcy and still trust the company with financial information?

-

Will the new corporate structure and business model be sustainable?

-

Will Planswell be able to receive funding if needed in the future?

All these questions are unanswered, and only time will tell if Planswell can recover from this and move on in the future.

Final Verdict - Planswell

The free financial plan that Planswell offers is an interesting service for Canadians and one that you might want to try out, but be aware that you stand a good chance of getting cold-called or emailed about signing up with an advisor.

But if you sign up for the paid version of Planswell, you will be signed up with a traditional financial planner with a standard fee, similar to walking into a bank and getting an advisor.

I used to be a financial advisor, and I just don’t think that the fees are worth it for most people. It’s a large amount to be spending on your investments every year and will eat into your returns.

Only if you need a complex financial plan and lots of human interaction would I recommend a traditional financial advisor, and even then, I would recommend only a fee-based one and not one that charges an annual fee.

So to summarize, I would say try out the free Planswell plan, but try to avoid signing up with a high-cost financial advisor.

If you’re willing to learn a little about investing, I would recommend going with a discount broker, which is the cheapest option. If you need advice, a robo-advisor will generally be much cheaper than a traditional advisor.

If you're starting out and you want to learn more, check out my how to start investing in Canada article.

FAQ: Planswell

What is Planswell? Planswell is a Canadian fintech company that provides free online financial planning services. It offers users personalized financial plans that include recommendations for investments, insurance, and mortgages based on user-provided information.

How does Planswell make money? Planswell operates by partnering with financial advisors across Canada and charges these advisors a flat monthly fee for access to potential clients. This model allows Planswell to offer financial planning services at no direct cost to the user.

Can I trust Planswell with my financial information? Yes, Planswell is licensed and regulated by the Financial Services Regulatory Authority of Ontario (FSRA) and adheres to strict data protection and privacy standards to safeguard your financial information.

How does Planswell's financial planning service work? To use Planswell’s financial planning service, you'll need to complete an online questionnaire on their website. This form collects information about your financial situation and goals. Once submitted, you'll receive a comprehensive financial plan that you can adjust as needed.

What types of insurance does Planswell offer? Planswell provides access to various types of insurance, including term-life, whole-life, critical illness, and disability insurance, ensuring a range of options to suit different needs and life stages.

Are there fees for using Planswell's service? The initial financial planning service provided by Planswell is free. However, if you choose to purchase financial products through their recommended advisors, standard fees for those services may apply, such as management fees for investments or commissions for insurance products.

Can I use Planswell if I'm not very knowledgeable about finances? Absolutely. Planswell is designed to be accessible for users with varying levels of financial knowledge. The platform offers straightforward guidance and support to help you understand your financial options and make informed decisions.

How do I update my financial plan with Planswell? You can update your financial plan by logging into your Planswell account and modifying your information or goals. Planswell also recommends updating your plan regularly to reflect any significant changes in your financial situation.

Is Planswell available outside of Canada? Currently, Planswell operates primarily in Ontario, BC, Alberta, and Manitoba within Canada. It is not available to users outside of these regions.

What should I do if I have more questions about Planswell? For more detailed inquiries or specific questions about your financial plan, you can contact Planswell directly through their website, where you can access live support or schedule a call with one of their licensed advisors.

Best next step

Keep exploring this topic

If you want to go deeper, these are the most useful follow-up pages and tools for this topic.

Stocks tool

Check Canadian stock movers

See the latest TSX and TSXV winners and losers before digging deeper into a sector.

Research hub

Browse Canadian stock research

Use the stock section to jump from a theme article into individual company pages.

Diversification

Compare stocks with ETF options

If you want exposure to a theme without single-stock risk, screen matching ETFs instead.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.