CIBC Investor's Edge

Get 200 free trades when you open an eligible CIBC Investor's Edge account with promo code EDGE2026.

- ✓200 free stock & ETF trades

- ✓Unlimited commission-free trades on 180+ select ETFs

- ✓Offer ends September 30, 2026

Robo-advisors help serve two primary investment goals for you; to save you money (with its low fees) and time (with its hands-off approach).

It's an exciting tech solution for the complicated task of investing.

I've taken apart over a dozen robo-advisors in Canada, peered closely at what's inside, and written detailed reviews on them. The results were surprising. Certain companies impressed me, and others were disappointing.

Here’s my in-depth guide to the best robo-advisors in Canada that should help you choose which one is right for you.

How to Choose the Best Robo-Advisor in Canada

As robo-advisor companies are relatively new and offer similar products, choosing the best one can get tricky. Here are the most important factors you should judge when choosing a robo-advisor in Canada.

1. Fees

Robo-advisor investing is usually a long-term commitment. That is why low fees are crucial in choosing a robo-advisor in Canada. A 0.2% fee difference per year might not seem like much.

But that small amount stretched out over a long time can add up to several thousands of lost dollars in fees.

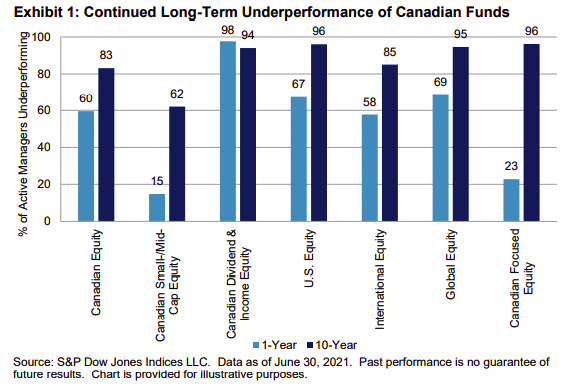

The main criticism against Canadian mutual fund companies in recent years has been the huge fees charged for active management, often over 2.0% per year.

As you can see from the chart below, the majority of actively managed funds underperform the market in Canada, in large part due to the excessive fees they charge.

The bottom line is that investment fees matter tremendously to your returns, which should also apply to robo-advisors. It's a big reason why I have BMO at a lower ranking in my robo-advisor rankings because its fees are so high, which should negatively impact returns in the long term.

Note that there are two types of fees to be aware of for robo-advisors:

-

Robo-Advisor Fee: The annual fees that the robo-advisor charges to manage your portfolio. (Ranges from 0.20% - 0.80%)

-

The Management Expense Ratio (MER): The fees that the exchange-traded funds (ETFs) charge. (Ranges from 0.10% - 0.25%)

2. Performance

Everyone is concerned with robo-advisor performance, but I want to caution against judging a company by its past returns. Robo-advisor performance is challenging to rank and predict between companies for the following reasons:

-

Many robo-advisor companies are relatively new, so you don't have much performance data to analyze.

-

It’s tough to compare apples to apples. Some robo-advisors have different methods of investing. For example, Questwealth is not a truly passive robo-advisor and uses active managers, and Nest Wealth has personalized portfolios for each investor, whereas Wealthsimple follows more of a traditional passive investment strategy.

-

Even if one robo-advisor has consistently outperformed another over the past few years does not mean it will continue to do so in the future.

-

Since all robo-advisors are investing in ETFs, it’s nearly impossible to predict which one will have the best performance in the future.

You can compare the asset selections and analyze the weightings to things like geography and market cap size of each robo-advisor company and see which one you like the most. But again, you can only gauge what you believe will have the best performance in the future, which is a tough forecast for anyone to make.

Here is where portfolio fees will come into play again. It’s the one factor that is predictable and controllable between robo-advisors. The lower the fees, the better the chances that the long-term performance of a robo-advisor will be comparatively higher.

3. Portfolio Selection

You have to make sure that the robo-advisor has a portfolio that is right for you, depending on what type of investor you are.

Example: After doing an investor questionnaire, David determines that he is an ultra-conservative investor and needs a 90% fixed-income portfolio. Some robo-advisors might not have the right portfolio for him.

Each robo-advisor has its own investor questionnaire that will place you in one of its categories. While they are mostly fine, you can go the extra mile and double-check this with a third party, such as with this free Vanguard Investor Questionnaire.

After you figure out what type of portfolio is right for you, check that the robo-advisors you are targeting will have something well-suited for you.

If you’re concerned about the ethics of investing in companies, you will also want to see if the company offers Socially Responsible Investing (SRI) options, but be aware they usually come at a higher cost.

4. Customer Service and Financial Advice

Whatever your preferred method of communication is, whether through phone, email or online live chat, you have to make sure that the robo-advisor you choose has that available.

Example: I prefer online live chat, so my robo-advisor provider must have this option.

Take advantage of the support helplines. Before choosing your robo-advisor, try emailing them for questions or calling them for advice before buying. See which ones get back to you the quickest or have the most helpful staff and support.

Best Robo-Advisors in Canada

1. Questwealth: Lowest Fees in Canada

Fees: 0.20% to 0.25%, plus 0.17% to 0.22% MER (0.37% - 0.47% total)

Wealthawesome Score: 9.8 / 10

Number of Portfolios: 5

Customer Support Channels: Phone, email, online live chat

How to Open an Account: Get $10,000 managed for free

Questwealth is the robo-advisor for Questrade, Canada's leading online broker. It was a close call between Questwealth and Wealthsimple for the number 1 spot, and you can't go wrong with either.

Where I feel Questwealth wins is on its shockingly low fees. At 0.20% - 0.25%, it’s about half or less than its main competitors! And while fees are not guaranteed to predict which robo-advisor will have the best performance in the long run, it is undoubtedly a huge factor to consider.

The incredible thing is that Questwealth somehow achieves this while having actively managed portfolios with dedicated portfolio managers. This means that they don't follow a set-and-forget passive ETF strategy that most robo-advisors do.

The main argument against active management is high fees, but if Questwealth can have people actively managing its funds at somehow half the price of other robo-advisors, fees of active management are not a negative point then.

Questwealth has a selection of five different portfolios, which is adequate to cover most investors' needs. I also love the fact that Questwealth has an online live chat, so I can communicate with them when I’m too busy to call and don’t want to wait for an email.

If you ever decide to become a DIY investor, Questwealth is owned by Questrade, Canada's most well-known trading platform, so that it would be an easy transition.

Pros

- Industry-leading low fees with active management

- Access to online live chat

- Offers Socially Responsible Investment (SRI) portfolios

- Free tax-loss harvesting

- First $10,000 managed free

- Affiliated with reputable Questrade brand

Cons

- Not everyone wants an actively managed portfolio

Read the full Questwealth review here

2. Wealthsimple Invest: Most Popular

[affiliatable id='26687']

Fees: 0.40% to 0.50%, plus 0.16% to 0.17% MER (0.56% - 0.67% total)

Wealthawesome Score: 9.6 / 10

Number of Portfolios: 3 main ones (excluding Halal and SRI)

Customer Support Channels: Phone, email, no live chat

How to Open an Account: Get a signup bonus here.

You might have seen some of Wealthsimple's clever commercials that feature well-known celebrities. This has helped propel the company to become the largest robo-advisor in Canada in terms of the number of customers and the size of assets. But aside from its flashy marketing, let's see what else makes Wealthsimple special.

With fees of 0.4% - 0.5% per year, Wealthsimple fees are average compared to its competitors. But where I feel that Wealthsimple outshines its competitors is its ease of use and its broad product offerings.

Investing should be made easy, and Wealthsimple lives up to its “simple” name. You can be set up and investing within minutes, and it has a friendly and trusted brand that will be enticing to beginner investors, which many robo-advisor investors are.

Wealthsimple also has the most impressive lineup of any other robo-advisor in the likelihood that you want other products. In addition to Wealthsimple Invest, the company has recently launched Wealthsimple Cash, which operates like a high-interest savings account, and Wealthsimple Crypto, where you can buy and sell cryptocurrency.

And if you ever decide to make the change to a DIY investor, the company also recently launched a zero-commission online broker platform called Wealthsimple Trade.

Having different products for evolving customer needs is important, as most people prefer to deal with one company and find it tedious to split up their services with multiple companies. Anything that makes investors' lives easier is a big plus.

Where I think Wealthsimple lacks is that it only has three main portfolios, a conservative, balanced, and growth portfolio. This will not be enough to cover a wide range of different investor types. Some people may see this as a benefit, though, as it keeps things simple.

Pros

- Broad product offering

- Well-known and trusted brand

- Easy to set up and start investing

- Acceptable fee structure

- First $10,000 managed free

Cons

- Only three main portfolios are available

- No online live chat is available

Read the full Wealthsimple Review here

3. Justwealth: Best Portfolio Choices

[affiliatable id='26953']

Fees: 0.40% - 0.50%, plus 0.20%-0.25% MER (0.60% to 0.75% total)

Wealthawesome Score: 9.3 / 10

Number of Portfolios: 70 Portfolios

Customer Support Channels: Phone, email, online live chat

How to open an account: Get up to a $500 signup bonus

Justwealth entered the robo-advisor space in Canada in 2015. If I were to sum up Justwealth in one word, it would be “choice.” If you ever find you don’t have a suitable portfolio choice at another robo-advisor, chances are Justwealth has you covered. With over 70 different ETF portfolios, you will find something that suits your risk profile.

Have a child? You can start a Registered Education Savings Plan (RESP) Target Date Portfolio. Want to invest in U.S. dollars? You can open a U.S. Dollar Portfolio.

There are also tax-efficient portfolios for your non-registered accounts and income portfolios for retirees. No other robo-advisor gives you this much choice with just its basic service.

After you fill out the initial online questionnaire, based on your response to its questions, it offers you a portfolio for you. If you have any questions, they have trained financial professionals to help walk you through this process and choose the right portfolio.

You’ll also get a dedicated portfolio manager for your account that you can call anytime. Financial planning is offered to all customers if you need to work out some financial goals you are trying to meet.

Pros

- Simple fee structure

- Many choices, with 70 different portfolio options

- USD investment accounts available for Canadians

- RESP option for parents

- Registered Portfolio Manager for each account

- Dedicated Financial Advisor

Cons

- $5,000 minimum account balance except for student, fresh grad, and RESP accounts

- If less than $12,000 in account balance will be charged a flat fee of $4.99/month

- No Socially Responsible Investment options

Read the full Justwealth review here

4. Nest Wealth: Best for High-Net-Worth Investors

Fees: $5, $20, $50, $100, or 150 a month, plus MER (0.13% for balanced)

Wealthawesome Score: 8.6 / 10

Number of Portfolios: Customized For Each Person

Customer Support Channels: Phone, email, no live chat

Nest Wealth has two big differences that set it apart from other robo-advisors. The first is its unique flat fee structure for different levels of investments, which can be confusing but is good for affluent investors. I’ll give an example of how much fees you will have to pay at each level of investment:

Example of Nest Wealth Fees: $10,000 invested = $300 / year in fees (3.00% annual fees) + MER

$50,000 invested = $300 / year in fees (0.60% annual fees) + MER

$75,000 invested = $600 / year in fees (0.80% annual fees) + MER

$149,000 invested = $600 / year in fees (0.40% annual fees) + MER

$150,000 invested = $1,200 / year in fees (0.80% annual fees) + MER

$325,000 invested = $1,800 / year in fees (0.55% annual fees) + MER

$1,000,000 invested = $1,800 / year in fees (0.18% annual fees) + MER

As you can see, if you have a large amount of money to invest in a robo-advisor, with its flat fee structure, Nest Wealth can't be beaten. But if you have less than $50,000 to invest, I wouldn't bother with Nest Wealth as the fees will be too high.

Nest Wealth also has a strange “trading” fee that other robo-advisors don’t seem to have, and that’s difficult to forecast ahead of time. The company has said it will cover the first $100 in trading fees per year, but it is possible to go over that amount.

Besides its fees, another difference about Nest Wealth is that it doesn’t have cookie-cutter portfolios and instead customizes it to your needs.

The benefit of this is that this approach could help satisfy your needs better than other robo-advisor companies. A downside of this is that it makes comparing portfolios to another robo-advisor difficult.

Nest Wealth is obviously targeting high-net-worth investors. If you don't have a large amount to invest, avoid Nest Wealth, but if you do, consider the company closely.

Pros

- Flat fee is great for wealthy investors

- Low MER fee of 0.13% for a balanced portfolio

- Customized portfolios for each individual investor

Cons

- No mobile version yet

- Most suitable for wealthy investors only

- May have to pay annual trading fees if over $100 per year

Read the full Nest Wealth review here

5. ModernAdvisor: Best Free Trial

Fees: 0.35% - 0.50%, plus 0.25% average MER (0.55% to 0.75% total)

Wealthawesome Score: 8.9 / 10

Number of Portfolios: 10 Risk Level Portfolios

Customer Support Channels: Phone, email, online live chat

ModernAdvisor is a Vancouver-based company and a fantastic choice for beginners for a couple of reasons. The first is that your first $10,000 is managed for free with the company.

This is a pretty common offer with robo-advisors. But what sets ModernAdvisor apart for beginners is its no-risk $1,000 trial period where you can earn real returns.

Example: Jason starts a free trial and invests $1,000 of ModernAdvisor’s “trial” money. At the end of the 30-day trial period, his investments are up 10% and are now worth $1,100. He decides to fund the real $1,000 with his own money and keeps the $100.

Example: Kathy starts a free trial and invests $1,000 of ModernAdvisor’s “trial” money. At the end of the 30-day trial period, her investments are down 5% and are now worth $950. She decides not to fund the $1,000 and doesn’t lose any of her money.

This free trial period is unique, and I haven't seen it offered by any other company. It's basically a free call option on your first $1,000. It's a neat entry point for those who are not sure about investing with robo-advisors.

You get to see how the whole robo-advisor process works without risking any of your own money, and yet you can reap all the gains and none of the losses when the 30-day trial is over. You'll get to see the daily shifts in your $1,000, and at the very least, you'll learn more about investing and ETFs.

I also like how ModernAdvisor has 10 different portfolios based on your risk profile. This is a large number of portfolios and should cover the majority of investors in Canada.

It's not just for beginner investors, either. The advisors at most robo-advisors generally give basic advice and aren't suitable for people who need complex financial advice.

However, with ModernAdvisor, you can pay an additional fee for a dedicated Certified Financial Planner (CFP) for your account, who can walk you through more complicated scenarios such as retirement, insurance, and mortgages.

Pros

- $1,000 free trial period funded by MoneyAdvisor is like a free no-risk call option for investors

- Adequate fee structure

- Have the option for paid premium financial advice for larger accounts

- First $10,000 managed free

Cons

- Average ETF MERs are high

Read the full ModernAdvisor review here

6. RBC InvestEase: Best Big Bank Robo-Advisor

Fees: 0.50%, plus 0.11%-0.13% MER (0.61% to 0.63% total)

Number of Portfolios: 2 - Standard Portfolio and Responsible Investing Portfolio

Customer Support Channels: Phone, email, online live chat

The Royal Bank of Canada (RBC) needs no introduction. As the largest bank in Canada, you’ll see one on every corner, probably next to a Tim Hortons.

Investing is about trust. For some people, few things in life are more intimate than trusting someone or some company with your money. Some people need that big brand recognition and the comfort of seeing bank branches on every corner. If that's the case with you, RBC InvestEase is a great choice for you.

It also has low fees for a big bank, especially its MERs. The standard portfolio is unique since it can be customized to whatever your specific risk tolerance and desired asset mix are.

7. CI Direct Investing (Formerly Wealthbar): Canada’s 1st Robo-Advisor

Fees: 0.35% - 0.60%, plus 0.19%-0.26% MER (0.54% to 0.86% total)

Wealthawesome Score: 8.0 / 10

Number of Portfolios: 5 Passive ETF Portfolios, 4 Active Private Portfolios

Customer Support Channels: Phone, email, online live chat

CI Direct Investing is the robo-advisor that started it all in Canada and has a unique approach to investing.

CI Direct Investing gives you the option for either five passively managed ETF portfolios. Where things get interesting are you can choose between four actively managed private portfolios that are managed by Nicola Wealth, a reputable investment management firm based out of Vancouver.

This will get you access to investments normally not available to the average investor, such as private equity or other alternative investments.

It comes at a cost, as CI Direct Investing management fees start out at 0.6% per year, plus the MER of the investments.

If you decide that it's worth it to get access to these private portfolios, CI Direct Investing can be a good choice for you, but I don't see it being worth it for the passively managed portfolios when there are other lower-cost options available.

Pros

- Access to private portfolios not normally available to investors

- First $5,000 managed for free

Cons

- Higher fees than most robo-advisors

Read the full CI Direct Investing review here

8. BMO Smartfolio: Excellent ETF Offerings

Fees: 0.40% - 0.70%, plus 0.25%-0.35% MER (0.65% to 1.05% total)

Number of Portfolios: 5 Portfolios

Customer Support Channels: Phone, email, online live chat

BMO is the big bank in Canada that has probably embraced ETF investing the most. They have a robust ETF lineup, which is being used by millions of Canadians. After you fill out an online questionnaire with BMO Smartfolio, they will place you into one of its five portfolios, all of which hold only BMO ETFs.

The one big downside to BMO Smartfolio is its pricing. With a 0.7% management fee for the first $100,000 invested and with very high ETF MERs, you will be paying more than the majority of robo-advisors if you invest with BMO Smartfolio.

If you need that big brand recognition and are ok with paying for it, then BMO Smartfolio can be a good choice for you. If not, choose a lower-priced but just as secure robo-advisor.

Pros

- Security and trust of a Big Five Canadian bank

- Great support options with live chat available

Cons

- Very high fees and ETF MERs could hurt your long-term returns.

Read the full BMO Smartfolio review here

9. QTrade Guided Portfolios

Fees: 0.35% - 0.60%, plus 0.15% MER (0.50% to 0.75% total)

Number of Portfolios: 6 Portfolios

Customer Support Channels: Phone, email.

Qtrade is better known for its trading platform, but it also has an excellent robo-advisor offering. It uses mostly Vanguard and iShares funds and there are socially responsible investing options.

There are six different portfolios to choose from, so you'll likely be able to find one that is suitable for your needs.

10. iA WealthAssist

Industrial Alliance is one of the largest insurance providers in Canada, and it has come out with a robo-advisor as well. The higher fees make it a tough choice to pick, which is why I have it at the bottom of this list.

Summary of top robo-advisors in Canada:

| Fees | MERs | Minimum Investments | Promos | |

|---|---|---|---|---|

| Questwealth | 0.20% to 0.25% | 0.17% to 0.22% | $1,000 | $10,000 Managed Free |

| Wealthsimple | 0.40% to 0.50% | 0.16% to 0.17% | None | $25 Signup Bonus |

| Justwealth | 0.40% to 0.50% | 0.20% to 0.25% | $5,000 | Up to $500 Signup Bonus |

| ModernAdvisor | 0.35% - 0.50% | 0.25% | $1,000 | |

| NestWealth | $5 - $150 per month | 0.13% | None | |

| BMO SmartFolio | 0.40% - 0.70% | 0.25%-0.35% | $1,000 | |

| CI Direct Investing | 0.35% - 0.60% | 0.19%-0.26% | None | |

| RBC InvestEase | 0.50% | 0.11% - 0.13% | None | |

| Qtrade Guided Portfolios | 0.35% - 0.60% | 0.15% | None | |

| iA WealthAssist | 0.50% | 0.20 - 0.30% | None |

Robo-Advisor ETF Investing Alternatives

Are robo-advisors right for you? It depends. Let’s go over some of the alternatives.

1. Robo-Advisors vs Do-It-Yourself (DIY) Investing

If you are willing to put in the time and effort to get educated on investing, you can build your own ETF portfolio using a discount broker. You won't have to pay any fees to a robo-advisor on your investments, so it will be the cheapest option. There are a couple of ways to build your own ETF portfolios:

-

Buy multiple ETFs that you will need to rebalance after some time to meet your desired asset mix. This is usually the cheapest way to build an ETF portfolio.

-

Buy an all-in-one ETF portfolio such as Vanguard VGRO or Vanguard VBAL that you won’t need to rebalance.

2. Robo-Advisor vs Mutual Funds

Essentially, mutual funds pool money from many investors to purchase a diversified portfolio of stocks, bonds, or other assets. The main drawbacks of mutual funds are:

-

High Fees: Mutual funds charge exorbitant management fees, which can limit potential returns over time

-

Underperformance: A significant number of actively managed funds fail to outperform their benchmark indices

-

Lack of Transparency: Some funds don't disclose holdings in real-time, leaving investors uncertain about their exact risk exposure

Mutual funds are generally much more expensive than robo-advisors, which should be a negative factor in the long run. I would choose a robo-advisor over mutual funds any day.

3. Robo-Advisors vs Traditional Financial Advisors

There are some traditional financial advisors that will offer ETF investing. But I would beware of this choice. First of all, they will almost certainly try to push you toward higher-priced mutual funds first.

Then, they will have to charge you a management fee for building your ETF portfolio, usually in the range of around 1% per year, unless you find a fee-based advisor. Robo-advisors are a much cheaper option than this.

I don’t recommend using a traditional financial advisor due to the high fees unless you really feel that you need the advice.

Robo-Advisors And TFSAs: How It Works

Tax-Free Savings Accounts (TFSAs) are easily the best investment vehicles that Canadians can use, as they're not subject to capital gains tax or any other type of income taxes.

Since the money you contribute to a TFSA is made with your post-tax dollars, your earnings are yours to keep.

Just make sure to stay within your annual and lifetime contribution limits, as outlined by the CRA.

Can Robo-Advisors Be Used For Registered Accounts?

Most leading robo-advisor platforms in Canada offer options to open and manage registered accounts, including TFSAs.

When setting up your account, you typically choose the kind of account you'd like to open, whether that be a non-registered account, a TFSA, an RRSP (Registered Retirement Savings Plan), or another registered account type.

The robo-advisor then curates a portfolio based on your risk tolerance, investment horizon, and other factors - the same as if you were opening a personal robo-advisor investment account.

How Are Taxes Calculated With TFSA Investments Made By A Robo-Advisor?

One of the many perks of investing with a TFSA is its tax-advantaged benefits.

Unlike other types of investment accounts, any income earned within a TFSA ( whether it be interest, dividends, or capital gains) is 100% tax-free.

When you invest in a TFSA through a robo-advisor, this tax advantage remains intact. The platform will manage your investments, rebalance your portfolio, and potentially make trades on your behalf.

However, all earnings within the TFSA will remain tax-free.

Conclusion

The crown for the best robo-advisor in Canada goes to Questwealth. Looking back on the factors I was using to judge robo-advisors, Questwealth comes out head and shoulders above every other competitor for the most important factor, which is fees.

The low fees should help impact it positively in terms of performance over the long term as compared to its competitors.

Along with the solid portfolio selection, the strong reputation with its parent company Questrade and the online live chat availability have helped raise Questwealth to my number one ranking.

Best next step

Keep exploring this topic

If you want to go deeper, these are the most useful follow-up pages and tools for this topic.

Stocks tool

Check Canadian stock movers

See the latest TSX and TSXV winners and losers before digging deeper into a sector.

Research hub

Browse Canadian stock research

Use the stock section to jump from a theme article into individual company pages.

Diversification

Compare stocks with ETF options

If you want exposure to a theme without single-stock risk, screen matching ETFs instead.

Advertisement

7 stocks to buy and hold forever

Proven winners for income investors — blue-chip dividend stocks to hold for decades.

Get the FREE Report

Christopher Liew, CFA, CFP®

Christopher is the founder of Blueprint Financial and a CTV News personal finance columnist. As a dual-designated CFA charterholder and Certified Financial Planner (CFP®), he helps Canadians reduce financial stress through clear, customized financial plans.

View Full Profile →✅ Reviewed by Certified Financial Professionals

This content has been reviewed by CFA® charterholders and Certified Financial Planners (CFP®) with over a decade of experience in Canadian financial markets. All information is fact-checked against official Canadian sources and regulations.

Why these credentials matter: CFA® charterholders complete 900+ hours of rigorous study in investment analysis and ethics. CFP® professionals are held to the highest standards of financial planning competency and fiduciary duty in Canada.

⚠️ Professional Disclaimer

This content is for educational purposes only and should not be considered personalized financial advice. While our team brings professional expertise, individual circumstances vary. For personalized guidance, consult with a qualified financial advisor, tax professional, or mortgage specialist.